For U.S. businesses and investors, foreign asset disclosure is a crucial component of tax compliance, yet it remains one of the most commonly overlooked areas. With the IRS increasingly focusing on FATCA and Form 8938, failing to disclose foreign assets can lead to significant penalties and legal complications.

Understanding these regulations is essential to safeguarding your financial and business interests.

This blog will walk you through everything you need to know about IRS foreign asset disclosure, including the intricacies of FATCA and the specific reporting requirements for assets held. Let’s get started.

A foreign financial asset refers to any financial asset held or maintained outside of the United States. These assets are key for accurate tax reporting and include various forms, such as:

The IRS requires U.S. taxpayers, including citizens, green card holders, residents, and business entities, to disclose foreign financial assets if they exceed the reporting thresholds. Form 8938 (Statement of Specified Foreign Financial Assets) helps track foreign financial assets and ensure compliance with tax obligations.

Also Read: IRS Wage Garnishment: How to Prevent and Fix It

Now that we understand what constitutes a foreign financial asset, let’s look at why reporting these assets is so important.

The IRS has significantly increased its efforts to identify unreported offshore assets due to concerns over tax evasion and money laundering. As part of this, FATCA and global tax treaties now require foreign banks to report U.S. account holders to the IRS.

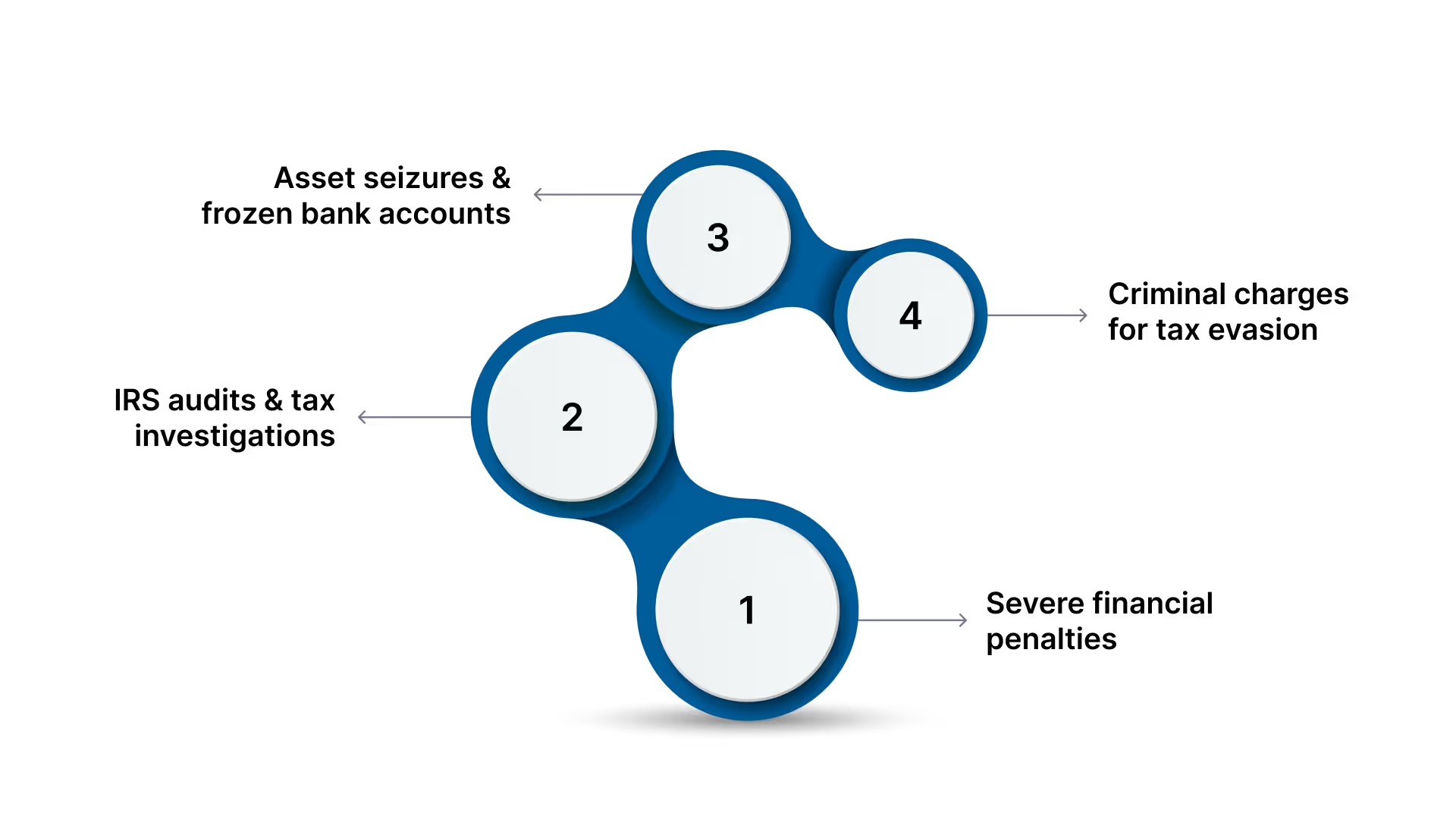

Failing to disclose foreign assets, such as bank accounts, real estate, or investments, can lead to serious consequences:

Staying compliant with foreign asset reporting requirements is essential to avoid these risks and prevent unwanted IRS scrutiny.

With the stakes clear, it’s essential to understand how IRS Form 8938 plays a key role in this process.

IRS Form 8938 is a critical tool in the U.S. government’s effort to curb tax evasion through foreign financial assets. While similar to the FBAR (FinCEN Form 114), Form 8938 has distinct reporting requirements and thresholds.

This form, part of the Foreign Account Tax Compliance Act (FATCA), ensures U.S. taxpayers disclose their foreign financial holdings to the IRS.

You must file Form 8938 if you are a specified individual or a specified domestic entity that holds foreign financial assets exceeding the IRS’s reporting thresholds.

The IRS defines specific reporting thresholds based on your filing status and residence. These thresholds determine when Form 8938 is required.

Accurate reporting on IRS Form 8938 ensures compliance with U.S. tax laws and provides transparency regarding foreign financial assets.

In addition to Form 8938, U.S. taxpayers may be required to file additional forms to report foreign assets such as trusts, business interests, and ownership in foreign corporations.

Staying on top of these additional reporting requirements ensures full compliance with U.S. tax laws and helps avoid complications with foreign asset holdings.

Also Read: IRS First-Time Penalty Abatement: Key Insights and Tactics for US Businesses

Next, let’s examine some situations where you might be exempt from this requirement.

While many U.S. taxpayers with foreign financial assets are required to file Form 8938, there are some notable exceptions to consider:

However, even if you're exempt from filing Form 8938, other forms like the FBAR (FinCEN Form 114) may still be required to report foreign financial assets.

To avoid confusion, let’s compare the key differences between Form 8938 and FBAR filing.

Many taxpayers confuse Form 8938 with the FBAR. Both deal with foreign financial assets, but the rules, thresholds, and filing processes differ.

Form 8938 captures a broader set of foreign assets and requires more detailed reporting, as it is part of the annual tax return. FBAR focuses only on foreign accounts, carries its own filing process, and applies even when the tax return is not required.

Note: Taxpayers meeting both thresholds must file both forms and ensure the same accounts are consistently reported.

Also Read: Understanding Schedule K-1 Tax Form 1065

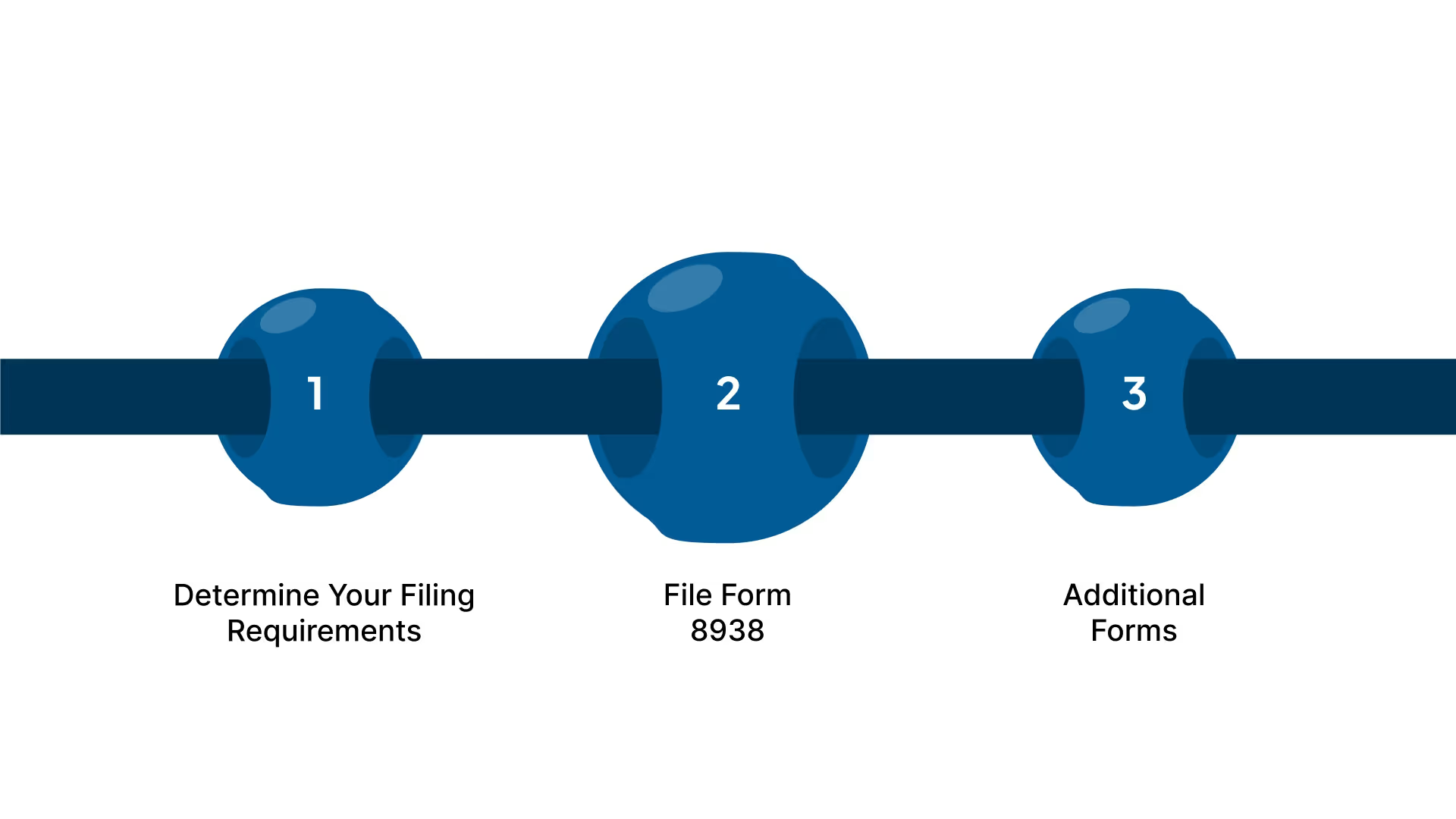

Once you know which forms to file, here's how you can go about reporting your foreign assets correctly.

Reporting foreign assets is a critical step in ensuring compliance with U.S. tax and financial disclosure regulations. Here’s a streamlined guide for U.S. taxpayers on how to report foreign financial assets:

Not all U.S. taxpayers must report foreign assets. If the combined value of your foreign financial accounts exceeds $10,000 at any point during the year, you must file FinCEN Form 114, the Report of Foreign Bank and Financial Accounts (FBAR). This is filed electronically with FinCEN, not the IRS.

If your foreign assets meet specific thresholds, you must file Form 8938, the Statement of Specified Foreign Financial Assets, with your tax return (usually Form 1040). This provides more details on your foreign financial assets.

Any income earned from your foreign assets, such as interest, dividends, or rental income, must also be reported on your U.S. tax return.

Depending on your situation, other forms may be required. For instance, Form 5471 is needed for foreign corporations, while Form 3520 or 3520-A may be required for foreign trusts. It's essential to keep accurate records of all your foreign assets and transactions. This will support your filing in case of an audit.

Taxpayers living abroad typically use Form 1040, but may need additional forms such as Form 2555 (Foreign Earned Income Exclusion) or Form 1116 (Foreign Tax Credit). Always refer to the latest IRS guidelines to ensure compliance.

Also Read: Outsourced Tax Services to India: A Guide for US Companies

You’ll need records of your foreign accounts, investments, and other assets, including the maximum value of each asset during the year.

For foreign accounts, use the highest value during the year. For other assets, use their fair market value at year-end, converting values to U.S. dollars at the year’s closing exchange rate.

Foreign real estate is not typically reported unless it's held through an entity or generates income, such as rental income. Review IRS guidelines for specific real estate reporting rules.

FATCA requires U.S. taxpayers to disclose their foreign assets and mandates that foreign financial institutions report U.S. account holders to the IRS. This law helps the IRS detect and prevent tax evasion related to foreign accounts.

If you hold foreign assets, FATCA may impose additional reporting obligations on both you and the foreign financial institutions holding your assets. Accountants assisting clients with foreign assets should be familiar with FATCA’s implications, ensuring that all assets are properly reported and that clients are aware of their obligations.

Missing a foreign asset disclosure deadline or making errors can lead to costly penalties. VJM Global specializes in helping U.S. businesses and investors manage the complexities of FBAR, Form 8938, and other foreign asset reporting requirements. With expertise in cross-border tax compliance and audit support, we ensure your disclosures are accurate and timely, keeping your operations fully compliant with IRS regulations. Get started today.

But what happens if you fail to report these assets? Let’s take a look at the penalties for non-compliance.

Failure to disclose foreign assets can result in severe financial penalties, civil cases, and criminal charges. Here’s a breakdown of the penalties associated with non-compliance:

Keeping accurate records and filing on time is the best way to ensure compliance and avoid the costly consequences of non-disclosure.

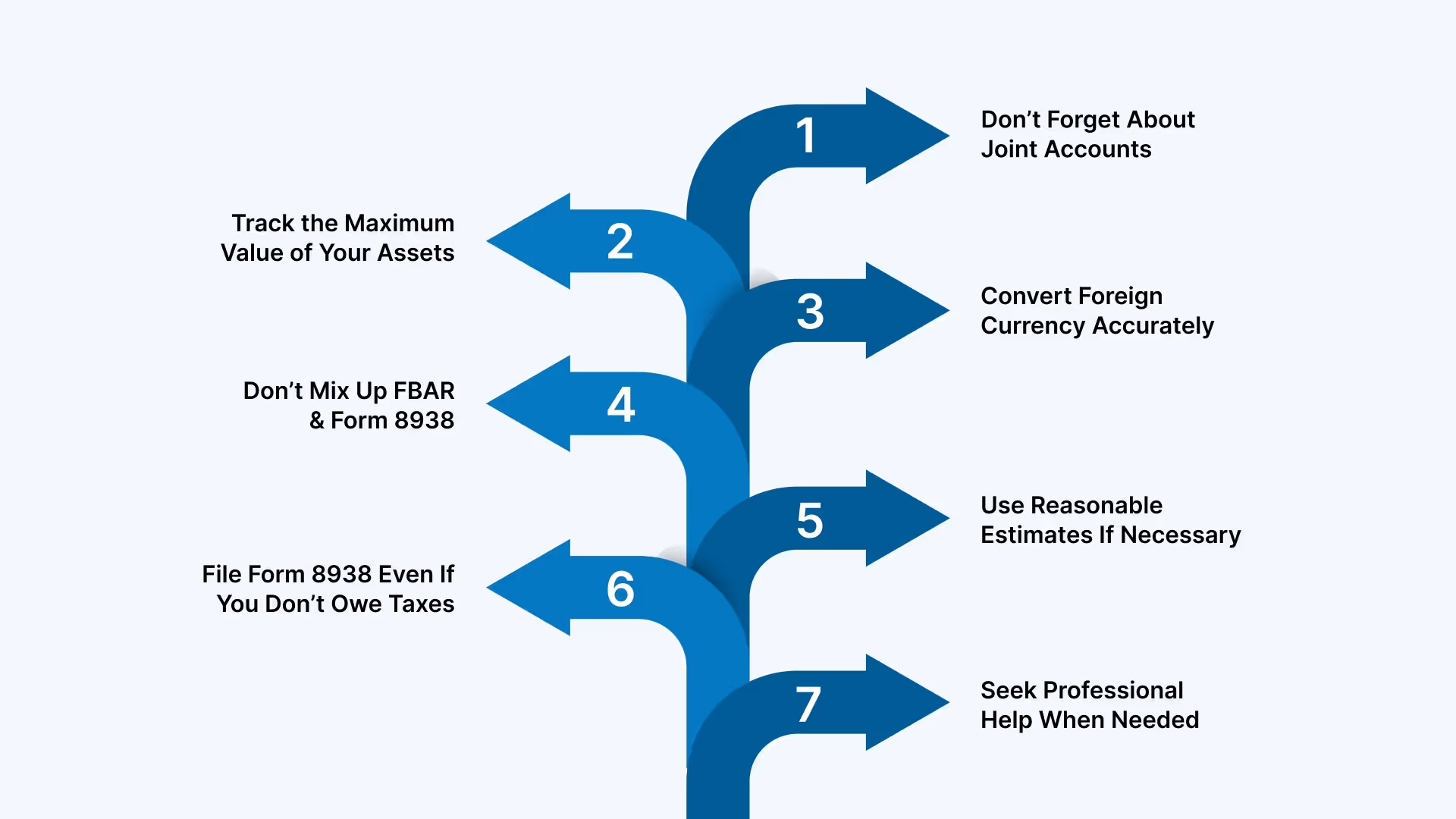

To wrap things up, here are some practical tips to ensure you file IRS Form 8938 correctly and remain compliant.

Filing IRS Form 8938 can seem daunting, especially when dealing with foreign financial assets. To help you tackle the process, here are some valuable tips to ensure you stay compliant:

Joint ownership affects how you report assets. If you’re filing jointly with a spouse, report the full value of jointly owned assets once. For joint ownership with individuals who are not your spouse, report the full value of the asset. This rule applies regardless of whether the other joint owner is a business partner, friend, or relative.

You must report the maximum value of your foreign assets during the year, not just their value at year-end. Use account statements to identify the highest value of your foreign assets during the tax year.

When converting foreign assets into U.S. dollars, use the exchange rate on December 31st of the tax year. If you sold or closed an asset before the year-end, still use the exchange rate on December 31st.

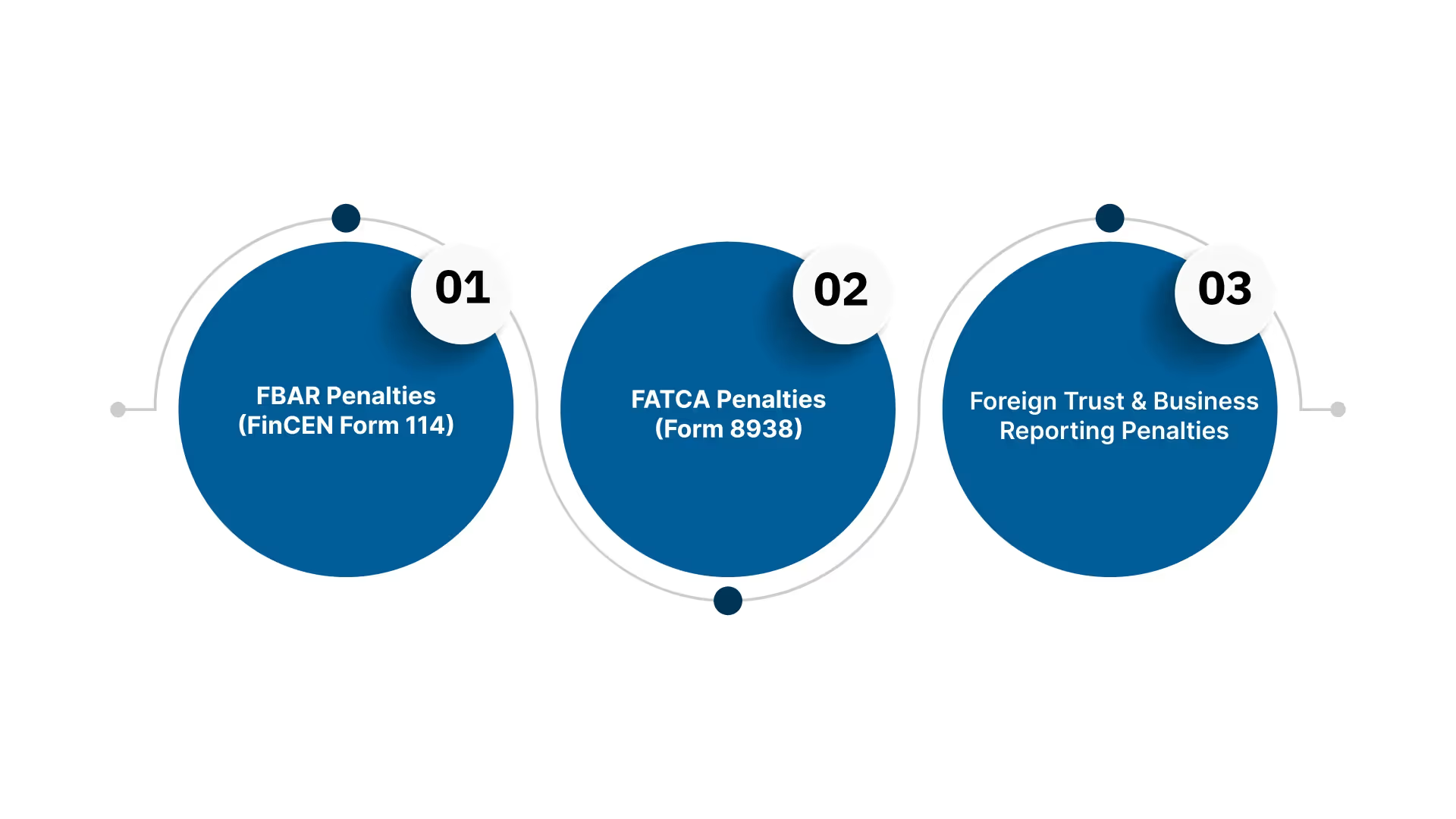

Both FBAR (FinCEN Form 114) and Form 8938 require reporting of foreign assets, but their filing requirements differ:

You may need to file both forms, depending on your assets.

If you’re unsure of an asset’s exact value, you can use a reasonable estimate based on available information. For example, use financial statements or publicly available market data to estimate values. Be sure to document how you arrived at your estimate in case the IRS asks for clarification.

You are required to file Form 8938 even if you don’t owe any U.S. taxes. The IRS uses this form to track foreign financial assets, so it must be filed regardless of your tax liability.

Filing Form 8938 can be complicated, especially when dealing with foreign assets. If you’re unsure about any part of the filing process, consult a professional. VJM Global offers U.S.‑trained CPA & CA teams, Form 8938/FBAR cross‑border compliance, and full accounting‑outsourcing support for U.S. companies with Indian operations, so you can stay compliant with ease.

Following these tips simplifies the Form 8938 filing process, ensures you meet IRS requirements, and helps you avoid penalties.

Accurately reporting foreign assets is a regulatory requirement and a crucial step in avoiding significant penalties. The complexity of international tax laws and foreign asset disclosure can be tricky, but ensuring compliance is essential for the long-term financial health of U.S. businesses and investors.

VJM Global’s specialized services ensure your compliance with U.S. tax regulations, including FBAR and Form 8938. Here’s how we can help:

Get in touch with our expert team today to ensure your foreign asset disclosure is handled seamlessly and in full compliance with U.S. tax laws.

FBAR (Foreign Bank and Financial Accounts Report) is required for U.S. taxpayers who have foreign financial accounts exceeding $10,000 in aggregate value at any point during the year. If you meet this threshold, you must file FinCEN Form 114.

Penalties for non-compliance can be severe, including civil fines up to $10,000 per violation for non-willful failures and up to $100,000 or 50% of the account balance for willful violations. Criminal charges may also apply in cases of intentional non-compliance.

Form 8938 is required for U.S. taxpayers with specified foreign assets exceeding certain thresholds. It must be filed with your annual tax return (Form 1040) if your foreign assets meet these thresholds.

VJM Global offers comprehensive support with FBAR, Form 8938, and other foreign asset disclosures. We provide tax preparation, audit support, and international tax advisory services to ensure full compliance with U.S. regulations.