Small and mid-sized US businesses often juggle lean accounting teams, multiple software platforms, and tight filing deadlines. The result? Missed IRS due dates or payment gaps that trigger costly penalties. Many business owners end up paying these charges simply because they don’t realize that relief options exist.

The IRS First-Time Penalty Abatement (FTA) program changes that. If your company has a clean compliance history, you may qualify for a one-time abatement of failure-to-file, failure-to-pay, or failure-to-deposit penalties. With the proper first-time abatement letter or request, you can cut unnecessary expenses and redirect cash back into your business.

The payoff: lower costs, fewer compliance headaches, and more time to focus on growth. In this blog, you’ll learn how the IRS First-Time Penalty Abatement works, how to determine eligibility, and practical tactics to make your request successful.

At a Glance

FTA covers three penalties only: Failure to file, failure to pay, and failure to deposit, each capped at 25% of the unpaid tax.

Eligibility hinges on compliance history: No significant penalties in the past three years, all current returns filed, and taxes paid or under an installment agreement.

FTA vs. Reasonable Cause: FTA is a one-time relief, whereas reasonable cause can be applied multiple times if backed by documented, uncontrollable circumstances.

Request methods vary: Phone calls often resolve simple penalties quickly, while written statements or Form 843 create stronger records for payroll or complex issues.

Approval is not automatic: Errors, missing documentation, or vague explanations commonly trigger denials, but you can appeal within 30 days through the IRS Independent Office of Appeals.

Understanding IRS First-Time Penalty Abatement

As a small or mid-sized business owner, you know how easy it is for deadlines to slip when your accounting team is handling multiple responsibilities. The IRS First-Time Penalty Abatement (FTA) program gives you a one-time opportunity to reduce or remove specific penalties if you have an otherwise clean compliance record.

The IRS generally applies FTA to three types of penalties:

Failure-to-file penalty: If you miss the filing deadline for your return, the IRS charges 5% of the unpaid tax every month (or part of a month) until you file. This penalty can grow quickly, but it won’t exceed 25% of the unpaid tax.

Failure-to-pay penalty: If you file on time but don’t pay the taxes owed, the IRS typically charges 0.5% to 1% of the unpaid balance per month (or part of a month). Like the filing penalty, this one is capped at 25%.

Failure-to-deposit penalty: If your business doesn’t make employment tax deposits correctly or on time, you could face a failure-to-deposit penalty.

Eligibility for Businesses

You may qualify for the FTA if:

You’ve stayed compliant over the past three years (no significant penalties during that period).

All your current returns are filed, and taxes owed are either paid or arranged under a payment plan.

As an employer, you haven’t had four or more payroll deposit penalty waivers in the last three years, and your case doesn’t involve avoiding the Electronic Federal Tax Payment System (EFTPS).

Example:

Suppose you’re a growing company with 40 employees. Your team files employment taxes, but in one quarter, a deposit is missed due to a staffing change. The IRS issues a failure-to-deposit penalty. Since your business has had a clean record for three years, you can request a first-time penalty abatement.

If approved, the penalty is waived, protecting your bottom line and allowing you to reinvest that money in payroll or operations.

Notes:

Penalty continues to accrue: If you request First-Time Penalty Abatement (FTA) for a failure-to-pay penalty, the IRS may grant relief, but the penalty keeps building until the full tax liability is paid.

Scope of abatement: The FTA only removes penalties up to the point of the request. Any new penalty amounts that accrue afterward remain payable.

Installment agreement benefit: If you set up an installment agreement with the IRS, the failure-to-pay penalty rate reduces from 0.5% to 0.25% per month.

Applicability: This rule applies to both individual taxpayers and businesses.

FTA is just one form of penalty relief. Another option is reasonable cause abatement. Let’s compare them.

First-Time Penalty Abatement vs Reasonable Cause Abatement

As a business owner, it’s essential to understand that the IRS offers more than one way to reduce penalties. While the First-Time Penalty Abatement (FTA) is a one-time opportunity, the IRS also provides reasonable cause penalty relief when circumstances beyond your control prevent you from meeting tax obligations. Being aware of their difference can help you decide which path is best for your company.

Aspect

First-Time Penalty Abatement

Reasonable Cause Penalty Abatement

What it means

A one-time administrative waiver for specific penalties if you have a clean record.

Penalty relief granted when circumstances beyond your control prevented compliance.

Eligibility

No significant penalties in the past 3 years.

All current returns have been filed or are on extension.

Current taxes paid or under an installment plan.

You must demonstrate that your operations were conducted with standard business care and prudence.

Evidence of unexpected events, such as illness, disaster, or IRS error.

Frequency

It can only be used once every 3 years.

Can be requested multiple times if justified by circumstances.

Business Example

Your business missed a quarterly payroll deposit due to oversight, but you’ve been compliant for 3 years.

Your payroll records are lost in a fire, preventing timely deposits.

Documentation needed

Basic compliance history check.

Detailed evidence including disaster reports, IRS correspondence, and more.

Did You Know? If you apply for reasonable cause, but the IRS sees you qualify for FTA, they may process your request as FTA instead. That means you’ll lose the chance to use FTA again for the next three years.

Choosing the correct type of relief is only half the equation. The real question is: what steps do you take if you want to request a first-time penalty abatement?

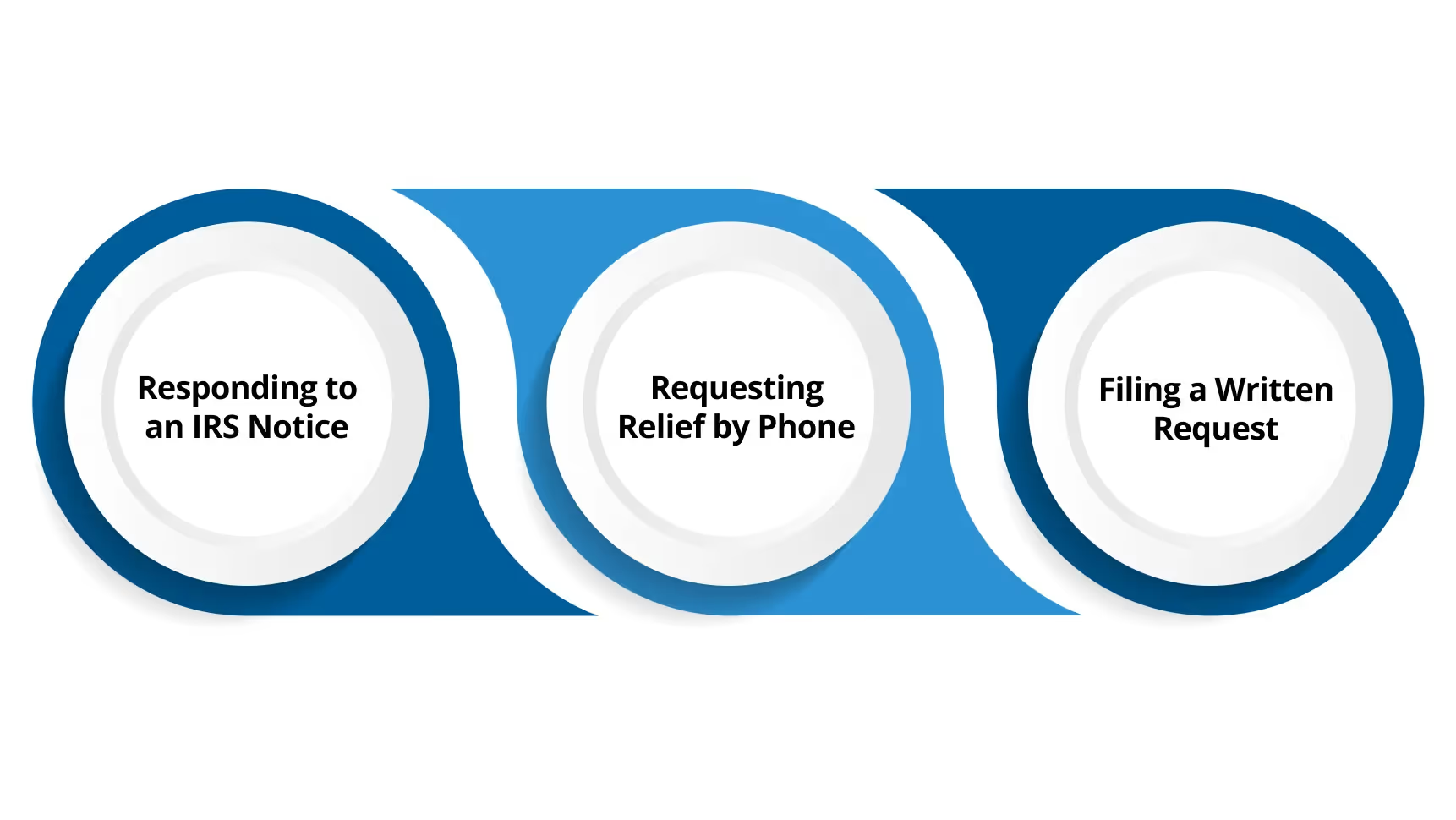

Ways to Request IRS First-Time Penalty Abatement

If your business qualifies for the IRS First-Time Penalty Abatement (FTA), the process to request relief is relatively simple. You can make the request in three main ways:

1. Responding to an IRS Notice

When the IRS issues a penalty, they’ll send you a notice by mail.

This notice includes instructions on how to request relief.

2. Requesting Relief by Phone

Call the toll-free number printed on the top corner of your IRS notice.

You don’t need to mention “First-Time Abatement” specifically; the IRS will check your compliance history automatically.

Pro Tip: Calling is often the quickest option, especially if the penalty is recent and your compliance history is straightforward.

3. Filing a Written Request or Form 843

If you want documented proof, you can submit your request in writing.

Option A: Written Statement

Include your business name, taxpayer ID (EIN), the tax year, the penalty type, and an explicit request for first-time penalty abatement.

After signing, send the statement either to the address provided in your IRS notice or to your usual filing service center.

Option B: IRS Form 843

File Form 843 (Claim for Refund and Request for Abatement)

Check the box on Line 5a for penalty abatement. (Follow the Instructions for Form 843)

On Line 7, provide a brief explanation requesting FTA.

Attach documentation if relevant, though it’s not always required for FTA since approval is based primarily on compliance history.

Did You Know? If your FTA request is denied because your compliance record doesn’t meet the IRS threshold, the IRS will automatically evaluate your claim under reasonable cause abatement.

Key Takeaways:

For straightforward failures to file or failures to pay, a phone call may resolve the issue in minutes.

If your business is penalized for payroll deposits or multiple issues, a written request or Form 843 creates a record of your claim.

Once you’ve submitted your request, the next step is knowing what happens behind the scenes with the IRS.

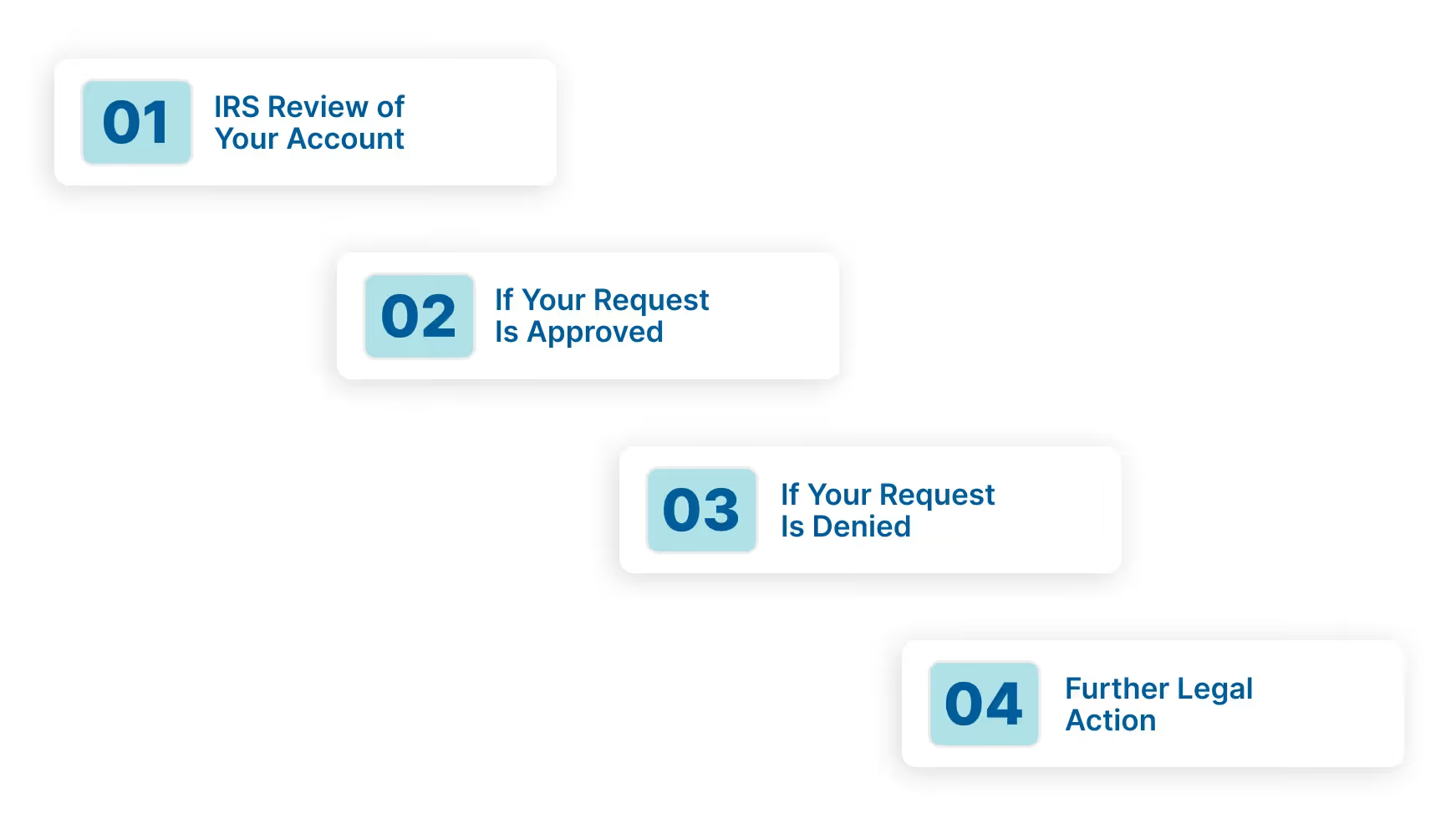

What to Expect After Requesting IRS First-Time Penalty Abatement (FTA)

Filing your IRS first-time penalty abatement request doesn’t end the process. The IRS still needs to review your account before making a decision. Here’s what you can expect once the IRS reviews your case:

1. IRS Review of Your Account

An IRS representative will examine your compliance history and determine whether you qualify.

In some cases, the IRS may even automatically review your account for FTA eligibility when you contact them about a penalty, even if you initially requested another type of relief.

2. If Your Request Is Approved

The penalty, along with related interest, will be removed from your account.

You’ll receive written confirmation in the form of IRS Letter 3502C or IRS Letter 3503C.

Pro Tip: Keep this letter in your records. It’s proof that the penalty was waived and may be necessary for future audits or reviews.

3. If Your Request Is Denied

The IRS will send a denial letter with instructions.

You generally have 30 days from the date of the denial letter to file an appeal with the IRS Independent Office of Appeals.

During this appeal:

The Appeals Office independently reviews your position, the IRS’s position, and any supporting documentation.

You may hire a CPA, attorney, or enrolled agent to represent your business.

If cost is a concern, you may qualify for free or low-cost representation through taxpayer assistance programs.

4. Further Legal Action

If you disagree with the Appeals Office decision:

You may take your case to the US District Court or the Court of Federal Claims.

Generally, you must pay the penalty first before pursuing the case in court.

Why It Matters for Your Business: Appealing an FTA denial gives you another chance to protect your cash flow. For example, if your firm missed a filing deadline due to a payroll system glitch and the IRS denies your initial abatement request, you still have the opportunity to present documentation in an appeal. This second review could save your company thousands of dollars in penalties.

An approved abatement can save your business thousands; however, even eligible businesses sometimes face denials because of minor errors or missing details. Following the right tactics reduces that risk.

Best Tactics for US Businesses Requesting IRS First-Time Penalty Abatement

Securing an IRS first-time penalty abatement (FTA) isn’t just about filling out a form. Success depends on preparation, compliance, and knowing how to present your case. Here are practical tactics to help your business maximize the chances of approval.

1. Confirm Eligibility Before You Apply

Review your compliance history: no significant penalties for the past three years on the same type of return.

Ensure all current returns are filed or under extension.

Pay current taxes owed or set up an installment agreement.

Why it matters: Applying without meeting these basics almost guarantees a denial and could delay resolving your penalty.

2. Strengthen Your Request with Documentation

Attach supporting evidence: prior filing/payment records, proof of emergencies, or correspondence with the IRS.

Label documents clearly with tax year, type of penalty, and amounts.

Include a short explanatory letter, even if not required, to make your case stronger.

Don’t assume reliance on a tax preparer, lack of funds, or oversights will qualify as valid reasons for FTA. The IRS rarely accepts these.

Incomplete forms or vague explanations can lead to automatic denials.

Submitting multiple requests without proper compliance wastes time and may flag your account.

4. Consider Professional Assistance

Tax professionals play a critical role in complex or high-value cases. Here’s how considering their help can be beneficial.

Accuracy: They ensure Form 843 and any statements are error-free and complete.

Advocacy: They can communicate directly with IRS agents and appeals officers.

Strategy: They assess whether FTA, reasonable cause, or another relief path is best for your situation.

Achieve more with less overhead through our global solutions.

5. Stay Organized and Patient

The IRS is known for processing delays, especially during periods of high volume. Protect your business by filing on time, double-checking accuracy, and maintaining complete records. Always keep copies of penalty notices, abatement requests, and IRS correspondence. These can be critical if questions arise later or if you need to appeal.

Wrapping Up

In this blog, we walked through how the IRS First-Time Penalty Abatement works, which penalties qualify, how to request relief, and what happens if your request is approved or denied. We also looked at the differences between FTA and reasonable cause abatement, along with best practices to improve your chances of success.

But here’s the bigger takeaway: while abatement offers short-term relief, long-term stability comes from avoiding penalties altogether. That means staying compliant with IRS deadlines, filing accurately, and keeping books and payroll deposits in order.

This is where VJM Global can help. By outsourcing your accounting and bookkeeping to our India-based team trained in US standards, you:

Stay on top of filings and reconciliations so IRS notices don’t land in your mailbox.

Avoid costly payroll and deposit penalties.

Gain real-time financial visibility, without the expense of extra in-house staff.

1. How long does it take the IRS to process an abatement request?

The IRS typically takes about three to four months to review a penalty abatement request.

2. Do I need an IRS first-time penalty abatement letter template?

You don’t need a formal IRS abatement letter template. A clear statement with tax year, penalty type, taxpayer ID, and request for FTA is sufficient, though professional drafting improves accuracy.

3. Can we reapply for first-time penalty abatement if denied?

Yes. If denied due to missing documentation, you can reapply with additional details. However, repeated requests without eligibility may flag your business, so it’s best to prepare a complete submission.

4. Does the first-time abatement penalty apply to estimated tax penalties?

No. The IRS does not grant first-time penalty abatement for estimated tax penalties. Relief for estimated taxes may only be requested under reasonable cause, not through the FTA program.

5. What forms does the IRS require besides Form 843 for abatement?

While Form 843 is primary, ensure underlying returns such as Form 1040, 1120, or 941 are correctly filed. Without current filings, the IRS will not grant first-time penalty abatement, even with a completed Form 843.

VJM Global

Explore expert insights, tips, and updates from VJM Global

%20(11).avif)