With over 310,000 property management companies across the U.S., the demand for streamlined, reliable accounting systems is more critical than ever. But here’s the catch: as portfolios grow, so does the complexity of managing everything from rent rolls to maintenance costs.

It’s easy for minor discrepancies to snowball into bigger financial headaches, whether it’s miscalculated expenses or the hassle of staying compliant with the constantly changing tax laws.

This blog cuts through the noise, offering property managers clear, actionable best practices to tackle complex accounting challenges head-on. We’ll explore how to automate your accounting workflow and ensure your financials stay in tip-top shape. Let’s jump in.

Property management accounting involves tracking and managing the financial activities related to real estate properties. This includes everything from residential complexes to commercial properties.

Accurate property management accounting helps property owners and stakeholders stay informed about cash flow, profitability, and overall financial health.

By tracking cash flow, profitability, and major expenses, U.S. property managers position themselves to support compliance with federal, state, and local tax laws while assisting property owners with tax implications, such as the SALT deduction cap.

With that in mind, let’s explore some key concepts and terminology that will help you manage property management accounting more effectively.

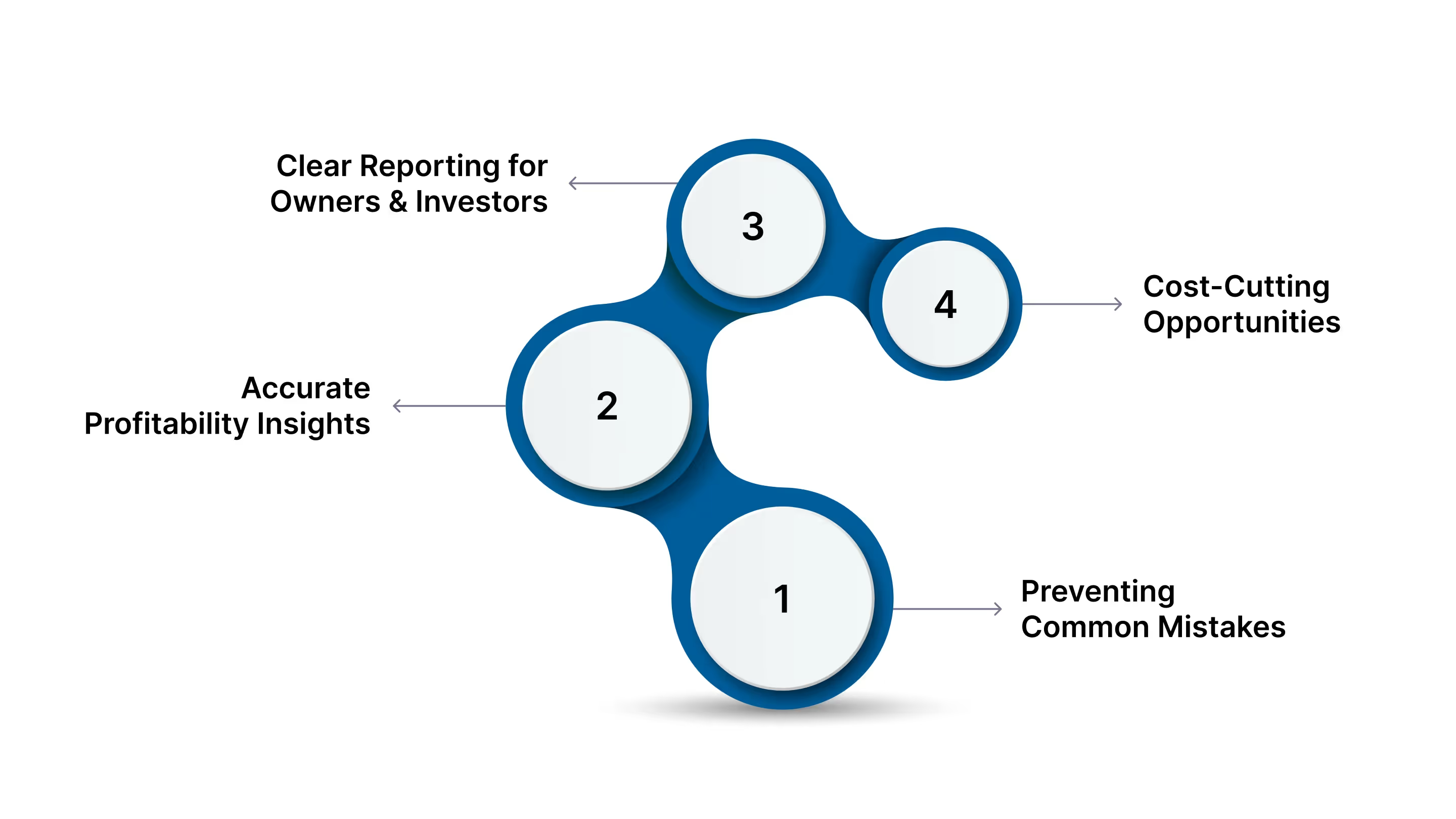

Every property manager has faced that sinking feeling when reviewing month-end reports and spotting an error that’s been compounding over time. The financial consequences of these mistakes can be significant. Here's why strong financial control is essential:

Also Read: Understanding Monthly Bookkeeping Costs and Services

With solid financial management in place, you safeguard your reputation and position your business for sustainable growth and long-term success in a competitive industry.

With that in mind, let’s explore some key concepts and terminology that will help you handle property management accounting more effectively.

Understanding the key terms in property management accounting is essential for accurate financial tracking and reporting. Here's a breakdown of the most important concepts:

Mastering these concepts helps property managers track finances, maintain compliance, and make informed decisions.

Next, we’ll compare cash vs. accrual accounting to see which method works best for your business.

One of the first and most crucial decisions you'll make as a property manager in the U.S. is choosing your accounting method. Whether you go with cash or accrual accounting depends on your business's complexity and growth stage.

Cash basis accounting is straightforward. You only record income when cash is actually received, and expenses when they’re paid. This method gives you a real-time view of your cash flow, but it doesn’t paint the full picture of your property’s profitability, especially if you have unpaid rent or deferred maintenance costs. This is ideal for small businesses, simple portfolios

On the other hand, accrual basis accounting is more detailed. Income is recorded when earned, and expenses when incurred, no matter when the cash changes hands. This method gives you a clearer view of your long-term financial health, making it ideal for larger portfolios or growing businesses looking to plan for the future.

In the U.S., most small property managers with fewer properties can get by with cash accounting, which is easier to manage and aligns with IRS guidelines for businesses earning under $31 million in gross receipts.

Now that you understand which method suits your needs, let’s move on to practical tips every property manager should follow.

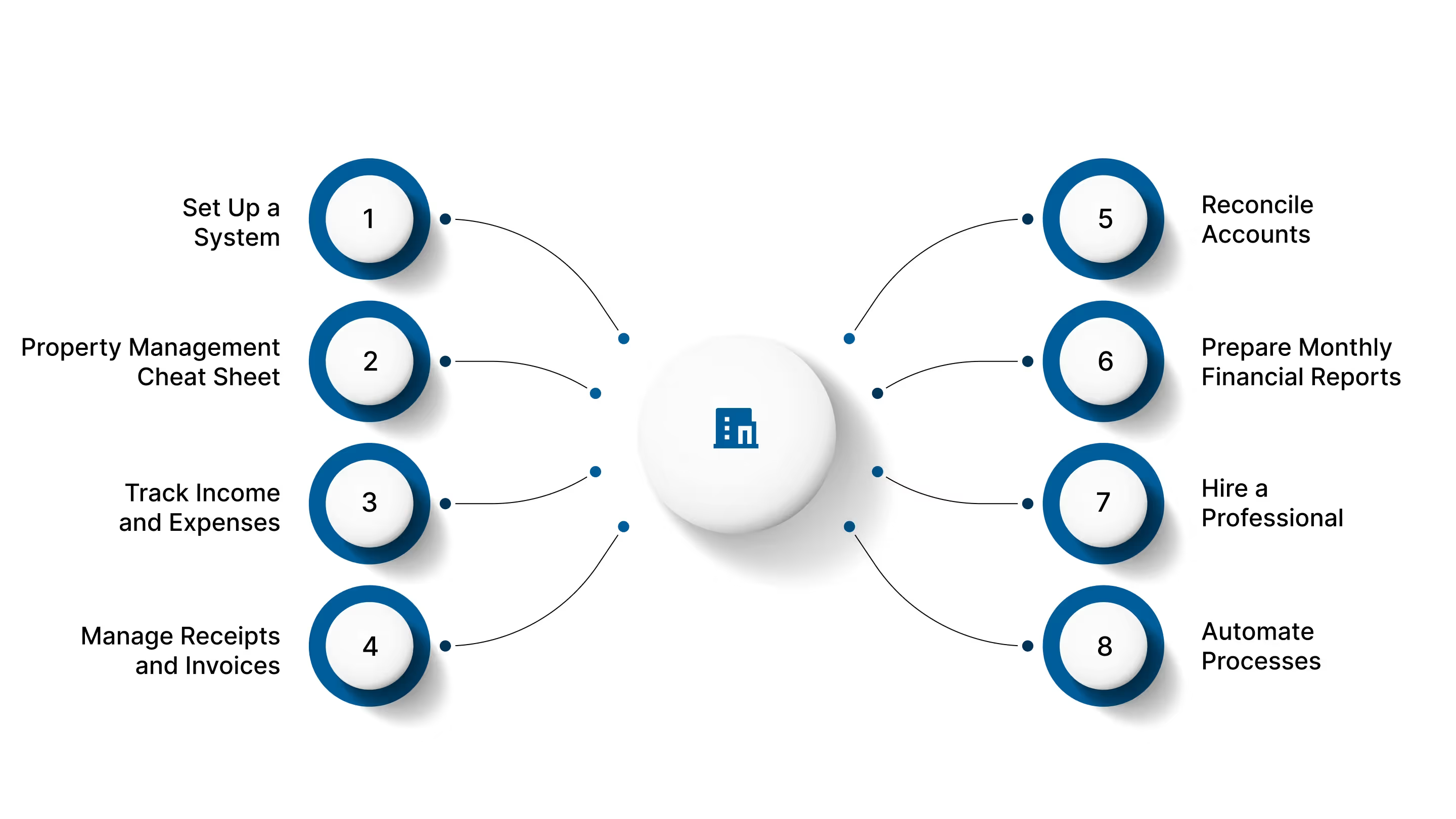

Managing property finances is a complex task, especially when you're overseeing a growing portfolio. Let’s break down the essential steps for setting up a reliable accounting system that keeps everything organized and compliant, from software selection to tracking income and automating tasks.

Select accounting software designed for property management. Depending on your business’s complexity, use software that handles everything from tracking income to reporting expenses. Platforms like QuickBooks and Xero can be great tools for handling your day-to-day accounting needs.

The Chart of Accounts is your financial cheat sheet, organizing all accounts into one place. It includes Balance Sheet Accounts, offering a snapshot of assets, liabilities, and equity, and Income Statement Accounts, which track revenue and expenses. This creates transparency and helps protect your personal assets from business liabilities.

Log all rental income promptly to stay on top of cash flow. Don’t forget to track additional revenue sources like late fees, parking fees, and laundry services. Additionally, record operating expenses such as maintenance, repairs, and utilities, while tracking major future improvements separately.

These major expenses should be tracked separately, as they may be capitalized for depreciation over time, a key factor in U.S. tax filings under the IRS guidelines for real property depreciation.

Keep digital or physical receipts for all expenses. In most U.S. property management operations, adopting a double‑entry bookkeeping system is recommended because it records each transaction twice, debits and credits. This helps you spot discrepancies and produce both profit‑loss and balance‑sheet reports.

Regularly reconcile your bank statements with accounting records to identify discrepancies and ensure your financials are accurate. Reconcile credit card transactions used for property expenses to maintain accurate financial records.

This is particularly important if you’re managing multiple properties and have numerous transactions happening throughout the month.

Key monthly reports should include the balance sheet, income statement, cash flow statement, and rent roll. These reports provide vital insights into the business, helping you assess financial health and report to property owners. They also assist in planning for the future and making informed decisions based on the business's financial standing.

A professional can help ensure your books are accurate, taxes are filed correctly, and financial strategies are optimized. VJM Global offers offshore accounting solutions tailored to property managers, including comprehensive bookkeeping services, payroll and tax compliance support, and assistance with U.S. tax filings and cross-border regulations.

We also provide scalable back-office services, such as software migrations (QuickBooks, Xero), virtual CFO reporting, and the infrastructure needed for growing portfolios. Talk to an expert today.

Use automation tools to streamline processes like rent collection, invoice processing, and financial reporting. Automation reduces the risk of human error and ensures timely, efficient operations.

By following these accounting practices, you’ll streamline your property management finances, ensuring accuracy, reducing errors, and staying compliant.

Also Read: Top 10 Proven Real Estate Financial Planning Tips to Maximize Investment Returns

With these practices in mind, it’s important to avoid common mistakes. Let’s take a look at what to watch out for and how to fix them.

Accounting for property management can be complex, and even minor missteps can lead to significant financial and legal challenges. Avoiding these common mistakes is crucial for maintaining smooth operations and ensuring long-term success.

Recognizing and addressing these mistakes helps property managers safeguard their financial health and grow their portfolios with confidence.

Property management accounting doesn’t have to be a hassle. Implementing a centralized system eliminates the chaos of juggling multiple property finances. Tracking expenses, automating invoicing, and ensuring tax compliance saves you time and prevents costly mistakes that could impact your bottom line.

Regular financial reviews, along with accurate and timely reporting, are essential for staying ahead, whether it's identifying new opportunities or addressing issues before they escalate.

VJM Global offers specialized accounting outsourcing services that cater to the unique needs of property management companies. Here’s how partnering with us can simplify your accounting processes:

By choosing VJM Global, you gain a trusted partner who understands the intricacies of property management accounting. Get started today.

A centralized system ensures all financial data for each property is stored in one place, making it easier to track income, expenses, and reconcile accounts. It helps improve accuracy and efficiency, reducing the risk of errors.

Regular reporting is essential for staying on top of your financial health. It’s recommended to generate reports weekly or bi-weekly, depending on the size of your portfolio, to make informed decisions and identify issues early.

Common mistakes include misreporting rental income, failing to track deductible expenses, and failing to follow local tax regulations. It’s important to stay updated on tax laws and consult professionals to avoid costly penalties.

Outsourcing your accounting allows you to reduce operational costs, save time, and ensure your financials are always accurate. Experts can handle tasks like bookkeeping, tax filings, and financial reporting so that you can focus on property management.

Automation streamlines repetitive tasks such as invoicing, payment reminders, and financial reporting. By automating these processes, you can reduce errors, save time, and keep your accounting system more organized and efficient.