Introduction

The UK charity sector is vast. As of January 2026, 171,227 main charities are registered in England and Wales, contributing total sector income of £69.1 billion in 2021/22. Unlike for-profit businesses focused on profit margins, charities must demonstrate that every pound is stewarded in line with their mission and donor expectations.

Trustees and finance managers face real challenges: navigating SORP compliance, separating restricted and unrestricted funds, determining when an audit is required, and preparing for the 2026 regulatory changes.

Yet 80% of charities report board vacancies, with 35% lacking financial expertise on their boards. This guide gives you the practical grounding to bridge that gap.

By the end, you'll understand exactly which standards apply to your charity, what reporting is required at your income level, and how to manage tax reliefs without leaving money on the table.

TLDR:

- Charity accounting prioritises accountability over profit, using a Statement of Financial Activities (SoFA) instead of a P&L

- SORP 2026 creates three income-based tiers, effective 1 January 2026

- From September 2026, the audit threshold rises to £1.5M and independent examination to £40K

- Restricted funds must be tracked separately from unrestricted—conflating them can lead to governance failures

- Gift Aid allows charities to reclaim 25p for every £1 donated, but declarations must be retained for 6 years

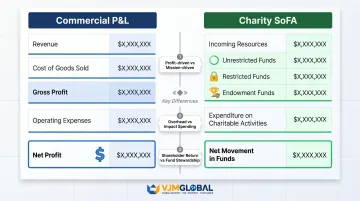

How Charity Accounting Differs from For-Profit Accounting

For-profit accounting aims to present profitability to shareholders. Charity accounting is about accountability and stewardship—demonstrating that funds were used appropriately and in line with charitable objectives. That distinction drives every structural difference in how charities prepare and present their accounts.

Restricted vs. Unrestricted Funds

Income in charity accounts must be classified as restricted (donated or granted for a specific purpose) or unrestricted (available for general use). Conflating these can lead to serious governance and compliance failures.

Example: Grant funding received for a specific programme cannot be redirected to cover administrative costs. The accounts must clearly reflect this separation, and any material deficit in a fund must be explained in the Trustees' Annual Report.

Restricted funds fall outside the definition of reserves. Permanent endowment is property that the charity must retain indefinitely.

The Statement of Financial Activities (SoFA)

Charities use a SoFA instead of a Profit & Loss statement. The SoFA records all incoming resources and expenditure across all funds (unrestricted, restricted, and endowment), showing how money moved in and out during the year rather than calculating a net profit.

This structure enables donors, trustees, and regulators to trace funds to specific activities — a level of transparency that standard commercial accounts are not designed to provide.

The Trustees' Annual Report

For a charity, the Trustees' Annual Report (TAR) is a legal requirement, not optional narrative. It must explain:

- The charity's objectives, activities, and achievements

- Financial position and reserves policy

- Public benefit delivered

- Risk management and future plans

Charities with income over £1 million must additionally report on trustee induction/training, grant-making policies, investment performance, and detailed risk management.

The Public Benefit Test

Charities must demonstrate public benefit in their reporting. The Charities Act 2011 requires that charitable purposes serve the public benefit, and trustees have a legal duty to "have regard" to the Charity Commission's public benefit guidance.

Charities with income over £500,000 must provide a detailed public benefit report; those below that threshold need only a brief summary.

Auditors and the Charity Commission both assess whether funds were used for charitable purposes — a layer of scrutiny that goes well beyond what commercial accounts face.

UK Charity Accounting Standards: SORP, FRS 102, and the 2026 Updates

The Charities SORP (Statement of Recommended Practice) governs how charities prepare accruals accounts in the UK. It is not a law itself but effectively mandatory for charities preparing accruals-based accounts, as it sets out best practice endorsed by the Charity Commission.

FRS 102 and UK GAAP

FRS 102 is the specific financial reporting standard (part of the UK GAAP framework) that underpins the Charities SORP. They are not the same thing: FRS 102 is one standard within the broader UK GAAP suite, and charities apply it through the lens of the SORP.

To distinguish the two:

- UK GAAP — the broader framework of UK accounting standards, covering multiple individual standards

- FRS 102 — the Financial Reporting Standard applicable in the UK and Republic of Ireland, issued by the Financial Reporting Council (FRC), and the specific standard charities apply via the SORP

With the framework established, the upcoming SORP 2026 revision introduces some of the most significant structural changes in years.

SORP 2026: What's Changing

SORP 2026 introduces three new income-based tiers, effective for reporting periods starting on or after 1 January 2026:

| Tier | Income Band | Key Features |

|---|---|---|

| Tier 1 | Up to £500,000 | Simplified disclosures; no cash flow statement required |

| Tier 2 | £500,000–£15 million | Moderate disclosures |

| Tier 3 | Over £15 million | Full disclosures; cash flow statement required |

Other SORP 2026 changes include:

- Income recognition: Adopts a new five-step model for exchange transactions, aligning with IFRS 15

- Lease accounting: Brings operating leases onto the balance sheet as a Right of Use asset with a corresponding lease liability

- Trustees' Annual Report: Mandates impact reporting for all charities and adds dedicated ESG sections

- Simplifies accounting and disclosure for mixed-motive social investments

- Introduces clearer, easier-to-apply requirements for provisions

Notably, Tier 1 charities are exempt from preparing a cash flow statement — a meaningful reduction in reporting burden for smaller organisations operating below the £500,000 income threshold.

New Accounting Thresholds from September 2026

The following threshold changes are expected to come into effect for accounting years ending on or after 30 September 2026:

| Requirement | Current Threshold | New Threshold |

|---|---|---|

| Independent examination required | Income over £25,000 | Income over £40,000 |

| Professionally qualified examiner | Income over £250,000 | Income over £500,000 |

| Receipts and payments eligibility | Income below £250,000 | Income below £500,000 |

| Statutory audit (income) | Income over £1,000,000 | Income over £1,500,000 |

| Statutory audit (assets) | Assets over £3,260,000 | Assets over £5,000,000 |

| Group accounts | Aggregate income £1,000,000 | Aggregate income £1,500,000 |

These are the most significant updates to charity financial thresholds in over a decade. The changes are currently awaiting commencement via secondary legislation.

Choosing the Right Accounting Method for Your Charity

Charities have two permitted accounting methods—Receipts and Payments and Accruals. Eligibility depends on income level and legal structure, not preference alone.

Receipts and Payments Accounts

Receipts and payments accounts involve a simple record of money received and paid out during the year, plus a statement of assets and liabilities.

Eligibility:

- Only available to unincorporated charities and CIOs with income below £250,000 (rising to £500,000 from September 2026)

- Charitable companies (companies limited by guarantee) are prohibited from using this method by company law

Limitations: This method provides a snapshot of cash movement but lacks year-on-year comparability and does not capture liabilities, debtors, or depreciation.

Accruals Accounts

Accruals accounts record income and expenditure in the period they relate to (not when cash moves), include adjustments for debtors, creditors, and depreciation, and provide a more accurate picture of the charity's financial position.

Required for:

- All charitable companies

- All charities above the income threshold (currently £250,000)

- Any charity where trustees choose this method or the governing document requires it

Accruals accounts contain a balance sheet, SoFA, and explanatory notes, and must follow the Charities SORP.

Setting Up a Chart of Accounts

A charity's chart of accounts must structure income and expenditure in a way that enables clear reporting to trustees, donors, and the Charity Commission. Categories should reflect the charity's activities and fund types, not just generic cost headings.

Many UK charities work with specialist accounting firms to set up SORP-compliant bookkeeping systems and maintain clean fund tracking records—particularly important where restricted grants require separate monitoring.

VJM Global supports UK organisations in establishing these frameworks, providing accounting outsourcing services tailored to each charity's structure and fund reporting requirements.

Charity Reporting Obligations by Income Band

Reporting obligations increase with income. The tiered structure is as follows:

| Income Band | Requirements | Filing Notes |

|---|---|---|

| Under £10,000 | Keep accounting records; prepare accounts; update charity details | No TAR or accounts filing unless requested by the Charity Commission |

| £10,000–£25,000 | Complete and file annual return online; prepare TAR and accounts | No TAR or accounts filing unless requested |

| Over £25,000 | File annual return, TAR, and accounts; external scrutiny required | Independent examination or audit mandatory |

Filing deadline: All required documents must be filed within 10 months of the end of the charity's financial year.

Requirements also vary by charity structure:

- CIOs: Must file an annual return, TAR, and accounts regardless of income level (even if income is zero)

- Charitable companies: Must file accounts and a directors' report with both Companies House and the Charity Commission (if income exceeds £25,000), and must always use accruals accounts

- Unincorporated charities: Filing requirements depend solely on income band

The charity's governing document may impose stricter requirements than the law requires—for example, a constitution may mandate a full audit even where one is not legally required. Trustees should review their governing document carefully.

Independent Examination vs. Statutory Audit

An independent examination provides negative assurance — the examiner reports if anything has come to their attention suggesting the accounts are incorrect or non-compliant. A statutory audit requires positive evidence that accounts give a "true and fair view." The two are not interchangeable, and the term "audit" is used loosely in practice — most charities below £1M income do not require a statutory audit.

Current thresholds:

- Statutory audit required if gross income exceeds £1 million, OR if total assets exceed £3.26 million and gross income exceeds £250,000

- Independent examination required for charities with income between £25,000 and £1 million

- Professionally qualified examiner required if gross income exceeds £250,000

From September 2026, these thresholds increase across the board:

- Statutory audit: income threshold rises to £1.5 million

- Independent examination: lower threshold rises to £40,000

- Professionally qualified examiner: income threshold rises to £500,000

Choosing an Independent Examiner

The examiner must be:

- Fully independent of the charity

- Have a good understanding of charity finance and law

- For charities above £250,000, be a member of a body specified in the Charities Act (such as ACIE — the Association of Charity Independent Examiners)

Tax Considerations for UK Charities

Gift Aid

Gift Aid allows registered charities to reclaim basic rate income tax on eligible donations from UK taxpayers—adding 25p for every £1 donated. This reflects the basic rate of Income Tax at 20% grossed up.

Requirements:

- The donor must have paid at least as much in Income Tax or Capital Gains Tax in that tax year as the charity claims

- A Gift Aid declaration must be obtained, including: donor's full name, full home address including postcode, description of the gift, and confirmation that the donor has paid sufficient tax

- Records must be kept for 6 years after the most recent donation claimed

How to claim: Charities can claim Gift Aid online through HMRC. Payment is typically received within 5 weeks.

Small donations scheme: Charities may claim on cash donations of £30 or less without requiring a Gift Aid declaration.

Common compliance risks (confirmed by HMRC Chapter 7 guidance): Missing declarations, donor benefit limit breaches, insufficient record-keeping, claims on conditional donations, donors not having paid sufficient tax, and charity not being recognised for tax purposes.

VAT for Charities

Charitable status does not automatically exempt an organisation from VAT. The VAT registration threshold is £90,000 in taxable turnover — once exceeded, registration with HMRC is mandatory.

Beyond registration, two other VAT considerations affect most charities:

- VAT reliefs: Charities don't pay VAT on certain goods and services purchases, but must prove eligibility to the seller. VAT registration is not required for this relief.

- Partial exemption: Charities running both taxable (standard or zero-rated) and exempt activities can only reclaim VAT on inputs tied to taxable activities. This requires tracking input and output VAT separately by activity type.

Corporation Tax Relief and Trading Activities

Charities are generally exempt from Corporation Tax on income used for charitable purposes. However, commercial or trading income may be taxable unless conducted through a wholly owned trading subsidiary—a structure many larger charities use to separate non-charitable income.

Primary purpose trading exemption: A charity is exempt from Corporation Tax on profits from any trade carried out in direct pursuit of its charitable purposes, provided that income is applied solely to those purposes.

Small trading tax exemption (current thresholds, updated from October 2018):

| Charity's Gross Annual Income | Maximum Permitted Small Trading Turnover |

|---|---|

| Under £32,000 | £8,000 |

| £32,001 to £320,000 | 25% of the charity's total annual turnover |

| Over £320,000 | £80,000 |

If a charity's small trading turnover exceeds the exemption limit, tax is due on all profits from that trade.

Trading subsidiary structure: Charities can establish a wholly owned subsidiary trading company to conduct non-primary-purpose trading. The subsidiary can donate all its profits to the parent charity as a Gift Aid payment (within 9 months of the end of the accounting period), eliminating Corporation Tax liability.

Frequently Asked Questions

What accounting is needed for a small charity?

Small charities (income under £250,000, rising to £500,000 from September 2026) can use receipts and payments accounts, must keep records of all income and expenditure, and are required to have accounts independently examined once income exceeds £25,000 (rising to £40,000 from September 2026).

What is the best accounting method for nonprofit organisations?

Accruals accounting gives a more accurate picture of finances, recording income and expenditure in the period they relate to — while receipts and payments is acceptable for smaller organisations below the threshold. The right method depends on the charity's size, complexity, and reporting obligations.

How is charity accounting different?

Charity accounting focuses on accountability rather than profitability, uses a Statement of Financial Activities instead of a P&L, must separate restricted and unrestricted funds, and requires a Trustees' Annual Report as a legal document rather than optional narrative.

Is UK GAAP and FRS 102 the same?

UK GAAP is the broader framework of UK accounting standards, while FRS 102 is one specific standard within that framework. Charities apply FRS 102 through the Charities SORP, which adapts it to the specific needs and structure of charitable organisations.

What is the 30/70 rule for charities?

The 30/70 rule has no formal regulatory basis in UK charity law. The Charity Commission's CC20 guidance explicitly states: "There is no set amount that a charity should spend on its fundraising." It functions as an informal donor confidence benchmark, nothing more.

What is the 33% rule for nonprofits?

The 33% rule has no formal basis in UK charity law. The Charity Commission's CC19 guidance on reserves confirms there is no legal rule dictating the proportion of income a charity can hold as reserves. The rule is an informal resilience guideline, not a statutory requirement.