The rules governing recognition, measurement, and amortisation under FRS 102 are precise and unforgiving. Get them wrong — whether by capitalising something that should be expensed, or misclassifying goodwill — and the downstream tax consequences under CTA 2009 Part 8 can compound the problem.

This article covers the core technical ground: what qualifies as an intangible asset under FRS 102, how to recognise and measure it, the specific treatment of goodwill, and how HMRC's corporation tax rules interact with the accounting approach.

Key Takeaways

- Intangible assets are identifiable non-monetary assets without physical substance, recognised under FRS 102 Section 18

- Recognition requires both probable future economic benefits and reliable cost measurement — simultaneously

- Internally generated brands, customer lists, and goodwill cannot be capitalised — qualifying development costs are the one permitted exception

- FRS 102 requires goodwill to be amortised over its useful economic life (capped at 10 years if uncertain) — unlike IFRS, which prohibits amortisation entirely

- CTA 2009 Part 8 follows the same accounting treatment, applying only to assets acquired on or after 1 April 2002

What Counts as an Intangible Asset Under UK Standards

FRS 102 Section 18 defines an intangible asset as "an identifiable non-monetary asset without physical substance" (para 18.2). The identifiability test is satisfied if the asset meets either of two conditions:

- Separable — capable of being sold, transferred, licensed, rented, or exchanged separately from the entity

- Arising from contractual or other legal rights — even where those rights are not themselves transferable

Assets that typically qualify include patents, trademarks, copyrights, customer lists arising from contracts, franchise agreements, software licences, non-compete agreements, and domain names.

By contrast, FRS 102 para 18.8C explicitly prohibits capitalisation of:

- Internally generated brands and mastheads

- Publishing titles

- Customer relationships not arising from contracts

There is no accounting policy choice here — these exclusions are mandatory.

The Post-2018 Business Combination Rule

For intangible assets acquired as part of a business combination, the recognition bar is higher. Following the FRC's Triennial Review 2017 (effective for periods beginning on or after 1 January 2019), an acquired intangible must meet both the separability criterion and the contractual/legal rights criterion to be recognised separately from goodwill.

This is more restrictive than the pre-2019 position — and more restrictive than IFRS 3, which still applies an either/or test. In practice, it means more acquired intangibles are subsumed into goodwill under FRS 102.

Note: The FRC's 2024 Periodic Review (effective 1 January 2026) reverses this, reverting to the either/or test and realigning FRS 102 more closely with IFRS 3. Entities preparing for this change should review their acquisition accounting policies now.

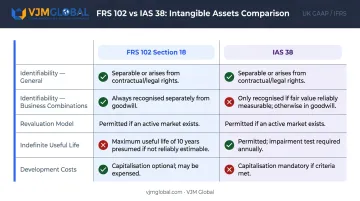

FRS 102 vs. IAS 38 — Key Definitional Differences

| Feature | FRS 102 Section 18 | IAS 38 |

|---|---|---|

| Identifiability (general) | Separable OR contractual/legal | Separable OR contractual/legal |

| Identifiability (business combinations) | BOTH required (post-2019) | Either/or |

| Revaluation model | Not permitted | Permitted if active market exists |

| Indefinite useful life | Not permitted | Permitted (annual impairment test required) |

| Development costs | Accounting policy choice | Mandatory capitalisation if criteria met |

The prohibition on revaluation and indefinite useful lives have real consequences for UK preparers: assets that could appreciate in value on an IFRS balance sheet must still be amortised to zero under FRS 102, regardless of commercial reality.

Initial Recognition and Measurement Under FRS 102

An intangible asset is recognised only when both of the following conditions are met simultaneously (FRS 102 para 18.4):

- It is probable that expected future economic benefits will flow to the entity

- The cost or value can be measured reliably

These are conjunctive — one without the other is not enough.

| Acquisition Route | Measurement Basis | Key Notes |

|---|---|---|

| Separately acquired | Purchase price (net of discounts) + directly attributable costs | Legal fees to register a patent are includable; general overheads and training costs are not |

| Acquired in a business combination | Fair value at acquisition date | Where fair value cannot be reliably measured, the intangible is absorbed into goodwill rather than recognised separately |

Internally Generated Intangibles

FRS 102 takes a strict line here. The following items can never be capitalised, regardless of their economic value:

- Internally generated goodwill

- Brands, logos, and corporate identities

- Publishing titles and mastheads

- Customer lists not arising from contracts

- Start-up costs, training, and advertising expenditure

- Relocation and reorganisation costs

The cost of developing these items cannot be reliably distinguished from the cost of developing the business as a whole — which is precisely why no capitalisation is permitted.

The narrow exception is internally generated software — this can be capitalised when both recognition criteria are met.

Research vs. Development Costs

FRS 102 draws a clear line between the two phases:

- Research expenditure must always be expensed as incurred. No capitalisation option exists.

- Development expenditure may be capitalised — but only when all six conditions in FRS 102 para 18.8H are satisfied:

- Technical feasibility of completing the asset

- Intention to complete and use or sell it

- Ability to use or sell the asset

- Probable future economic benefits (demonstrated by a market or internal use case)

- Availability of adequate technical and financial resources

- Ability to measure attributable expenditure reliably

All six must be met before any capitalisation begins. Expenditure incurred before that threshold is reached cannot be retroactively capitalised — a rule that catches many companies off guard when they begin capitalising partway through a project rather than from the point all criteria are demonstrably satisfied.

Amortisation, Impairment, and Derecognition of Intangible Assets

Once recognised, every intangible asset under FRS 102 has a finite useful life and must be amortised systematically over that life. The amortisation method should reflect the pattern in which economic benefits are consumed. Where that pattern cannot be reliably determined, straight-line is the default.

The 10-Year Cap

FRS 102 para 18.20 contains a critical practical rule: if an entity cannot reliably estimate the useful life of an intangible asset, the life must not exceed 10 years. This cap was amended from five years to ten years effective 1 January 2016.

Think of the cap as a fallback: where a reliable estimate exists, that estimate governs — even if it exceeds 10 years. When evidence is thin, the 10-year ceiling applies.

IAS 38 takes a different approach, permitting an indefinite useful life designation. Assets assigned an indefinite life under IAS 38 are not amortised; they are tested for impairment annually instead. FRS 102 entities have no equivalent option.

Impairment Triggers

Once amortisation policy is set, the next checkpoint is impairment. At each reporting date, entities must assess whether indicators of impairment exist. FRS 102 Section 27 (para 27.9) lists both external and internal triggers:

External indicators:

- Significant decline in the asset's market value

- Adverse changes in technological, market, economic, or legal environment

- Rising interest rates affecting value-in-use calculations

Internal indicators:

- Evidence of obsolescence or physical damage

- Plans to discontinue or substantially restructure the asset's use

- Internal reporting showing worse-than-expected economic performance

The FRC's corporate reporting review found that impairment accounted for 12% of all cases opened in 2023/24 — for the second consecutive year. Recurring weaknesses cited include insufficient sensitivity analysis and unclear goodwill allocation to cash-generating units.

Derecognition

An intangible asset is derecognised on disposal or when no future economic benefits are expected. The resulting gain or loss — the difference between net disposal proceeds and carrying amount — goes through profit or loss. Gains must not be classified as revenue.

Goodwill vs. Other Intangibles: Key Distinctions Under FRS 102

Goodwill under FRS 102 arises exclusively from a business combination — specifically, the excess of the cost of the combination over the acquirer's interest in the net fair value of identifiable assets, liabilities, and contingent liabilities at the acquisition date (para 19.22). Self-generated goodwill cannot be recognised under any circumstances.

After recognition, goodwill must be measured at cost less accumulated amortisation and impairment losses. Amortisation must be systematic over its estimated useful economic life. If that life cannot be reliably estimated, it must not exceed 10 years (para 19.23(a)).

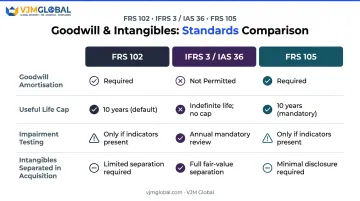

| Framework | Goodwill Amortisation | Useful Life Cap | Impairment Testing | Intangibles Separated in Acquisition? |

|---|---|---|---|---|

| FRS 102 | Mandatory | 10 years if uncertain | When indicators exist | Yes, if fair value reliably measurable |

| IFRS 3 / IAS 36 | Prohibited | N/A | At least annually | Yes, mandatory if identifiable |

| FRS 105 | Mandatory | 5 years if uncertain | When indicators exist | No — all subsumed into goodwill |

The table above highlights a critical divergence between UK GAAP and full IFRS. Under IFRS 3, goodwill sits on the balance sheet indefinitely until impaired — creating exposure to large, sudden write-downs. Under FRS 102, the amortisation charge is predictable and annual, which reduces net assets steadily but eliminates that cliff-edge impairment risk.

For companies near the micro-entity threshold, FRS 105 produces a larger goodwill figure than FRS 102 would. Because FRS 105 subsumes all acquired intangibles into goodwill rather than separating them at fair value, the opening balance sheet carries more goodwill — and amortises it faster, over a maximum of five years where useful life is uncertain.

Corporation Tax Treatment of Intangible Assets Under CTA 2009 Part 8

The corporate intangibles regime under CTA 2009 Part 8 broadly follows the accounting treatment. Where a company charges amortisation or impairment through the income statement, a corresponding tax deduction is generally available. Accounting credits — including revaluation uplifts or impairment reversals — are brought into charge as taxable income. Accounting credits — including revaluation uplifts or impairment reversals — are brought into charge as taxable income. Three specific conditions and date thresholds shape how Part 8 applies in practice.

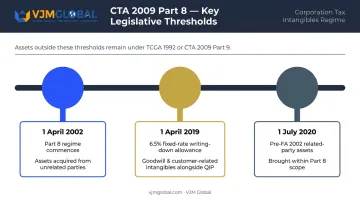

The 1 April 2002 Cut-Off

Part 8 only applies to intangible fixed assets created or acquired from an unrelated party on or after 1 April 2002. Assets held before that date remain under the capital gains regime (TCGA 1992) or Part 9 CTA 2009.

This cut-off still matters in practice. Acquisitions involving long-established brands or legacy IP often include assets straddling the 2002 date, requiring separate treatment for pre- and post-commencement assets.

Maintaining a detailed intangible asset register — showing acquisition date, counterparty relationship, asset category, and applicable tax regime — is not optional; it is essential.

The 6.5% Fixed-Rate Writing-Down Allowance

From 1 April 2019, CTA 2009 Chapter 15A introduced a fixed-rate deduction of 6.5% per annum for goodwill and certain customer-related intangibles (customer information, customer relationships, unregistered trademarks, and related licences) acquired alongside qualifying intellectual property (QIP).

Key conditions to check:

- The goodwill or customer-related intangible must be acquired as part of a business acquisition alongside QIP

- Relief is capped at six times the cost of the QIP acquired

- QIP excludes registered or unregistered trademarks

- A separate non-revocable election for a 4% fixed-rate deduction is also available within two years of the accounting period end

Assets Excluded from Part 8

Several asset categories fall outside the regime entirely:

- Financial assets (shares, loan relationships)

- Rights over tangible assets (land leases, machinery leases)

- Oil licences and interests in land

- Assets covered by other specific legislation (film relief, sound recording reliefs)

The 1 July 2020 Change

Finance Act 2020 brought pre-FA 2002 intangible assets acquired from related parties on or after 1 July 2020 within the Part 8 regime. Previously, these would have remained under capital gains rules. However, debit relief may be restricted until realisation. Anti-forestalling rules cover the period 11 March to 30 June 2020.

UK businesses managing complex intangible portfolios — particularly those involved in cross-border IP ownership, licensing arrangements, or M&A activity — face a layered compliance challenge across these different date thresholds.

VJM Global's chartered accountants and tax advisers help UK businesses ensure their FRS 102 treatment aligns with CTA 2009 obligations — and that no available deduction goes unclaimed.

Frequently Asked Questions

What is the difference between internally generated and purchased intangible assets under FRS 102?

Purchased intangibles are capitalised at cost when both recognition criteria are met. Internally generated intangibles — including brands, customer lists, and goodwill — are largely prohibited from capitalisation under FRS 102 para 18.8C. The narrow exception is qualifying development costs that satisfy all six conditions in para 18.8H.

Can development costs be capitalised under UK GAAP?

Yes — FRS 102 gives entities an accounting policy choice to capitalise development costs when all six criteria in para 18.8H are met (including technical feasibility, intention to complete, and reliable cost measurement). Research costs, however, must always be expensed as incurred, with no capitalisation option.

What happens if the useful life of an intangible asset cannot be determined?

Under FRS 102, if an entity cannot reliably estimate useful life, the amortisation period must not exceed 10 years. This differs from IAS 38, which permits an indefinite useful life designation subject to annual impairment testing rather than systematic amortisation.

How is goodwill treated under FRS 102 compared to full IFRS?

FRS 102 requires goodwill to be amortised over its useful economic life, capped at 10 years if that life cannot be reliably estimated. Under IFRS 3, goodwill is never amortised — it remains on the balance sheet and is tested for impairment at least annually.

How does HMRC tax intangible assets acquired in a business combination?

CTA 2009 Part 8 generally allows tax deductions following the accounting amortisation or impairment charge, but only for assets acquired on or after 1 April 2002. Goodwill and certain customer-related intangibles acquired alongside qualifying IP from 1 April 2019 may instead qualify for the 6.5% fixed-rate writing-down allowance.

Does FRS 102 allow revaluation of intangible assets?

FRS 102 does not permit revaluation of intangible assets, as active markets for most intangibles rarely exist in practice. IAS 38 does allow revaluation to fair value where an active market can be demonstrated — making this a key distinction for entities weighing a move to full IFRS.