Introduction

When one business takes control of another, the accounting treatment can make or break the integrity of your consolidated accounts. Get it wrong, and you risk misstated goodwill, incorrect fair value allocations, and regulatory exposure under the Companies Act 2006.

Business combination accounting under UK GAAP is governed by FRS 102 Section 19. It sets out how an acquiring entity recognises and measures the assets, liabilities, and goodwill that arise when control of another business transfers hands.

This guide is written for UK finance directors, accountants, and businesses navigating mergers, acquisitions, or group restructuring. Many practitioners still struggle with the post-FRS 102 landscape — particularly the shift away from merger accounting that was permitted under old UK GAAP (FRS 6).

The single most important rule to understand: the acquisition method is now mandatory for commercial deals, and merger accounting is prohibited. What follows explains exactly how to apply it.

Key Takeaways

- FRS 102 requires all commercial business combinations to use the acquisition method; merger accounting is only permitted for qualifying group reconstructions

- Acquirers must identify the acquisition date, fair-value all identifiable assets and liabilities, and recognise any goodwill or bargain purchase gain arising

- Goodwill must be amortised over its useful life (maximum 10 years if life cannot be estimated), unlike IFRS 3's impairment-only model

- Under FRS 102, transaction costs are capitalised — not expensed as under IFRS 3

- Small groups below £15M turnover, £7.5M balance sheet, and 50 employees may qualify for a consolidation exemption

What Is a Business Combination Under UK GAAP?

FRS 102 Section 19.3 defines a business combination as "the bringing together of separate entities or businesses into one reporting entity." This covers:

- Share acquisitions — buying another entity's equity to gain control

- Asset acquisitions — purchasing a net set of assets that together constitute a business

Not every asset purchase qualifies. FRS 102 defines a "business" as an integrated set of activities and assets capable of being conducted and managed for the purpose of providing a return. This gives stakeholders a consolidated view of the combined entity's financial position.

Transactions Excluded from Section 19

Section 19 does not apply to:

- Single asset acquisitions — buying property, equipment, or other assets that don't constitute a business

- Formation of joint ventures — covered under Section 15

- Common control transactions (group reconstructions) — these may use merger accounting if specific conditions are met

Why FRS 102 Mandates the Acquisition Method

The Regulatory Requirement

Under FRS 102 (effective for accounting periods beginning on or after 1 January 2015), all business combinations must be accounted for using the acquisition method. There is no choice.

This contrasts sharply with old UK GAAP under FRS 6, which permitted merger accounting if specific qualifying criteria were met. The change was made to:

- Align with international standards (though FRS 102 differs from IFRS 3 on key points)

- Increase transparency — users can see the true cost of the transaction and the premium paid (goodwill)

- Ensure consistency — one method for all commercial combinations

What the Acquisition Method Achieves

FRS 102 demands that an acquirer is always identified and that all identifiable assets and liabilities are brought onto the balance sheet at fair value. This creates a clean, consistent opening position for the acquired entity — one that reflects economic reality rather than historical book values.

The result is a balance sheet that stakeholders, lenders, and auditors can actually rely on.

Risks of Incorrect Application

Failing to apply the acquisition method correctly can lead to:

- Understated intangible assets — such as customer lists, brand value, technology not separated from goodwill

- Incorrect goodwill figures — inflating or deflating the balance sheet

- Misstated P&L — wrong amortisation charges affecting profitability

- Non-compliance — audit sign-off issues or covenant breaches

How the Acquisition Method Works Under FRS 102

The acquisition method is a four-stage process:

- Identify the acquirer

- Determine the acquisition date

- Recognise and measure identifiable assets and liabilities

- Recognise goodwill or gain from bargain purchase

Identify the Acquirer

The acquirer is the entity that obtains control over the acquiree — typically the entity that transfers cash, issues equity, or takes on obligations in exchange for ownership.

In complex group structures, identifying the acquirer requires judgment. The 2024 amendments to FRS 102 (effective 1 January 2026) add new guidance on identifying the acquirer in multi-party and reverse acquisition scenarios.

Determine the Acquisition Date

The acquisition date is when the acquirer effectively obtains control. This matters because:

- All assets and liabilities are measured as of this date

- Consideration transferred (including contingent consideration) is assessed at this point

Step 1: Identify and Measure Consideration Transferred

Consideration includes:

- Cash paid

- Fair value of shares issued

- Deferred payments

- Contingent consideration (e.g., earn-outs tied to future performance)

Critical difference from IFRS 3: Under FRS 102, directly attributable transaction costs such as legal or advisory fees are capitalised as part of the cost of the combination, not expensed as incurred. This treatment is consistent with old UK GAAP but differs from IFRS 3, where such costs are expensed.

Include contingent consideration when it is probable and reliably measurable. If it fails to meet these criteria at acquisition date but qualifies later, the adjustment goes to goodwill.

Step 2: Recognise and Measure Identifiable Assets and Liabilities

The acquirer must recognise all identifiable assets and liabilities at their acquisition-date fair values, including:

- Intangible assets not previously on the acquiree's books — customer relationships, trade names, technology

- Tangible assets — property, plant, and equipment

- Liabilities — debt, provisions, and contingent liabilities (if reliably measurable)

Specialist valuation support is typically needed here, particularly for intangibles where no active market exists. Purchase price allocation (PPA) demands significant judgement — getting it wrong affects both goodwill figures and ongoing amortisation charges.

Step 3: Calculate and Recognise Goodwill

Goodwill equals:

Consideration transferred + Fair value of NCI − Fair value of net identifiable assets acquired

If this results in a negative amount, it is a gain on bargain purchase, recognised immediately in profit or loss.

Example:

- Parent pays £800,000 to acquire 100% of a subsidiary

- Fair value of subsidiary's net identifiable assets: £600,000

- Goodwill = £800,000 − £600,000 = £200,000

Under FRS 102, this £200,000 goodwill must be amortised over its useful economic life — with a maximum of 10 years if the useful life cannot be reliably estimated.

Goodwill and Fair Value Adjustments Under UK GAAP

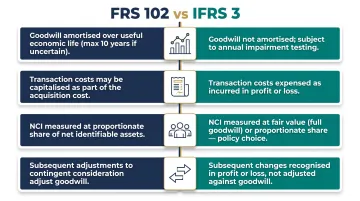

Goodwill Treatment: FRS 102 vs. IFRS 3

| Feature | FRS 102 | IFRS 3 |

|---|---|---|

| Amortisation required? | Yes, over finite useful life | No |

| Default cap if life not estimable | 10 years | N/A (impairment-only) |

| Annual impairment test? | Only if indicators exist | Yes, mandatory annually |

| Transaction costs | Capitalised | Expensed as incurred |

| NCI measurement | Proportionate share only | Fair value or proportionate share (choice) |

Under FRS 102, goodwill must be amortised systematically over its useful life. If the useful life cannot be reliably estimated, the maximum is 10 years. This creates a recurring P&L charge that directly affects profitability.

This differs fundamentally from IFRS 3, which prohibits amortisation and requires annual impairment testing instead.

Fair Value Adjustments and Intangible Assets

Each identifiable intangible asset separated from goodwill at acquisition must be recognised separately on the balance sheet, amortised over its own useful life, and recognised separately on the balance sheet, amortised over its own useful life, and tested for impairment if indicators arise.

The combined effect on post-acquisition P&L can be substantial, as the example below illustrates.

Example:

If a £500,000 acquisition includes:

- Brand value: £100,000 (10-year life)

- Customer list: £80,000 (5-year life)

- Goodwill: £320,000 (10-year life)

Annual amortisation would be:

- Brand: £10,000

- Customer list: £16,000

- Goodwill: £32,000

- Total: £58,000/year

Failing to separate intangibles from goodwill results in understated intangibles, overstated goodwill, and incorrect P&L charges.

The Measurement Period

FRS 102 allows a measurement period of up to 12 months from the acquisition date during which provisional fair values can be revised if new information emerges about conditions existing at the acquisition date.

- Changes within this period: Applied retrospectively

- Changes after this period: Treated as post-acquisition adjustments

Non-Controlling Interests (NCI)

Unlike IFRS, which allows a choice between measuring NCI at fair value or at the proportionate share of net identifiable assets, FRS 102 requires NCI to be measured at the proportionate share of identifiable net assets only. This affects the goodwill figure recognised.

Specialist Support for PPA

Accurate purchase price allocation is critical for complex acquisitions — errors in separating intangibles from goodwill flow through to years of misstated amortisation charges. VJM Global works with UK businesses on consolidation accounting and FRS 102 compliance, with particular experience supporting entities involved in cross-border transactions or group restructuring with an India dimension.

Common Misconceptions and When Merger Accounting Still Applies

Misconception 1: Merger Accounting Can Still Be Used for Commercial Mergers

FRS 102 does not permit merger accounting for arm's-length commercial mergers. It's only available for qualifying group reconstructions — such as:

- Inserting a new holding company above an existing group

- Transferring a subsidiary between group members

The qualifying conditions are strict:

- Same ultimate equity holders before and after

- No change in non-controlling interests

- Not prohibited by company law

On share issuance, Sections 611–612 of the Companies Act 2006 provide merger relief and group reconstruction relief from crediting the share premium account.

Misconception 2: All Intangible Assets Can Be Lumped Into Goodwill

FRS 102 requires separately identifiable intangible assets to be recognised apart from goodwill — they cannot be absorbed into a single goodwill figure. Failing to separate them results in:

- Understated intangibles

- Overstated goodwill

- Incorrect amortisation charges

Misconception 3: FRS 102 Mirrors IFRS 3

While the two frameworks share structural similarities, they diverge on several practical points that matter at the balance sheet level:

- Goodwill amortisation — FRS 102 requires it; IFRS 3 prohibits it

- Transaction costs — FRS 102 capitalises them; IFRS 3 expenses them

- NCI measurement — FRS 102 uses proportionate share only; IFRS 3 offers a choice

- Contingent consideration adjustments — FRS 102 adjusts goodwill; IFRS 3 uses profit or loss

Consolidation Exemptions

Beyond accounting treatment, it's worth knowing that not all companies must consolidate at all. Companies subject to FRS 105 (the micro-entities regime) do not need to produce consolidated accounts. Small parent companies may also qualify for an exemption under the Companies Act 2006 if they meet size thresholds.

New thresholds from 6 April 2025:

| Criterion | Threshold |

|---|---|

| Turnover (net) | Not more than £15M |

| Balance sheet total (net) | Not more than £7.5M |

| Average employees | Not more than 50 |

A company or group must meet at least 2 of the 3 criteria. Groups that now fall within these revised thresholds should review whether filing consolidated accounts remains a legal requirement for their next period.

Frequently Asked Questions

How do you record acquisition in accounting?

Under UK GAAP (FRS 102), an acquisition is recorded using the acquisition method: the acquirer recognises all identifiable assets and liabilities at fair value as of the acquisition date, with any excess of consideration over net fair value recognised as goodwill and amortised over its useful life.

What are the 4 types of acquisitions?

The four common acquisition types are horizontal (same industry), vertical (supply chain integration), conglomerate (unrelated sectors), and market extension/product extension. All four types follow the same FRS 102 acquisition method for accounting purposes.

What is the difference between merger accounting and acquisition accounting under FRS 102?

Acquisition accounting (the acquisition method) is mandatory for all commercial business combinations under FRS 102 and requires fair value recognition and goodwill calculation. FRS 102 only permits merger accounting for qualifying group reconstructions — not for arm's-length commercial mergers.

How is goodwill treated under FRS 102 compared to IFRS?

Under FRS 102, goodwill must be amortised over its useful economic life (capped at 10 years if the life cannot be estimated), creating a recurring P&L charge. Under IFRS 3, goodwill is not amortised but tested annually for impairment instead.

Who is exempt from preparing consolidated financial statements under UK GAAP?

Three groups are typically exempt: small parent companies meeting the Companies Act 2006 size thresholds, micro-entities under FRS 105, and intermediate parent companies whose own parent already prepares publicly available consolidated accounts covering the group.

What is the measurement period for business combinations under FRS 102?

FRS 102 allows up to 12 months from the acquisition date to finalise fair values. Provisional figures can be retrospectively adjusted if new information emerges about conditions that existed at acquisition date — after this window, any adjustments are treated as post-acquisition events.