Introduction

Picture a UK business owner signing the final papers on an acquisition, only to realise the purchase price is £500,000 higher than the value of the physical assets being acquired. What accounts for that difference?

This "excess" is goodwill — one of the most discussed yet misunderstood items in UK accounting. How you account for it depends entirely on your reporting framework. UK companies applying FRS 102 must amortise goodwill over its useful life, while those using IFRS 3 test it annually for impairment instead.

This guide covers:

- The definition and types of goodwill

- How goodwill is calculated

- Where it appears on the balance sheet

- How UK GAAP (FRS 102) and IFRS treatment differs in practice

Key Takeaways

- Goodwill arises when a business is acquired for more than the fair value of its net identifiable assets and liabilities

- It only appears on a balance sheet as a result of a transaction — internally generated goodwill is never recognised

- UK GAAP (FRS 102) requires amortisation over its useful life; IFRS 3 uses annual impairment testing instead

- Negative goodwill occurs when the purchase price is below the fair value of net assets

- Misclassifying or failing to amortise goodwill under FRS 102 can distort your balance sheet and trigger regulatory scrutiny

What is Goodwill in UK Accounting?

Goodwill in accounting terms is the excess of the consideration paid for a business over the aggregate fair value of its identifiable net assets and liabilities at the date of acquisition. The legal foundation used in UK practice comes from the 1901 case IRC v Muller & Co's Margarine, where Lord Macnaghten defined goodwill as "the benefit and advantage of the good name, reputation and connection of a business."

In practical terms, goodwill represents intangible value that buyers are willing to pay a premium for:

- Brand reputation and recognition

- Customer loyalty and relationships

- Employee expertise and relationships

- Proprietary processes and know-how

- Market position and competitive advantage

One distinction matters above all others: goodwill only arises from an external transaction (purchased goodwill). Internally generated goodwill — the value a business builds organically through reputation and customer relationships — cannot be recognised or capitalised on the balance sheet under UK accounting standards.

Both FRS 102 para 18.8C(f) and IAS 38 para 48 explicitly state that internally generated goodwill shall not be recognised as an asset. The reason: internally generated goodwill is not an identifiable resource, it cannot be separated from the business, and no reliable cost measurement exists.

Goodwill differs from other intangible assets (patents, trademarks, copyrights) in a fundamental way: those can be identified, measured, and recognised separately. Goodwill is a residual figure that captures everything else of value that cannot be separately identified.

Inherent Goodwill vs. Purchased Goodwill

Inherent (internally generated) goodwill is value built over time through reputation and customer relationships. It is not recorded in accounts because no transaction has taken place to confirm its value.

Purchased goodwill arises only when one entity acquires another and pays more than the fair value of identifiable net assets. This is the only type capitalised as an intangible asset on the acquirer's balance sheet, in line with both FRS 102 Section 19 and IFRS 3.

How is Goodwill Calculated in the UK?

The core formula is straightforward:

Goodwill = Purchase Price Paid − Fair Value of Net Identifiable Assets

Where Net Identifiable Assets = Assets minus Liabilities at the date of acquisition.

Fair Value Restatement Requirement

All identifiable assets and liabilities of the acquired business must be restated to their fair value at acquisition date (not book value) before the calculation. This often includes adjustments for:

- Property and equipment revalued to current market prices

- Inventory restated to fair value

- Previously unrecognised intangible assets such as customer lists or brand names

Step-by-Step Calculation Example

The following example walks through a typical UK acquisition:

Scenario: ABC Ltd acquires XYZ Ltd for £800,000.

Fair value of XYZ Ltd's assets and liabilities at acquisition:

- Identifiable assets (restated to fair value): £1,000,000

- Liabilities assumed: £400,000

- Net identifiable assets: £600,000

Goodwill calculation: £800,000 (purchase price) − £600,000 (net assets) = £200,000 goodwill

This £200,000 represents the premium ABC Ltd paid for XYZ Ltd's brand reputation, customer relationships, and other intangible value that cannot be separately identified.

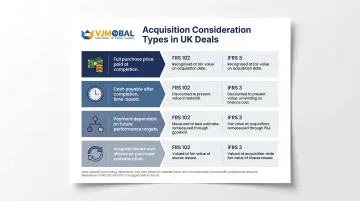

Types of Consideration

UK acquisitions can involve different consideration types, each with specific accounting treatment:

- Immediate cash payment: The amount paid in cash forms the purchase consideration directly.

- Deferred cash consideration: Recognised at present value using an appropriate discount rate to reflect the time value of money.

- Contingent consideration: Under FRS 102, included in the cost at acquisition if probable and reliably measurable. Under IFRS 3, recognised at fair value at acquisition date, with subsequent changes taken through profit or loss.

- Share-for-share exchanges: Valued at the acquirer's share price at acquisition date.

Negative Goodwill (Bargain Purchase)

Negative goodwill occurs when the purchase price falls below the fair value of net assets — meaning the business was acquired at a discount to its underlying worth.

Under both FRS 102 and IFRS 3, this must be reviewed carefully for errors before recognition:

- FRS 102: After reassessment, any remaining excess is recognised in profit or loss and presented below the goodwill heading on the balance sheet, released systematically over time

- IFRS 3: After reassessment, the gain is recognised immediately in profit or loss on the acquisition date

Partnership Goodwill in the UK

Goodwill also arises in UK partnership accounting when a new partner joins or an existing partner leaves. The accounting treatment ensures existing partners are compensated for the value they're giving up.

Standard double-entry treatment:

Step 1 — Goodwill is raised:

- Debit: Goodwill Account (agreed valuation)

- Credit: Partners' Capital Accounts in old profit-sharing ratio

Step 2 — Goodwill is written off:

- Debit: Partners' Capital Accounts in new profit-sharing ratio

- Credit: Goodwill Account

After both entries, the goodwill account carries a nil balance — no goodwill remains on the partnership balance sheet. As confirmed by ACCA, this approach transfers value between partners without leaving an intangible asset on the books.

How is Goodwill Recorded on the Balance Sheet?

Purchased goodwill is recognised as an intangible non-current asset on the acquirer's balance sheet, sitting within the intangible assets section. It's initially measured at cost — the amount paid above the fair value of net identifiable assets at acquisition.

The balance sheet figure represents the carrying amount, not the original acquisition-date value:

Under FRS 102: Carrying Amount = Cost − Accumulated Amortisation − Accumulated Impairment Losses

Under IFRS 3: Carrying Amount = Cost − Accumulated Impairment Losses (no amortisation)

When the purchase price falls below the fair value of net assets acquired, the result is negative goodwill — and its balance sheet treatment differs sharply from positive goodwill.

Negative Goodwill Presentation

Negative goodwill must not be presented as a negative asset. The treatment depends on the applicable framework:

Under FRS 102:

- Presented on the face of the balance sheet, below the goodwill line and clearly distinguished from it

- Released to the income statement systematically as the related non-monetary assets are recovered

Under IFRS 3:

- Not recognised on the balance sheet at all

- Recognised immediately as a gain in the income statement, but only after reassessment of the acquisition calculation

UK GAAP (FRS 102) vs IFRS 3: Goodwill Treatment After Acquisition

The choice between FRS 102 and IFRS 3 directly affects reported profits, balance sheet values, and the annual compliance burden — so understanding which applies to your business matters.

Which UK Entities Must Use Which Standard?

Under Companies Act 2006 s403(2), parent companies with securities admitted to trading on a UK regulated market must prepare group accounts under IFRS. All other UK entities may choose FRS 102. In practice, the vast majority of UK private companies use FRS 102.

FRS 102: Mandatory Amortisation

Under FRS 102, goodwill is amortised on a straight-line basis over its useful economic life. Key requirements:

- Useful life cannot be indefinite

- If useful life cannot be reliably estimated, a maximum default period of 10 years applies

- Each year's amortisation charge reduces both the goodwill asset and operating profit

IFRS 3: Impairment-Only Model

Under IFRS 3, goodwill is never amortised. Instead:

- Allocated to cash-generating units (CGUs)

- Tested annually for impairment, or more frequently if indicators exist

- Any impairment loss is charged to the income statement and cannot be reversed

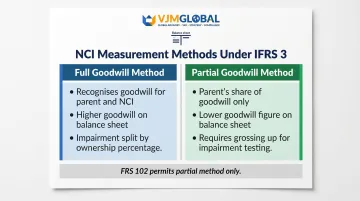

Non-Controlling Interest (NCI) Measurement Choice

Under IFRS 3 para 19, the acquiring entity can choose to measure NCI using one of two methods:

Full goodwill method (NCI at fair value):

- Recognises goodwill attributable to both parent and NCI

- Results in higher total goodwill on the balance sheet

- Impairment is split between the group and NCI in proportion to ownership

Partial goodwill method (NCI at proportionate share of net assets):

- Recognises only the parent's share of goodwill

- Lower goodwill figure on the balance sheet

- Requires "grossing up" of goodwill for impairment testing purposes

Under FRS 102, only the proportionate share method is permitted.

Practical Implications for UK Business Owners

The choice of reporting framework affects three areas in particular:

- FRS 102 amortisation creates predictable annual P&L charges; IFRS 3's impairment-only model preserves profits until a triggering event causes a potentially large, one-off write-down

- Goodwill balances and acquisition values appear differently on the balance sheet depending on which standard applies — relevant when presenting accounts to lenders or investors

- Annual impairment testing under IFRS 3 carries a heavier compliance burden than the trigger-based testing approach under FRS 102

Getting the framework choice wrong — or misapplying either standard — can distort reported profits and create compliance exposure. VJM Global has worked with 250+ UK businesses on exactly these reporting decisions, including cross-border acquisitions under both UK GAAP and IFRS.

Goodwill Impairment Under UK Accounting Standards

Impairment occurs when goodwill's recoverable amount falls below its carrying amount on the balance sheet. The recoverable amount is defined as the higher of two figures: fair value less costs to sell, and value in use. When this threshold is breached, an impairment loss must be recognised.

Common Impairment Triggers

UK businesses should review goodwill for impairment when any of these occur:

- Loss of key customers or contracts

- Departure of key management

- Deteriorating market conditions

- Regulatory changes affecting the business

- Underperformance against acquisition projections

- Economic downturn impacting the acquired business

Testing frequency differs by standard:

| Standard | Testing Requirement |

|---|---|

| FRS 102 | Annual review for indicators; detailed test only if indicators exist |

| IFRS 3 | Mandatory annual impairment test regardless of indicators |

Accounting Impact

The impairment loss is charged to the income statement, reducing both the goodwill asset and reported profit. Three points are worth understanding clearly:

- Income statement charge: The full impairment loss hits profit immediately in the period it is recognised

- NCI allocation (IFRS 3): If non-controlling interest was measured at fair value, the impairment is split between the group and NCI pro-rata based on ownership percentage

- No reversal permitted: Under FRS 102 para 27.28 and IAS 36 para 124, impairment losses on goodwill cannot be reversed — even if the acquired business fully recovers

This last point has real consequences for acquisition planning. A poorly performing acquisition can permanently reduce reported goodwill and profits, with no accounting remedy available later. Thorough due diligence before a deal closes is far more valuable than any post-impairment recovery.

Frequently Asked Questions

What is goodwill in accounting in the UK?

Goodwill is the excess of the price paid to acquire a business over the fair value of its identifiable net assets, representing intangible value such as brand reputation and customer loyalty. It only arises from acquisitions under both FRS 102 and IFRS 3.

How is goodwill calculated?

Goodwill = Purchase Price minus Fair Value of Net Identifiable Assets. All assets and liabilities of the acquired entity must first be restated to fair value at acquisition date before applying the formula.

What is the accounting entry for goodwill?

Debit Goodwill (intangible asset) and Credit Cash/Consideration Payable for the goodwill amount. In partnership contexts, Debit Goodwill Account and Credit Partners' Capital Accounts in the old profit-sharing ratio.

Where does goodwill go on a balance sheet?

Goodwill is listed under non-current intangible assets on the acquirer's balance sheet, shown at cost less accumulated amortisation (FRS 102) or less accumulated impairment losses (IFRS 3).

Is goodwill capitalised or expensed?

Purchased goodwill is capitalised as an intangible asset and then treated differently depending on the framework: FRS 102 requires gradual amortisation, while IFRS 3 keeps it on the balance sheet until an impairment loss occurs.

Does UK GAAP amortise goodwill?

Yes. FRS 102 requires goodwill to be amortised over its useful economic life — capped at 10 years if that life cannot be reliably estimated. IFRS 3 takes the opposite approach, prohibiting amortisation and requiring annual impairment testing instead.