Introduction

Singapore investors are pouring capital into Dubai's skyline at record pace—yet many discover too late that UAE real estate compliance carries serious financial exposure. Cross-border property investment from Southeast Asia to the UAE has surged, driven by the UAE's tax-efficient structure, freehold ownership zones, and 10-year Golden Visa incentives. But the appeal of Marina towers and Downtown penthouses doesn't protect investors from the compliance failures that follow poor accounting setup.

Singapore investors face a distinct challenge. The UAE operates under a regulatory and tax framework—International Financial Reporting Standards (IFRS), the Federal Tax Authority (FTA), and the Real Estate Regulatory Agency (RERA)—that differs fundamentally from Singapore's familiar territory.

The risks are concrete: misclassifying a commercial lease as VAT-exempt can trigger penalties reaching 300% of unpaid tax; failing to recognize a ground lease liability under IFRS 16 can derail audit readiness; and assuming your Singapore tax position mirrors your UAE structure can create unexpected IRAS disclosure gaps.

This guide covers exactly what Singapore investors need to get right—UAE accounting standards, VAT and corporate tax obligations, Singapore-side reporting, and the compliance pitfalls that catch first-time buyers off guard.

Key Takeaways

- UAE real estate accounting follows IFRS (full or SME tier, based on revenue)

- Commercial property attracts 5% VAT; first residential supply is zero-rated; resales are exempt

- 9% corporate tax applies to net profits above AED 375,000 for UAE entities

- Singapore's territorial tax system exempts most UAE rental income for individuals

- IFRS-compliant books and FTA/RERA compliance are mandatory from day one

UAE Accounting Standards and Framework: What Singapore Investors Must Know

The UAE mandates International Financial Reporting Standards (IFRS) for all financial reporting under Federal Decree-Law No. 32 of 2021. Entities with annual revenue up to AED 50 million may apply IFRS for SMEs; those under AED 3 million can use cash-basis accounting. Singapore investors must ensure their UAE holding entities comply from the first transaction. Retroactive compliance is not accepted.

Four primary authorities govern UAE real estate accounting and compliance:

Key Regulatory Bodies

You'll interact with four primary authorities:

- Federal Tax Authority (FTA): Administers VAT and corporate tax registration, returns, and penalties

- RERA (Real Estate Regulatory Agency): Regulates developers, escrow accounts, and broker licensing in Dubai

- Dubai Land Department (DLD): Registers property ownership and transfers; maintains the official property register

- UAE Ministry of Economy: Oversees company registration and enforcement of Commercial Companies Law

Accrual Accounting Under IFRS

Accrual-basis accounting is the IFRS-compliant standard. Unlike cash accounting (which records transactions when money moves), accrual accounting matches rental income against expenses in the same period and recognizes obligations as they arise. For property ownership scenarios, this means:

- Rental income is recorded when due, not when received

- Expenses are recognized when incurred, not when paid

- Depreciation, lease liabilities, and revenue recognition follow IFRS timing rules

IFRS 16 Lease Accounting

If your UAE property sits on a long-term ground lease (common in many freehold zones), IFRS 16 requires recognition of right-of-use (ROU) assets and lease liabilities on your balance sheet. Many first-time UAE investors miss this requirement entirely, treating ground leases as off-balance-sheet arrangements. Where investment properties are held on leased land, the ROU asset is classified as investment property — and if you apply the fair value model under IAS 40, that same fair value basis must apply to ROU assets.

Mandatory Record Retention

UAE tax law requires financial records to be maintained for 15 years for real estate transactions—more than double the general 7-year requirement. This applies whether you're based in the UAE or managing the investment remotely from Singapore. Set up a dedicated archival system from day one.

Tax Obligations in the UAE: VAT and Corporate Tax for Property Investors

UAE VAT Framework for Real Estate

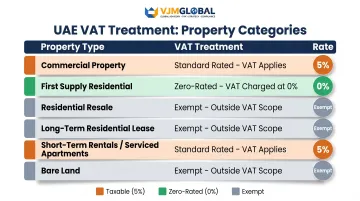

The UAE applies 5% Value Added Tax (VAT) across most commercial property transactions, but residential property treatment is nuanced:

| Property Type | VAT Treatment | Rate |

|---|---|---|

| Commercial property sale/lease | Standard rated | 5% |

| First supply of new residential property (within 3 years of completion) | Zero-rated | 0% |

| Subsequent residential sale (resale) | Exempt | N/A |

| Long-term residential lease | Exempt | N/A |

| Short-term rentals / serviced apartments | Standard rated | 5% |

| Bare land | Exempt | N/A |

Critical distinction: Furnished holiday homes, serviced apartments, and hotel-style accommodations are explicitly excluded from the "residential" definition and treated as commercial supplies at 5%. Misclassifying these triggers fixed penalties of AED 1,000-2,000 plus percentage-based assessments.

VAT Registration Thresholds

- Mandatory registration: AED 375,000 annual taxable supplies

- Voluntary registration: AED 187,500 annual taxable supplies or expenses

- Non-resident landlords: Must register regardless of threshold (NIL threshold)

Once registered, you'll file quarterly returns if annual turnover is below AED 150 million, or monthly if above.

UAE Corporate Tax (Effective June 2023)

Federal Decree-Law No. 47 of 2022 imposes:

- 0% on taxable income up to AED 375,000

- 9% on taxable income exceeding AED 375,000

Key exemption for individuals: Natural persons earning real estate investment income in their personal capacity are excluded from corporate tax under Cabinet Decision No. 49 of 2023. This exclusion has no upper income limit, provided you're not operating through a commercial license.

Singapore individuals holding UAE property personally face no UAE income tax. However, if you structure holdings through a UAE LLC, free zone company, or offshore entity, corporate tax applies above the AED 375,000 threshold.

Free Zone Corporate Tax Advantage

Qualifying Free Zone Persons pay 0% on Qualifying Income. Conditions include:

- Specific substance requirements (physical office, staff, core activities performed in UAE)

- Audited financial statements maintained

- No mainland UAE income (with limited exceptions)

Some Singapore investors structure holdings through free zones for this 0% rate. The substance requirements are non-negotiable: the FTA audits free zone entities for genuine operational presence, and failures result in reclassification to the 9% rate with back-assessment.

Deductible Expenses

Operational expenses reduce taxable income, including:

- Property maintenance and repairs (revenue nature)

- Third-party management fees

- Depreciation (per IFRS rules; deemed depreciation available for fair-value investment property)

- Interest and financing costs (subject to 30% EBITDA cap or AED 12 million safe harbor)

- Recoverable input VAT is non-deductible

During an FTA review, auditors typically request 5 years of supporting documentation — invoices, contracts, bank records, and depreciation schedules. Maintaining IFRS-compliant books from day one avoids costly reconstructions later.

Singapore-UAE Cross-Border Tax Considerations

Singapore's Territorial Tax System

Singapore taxes income on a territorial basis. Overseas income received in Singapore is generally not taxable for individuals. UAE-derived rental income remitted to a Singapore bank account typically escapes Singapore tax.

One exception applies: if IRAS determines you're "trading in properties" — assessed via frequency, holding period, and motive — gains may become taxable as income. Singapore does not impose capital gains tax on property sales deemed capital in nature.

Singapore-Incorporated Companies

Foreign income is taxable when remitted to and received in Singapore. Tax exemption under Section 13(8) requires:

- Income was subject to tax in the foreign jurisdiction

- Headline tax rate in the foreign jurisdiction is at least 15%

- The Comptroller is satisfied the exemption is beneficial

The UAE's 9% corporate tax rate falls below the 15% threshold, meaning automatic S13(8) exemption may not apply. Double Taxation Relief or Unilateral Tax Credit may still reduce the liability. Even so, corporate structures carry double-taxation exposure that individual ownership avoids entirely.

This exposure makes the UAE-Singapore DTA especially relevant for corporate investors.

UAE-Singapore Double Tax Agreement (DTA)

A comprehensive DTA exists, effective 30 August 1996. Withholding tax rates under the agreement:

- Dividends: 0%

- Interest: 0%

- Royalties: 0%/5%

The UAE currently imposes 0% withholding tax on dividends, interest, and royalties paid to foreign investors, making profit repatriation to Singapore straightforward.

Currency and Foreign Exchange Accounting

UAE accounts are maintained in AED; Singapore investors may report in SGD. Under IAS 21 (Foreign Currency Translation), the functional currency is typically AED for a UAE property entity.

Where the presentation currency is SGD — for consolidation into a Singapore parent — apply the closing rate method:

- Assets and liabilities: closing exchange rate at the reporting date

- Income and expenses: exchange rates at transaction dates, or average rates

- Exchange differences: recognized in other comprehensive income (OCI)

Inconsistent FX treatment across periods can produce mismatched consolidation figures and trigger compliance queries on both sides of the arrangement.

Key Accounting Records and Financial Reporting Requirements

Core Financial Documents

Your UAE real estate entity must produce:

- Income statement: Rental income, property-related revenue, operating expenses

- Balance sheet: Property assets, liabilities, equity

- Cash flow statement: Operating, investing, and financing activities

Entities with revenue exceeding AED 50 million must prepare audited financial statements by a UAE-registered auditor. Outsourcing to a firm with UAE expertise, like VJM Global, keeps records audit-ready without requiring your physical presence in Dubai.

RERA Escrow Account Reporting

If you're engaged in development or off-plan sales, Law No. 8 of 2007 mandates:

- Separate escrow account for each project with a DLD-accredited bank

- 100% of buyer payments deposited to escrow

- Withdrawals allowed only per construction milestones, requiring RERA approval

- 5% retention of total escrow value held for one year after project completion

- Funds legally ring-fenced from developer creditors

Mixing project funds with general accounts violates RERA regulations and can result in project suspension or revocation of your developer registration.

Revenue Recognition Nuances

Revenue timing rules vary by property type:

- Rental income is recognized when rent falls due, not when payment arrives

- Development projects follow the percentage-of-completion method under IFRS 15, provided you have an enforceable right to payment for work completed to date

- If that IFRS 15 criterion isn't met, revenue is recognized only at handover, when control transfers to the buyer

Incorrect revenue recognition timing is a common audit red flag.

How to Structure Your UAE Real Estate Investment as a Singapore Investor

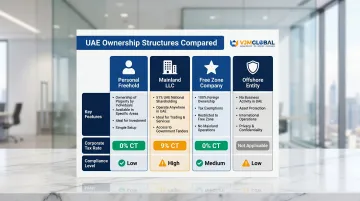

Main Ownership Structures

| Structure | Key Features | Accounting/Tax Implications |

|---|---|---|

| Personal freehold | Full ownership in designated zones; no corporate entity | Simplest reporting; excluded from corporate tax; must track rental income/expenses |

| Mainland LLC | 100% foreign ownership permitted; requires trade license | Full corporate compliance; annual audit if revenue exceeds AED 50M; 9% CT above AED 375,000 |

| Free zone company | 100% foreign ownership; zone-specific regulations | 0% CT on qualifying income if substance met; full audit and CT filing required |

| Offshore entity (RAK ICC, JAFZA Offshore) | Asset-holding vehicle; no physical office required | Limited to holding assets; may simplify structure but still requires UAE compliance |

Each structure carries distinct compliance obligations — the accounting treatment of your property depends heavily on which entity (if any) holds it.

Freehold vs. Leasehold: Accounting Treatment

- Freehold property: Recorded as an asset at cost (or fair value under IAS 40 if held as investment property)

- Leasehold interest: Requires IFRS 16 treatment (ROU asset and lease liability)

Investment property held for capital appreciation or rental income is accounted for under IAS 40, which allows either:

- Cost model: Carried at cost less accumulated depreciation and impairment

- Fair value model: Carried at fair value with changes recognized in profit or loss

Even under the cost model, fair value must be disclosed.

Golden Visa Opportunity

Your choice of ownership structure can also intersect with residency. Singapore investors who purchase UAE real estate valued at AED 2 million or more qualify for a 10-year Golden Visa. This affects your UAE tax residency status, which can in turn trigger changes to your Singapore tax residency classification and IRAS reporting obligations. A cross-border tax advisor can assess how the UAE-Singapore DTA applies to your situation and whether any additional disclosures are required before you finalise the investment.

Common Accounting Mistakes Singapore Investors Make in the UAE

VAT Misclassification

Treating a commercial lease as VAT-exempt, or failing to charge VAT on a short-term residential rental that qualifies as taxable, is the primary compliance risk. The FTA's penalty schedule for VAT misclassification includes:

- Fixed penalties of AED 1,000–2,000 per violation

- Percentage-based assessments on the misclassified amount

- Late payment surcharges that can reach 300% of unpaid tax

Mixing Personal and Investment Funds

Singapore investors who hold UAE property personally and commingle personal spending with property expenses compromise accounting integrity. Maintain a dedicated UAE business bank account for all property-related transactions.

Delaying Accounting Setup

This third mistake often compounds the first two. Many investors delay establishing proper bookkeeping until facing an audit or filing deadline. IFRS-compliant books must be maintained from the date of the first transaction, not assembled retroactively. Late or inaccurate filings carry FTA penalties that compound rapidly.

Frequently Asked Questions

What accounting standard does the UAE use?

The UAE requires International Financial Reporting Standards (IFRS) for financial reporting, with IFRS for SMEs available for entities with revenue up to AED 50 million. All real estate companies — including those held by foreign investors — must follow this framework.

What type of accounting is used in real estate in the UAE?

Accrual-basis accounting under IFRS is required. This covers revenue recognition for rental income and off-plan sales (using the percentage-of-completion method), lease accounting under IFRS 16, and investment property accounting under IAS 40 — either the cost model or the fair value model.

Do Singapore investors pay tax on UAE rental income in Singapore?

Singapore's territorial tax system generally does not tax overseas-sourced income for individuals, and the UAE currently imposes no withholding tax on income paid to foreign investors. That said, your specific position can vary based on entity type and remittance structure — confirm with a cross-border tax advisor before assuming no liability.

Do Singapore real estate investors in the UAE need to register for VAT?

VAT registration is mandatory if UAE taxable supplies exceed AED 375,000 annually. Commercial property rentals and sales attract 5% VAT. Certain residential transactions are zero-rated or exempt, so review your portfolio's mix carefully before assuming no VAT obligation applies.

Does UAE corporate tax apply to Singapore investors holding real estate?

The UAE introduced a 9% corporate tax effective June 2023, applicable to juridical persons earning taxable income above AED 375,000. Singapore investors holding UAE property through a UAE-registered entity should assess their corporate tax exposure — certain qualifying free zone structures may attract a 0% rate, but conditions apply.