Introduction: UAE VAT and Singapore Businesses — Why This Matters

Singapore-UAE bilateral trade in goods reached S$27.94 billion in 2025, according to Enterprise Singapore — a volume that puts UAE VAT compliance squarely on the agenda for any Singapore business selling into that market. As more Singapore companies expand into or supply the UAE, understanding VAT obligations has become essential, not optional.

Here's the critical misconception: many Singapore business owners assume the UAE's AED 375,000 registration threshold applies to them the same way it applies to UAE-resident businesses. It does not. Non-resident foreign companies, including Singapore-registered entities, face fundamentally different rules. Those rules can trigger immediate VAT registration obligations from the very first dirham of taxable supply.

This guide covers:

- UAE VAT thresholds and how they apply to resident vs. non-resident businesses

- The special non-resident rule and why Singapore companies are directly affected

- Specific scenarios that trigger registration obligations

- The UAE VAT registration process for foreign entities

- Upcoming e-invoicing requirements to plan for

Whether you're exporting goods, selling SaaS subscriptions, or providing professional services to UAE clients, you need to know where you stand.

TLDR: Key Takeaways

- Mandatory UAE VAT threshold for UAE-resident businesses is AED 375,000/year; voluntary threshold is AED 187,500/year

- Non-resident businesses have no registration threshold: VAT registration is required immediately upon making taxable supplies when the UAE customer cannot self-account

- UAE VAT rate is 5%; some supplies are zero-rated (0%) or exempt

- Failure to register carries an AED 10,000 penalty plus retroactive tax liability

- E-invoicing becomes mandatory from January 2027 for larger businesses; July 2027 for all others

UAE VAT Basics: A Quick Primer for Singapore Business Owners

The UAE introduced VAT on 1 January 2018 at a standard rate of 5%, enacted under Federal Decree-Law No. 8 of 2017 and administered by the Federal Tax Authority (FTA). Singapore's GST currently sits at 9% (effective 1 January 2024), which is nearly twice the UAE rate — a useful reference point when assessing your cross-border tax exposure.

Understanding how the UAE classifies different types of supplies is essential before you assess your registration obligations. UAE VAT divides all supplies into three categories:

Three VAT Categories

| Category | Rate | Examples |

|---|---|---|

| Standard-rated | 5% | Most goods and services supplied in the UAE |

| Zero-rated | 0% | Exports outside GCC states; international transport; first supply of residential property; certain healthcare and education services |

| Exempt | No VAT | Certain financial services; subsequent supply of residential real estate; bare land; local passenger transport |

Why this matters for registration: The zero-rated vs. exempt distinction directly affects your threshold calculation:

- Zero-rated supplies — classified as taxable supplies, so they count toward the VAT registration threshold

- Exempt supplies — not considered taxable, so they do not count toward the threshold

When assessing whether you need to register, include zero-rated transactions but exclude exempt ones.

UAE VAT Registration Thresholds Explained

Mandatory Registration Threshold

UAE-resident businesses must register for VAT when:

- Taxable supplies and imports exceed AED 375,000 over the previous 12 months, or

- The business anticipates exceeding this amount in the next 30 days

SGD equivalent: Approximately SGD 131,250 to SGD 133,500 (using an exchange rate of 1 AED = 0.35 SGD; verify current rates before planning).

Once this threshold is crossed, the business has 30 days to apply for VAT registration through the FTA's EmaraTax portal.

Voluntary Registration Threshold

Businesses may apply for voluntary registration at AED 187,500 (approximately SGD 65,625 to SGD 66,750) if:

- Taxable supplies and imports, or taxable expenses, in the previous 12 months exceed AED 187,500, or

- The business anticipates exceeding this amount in the next 30 days

Voluntary registration offers three practical advantages:

- Enables input VAT recovery on business expenses

- Useful for startups incurring costs before generating revenue

- Demonstrates VAT compliance credibility to UAE partners

What Counts Toward the Threshold?

Not all supply types count toward either threshold. Here's how they break down:

| Supply Type | Counts Toward Threshold? |

|---|---|

| Standard-rated supplies (5%) | ✅ Yes |

| Zero-rated supplies (0%) | ✅ Yes |

| Exempt supplies | ❌ No |

These thresholds apply specifically to UAE-resident businesses — entities with a UAE trade license and physical presence. Singapore companies without a UAE entity fall under a separate non-resident registration framework, covered in the next section.

The Critical Exception: How the Rules Differ for Non-Resident Foreign Businesses

Here's the rule that catches most Singapore businesses off guard:

The AED 375,000 mandatory registration threshold does NOT apply to non-resident businesses. According to UAE VAT law and confirmed by the FTA, a foreign company (including a Singapore-registered entity) that makes taxable supplies in the UAE where the customer is not required to self-account for VAT must register immediately—from the first dirham of taxable supply.

The Reverse Charge Mechanism

The reverse charge mechanism (Article 48, Federal Decree-Law No. 8 of 2017) provides an alternative—but only under specific conditions.

If a Singapore business provides services to a UAE VAT-registered business (B2B), the UAE client applies reverse charge VAT and self-accounts for it. The Singapore supplier does not need to register.

This protection disappears, however, when the Singapore business supplies to:

- UAE end-consumers (B2C)

- Non-registered UAE businesses

- UAE individuals

In these cases, reverse charge does not apply. The Singapore business must register for UAE VAT and charge VAT directly.

Situations That Trigger Non-Resident Registration

You must register immediately if you:

- Sell goods directly to UAE consumers (for example, via e-commerce)

- Provide SaaS or digital services to UAE retail subscribers

- Supply consulting, legal, or professional services to UAE individuals or small unregistered businesses

- Sell any taxable supplies where your UAE customer cannot self-account

Example: When reverse charge protects you A Singapore marketing agency contracted by a Dubai-based, VAT-registered firm to run a digital campaign. The Dubai client has a valid Tax Registration Number (TRN), self-accounts for VAT via reverse charge, and the Singapore agency does not need to register.

Example: When you must register The same Singapore agency provides consulting to a UAE startup that hasn't yet registered for VAT. No reverse charge applies—the Singapore agency must register for UAE VAT before invoicing.

Practical Implication

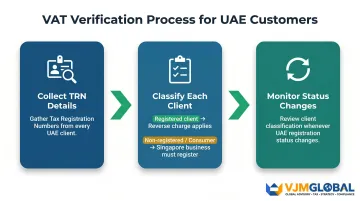

These scenarios make one action non-negotiable: Singapore businesses must map their UAE customer base before invoicing a single client.

- Collect TRN details from every UAE client

- Classify each as registered (reverse charge applies) or non-registered/consumer (you must register)

- Review the classification whenever a client's registration status changes

Missing this step means operating outside UAE VAT law—with penalties that apply from the first unregistered taxable supply.

Scenarios: Does Your Singapore Business Need to Register for UAE VAT?

Scenario 1: Goods Exporter Selling to UAE Consumers

Situation: A Singapore e-commerce company selling consumer electronics directly to UAE customers via an online store.

VAT obligation: The UAE applies no de minimis import threshold. VAT at 5% applies to the customs value (CIF—Cost, Insurance, Freight) of all imported goods regardless of value. If you're not VAT-registered, UAE customs collects VAT at import. If you are registered, you charge VAT to customers and file returns.

Registration requirement: Must register immediately before the first taxable supply.

Scenario 2: Digital/SaaS Company with UAE Retail Subscribers

Situation: A Singapore SaaS provider offering project management software to UAE subscribers, including individual freelancers and small businesses.

VAT obligation: There is no VAT registration threshold for non-resident providers of digital services to UAE consumers. The FTA requires foreign digital service providers to register immediately, with no simplified registration process available.

Registration requirement: Mandatory from the first subscriber who is not VAT-registered or is a consumer.

Scenario 3: Professional Services Firm with UAE Clients

Situation: A Singapore accounting firm providing bookkeeping and advisory services to UAE clients.

Key question: Are your UAE clients VAT-registered?

If yes (client is VAT-registered):

- Reverse charge applies

- UAE client self-accounts for VAT

- Singapore firm does not need to register

- Action: Collect and verify TRN details from all UAE clients

If no (client is not registered or is an individual):

- No reverse charge

- Singapore firm must register for UAE VAT

- Action: Register before invoicing the first non-registered client

Scenario 4: Setting Up a UAE Branch or Subsidiary

Situation: A Singapore company establishes a UAE branch office or subsidiary with a UAE trade license.

VAT treatment: Once a UAE legal presence is established, the entity is treated as a UAE-resident business subject to:

- Standard AED 375,000 mandatory registration threshold

- AED 187,500 voluntary registration threshold

Before choosing between a branch, subsidiary, or distributor model, it's worth assessing how each structure affects your VAT obligations and compliance burden from day one. Getting the entity structure right at the outset can significantly reduce administrative costs as you scale into the UAE market.

How to Register for UAE VAT as a Foreign Business

Registration Process

Applications are submitted online through the FTA's EmaraTax portal: https://eservices.tax.gov.ae/

Steps:

- Create an EmaraTax account

- Complete the taxable person profile

- Select the non-resident registration option

- Upload required documents

- Await FTA review (5-20 business days)

- Receive your 15-digit Tax Registration Number (TRN)

Required Documents

- Certificate of incorporation or Memorandum of Association

- Valid trade license (or foreign equivalent)

- Passport copies of owners and authorized signatories

- Emirates ID copies (if applicable)

- Power of Attorney (if using a representative)

- Bank account confirmation letter with company name and IBAN

- Proof of taxable supplies in UAE (invoices, contracts, or anticipated supply evidence)

- Description of business activities

Tax Agent or UAE Representative

Non-resident businesses typically engage a UAE-based tax agent or authorized representative to manage registration and compliance. The FTA does not explicitly require this for all cases, but businesses without UAE staff will find local expertise essential for accurate, on-time filings.

Post-Registration Obligations

Filing frequency and payment deadlines:

| Turnover | Filing Cycle | Payment Deadline |

|---|---|---|

| Below AED 150 million | Quarterly | 28 days after tax period ends |

| AED 150 million and above | Monthly | 28 days after tax period ends |

All returns and payments are submitted via the EmaraTax portal.

Invoice requirements: VAT-registered businesses must issue tax-compliant invoices showing:

- Supplier TRN

- Tax invoice number and date

- Description of goods/services

- VAT amount charged separately

- Total amount payable

2026 E-Invoicing Mandate

From 1 July 2026, the UAE launches a pilot e-invoicing system. Mandatory adoption follows in phases:

| Phase | Date | Target Group |

|---|---|---|

| Phase 1 | 1 July 2026 | Pilot businesses (voluntary) |

| Phase 2 | 1 January 2027 | Revenue ≥ AED 50 million (mandatory) |

| Phase 3 | 1 July 2027 | All other businesses (mandatory) |

Technical requirements:

- Structured XML format following the PINT AE (Peppol International Invoice for UAE) schema

- Transmission via the Peppol 5-corner model

- Use of Ministry of Finance-accredited Accredited Service Providers (ASPs)

Deadlines to appoint an ASP:

- Businesses with revenue ≥ AED 50 million: 31 July 2026

- Smaller businesses: 31 March 2027

Singapore businesses registering for UAE VAT now have firm ASP appointment deadlines to meet — build e-invoicing readiness into your registration timeline from the start.

Key Penalties Singapore Businesses Must Avoid

The UAE updated its penalty framework under Cabinet Decision No. 49 of 2021 (effective 28 April 2021). These are the violations Singapore businesses are most likely to encounter:

| Violation | Penalty |

|---|---|

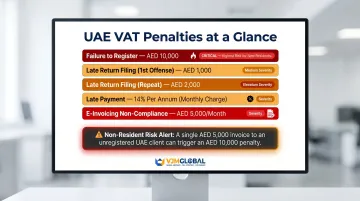

| Failure to register on time | AED 10,000 |

| Late VAT return filing (first offense) | AED 1,000 |

| Late VAT return filing (repeat within 24 months) | AED 2,000 |

| Late payment (from 14 April 2026) | 14% per annum monthly charge |

| E-invoicing non-compliance | AED 5,000/month for failure to implement; AED 100 per non-compliant invoice (capped at AED 5,000/month) |

Why Non-Residents Face Higher Risk

Penalty exposure for non-resident Singapore businesses tends to be higher because they may not realize registration was required in the first place. Unlike UAE-resident businesses, there is no threshold safety net for non-residents. A Singapore consultancy invoicing AED 5,000 for a single project to a non-registered UAE client could face a AED 10,000 registration penalty: twice the value of the work itself.

Voluntary Disclosure Option

The FTA's voluntary disclosure mechanism (Form 211 via EmaraTax) lets businesses self-report errors before an FTA audit triggers them.

Penalty structure (from 14 April 2026):

- Voluntary disclosure: 1% monthly on the tax difference

- Errors discovered during FTA audit: 50% fixed penalty on error amount plus 4% monthly from original due date

If you discover late registration, underreported VAT, or other errors, voluntary disclosure typically results in far lower penalties than waiting for an audit to surface them.

Frequently Asked Questions

What is the mandatory VAT registration threshold in the UAE?

The mandatory threshold is AED 375,000 in annual taxable supplies and imports for UAE-resident businesses, with a 30-day registration deadline once crossed. This threshold does not apply to non-resident foreign businesses.

What is the turnover threshold for voluntary VAT registration in the UAE?

The voluntary threshold is AED 187,500, applicable where taxable supplies/imports or business expenses exceed this amount. Registering voluntarily allows early input tax recovery and demonstrates compliance credibility.

Who is required to register for VAT in the UAE?

UAE-resident businesses with taxable supplies exceeding AED 375,000 and non-resident foreign businesses making taxable B2C supplies or supplies to non-registered UAE entities—regardless of value.

What is the VAT charge for voluntary disclosure in the UAE?

Voluntary disclosure allows businesses to self-correct past VAT errors with reduced penalties. From 14 April 2026, the penalty is 1% monthly on the tax difference—significantly lower than the 50% fixed penalty plus 4% monthly for audit-discovered errors.

Who is exempt from VAT in the UAE?

No businesses are broadly exempt. Certain supply categories are exempt, including certain financial services, residential real estate (subsequent supply), bare land, and local passenger transport. Exemption applies to the transaction type, not the business itself.

What are the new VAT rules in the UAE for 2026?

Two key updates are in effect: a five-year time limitation on excess input VAT refund claims took effect in January 2026, and mandatory e-invoicing launches 1 January 2027 for B2B and B2G transactions (businesses with revenue ≥ AED 50 million), with full rollout by 1 July 2027.

Final Word

UAE VAT compliance for Singapore businesses hinges on one critical distinction: whether your UAE customers can self-account for VAT via reverse charge. If they cannot—because they're consumers, individuals, or non-registered entities—you must register immediately, regardless of transaction value.

Getting this wrong carries real cost—the AED 10,000 late registration penalty alone outweighs the administrative effort of compliance. Before your first taxable UAE supply:

- Assess your customer base to identify non-registered buyers

- Collect TRN details from all UAE business clients

- Register proactively rather than waiting for a threshold trigger

For Singapore businesses navigating UAE market entry or cross-border tax obligations, VJM Global provides international tax planning, compliance advisory, and business setup services across multiple jurisdictions. Contact us at info@vjmglobal.com or +91 98915 76441 to discuss your UAE VAT registration and compliance strategy.