Introduction

Mishandling UK VAT as a Singapore business can trigger compliance penalties, unexpected registration costs, or rejected invoices from UK clients. In most B2B transactions, this is entirely avoidable — because the reverse charge mechanism shifts VAT responsibility to the UK buyer, not you.

Both countries operate consumption tax systems — Singapore's GST and the UK's VAT — but the reverse charge rules remain widely misunderstood among Singapore exporters and service providers. The confusion typically comes down to a few recurring problems:

- Invoicing without the correct "reverse charge" statement

- Misclassifying a B2C sale as a B2B transaction (or vice versa)

- Assuming the mechanism eliminates all UK VAT registration obligations

This guide explains what the UK VAT reverse charge is, when it applies to Singapore businesses, how to invoice correctly, and when UK VAT registration is still required.

Key Takeaways

- Under the UK VAT reverse charge, the UK buyer handles VAT reporting — Singapore sellers don't charge VAT on qualifying B2B sales

- Applies when the UK buyer is VAT-registered, purchasing for business use, and the supply covers services or specified goods under HMRC rules

- Invoices must omit VAT but include a "reverse charge" notation and the buyer's UK VAT registration number

- Does not apply to UK consumers (B2C) or non-VAT-registered buyers — standard UK VAT rules or direct registration may apply instead

- Post-Brexit, Singapore suppliers are treated the same as any non-UK, non-EU seller; rules are governed by UK domestic law

What Is UK VAT Reverse Charge?

The UK VAT reverse charge is a mechanism where the buyer — not the seller — accounts for and reports VAT to HMRC on qualifying transactions. The supplier issues an invoice at 0% VAT, and the UK buyer self-assesses the correct VAT rate (20% standard rate) on their VAT return.

This differs from standard VAT transactions. Normally, the supplier charges VAT, collects it from the buyer, and remits it to HMRC. Under the reverse charge, that collection step is bypassed entirely.

HMRC introduced the reverse charge primarily to counter Missing Trader fraud — where sellers collect VAT and disappear without remitting it. Shifting VAT responsibility to the buyer creates VAT-neutral B2B transactions, removing the opportunity for that fraud entirely.

Two main contexts for UK reverse charge:

- Cross-border B2B services — applies when overseas suppliers, including Singapore businesses, sell to UK VAT-registered buyers

- Domestic UK sectors — covers fraud-prone industries: construction, mobile phones, computer chips, wholesale energy, emissions allowances, and telecommunications

How UK VAT Reverse Charge Works: A Step-by-Step Breakdown

The end-to-end process works like this:

- Singapore business provides services or goods to a UK VAT-registered business

- Singapore business issues an invoice with no VAT charged

- UK buyer applies the 20% UK VAT rate on their own VAT return

- UK buyer simultaneously claims this as input tax

- Net VAT impact on the UK buyer is zero for fully taxable businesses — but HMRC has full visibility throughout

The "place of supply" rule drives the mechanism. For most B2B services, the place of supply is where the customer (UK buyer) is located — meaning UK VAT applies even if the Singapore supplier has no UK presence and isn't UK VAT-registered.

VAT registration threshold: If a UK business purchases services from a Singapore supplier before becoming VAT-registered, those purchase values still count toward the £90,000 registration threshold (effective from 1 April 2024).

Step 1: Singapore Business Issues the Invoice

The Singapore supplier issues an invoice showing:

- Net price of goods or services (no VAT charged)

- Statement that reverse charge applies

- UK buyer's VAT registration number

This documentation isn't optional — it serves as evidence of correct treatment and protects both parties from compliance issues.

Step 2: UK Buyer Self-Assesses VAT

The UK VAT-registered buyer calculates VAT at 20% standard rate and enters it as:

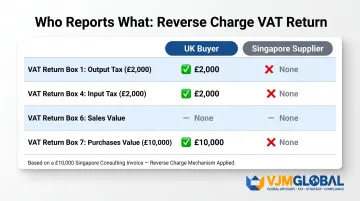

- Box 1: Output tax (VAT due on sales) — £2,000

- Box 4: Input tax (VAT reclaimed on purchases) — £2,000

- Net VAT impact: £0 for fully taxable businesses

Step 3: UK Buyer Reports on VAT Return

The UK buyer also records the net purchase value in Box 7 (total inputs). The Singapore supplier has no UK VAT return obligation for this transaction and doesn't report in Box 6. That box applies only if the overseas supplier is UK VAT-registered.

Example: A Singapore consulting firm charges £10,000 to a UK company

| VAT Return Box | UK Buyer Entry | Singapore Supplier Entry |

|---|---|---|

| Box 1 (Output tax) | £2,000 | None |

| Box 4 (Input tax) | £2,000 | None |

| Box 6 (Sales value) | None | None (not UK VAT-registered) |

| Box 7 (Purchases value) | £10,000 | None |

When Does UK Reverse Charge Apply to Singapore Businesses?

Scenario 1: B2B Services to UK Clients

For most cross-border services (consulting, software development, marketing, IT, and professional services) the reverse charge applies when the UK buyer is VAT-registered and purchasing for business use. The Singapore seller doesn't charge UK VAT and doesn't need UK VAT registration to supply these services compliantly.

Scenario 2: Specified Goods to UK VAT-Registered Buyers

Certain domestic reverse charge goods categories trigger the mechanism when supplies exceed relevant thresholds:

- Mobile phones in bulk (above £5,000 per invoice)

- Computer chips (above £5,000 per invoice)

- Wholesale gas/electricity (no threshold)

- Emission allowances (no threshold)

- Renewable energy certificates (no threshold)

- Wholesale telecoms (no threshold)

The £5,000 de minimis threshold applies only to mobile phones and computer chips, calculated per invoice on a VAT-exclusive basis.

Required Conditions Checklist

All three conditions must be met:

- ✅ UK buyer must be VAT-registered or liable to be registered

- ✅ Purchase must be for business purposes (not personal)

- ✅ Supply must fall within HMRC-specified categories

When Reverse Charge Does NOT Apply

The reverse charge does not apply in two key situations:

- B2C sales to UK consumers — individual buyers without VAT registration require the Singapore seller to charge UK VAT, which typically means registering for UK VAT once supplies exceed the registration threshold

- Sales to non-VAT-registered UK businesses — the mechanism only activates when the UK buyer holds (or is liable for) VAT registration

Post-Brexit Context for Singapore Businesses

Singapore was never part of the EU, so Brexit didn't materially change how UK reverse charge applies to Singapore suppliers. Singapore businesses have always been treated as non-EU overseas suppliers, and the same cross-border reverse charge logic continues to apply.

In practice, Brexit matters most to EU-based sellers, who were reclassified to match the rules Singapore businesses have operated under all along.

How to Create a Compliant Reverse Charge Invoice as a Singapore Business

Required Invoice Elements

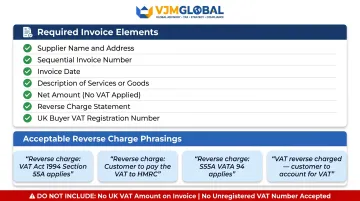

Must include:

- Singapore supplier's business name and address

- Sequential invoice number

- Date

- Description of services or goods supplied

- Net amount (no VAT)

- Clear reverse charge statement

- UK buyer's VAT registration number

Acceptable reverse charge phrasings (per HMRC Notice 735):

- "Reverse charge: customer to account for VAT to HMRC"

- "Reverse charge: VAT Act 1994 Section 55A applies"

- "Reverse charge: S55A VATA 94 applies"

- "Reverse charge: customer to pay the VAT to HMRC"

What Must NOT Appear

- ❌ UK VAT added to the invoice

- ❌ UK VAT registration number you don't hold

- ❌ 0% VAT line without explicit reverse charge wording

A 0% VAT invoice without the mandatory "reverse charge" reference fails to meet legal requirements under VAT Regulations 1995 and could create compliance issues for both parties.

Exception: If you hold UK VAT registration

Some Singapore businesses carry UK VAT registration — typically those selling to UK consumers or with UK-taxable activities. In that case, report the net sale in Box 6 but do not include output tax in Box 1.

Practical Verification Tip

Obtain and verify your UK client's VAT registration number before issuing invoices. Use HMRC's online VAT number checker to confirm validity and see the registered business name and address.

VJM Global has supported 250+ UK businesses with cross-border accounting and tax compliance. Their team can help Singapore companies set up compliant invoicing workflows and apply correct VAT treatment across different UK client types.

Common Mistakes Singapore Businesses Make with UK Reverse Charge

Mistake 1: Charging UK VAT Without Being Registered

Some Singapore businesses mistakenly add "20% UK VAT" to invoices without being UK VAT-registered. This creates a serious compliance problem — HMRC can charge penalties under Finance Act 2008, Schedule 41, Paragraph 2 for unauthorised VAT invoices.

If this error occurs, the Singapore business must issue a corrected invoice and cannot keep the VAT collected. The reputational and contractual damage with UK clients is real.

Mistake 2: Treating B2C Sales the Same as B2B

Singapore businesses selling digital services, subscriptions, or physical goods to UK individual consumers cannot use the reverse charge. Instead, they must:

- Charge UK VAT directly on the sale

- Register for UK VAT or use an available simplification scheme

- Track UK consumer sales separately from B2B transactions

The reverse charge only applies to business-to-business supplies — B2C sales require a different compliance approach entirely.

Mistake 3: Missing Reverse Charge Wording or VAT Number

A zero-VAT invoice without explicit reverse charge notation isn't compliant. HMRC can treat this as a missing or incorrect invoice, which exposes the UK buyer to penalties. The wording is legally required under VAT Regulations 1995 and must appear on every qualifying invoice.

When Singapore Businesses May Still Need UK VAT Registration

Selling to UK Consumers (B2C)

If a Singapore business sells goods or digital services directly to UK individuals, it must charge UK VAT. For non-resident businesses selling digital services to UK consumers, there's no minimum threshold — registration is required for any taxable supplies.

For other taxable supplies, if the value exceeds £90,000 in a rolling 12-month period, UK VAT registration becomes mandatory.

Having a UK Business Establishment

If a Singapore company opens a UK branch, maintains a UK office, employs UK-based staff, or has sufficient presence to constitute a UK fixed establishment, it loses the overseas supplier status that supports reverse charge treatment and must register for UK VAT.

HMRC defines a fixed establishment as having:

- A defined place (such as an office)

- Permanent presence of human resources

- Permanent presence of technical resources

- Resources necessary for making or receiving supplies

The VAT Registration Trap

Singapore businesses not yet registered for UK VAT should be aware that purchasing taxable services from UK or overseas suppliers can count toward the registration threshold. This catches many businesses off guard — particularly those using the reverse charge.

If total taxable supply values (including imported services subject to reverse charge) exceed £90,000 in a rolling 12-month period, registration with HMRC is required.

Professional guidance from advisors like VJM Global, who have served 250+ UK businesses across cross-border tax compliance, can help Singapore businesses assess their UK VAT exposure before it becomes a liability.

Frequently Asked Questions

What is VAT reverse charge in the UK?

UK VAT reverse charge is a mechanism where the buyer (not the seller) accounts for VAT on qualifying B2B transactions. This ensures VAT is reported in the buyer's country without the overseas supplier needing to charge or collect it.

How does VAT reverse charge work in the UK?

The supplier issues an invoice without VAT. The UK-registered buyer then reports the applicable VAT as both output tax (Box 1) and input tax (Box 4) on their VAT return — resulting in a net-zero VAT impact for fully taxable businesses.

Does VAT reverse charge still apply in the UK after Brexit?

Yes, the UK reverse charge still applies post-Brexit. For Singapore businesses specifically, Brexit changed little since Singapore was never an EU member — UK businesses continue to apply the reverse charge when receiving B2B services from Singapore suppliers.

What should I put on my invoice for VAT reverse charge in the UK?

Show the net amount with 0% VAT, include a statement such as "Reverse charge: customer to account for VAT to HMRC," and include the UK buyer's VAT registration number. No UK VAT amount should be charged by the Singapore supplier.

How do I calculate reverse charge VAT in the UK?

The UK buyer applies the 20% standard rate to the net invoice value, reports that amount in Box 1 of their VAT return, and reclaims it in Box 4. The Singapore supplier's only obligation is to issue a compliant invoice with the correct reverse charge notation.

What is an example of a VAT reverse charge?

A Singapore IT consultancy invoices a UK company £15,000 for software development services. The invoice shows £15,000 net with no VAT and a reverse charge note. The UK company reports £3,000 as output tax in Box 1 and claims back £3,000 in Box 4 on their VAT return.

Have questions about UK VAT compliance for your Singapore business? VJM Global's cross-border tax team can help you implement compliant invoicing workflows, verify UK client VAT numbers, and assess your VAT exposure. Reach us at info@vjmglobal.com or call +91 98915 76441.