Introduction

UK withholding tax (WHT) creates compliance friction on both sides of cross-border interest and royalty payments. The payer must deduct tax at source — typically 20% — before transferring funds, while the recipient must decide whether to treat that withheld amount as a recoverable asset or an irrecoverable expense.

Many businesses struggle with recording gross income correctly, filing quarterly CT61 returns on time, and confirming whether a double taxation treaty reduces the 20% rate. Those mistakes trigger HMRC penalties, overstated expenses, and misstated balance sheets.

This guide covers each of those challenges directly: when UK WHT applies, how to record it from both sides of the transaction, how to present it on the balance sheet, and the most common accounting errors to avoid.

TL;DR

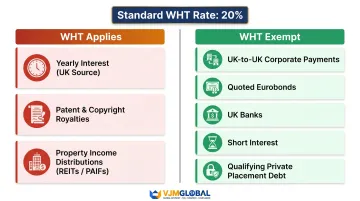

- UK WHT of 20% applies to "yearly" interest and royalty payments with a UK source — ordinary company dividends are exempt

- Payers deduct WHT and remit it to HMRC via quarterly CT61 returns filed within 14 days of quarter-end

- Recipients record gross income and classify WHT as a current asset (reclaimable) or expense (not reclaimable)

- Treaty relief can reduce or eliminate the 20% rate, but requires HMRC pre-authorisation or an active reclaim

What Is UK Withholding Tax and When Does It Apply?

Under the Income Tax Act 2007, Section 874, UK withholding tax (WHT) requires the payer — not the recipient — to deduct tax at source before making certain cross-border payments. This obligation applies whether or not the payer is based in the UK.

The standard rate is 20%, known as the savings basic rate. The UK government has proposed an increase to 22% from 6 April 2027.

Three payment types trigger UK WHT:

- "Yearly" interest with a UK source — short-term interest expected to run one year or less is generally exempt

- Patent, copyright, design, trademark, and know-how royalties — governed by ITA 2007 s.903 and Part 15 Chapters 6-7

- Property Income Distributions (PIDs) from UK Real Estate Investment Trusts (REITs) and Property Authorised Investment Funds (PAIFs)

Dividends paid by ordinary UK companies are exempt from WHT under domestic law.

Not every payment falls within scope, though. Several domestic exemptions eliminate the WHT obligation entirely.

Key Domestic Exemptions

No WHT needs to be deducted in these circumstances:

- UK-to-UK corporate payments — recipient is UK-resident and chargeable to UK corporation tax

- Quoted Eurobonds — interest on publicly listed bonds

- UK banks — payments to or from UK banks or UK permanent establishments of foreign banks

- Short interest — loans not intended to run beyond one year

- Qualifying private placement debt — interest on qualifying private placements by UK companies (not available for connected-party loans)

Source: PWC UK Withholding Taxes

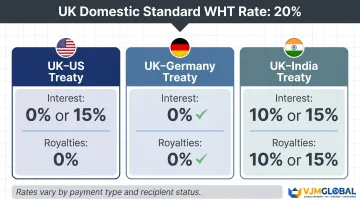

The UK-India treaty in particular involves tiered rates depending on the nature of the payment and the recipient's status — making it one of the more nuanced treaties to apply in practice. Once you know your applicable treaty rate, the next step is claiming that relief through the correct HMRC process.

Two Routes for Claiming Treaty Relief

1. HMRC Double Taxation Treaty Passport Scheme (DTTP)

This allows pre-approved lenders to receive interest gross without needing per-payment authorisation.

- Lender applies for a passport (valid 5 years) using Form DTTP1

- Borrower notifies HMRC within 30 days using Form DTTP2

- HMRC issues a Direction to Pay at the treaty rate

Guidance: DTTP Scheme Terms and Conditions

2. Filing a DTT Relief Application

Use Form DT-Individual or Form DT-Company before payment.

For royalties specifically, a payer can apply a reduced rate without prior HMRC clearance if they "reasonably believe" relief is due — but carry the risk if that belief proves incorrect. For interest, a formal HMRC Direction is required before paying at a reduced rate.

Source: HMRC Double Taxation Relief for Companies

Domestic Exemptions That Eliminate WHT Entirely

UK domestic law provides several exemptions:

- Quoted Eurobond exemption — publicly listed bonds

- UK corporate exemption — recipient within UK corporation tax charge

- Private placement exemption — qualifying private placements (not available for connected parties)

Before making a gross payment under any exemption, confirm that all statutory conditions are met — incorrectly applying an exemption exposes the payer to the full 20% WHT liability, plus potential HMRC penalties.

Common Mistakes When Accounting for UK Withholding Tax

Payer Error: Making Gross Payments Without Clearance

The most common payer error is making gross payments without verifying whether a WHT obligation applies — or assuming a treaty exemption exists without checking the relevant treaty provisions or obtaining HMRC clearance.

The payer remains liable for the full WHT amount — plus penalties and interest — even if the recipient was treaty-exempt, unless pre-authorisation was secured. HMRC's paused concession means payers now face full 20% liability without mitigation.

Recipient Error: Recording Income at Net Amount

Recording income at the net (received) amount rather than the gross amount understates revenue and distorts the tax computation. Immediately expensing WHT that should be held as a recoverable asset also inflates costs and undervalues the balance sheet.

Correct approach: Always record gross income, then classify the WHT correctly based on recoverability.

Reporting Error: Missing CT61 Deadlines

Failing to file CT61 returns on time — or at all — for WHT deducted triggers automatic penalties. HMRC requires quarterly CT61 submissions even if the net amounts are small.

Penalty ranges under Schedule 24 Finance Act 2007:

- Careless: 0% to 30% of potential lost revenue

- Deliberate but not concealed: 20% to 70%

- Deliberate and concealed: 30% to 100%

Source: HMRC COTAX Manual COM100013

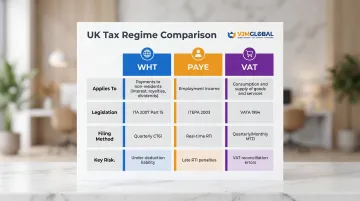

Classification Error: Conflating WHT with PAYE or VAT

WHT is a distinct regime — don't confuse it with PAYE or VAT. Here's how the three differ:

| Regime | Applies To | Legislation | Filing |

|---|---|---|---|

| WHT | Payments to non-residents (interest, royalties, dividends) | ITA 2007 Part 15 | Quarterly CT61 |

| PAYE | Employment income | ITEPA 2003 | Real-time (RTI) |

| VAT | Consumption / supply of goods and services | VATA 1994 | Quarterly/monthly MTD |

Misclassifying WHT as a VAT or PAYE obligation leads to reconciliation errors and missed CT61 deadlines — both of which HMRC treats as separate compliance failures.

Conclusion

Accounting for UK withholding tax correctly means understanding both sides of the transaction. The payer must deduct, remit, and report via CT61; the recipient must recognise gross income and treat the withheld amount as either a recoverable asset or an irrecoverable expense, depending on treaty entitlement.

Errors in WHT accounting — under-deducting, misclassifying the withheld amount, or missing a treaty relief claim — can lead to unexpected tax liabilities, HMRC penalties, and misstated accounts. Businesses managing regular cross-border interest or royalty flows should work with a specialist who understands both UK mechanics and applicable treaty positions.

VJM Global has supported over 250 UK businesses with cross-border tax compliance, covering treaty applications, CT61 compliance, and HMRC clearance filings. If your business needs hands-on help with WHT accounting, their team offers the depth to handle it end to end.

Frequently Asked Questions

How does UK withholding tax work?

UK WHT requires the payer to deduct income tax (typically 20%) at source from certain qualifying payments — primarily "yearly" interest and royalties with a UK source — and remit the deducted amount to HMRC, usually via a quarterly CT61 return.

How do you account for withholding tax?

For the payer, WHT is recorded as a liability (WHT Payable), not an expense. For the recipient, income is recorded at the gross amount — the withheld portion is held as a current asset if reclaimable (offset against UK tax accounting obligations), or expensed if irrecoverable.

Is withholding tax an expense or a liability?

It depends on the party: for the payer, WHT is a liability owed to HMRC (not their own expense); for the recipient, it is a current asset if covered by a double tax treaty (reclaimable) or an expense if irrecoverable.

What is the withholding tax rate in the UK?

The standard UK WHT rate is 20% on qualifying interest and royalty payments, with a proposed increase to 22% from 6 April 2027. Double taxation treaties can reduce this rate, often to 0–10% depending on the country.

Do I need to file a CT61 return for withholding tax?

Yes. Companies that have deducted WHT must submit a CT61 return to HMRC quarterly (within 14 days of each quarter-end) and remit the tax at the same time.

Can UK withholding tax be reclaimed under a double tax treaty?

Yes. Recipients resident in a treaty country may qualify for a reduced or zero WHT rate. Relief can be claimed upfront via prior HMRC authorisation or retrospectively through the relevant tax return or DTT Treaty Passport Scheme.