Introduction

Pick the wrong Financial Year End (FYE) for your Singapore company, and the consequences show up fast: compressed reporting cycles, higher audit costs, and cash flow pressure right when you least need it. What looks like a routine administrative decision has real effects on tax planning, compliance deadlines, and financial reporting accuracy.

Unlike many countries with a fixed fiscal calendar, Singapore lets businesses choose any FYE date. That flexibility is genuinely useful — but it demands careful thought upfront. The date you pick anchors your entire compliance calendar, from AGM scheduling to corporate tax filing.

Changing it later requires regulatory approval and can trigger messy transitional reporting. This guide covers the key factors to weigh, the most common FYE dates Singapore companies use, and how to make the right call for your situation.

Key Takeaways

- Your FYE is the last day of your 12-month accounting period — Singapore companies can choose any calendar date

- Popular choices (31 March, 30 June, 30 September, 31 December) typically align with tax cycles or parent company reporting

- Your FYE determines AGM timing, annual return deadlines, and corporate tax filing obligations

- New companies can extend their first accounting period up to 18 months for strategic flexibility

- Changing your FYE requires ACRA notification, with prior approval needed if the change extends beyond 18 months

What is a Financial Year End in Singapore?

The Financial Year End is the last day of a company's accounting period — the structured interval over which a business tracks income, expenses, and financial performance. In Singapore, the terms "financial year end" and "fiscal year end" are used interchangeably.

Section 198 of the Companies Act 1967 defines a company's financial year as "the period in respect of which any financial statements of the company are made up, whether that period is a year or not." This deliberately flexible definition gives Singapore companies significant flexibility in structuring their reporting cycles.

12-Month Period vs. 52-Week Period

Companies can choose between two accounting period structures:

- 12-month period: Runs from a specific date to the same date the following year (e.g., 1 January 2026 to 31 December 2026)

- 52-week period: Runs for exactly 364 days (e.g., 1 January 2026 to 30 December 2026)

The distinction matters for businesses that track weekly performance metrics or operate on weekly cycles — 52-week periods create consistency in weekday alignment year-over-year. ACRA explicitly permits both structures, and Section 198(1)(b) of the Companies Act allows financial years to vary by up to seven days to accommodate this approach.

The First Financial Year: A Special Case

Newly incorporated companies enjoy unique flexibility. Section 198(2) of the Companies Act permits the first financial year to extend up to 18 months from the date of incorporation (longer periods require ACRA approval).

There's an important tax implication to keep in mind: IRAS treats any period exceeding 12 months as two separate Years of Assessment. If your first financial year spans 15 months, you'll need to split income and expenses across two assessment periods.

This adds reporting complexity, but it can also create strategic tax planning opportunities — particularly for startups managing their Tax Exemption Scheme eligibility.

Key Factors to Consider When Choosing Your FYE

While any date is technically permissible, the right FYE depends on several operational, financial, and regulatory factors. Aligning these strategically can improve tax outcomes, simplify reporting, and reduce administrative burden.

Business Seasonality and Operating Cycle

Align your FYE with the end of your peak season. This ensures financial statements capture a complete picture of performance after high-revenue periods, rather than splitting them across two reporting years.

For example:

- Retail businesses with December holiday peaks often choose 31 January or 28 February

- Education service providers aligned to academic calendars may select 30 June

- Tourism operators in Singapore might choose 30 September after the summer travel season

The same logic applies to inventory-heavy businesses — closing books when stock levels are lowest simplifies year-end counts and produces cleaner balance sheet figures.

Tax Planning and Startup Exemptions

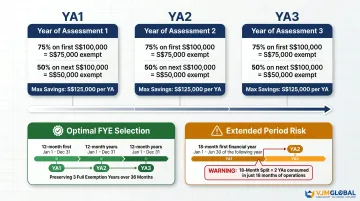

For newly incorporated Singapore companies, FYE selection directly affects eligibility timing for the Tax Exemption Scheme for New Start-Up Companies.

Current exemption rates (YA 2020 onwards):

| Chargeable Income Band | Exemption Rate | Exempt Amount |

|---|---|---|

| First S$100,000 | 75% | S$75,000 |

| Next S$100,000 | 50% | S$50,000 |

| Maximum per YA | S$125,000 |

The scheme applies for the first three consecutive Years of Assessment only. Setting your FYE at the end of your 11th or 12th month from incorporation maximises the full 12-month exemption window. If you extend the first financial year to 18 months, remember that IRAS will split this into two tax assessment periods — potentially consuming two of your three exemption years while only covering 18 months of operations.

Alignment with Parent Company or Investor Reporting

Foreign-owned companies and MNC subsidiaries need to consolidate financial statements with their parent entities. Matching the parent's reporting cycle delivers real operational benefits:

- Reduces consolidation complexity and inter-company reconciliation time

- Cuts audit coordination costs across jurisdictions

- Eliminates internal reporting friction and timeline mismatches

Most US and European multinationals use 31 December, making it the practical default for Singapore subsidiaries seeking seamless group reporting.

Availability of Auditors and Accounting Professionals

Approximately 60% of SGX-listed companies end their financial year on 31 December, creating high demand for auditors and accounting professionals from January through March.

Choosing a non-December FYE (31 March, 30 June, or 30 September) can:

- Improve access to audit firms and qualified accountants

- Reduce service costs during less competitive periods

- Enable faster turnaround times for financial statement preparation

How Your FYE Affects Compliance Deadlines

Your FYE is the anchor date from which all statutory compliance deadlines are calculated. Missing these deadlines can result in penalties from ACRA or IRAS.

Annual General Meeting (AGM) Deadline

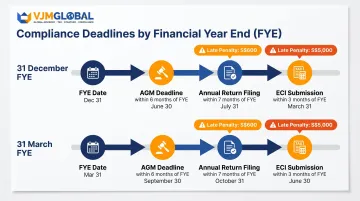

Private companies must hold their AGM within 6 months after the FYE. Listed companies have a tighter 4-month deadline.

Example: If your FYE is 31 December 2026, your AGM must be held by 30 June 2027.

Private companies can be exempted from holding an AGM if they pass a resolution to dispense with AGMs or send financial statements to all entitled persons within 5 months after FYE.

Annual Return (AR) Filing Deadline

The AR must be filed with ACRA within 7 months after FYE for domestic private companies, and within 8 months for companies maintaining an overseas branch register.

| FYE Date | AGM Deadline (Private) | AR Filing Deadline |

|---|---|---|

| 31 December 2026 | 30 June 2027 | 31 July 2027 |

| 31 March 2027 | 30 September 2027 | 31 October 2027 |

| 30 June 2027 | 31 December 2027 | 31 January 2028 |

Late lodgement carries penalties up to S$600 per return.

Estimated Chargeable Income (ECI) Submission

Companies must file ECI with IRAS within 3 months after the end of the financial year. This deadline shifts based on your FYE, giving you more control over when tax payments fall due.

ECI filing waiver applies if:

- Annual revenue is not more than S$5 million, AND

- ECI is nil for the Year of Assessment

Corporate Income Tax Return Deadline

Unlike ECI, the deadline for filing Form C-S or Form C with IRAS is fixed at 30 November each year, regardless of your chosen FYE. All filings are exclusively online at mytax.iras.gov.sg.

Late filing or non-filing carries penalties up to S$5,000.

Changing Your FYE: Rules and Restrictions

Companies can change their FYE, but only for the current or immediately preceding financial year — and not if statutory deadlines for AGM, AR filing, or financial statement submission have already passed.

When ACRA's Approval Is Required

Section 198(5) of the Companies Act requires ACRA's formal approval if:

- The change would result in a financial year exceeding 18 months

- The change is lodged less than 5 years after a previous FYE change (for changes made on or after 31 August 2018)

Notifying IRAS of an FYE Change

Once you file an FYE change with ACRA, IRAS handles the rest automatically — no separate notification is needed. Key points to know:

- IRAS syncs with ACRA data weekly — changes filed Sunday to Saturday appear in IRAS records by the following Friday

- If your FYE change creates a period exceeding 12 months, income must be split across two separate Years of Assessment, each requiring separate financial statements

- Income allocation uses either direct identification by transaction date or time apportionment across each YA

How VJM Global Can Help

VJM Global has spent 30+ years helping foreign companies — particularly from the US, UK, and Australia — navigate cross-border accounting, tax compliance, and business setup. Getting the FYE right from the start prevents compliance headaches and costly corrections down the line.

Our Chartered Accountants and business setup professionals evaluate the right FYE for your situation — factoring in parent company reporting cycles, tax exemption eligibility, and regulatory requirements.

Our support covers the full scope of what you need to stay compliant and organized:

- Bookkeeping and financial recordkeeping

- Tax preparation and statutory compliance filings

- Strategic financial planning and management reporting

- Business setup and entity structuring advisory

Conclusion

The financial year end is a foundational decision that shapes your company's entire compliance calendar, tax position, and financial reporting rhythm. Getting it right at incorporation is far easier than changing it later — ACRA restricts FYE amendments once your company has filed its first annual return.

The goal is not to pick the most popular FYE date, but the one that fits your business cycle, parent company structure, and financial strategy. If you're unsure where to start, a corporate secretary or tax adviser familiar with Singapore regulations can help you map the right date before you register — saving you a formal change application down the line.

Frequently Asked Questions

What is the fiscal year for Singapore?

Singapore does not mandate a single national fiscal year for companies — businesses can choose any FYE date. However, the Singapore government's own fiscal year runs from 1 April to 31 March.

Is Singapore a calendar year or financial year?

Singapore companies are not required to follow the calendar year (January–December). They can adopt any 12-month financial year, giving them flexibility to align with their business cycle or parent company reporting needs.

What is the accounting period in Singapore?

An accounting period is the timeframe a company uses to track financial activity — either 12 months or 52 weeks. The FYE marks the last day of this period, as defined by Section 198 of the Companies Act.

Can a company change its financial year end in Singapore?

Yes, but only for the current or previous financial year. Changes must be notified to ACRA via BizFile+, and approval is required if the change creates a period exceeding 18 months or occurs within 5 years of a previous change.

How does the financial year end affect tax filing in Singapore?

The FYE determines when ECI must be submitted to IRAS (within 3 months of FYE). The annual corporate income tax return deadline remains fixed at 30 November each year, but your FYE affects which financial year's income is reported in each filing.

Is the current financial year 25 or 26?

FY naming depends on when your financial year ends. FY25 refers to a year ending in 2025, and FY26 to one ending in 2026. A company with a 31 December FYE is currently in FY26.