Introduction

At 11pm on 31 December 2020, the Brexit transition period ended — and with it, decades of simplified intra-community VAT trading. From 1 January 2021, Great Britain left the EU's single VAT area and is now treated as a third country, subject to the same rules as any non-EU nation.

UK businesses trading with the EU now face VAT decisions on every transaction: whether to zero-rate exports, how to account for import VAT, which reverse charge rules apply, and when EU VAT registration becomes mandatory.

Get these decisions wrong, and you risk HMRC disallowing zero-rating claims, cash flow shocks from unexpected import VAT, or penalties across multiple EU jurisdictions. This guide covers the full post-Brexit VAT framework for both goods and services.

TLDR:

- Zero-rate UK goods exports to the EU — but retain valid evidence of export to protect the claim

- Use Postponed VAT Accounting (PVA) on EU imports to avoid upfront VAT cash flow impact

- B2B services: the EU customer self-accounts via reverse charge under the destination country rule

- No €10,000 threshold for UK sellers — EU VAT applies from the first B2C digital or distance sale

- Northern Ireland follows EU VAT rules for goods (not services) under the Windsor Framework

How Brexit Reshaped UK-EU VAT: What Changed on 1 January 2021

Before Brexit, the UK operated within the EU's single VAT area. UK businesses dispatched goods to EU customers as intra-community supplies, completed EC Sales Lists, and enjoyed simplified VAT reporting. From 1 January 2021, those mechanisms ceased to apply to Great Britain—all trade with the EU is now treated identically to trade with countries like the USA or Australia.

Great Britain vs Northern Ireland

Great Britain and Northern Ireland now operate under fundamentally different VAT frameworks. Northern Ireland maintains alignment with EU VAT rules for goods (not services) under the Northern Ireland Protocol (now the Windsor Framework).

Goods moving between Northern Ireland and EU member states are still treated as intra-community supplies and acquisitions, rather than imports or exports. Northern Ireland businesses use XI-prefix VAT numbers and continue filing EC Sales Lists for goods.

Four Key Simplifications Lost for GB Businesses

GB businesses lost three significant VAT simplifications when the transition period ended:

- EC Sales Lists are no longer required for goods or services supplied from Great Britain to EU customers.

- Intra-community triangulation and call-off stock — the simplified VAT arrangements for multi-party EU supply chains — no longer apply to Great Britain. Northern Ireland businesses can still use them.

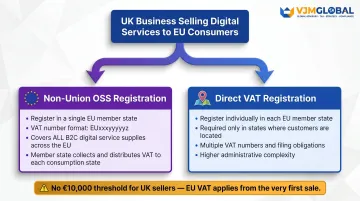

- UK VAT MOSS closed for sales made from 1 January 2021. UK businesses selling digital services to EU consumers must now register under the EU's Non-Union OSS scheme or register for VAT individually in each EU member state where they have customers.

Accounting for VAT on Goods Exported from the UK to the EU

Sales of goods from Great Britain to the EU are now treated as exports for VAT purposes. This fundamental shift means UK VAT is not charged—provided you meet HMRC's evidence requirements.

Exports to EU Business Customers (B2B)

UK sellers zero-rate goods exported to EU VAT-registered businesses. No UK VAT appears on the invoice. The EU customer accounts for VAT on arrival under intra-community acquisition rules in their own country.

You must obtain and retain evidence proving the goods left the UK. HMRC accepts two categories of proof:

- Customs declarations or freight documents (official evidence)

- Delivery notes or written customer confirmations (commercial evidence)

- Sales invoices and proof of payment (evidence of supply)

Both official or commercial evidence must be supported by evidence of supply. Missing acceptable proof at audit can trigger a retrospective 20% VAT charge.

You no longer complete EC Sales Lists for goods dispatched to EU customers. This administrative requirement ended on 1 January 2021.

Exports to EU Consumers (B2C)

Sales to EU private consumers follow the same UK VAT treatment—zero-rated as exports. However, EU import VAT and customs duties may apply in the destination country.

For low-value consignments (up to €150), UK businesses can register for the EU's Import One Stop Shop (IOSS) to collect and remit EU VAT at the point of sale. This simplifies customs clearance and improves the customer experience.

One threshold rule catches many UK sellers off guard: the EU's €10,000 annual distance sales threshold applies only to EU-established sellers. UK businesses have no threshold benefit, meaning EU VAT is due from your very first cross-border B2C sale into the EU.

Without IOSS registration or local EU VAT registration, customers face unexpected VAT and duty charges on delivery—damaging both your reputation and conversion rates.

Accounting for VAT on Goods Imported into the UK from the EU

Goods brought into Great Britain from the EU are now imports requiring customs declarations and import VAT accounting. What were once "acquisitions" are now handled under standard import procedures.

The £135 Consignment Value Threshold

The £135 intrinsic value threshold determines how you account for import VAT:

Consignments of £135 or less (B2B): If your EU supplier holds your UK VAT registration number, they don't charge VAT. You account for it using the reverse charge on your VAT return — reporting the same amount in Box 1 (output tax) and Box 4 (input tax). Net VAT payment is nil, but HMRC maintains full transaction visibility.

Consignments over £135: Import VAT is due at the border. You choose between paying upfront (C79 method) or using Postponed VAT Accounting.

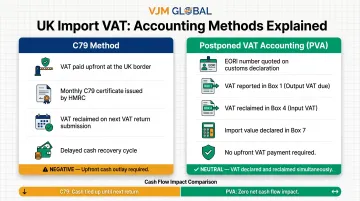

C79 Method vs Postponed VAT Accounting (PVA)

C79 method: You or your courier pay import VAT at the border. HMRC issues a monthly C79 certificate listing all import VAT payments. You reclaim this VAT on your next VAT return after receiving the certificate. The cash flow drawback is real: you pay upfront and may wait weeks before reclaiming.

Postponed VAT Accounting (PVA): PVA is the preferred method for most UK VAT-registered importers because it eliminates upfront cash outflow. PVA is permanently available with no approval needed. Instead of paying VAT at the border, you quote your EORI number on the customs declaration. Import VAT is accounted for directly on your VAT return:

- Box 1: VAT due on imports

- Box 4: VAT reclaimed on imports

- Box 7: Total value of imports (excluding VAT)

PVA removes the cash flow burden: no upfront border payment required. Download these figures from HMRC's monthly postponed VAT statements online.

Accounting for VAT on Services Between the UK and EU

Services follow different rules to goods, based on where the supply takes place and whether your customer is a business or consumer.

B2B Services: The General Rule

The general B2B rule treats services as supplied where the customer belongs. When a UK business supplies services to an EU business customer, the place of supply is in the EU member state where that customer is established—outside UK VAT scope.

How it works in practice:

- UK supplier issues invoice without UK VAT

- Obtains customer's EU VAT number

- EU customer accounts for VAT in their country using reverse charge

- UK suppliers no longer submit EC Sales Lists — abolished 1 January 2021

Verify your customer's EU VAT number using the VIES (VAT Information Exchange System) tool. Without a valid VAT number, you may need to treat the supply as B2C, changing where VAT is due.

B2C Services: The General Rule and Exceptions

The general B2C rule places supply where the supplier belongs. A UK business supplying standard services to an EU consumer treats the supply as made in the UK—outside UK VAT scope when the customer is outside the UK.

Key exceptions—where supply follows the customer:

- Copyright, patents, licences, trademarks

- Advertising services

- Consultancy, engineering, legal, accountancy, data processing

- Banking, financial, and insurance services

- Supply of staff

- Letting on hire of goods (except transport means)

- Telecommunications, broadcasting, electronically supplied services

These services supplied B2C to EU consumers are treated as supplied where the customer belongs (in the EU), placing them outside UK VAT scope. However, you may need to register for VAT in the customer's EU country or use the Non-Union OSS scheme.

Beyond registration requirements, some services carry an additional layer: the use and enjoyment rules. Where certain services — such as equipment hire or broadcasting — are consumed outside the UK, VAT treatment shifts to where that consumption happens. A UK business renting equipment to a French consumer for use in France, for instance, applies French VAT rather than UK VAT.

Finance, Insurance, and Special Services

From 1 January 2021, UK financial and insurance services firms gained a Brexit benefit: they can now recover input VAT on specified supplies made to EU customers, previously limited to non-EU customers only.

Affected firms should take three practical steps:

- Review partial exemption calculations to capture the expanded recovery right

- Identify EU customer supplies that now qualify under the specified supplies rules

- Update input VAT attribution models — the change may meaningfully increase recoverable VAT

Banks, insurers, and investment managers are most commonly affected, but any firm providing exempt financial services to EU clients should assess its position.

The Reverse Charge Mechanism: How It Works in Practice

The reverse charge shifts VAT accounting responsibility from supplier to customer. Instead of the supplier charging VAT on the invoice, the customer self-assesses—reporting output tax on the supply received and simultaneously reclaiming it as input tax, subject to normal recovery rules.

When Reverse Charge Applies

UK-EU context:

- B2B services where supply is deemed in the customer's country

- Goods imports under £135 in Great Britain

- EU businesses receiving services from UK suppliers

VAT Return Treatment Example

When a UK business receives B2B services from an EU supplier and applies reverse charge:

- Box 1: Output tax (VAT due on the supply)

- Box 4: Input tax (VAT recoverable, subject to normal recovery rules)

- Box 6: Full value of supply (sales)

- Box 7: Full value of supply (purchases)

For fully taxable businesses, the net VAT payment is nil—output tax and input tax cancel each other out. Partial exemption rules may restrict Box 4 recovery where applicable.

Before applying the reverse charge, one compliance step must come first.

Critical warning: Obtain a valid EU VAT number before applying reverse charge. Without verified VAT registration, you may need to charge local VAT instead. Use the VIES validation tool to check EU VAT numbers—including Northern Ireland's XI-prefix registrations—before treating any supply as B2B.

Special Cases: Northern Ireland, Digital Services, and EU VAT Registration

Northern Ireland's Unique Position

Northern Ireland operates a dual VAT regime. For goods, NI remains aligned with EU VAT rules under the Northern Ireland Protocol (Windsor Framework). Goods moving between Northern Ireland and EU member states are still intra-community supplies and acquisitions—not imports or exports.

What this means for NI businesses:

- Use XI-prefix VAT numbers for EU trade in goods

- Complete EC Sales Lists for goods supplied to EU customers

- Report acquisition VAT for goods received from EU: Box 2 (acquisition VAT) and Box 4 (input tax)

- Services remain outside the Protocol—follow standard UK rules

The Windsor Framework (agreed 27 February 2023) introduced temporary VAT zero-rating for energy-saving materials and a second-hand motor vehicle payment scheme, but core VAT alignment for goods continues unchanged.

Digital Services: VAT MOSS No Longer Available

UK businesses selling digital services (software, streaming, e-books) to EU consumers lost access to UK VAT MOSS from 1 January 2021. The UK VAT MOSS system remains accessible only for amending returns for periods up to Q4 2020.

Your options now:

- Register for the EU's Non-Union OSS scheme in any single EU member state

- Register for VAT directly in each EU member state where you have customers

The Non-Union OSS scheme covers all B2C service supplies to EU consumers, not just digital services. You can choose any EU member state as your registration point, receiving a VAT identification number in format EUxxxyyyyyz. That member state then forwards VAT details and payments to the relevant consumption states.

Note that unlike EU-established sellers who benefit from the €10,000 annual threshold, UK businesses must charge destination-country VAT from the first euro of B2C sales.

EU VAT Registration: When UK Businesses May Need It

UK businesses may need direct VAT registration in one or more EU countries when:

- Holding stock in EU warehouses or fulfilment centres — physical presence creates a taxable establishment, and OSS schemes don't cover supplies from local stock

- Selling B2C to EU consumers without using IOSS (for goods under €150) or Non-Union OSS (for services), where local thresholds are exceeded

- Operating in sectors with compulsory registration requirements regardless of turnover

VJM Global advises UK businesses on cross-border tax compliance, with particular depth in international tax obligations for companies operating between the UK, EU, and India. Through our membership in EAI International — an international network of independent accounting and tax firms — we can connect businesses with qualified specialists for EU VAT registration and multi-jurisdiction compliance queries. Reach us at info@vjmglobal.com to discuss your requirements.

Frequently Asked Questions

Do you charge VAT on goods from the UK to the EU?

No, UK businesses do not charge UK VAT on goods exported to the EU. These supplies are zero-rated as exports, provided you retain valid evidence that the goods left the UK (customs declarations, shipping documents). EU import VAT may be due in the destination country.

How to account for VAT on EU purchases?

UK VAT-registered businesses account for EU purchases as imports. For consignments valued at or below £135, apply the reverse charge on your VAT return (Box 1 and Box 4). For consignments over £135, use either Postponed VAT Accounting (PVA) for better cash flow or pay import VAT at the border and reclaim via monthly C79 certificates.

Is the UK in the EU for VAT purposes?

Great Britain (England, Scotland, Wales) is no longer in the EU VAT area from 1 January 2021 and is treated as a third country. Northern Ireland is the exception—it remains aligned with EU VAT rules for goods (not services) under the Northern Ireland Protocol, using XI-prefix VAT numbers.

What is Postponed VAT Accounting (PVA) and how does it work?

PVA allows UK VAT-registered importers to account for import VAT directly on their VAT return rather than paying at the border, improving cash flow. You quote your EORI number on customs declarations, then report import VAT in Box 1 (due) and Box 4 (reclaimable) based on monthly PVA statements from HMRC; no approval is needed and it's permanently available to all VAT-registered importers.

Does the reverse charge mechanism apply to UK-EU services after Brexit?

Yes, the reverse charge applies to B2B services supplied from a UK business to an EU business. The place of supply is where the customer belongs (the EU), so the EU customer accounts for VAT in their country rather than the UK supplier charging UK VAT. The UK supplier must obtain a valid EU VAT number to apply this treatment.

Do UK businesses need to register for VAT in EU countries?

Registration may be required if you hold stock in an EU country, make B2C sales above local thresholds without using IOSS or OSS schemes, or sell digital services without Non-Union OSS registration. Most B2B supplies are handled via reverse charge without local registration.