Introduction

Singapore businesses expanding into the UK often underestimate the complexity of the UK's Value Added Tax (VAT) system. While Singapore operates a straightforward 9% GST, the UK uses a multi-tiered VAT structure with rates of 20%, 5%, and 0%, plus a fourth category—exempt supplies—that works entirely differently. For Singapore companies selling goods or services in the UK, importing inventory, or establishing operations, understanding these distinctions isn't optional: it's essential to avoid costly compliance penalties.

One of the most common traps? Singapore businesses mistakenly assume they benefit from the UK's £90,000 registration threshold. They don't. Non-UK-established businesses must register for VAT from their very first taxable supply, with no threshold at all. HMRC's registration guidance confirms this applies regardless of turnover.

This catches out businesses across the board — whether you're supplying digital services to UK consumers or holding inventory in a UK warehouse. This guide breaks down each VAT rate, what it covers, and what Singapore businesses need to get right before making their first UK sale.

Key Takeaways

- The UK operates four VAT classifications: 20% standard, 5% reduced, 0% zero-rated, and exempt (which prevents input VAT recovery).

- Singapore businesses must register from their first UK taxable supply—there's no £90,000 threshold for non-UK entities.

- VAT-registered businesses charge output tax, reclaim input tax, and file returns quarterly via Making Tax Digital software.

- Exports from the UK to Singapore are zero-rated, making them VAT-free at the point of sale.

- UK imports typically face 20% import VAT, recoverable through Postponed VAT Accounting.

- Post-Brexit, UK and EU VAT systems are separate—EU registrations don't cover UK obligations.

What Is UK VAT?

UK VAT (Value Added Tax) is an indirect consumption tax administered by HMRC (His Majesty's Revenue and Customs), collected by businesses on behalf of the government and ultimately paid by the final consumer. Unlike Singapore's single-rate GST, UK VAT operates at multiple rates and applies at each stage of the supply chain—covering every link from manufacturer through wholesaler and retailer to the end buyer.

How the VAT chain works:

A VAT-registered business charges VAT on sales (output tax) and reclaims VAT paid on business purchases (input tax). The business pays only the net difference to HMRC. For example, a Singapore wholesaler buying £1,000 of goods (£200 VAT) and selling them for £2,000 (£400 VAT) pays HMRC only £200 (£400 output tax minus £200 input tax). The final consumer bears the full tax cost because they cannot reclaim input VAT.

Taxable vs. exempt supplies—a critical distinction:

- Taxable supplies (standard-rated, reduced-rated, zero-rated) allow businesses to register for VAT and reclaim input tax

- Exempt supplies (financial services, healthcare, education) do not allow VAT registration or input tax recovery

A Singapore business supplying zero-rated children's clothing can reclaim VAT on UK logistics and warehousing costs. A business providing only exempt insurance services cannot—and may face significant irrecoverable VAT expenses.

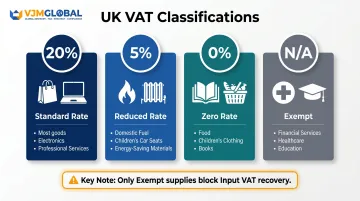

UK VAT Rate Structure: Standard, Reduced, Zero-Rated, and Exempt

The UK operates four VAT classifications, each with distinct rules and implications for Singapore businesses.

| Rate | Percentage | Applies To | Singapore Export Examples |

|---|---|---|---|

| Standard | 20% | Most goods and services | Electronics, adult clothing, professional services, B2B consultancy |

| Reduced | 5% | Specific domestic items | Children's car seats, domestic fuel, energy-saving materials |

| Zero | 0% | Essential goods (still taxable) | Children's clothing, most food (non-catering), books, newspapers |

| Exempt | N/A | Financial, health, education | Insurance services, medical care, vocational training |

Standard Rate (20%)

The standard rate applies to any goods or services not specifically listed under a lower rate. According to HMRC's VAT rates page, this covers:

- Electronics and adult clothing

- Professional services and B2B consultancy

- Hotel accommodation and restaurant meals

This is the rate most Singapore exporters will encounter when selling into the UK market.

Reduced Rate (5%)

The 5% reduced rate applies to a narrowly defined list:

- Domestic fuel and power (gas, electricity for residential properties)

- Children's car seats, booster seats, and cushions

- Energy-saving materials installed in homes

- Mobility aids for elderly people

- Smoking cessation products (nicotine patches, gum)

Zero Rate (0%)

Zero-rated supplies are taxable at 0%, which means businesses can still register for VAT and reclaim input tax on their costs. Key zero-rated categories include:

- Most food for human consumption (excluding restaurant meals and catering)

- Children's clothing and footwear

- Books, newspapers, magazines

- Prescription medicines dispensed by pharmacists

- Public transport (vehicles carrying 10+ passengers)

A Singapore apparel exporter selling children's garments into the UK would charge 0% VAT but could reclaim VAT on UK warehousing, shipping, and professional fees.

Exempt Supplies

Exempt supplies differ from zero-rated in one consequential way: VAT cannot be reclaimed on costs related to those supplies. Businesses making only exempt supplies cannot register for VAT at all. Exempt categories include:

- Financial and insurance services

- Healthcare (doctors, dentists, opticians)

- Education and vocational training

- Certain property transactions

- Gambling

A Singapore fintech company providing exempt financial advice to UK clients would face irrecoverable VAT on UK office rent, legal fees, and technology costs — a cost that compounds quickly at scale.

VAT Registration in the UK: Critical Rules for Singapore Businesses

The £90,000 Threshold Doesn't Apply to You

UK-established businesses must register for VAT when taxable turnover exceeds £90,000 in a rolling 12-month period (increased from £85,000 on 1 April 2024). Singapore businesses do not benefit from this threshold.

HMRC states explicitly: "You must also register (regardless of taxable turnover) if all of the following are true: you're based outside the UK; your business is based outside the UK; you supply any goods or services to the UK (or expect to in the next 30 days)."

This means a Singapore SaaS company selling a single £10/month subscription to a UK consumer must register for UK VAT. There is no minimum threshold.

What Triggers UK VAT Registration for Singapore Businesses

You're making taxable supplies in the UK if you:

- Sell goods already located in the UK at the time of sale

- Hold inventory in UK warehouses or fulfilment centres (including Amazon FBA)

- Provide digital services (software, e-books, streaming) to UK consumers

- Supply certain B2C services where the customer is in the UK

Post-Brexit, the UK operates an entirely separate VAT system from the EU. An EU VAT registration does not cover UK obligations, and vice versa.

The Registration Process

Singapore businesses must:

- Apply to HMRC for a UK VAT number using form VAT1 or the online registration service

- Provide proof of UK business activity and supply details

- Consider appointing a UK VAT agent to manage filings and HMRC correspondence

Registration typically takes 2-4 weeks. HMRC assigns a VAT number that must appear on all UK invoices.

Voluntary Registration

Mandatory registration isn't the only reason to get a UK VAT number. Even if not legally required — for example, when making only zero-rated supplies — Singapore businesses can register voluntarily to reclaim input VAT on UK purchases. This is particularly useful for businesses incurring UK costs such as warehousing, logistics, or professional fees before commencing sales.

For Singapore businesses managing obligations across multiple jurisdictions, VJM Global can coordinate with UK-based professionals through its EAI International network to support compliance requirements alongside any India-side accounting or advisory work.

How UK VAT Works in Practice: Returns, Input Tax, and Making Tax Digital

Output Tax vs. Input Tax: The Core Mechanism

- Output tax: VAT you charge on sales

- Input tax: VAT you pay on business purchases

You remit the net difference to HMRC. If input tax exceeds output tax (common for export-focused businesses), HMRC issues a refund.

Example: A Singapore electronics distributor imports £50,000 of goods into the UK, paying £10,000 import VAT. It sells the goods for £80,000 plus £16,000 output VAT. The business reclaims £10,000 input tax and pays HMRC £6,000 net (£16,000 output minus £10,000 input).

VAT Return Filing: Quarterly, Monthly, or Annual

Quarterly filing (default): Most businesses file four VAT returns per year, covering three-month periods.

Monthly filing: Available to businesses expecting regular VAT repayments. This suits Singapore exporters with zero-rated UK sales who accumulate input tax credits. However, it requires 12 returns annually instead of four.

Annual Accounting Scheme: Businesses with estimated taxable turnover of £1.35 million or less can file one annual return and make advance payments throughout the year. Not recommended for businesses regularly reclaiming VAT.

Making Tax Digital (MTD) Is Mandatory

All VAT-registered businesses must keep digital VAT records and submit returns using MTD-compatible software. HMRC automatically enrols new registrations into MTD. HMRC no longer accepts manual returns.

Special VAT Schemes

Flat Rate Scheme: Businesses with turnover under £150,000 can pay a fixed percentage of gross turnover rather than tracking individual transactions. This reduces admin burden but blocks input VAT recovery (except for capital purchases over £2,000).

Cash Accounting Scheme: Allows businesses with turnover under £1.35 million to account for VAT only when payment is received (not when invoiced). This improves cash flow for businesses with extended payment terms.

For most Singapore businesses importing goods into the UK, neither scheme is optimal — the Flat Rate Scheme eliminates input tax recovery, while the Cash Accounting Scheme only benefits those with delayed customer payments. A UK tax adviser can confirm which, if any, applies to your model.

Invoicing and Record-Keeping

UK VAT invoices must include:

- Supplier's VAT number

- Sequential invoice number

- Date of supply (tax point)

- Customer's name and address

- Description of goods or services

- VAT rate applied and amount

- Total excluding and including VAT

Records must be retained for at least 6 years. Note the tax point rule: VAT becomes due on the earlier of the invoice date or date of supply, though issuing an invoice within 14 days of supply shifts the tax point to the invoice date.

VAT on Imports and Exports: What Singapore Businesses Need to Know

Importing Goods from Singapore into the UK

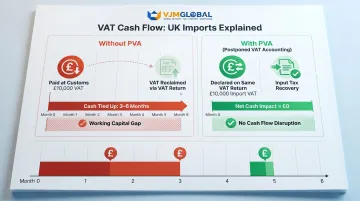

Goods imported into the UK are subject to import VAT at the applicable rate—typically 20% for standard-rated goods. However, VAT-registered businesses can use Postponed VAT Accounting (PVA) to account for import VAT on their VAT return rather than paying upfront at the border.

How PVA eliminates cash flow drag:

Without PVA, you pay £10,000 import VAT at customs, then reclaim it 3-6 months later on your VAT return—tying up working capital. With PVA, you declare £10,000 import VAT and £10,000 input tax recovery on the same return. Net cash impact: zero.

HMRC's PVA guidance confirms this is available to all UK VAT-registered businesses importing goods. For Singapore businesses importing goods into the UK monthly or more, PVA can free up tens of thousands of pounds in working capital each year.

Exporting Goods from the UK to Singapore

Goods exported from the UK are generally zero-rated, meaning UK VAT is not charged. Singapore businesses buying from UK suppliers benefit from this. However, the UK seller must retain evidence of export to qualify for zero-rating:

- Customs declaration via the Customs Declaration Service (CDS), including Movement Reference Number (MRN) or Document Unique Consignment Reference (DUCR)

- Commercial transport evidence (bills of lading, waybills, CMR notes)

- Evidence of supply (invoices, orders, packing lists)

Evidence must be obtained within 3 months of the time of supply.

Post-Brexit: UK and EU VAT Are Separate

From 1 January 2021, goods movements between Great Britain and the EU are treated identically to non-EU transactions. UK and EU VAT registrations are entirely separate.

A Singapore business selling across both markets needs to assess registration requirements in each jurisdiction independently. The EU One Stop Shop (OSS) scheme applies only to distance sales from Northern Ireland to the EU. It does not cover UK domestic VAT obligations.

Digital Services to UK Consumers

Singapore businesses providing digital services (software, e-books, streaming, online courses) to UK consumers must charge UK VAT at 20% from the first supply, regardless of turnover. The place of supply is the consumer's location.

Exception: If services are provided via a third-party platform (such as app stores), the platform typically accounts for VAT instead.

Common Misconceptions Singapore Businesses Have About UK VAT

Misconception 1: "The £90,000 Threshold Applies to Us"

Many Singapore businesses incorrectly assume the UK's domestic registration threshold applies to them. It doesn't. The £90,000 threshold is exclusively for UK-established businesses.

Non-UK businesses must register from their first UK taxable supply. Missing that deadline creates real exposure:

- Backdated VAT liabilities on all supplies made since the registration date should have applied

- Penalties from 0% to 100% of unpaid VAT depending on whether the failure was deliberate or concealed

- Interest charges on top of any outstanding tax owed

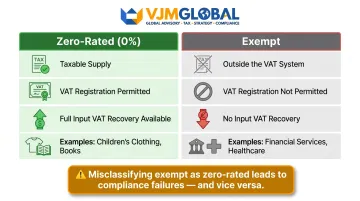

Misconception 2: "Zero-Rated and Exempt Mean the Same Thing"

The distinction matters more than most businesses realise. Zero-rated supplies are taxable at 0%, which means full input VAT recovery is still available. Exempt supplies sit entirely outside the VAT system — no input VAT recovery at all.

A Singapore business incorrectly classifying its supplies as exempt rather than zero-rated could miss out on significant input VAT refunds, especially on UK logistics, warehousing, and professional service costs. The reverse error — treating exempt supplies as zero-rated — leads to incorrect VAT invoicing and compliance failures.

Misconception 3: "UK VAT Is the Same as EU VAT Post-Brexit"

Since Brexit, the UK operates an independent VAT system separate from the EU. EU VAT rules, thresholds, and schemes (such as the EU OSS) do not apply in the UK.

Singapore businesses with EU VAT registrations must assess UK obligations separately. An EU VAT number is not valid for UK filings, and HMRC does not accept EU returns as proof of UK compliance. Businesses selling into both markets need at minimum two VAT registrations.

Frequently Asked Questions

What are the VAT rates in the UK?

The UK operates three active VAT rates: 20% (standard, applying to most goods and services), 5% (reduced, applying to items like domestic fuel and children's car seats), and 0% (zero-rated, covering most food, children's clothing, and books). Additionally, some supplies—such as financial services, healthcare, and education—are exempt from VAT altogether.

What is VAT in the UK?

UK VAT is an indirect consumption tax administered by HMRC, charged at each stage of the supply chain on most goods and services. VAT-registered businesses collect and remit it to HMRC but can reclaim VAT on their own purchases (input tax) — so only the end consumer bears the full cost.

What goods are charged the 5% reduced VAT rate in the UK?

Key reduced-rate items include domestic fuel and power (gas and electricity for homes), energy-saving materials installed in residential properties, children's car seats and booster cushions, mobility aids for elderly people, and smoking cessation products such as nicotine patches and gum.

What goods and services are exempt from VAT in the UK?

VAT-exempt supplies include most financial and insurance services, healthcare, education and vocational training, certain commercial property transactions, and gambling. Businesses making only exempt supplies cannot register for VAT or reclaim input tax — which can significantly raise their operating costs.

Do Singapore businesses have to pay VAT in the UK?

VAT is charged based on where the supply takes place, not the buyer's nationality or country of registration. Singapore businesses purchasing standard-rated or reduced-rated goods and services in the UK pay VAT at the applicable rate. The VAT Retail Export Scheme, which previously allowed refunds on goods, was removed for Great Britain purchases from January 2021.

Can tourists get VAT refunds in the UK?

The VAT Retail Export Scheme was removed for Great Britain in January 2021, so visitors to England, Scotland, and Wales cannot reclaim VAT on personal purchases. Visitors to Northern Ireland who are not UK or EU residents may still apply for refunds using form VAT 407(NI), provided goods leave Northern Ireland and the EU within 3 months.