Introduction

Picture this: a UK-resident IT consultant receives £15,000 in dividends from an Indian subsidiary, only to find herself facing tax demands from both HMRC and the Income Tax Department of India on the exact same income. Or consider a British expatriate receiving a US pension who discovers both countries claim a portion. This is the classic double taxation trap — precisely what Double Taxation Relief (DTR) is designed to prevent.

The UK operates one of the world's most extensive networks of Double Taxation Agreements (DTAs), covering more than 130 territories. Relief is available through both bilateral treaties and UK domestic law, meaning even where no treaty exists, you may still be protected. This guide explains what DTR means, which relief methods apply, what income qualifies, and how to actually claim it.

It's written for UK residents with foreign income, NRIs with UK-source income, and businesses managing cross-border tax between the UK and countries like India.

TLDR:

- Double taxation relief prevents paying full tax twice on the same income in two countries

- The UK has DTAs with more than 130 countries — one of the largest treaty networks globally

- Three relief methods apply: DTA credit relief, unilateral UK law relief, and deduction relief

- Claim DTR through SA106 supplementary pages on your Self Assessment return

- UK residents pay the higher of the two tax rates, not both rates in full

What is Double Taxation Relief in the UK?

Double taxation occurs when the same income or capital gain is taxed in two different countries—once where the income is earned (the source country) and again where the individual or business is resident. For example, a UK resident earning rental income from a property in Spain faces Spanish tax on that rental income and UK tax on their worldwide income, which includes the Spanish rent.

Double Taxation Relief (DTR) is a mechanism under UK law and bilateral treaties that removes or reduces this dual tax charge. It does not mean paying no tax—it means you should not pay full tax twice on the same income. The GOV.UK guidance confirms: "If the tax rates in the 2 countries are different, you'll pay the higher rate of tax."

How the UK Implements DTR

The UK uses two main routes:

- Double Taxation Agreements (DTAs) – negotiated treaties with specific countries that divide taxing rights and set out which country gets priority on specific income types

- Unilateral relief – domestic provisions under UK law that apply where no treaty exists, provided the foreign tax is comparable to UK Income Tax or Capital Gains Tax

DTAs allocate taxing rights between the source country and the residence country, with built-in mechanisms to prevent the same income being fully taxed in both. The UK has concluded agreements with more than 130 countries, making its DTA network among the most extensive in the world, according to the Institute of Chartered Accountants in England and Wales (ICAEW). Understanding which route applies to your situation determines exactly how much relief you can claim.

Key Principle: Pay the Higher Rate, Not Both

Under most DTAs, if tax rates differ between the two countries, the individual pays the higher of the two rates—not both rates in full.

Example:

- India taxes your dividend income at 15%

- UK tax on the same dividend would be 20%

- You pay 15% in India and an additional 5% in the UK — a total of 20%, not 35%

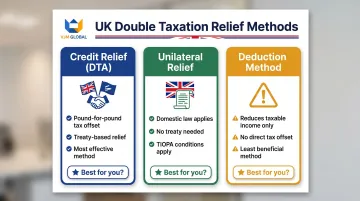

Three Types of Double Taxation Relief Available in the UK

HMRC recognises three mechanisms for double taxation relief, each governed by specific provisions in the Taxation (International and Other Provisions) Act 2010 (TIOPA 2010):

- Credit relief under a Double Taxation Agreement (treaty relief)

- Unilateral relief under UK domestic law

- Deduction of foreign tax from taxable income

Credit relief is usually most beneficial because it provides a pound-for-pound offset. The deduction method reduces your taxable income rather than your tax bill, resulting in less overall relief.

Credit Relief Under a Double Taxation Agreement (Treaty Relief)

Where a DTA exists, the UK typically allows a credit for tax paid in the foreign country against UK tax liability on the same income. This is governed by TIOPA10/S2 (which gives legal effect to DTAs) and TIOPA10/S18 (which provides the entitlement to credit).

The foreign tax paid is offset pound-for-pound against the UK tax due on that income. You effectively pay only the difference if UK rates are higher, or nothing more if foreign rates are equal or higher.

France example:

- Income: £10,000 employment income from France

- French withholding tax (20%): £2,000

- UK tax at 40%: £4,000

- Credit applied: £2,000

- You owe HMRC: £2,000 — total tax paid equals the higher UK rate

Unilateral Relief (Credit Under UK Domestic Law)

Even without a DTA, UK residents can claim unilateral foreign tax credit relief through HMRC's domestic provisions under TIOPA10/S8 and TIOPA10/S18.

Three conditions must be met:

- The foreign tax must correspond to UK Income Tax, Corporation Tax, or Capital Gains Tax

- The foreign tax must be charged on income or chargeable gains

- The income must be taxable in the UK

Malaysia example:

- Income: £5,000 interest from a Malaysian bank account

- Malaysian withholding tax (10%): £500

- UK tax at 20%: £1,000

- Credit applied: £500

- You owe HMRC: £500 — total tax paid £1,000

HMRC guidance confirms unilateral relief is available for countries with which the UK has no DTA, provided the foreign tax meets these criteria.

Deduction Method

Instead of crediting the foreign tax against UK tax, this method allows you to deduct the foreign tax paid from the foreign income before calculating UK tax. This is governed by TIOPA10/S112.

It applies in limited circumstances:

- Credit relief is not available

- The income is from a business where the foreign tax is an allowable expense

- It produces a better outcome in specific loss-making scenarios

The table below shows why the deduction method almost always results in a higher total tax bill:

| Method | Foreign Income | Foreign Tax Paid | UK Tax Calculation | Total Tax Paid |

|---|---|---|---|---|

| Credit method | £10,000 | £2,000 (20%) | 40% on £10,000; credit £2,000 | £4,000 |

| Deduction method | £10,000 | £2,000 (20%) | 40% on £8,000 = £3,200 | £5,200 |

The deduction method costs £1,200 more in this scenario. Understanding which method applies — and whether you can elect for credit relief instead — is where the real planning opportunity lies.

What Income Qualifies for Double Taxation Relief?

GOV.UK guidance confirms that DTR is available for:

- Employment income and self-employment earnings

- Most pension income (with important caveats—see below)

- Bank interest

- Dividends (subject to special rules under each DTA)

- Rental income from foreign property

Eligibility varies by the specific DTA in question. Each treaty has its own articles governing which country has taxing rights over which income types.

Government Service Pensions: A Key Exception

Most UK government service pensions—including civil service, armed forces, and local authority pensions—are taxable only in the UK, regardless of where the recipient lives. This is governed by Article 19 of most DTAs.

HMRC guidance states: "Relief from UK tax for government pensions is not available for those directly employed in central, regional, or local government and members of the armed forces."

If you're a UK expatriate receiving a government service pension abroad, you cannot claim relief in your new country of residence—the UK retains exclusive taxing rights.

Capital Gains: Generally Taxable Where You Live

Under most DTAs, capital gains are taxable in the country of residence, not the source country—so relief is less commonly needed.

Critical exception: Non-residents are still subject to UK Capital Gains Tax on disposals of UK residential property. GOV.UK confirms: "Double taxation agreements do not apply to tax on gains from selling UK residential property."

Non-residents must report UK property disposals within 60 days of completion, even if there's no tax to pay or a loss was made.

Beyond the capital gains exception, two further categories fall outside the standard DTR framework.

US-UK Treaty Saving Clause

Article 1(4) of the US-UK Convention includes a "saving clause" that allows the US to tax its citizens and residents "as if the Convention had not come into effect," with limited exceptions. This means US citizens living in the UK cannot avoid US tax obligations on certain income types, even under the treaty.

The Foreign Tax Credit on the US side typically prevents actual double taxation—but US citizens must still file US returns on worldwide income.

Social Security and National Insurance

DTAs do not cover social security contributions or National Insurance. These are governed by separate bilateral social security agreements (totalization agreements—agreements that coordinate social security benefits between countries), not DTAs.

How to Claim Double Taxation Relief in the UK: Step-by-Step

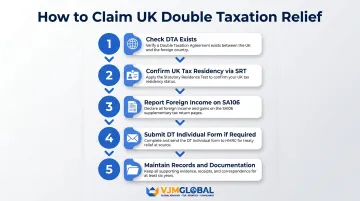

Step 1 — Identify Whether a DTA Exists

Check HMRC's official tax treaties collection to confirm whether the UK has a treaty with the relevant country and what that treaty says about your specific type of income.

Each DTA has its own articles governing employment income, pensions, dividends, interest, royalties, and business profits. The type of income determines which article applies and which country has primary taxing rights.

Step 2 — Determine Your UK Tax Residency

DTR is generally only available to UK residents (assessed under the Statutory Residence Test) or to non-residents with UK-source income seeking relief in their home country.

UK Statutory Residence Test (SRT) key thresholds:

- Spending 183 or more days in the UK in the tax year triggers automatic UK residence

- Fewer days may still result in UK residency if combined with sufficient ties (family, accommodation, work, 90-day tie, country tie)

Getting this step right is foundational. Claiming relief as a resident when you are not—or vice versa—can lead to penalties.

Step 3 — Report Foreign Income on Your UK Self Assessment Tax Return

Relief is claimed through the SA106 (Foreign) supplementary pages of the Self Assessment return.

Key fields on the SA106:

- Box 1-4: Foreign income received (by type)

- Box 19-21: Foreign tax already paid on that income

- HMRC calculates the credit or relief automatically based on what you enter

HMRC guidance confirms: "Use the SA106 supplementary pages to declare foreign income and gains and claim foreign tax credit relief."

Step 4 — Use the Correct Country-Specific DT Individual Form Where Required

For certain countries, HMRC requires completion of a specific DT Individual form, which is submitted to the foreign tax authority for confirmation before relief can be granted.

Countries with specific DT Individual forms (13 total):

- Australia

- Canada

- France

- Germany

- Ireland

- Japan

- Netherlands

- New Zealand

- South Africa

- Spain

- Sweden

- Switzerland

- USA

For all other countries with UK DTAs, use the standard Form DT-Individual.

Process:

- Complete the relevant form

- Send it to HMRC (for UK residence confirmation) or to the foreign tax authority (for foreign residence confirmation)

- The certified form is then submitted to the relevant tax authority for relief to be granted

Step 5 — Maintain Documentation and Records

Keep evidence of:

- Foreign income received (bank statements, contracts, invoices)

- Foreign tax paid (tax certificates, assessments, or statements from the foreign authority)

- Correspondence with foreign tax authorities

- Tax Residency Certificates

Incorrect or incomplete records are a leading cause of rejected DTR claims. This is where professional guidance often makes the difference.

For UK businesses and NRIs navigating the India-UK DTA, treaty provisions around royalties, technical fees, and business profits can be particularly complex. VJM Global works with 250+ UK businesses on cross-border tax matters, covering document preparation, DTAA analysis, form filing, and refund claims across both jurisdictions.

Determining Tax Residency and Dual Residency Rules

The UK Statutory Residence Test (SRT)

HMRC uses the SRT to determine UK tax residency based on days spent in the UK, employment ties, accommodation ties, family ties, and other connection factors.

Automatic UK residence tests:

- Spending 183 or more days in the UK in the tax year

- Only home in the UK for 91 days or more in a row, with at least 30 days spent in it during the tax year

- Working full-time in the UK for any period of 365 days with at least one day in the relevant tax year

Automatic overseas tests:

- Spending fewer than 16 days in the UK (or fewer than 46 days if not UK resident in any of the 3 previous tax years)

- Working abroad full-time with fewer than 91 days in the UK

When neither automatic test produces a clear answer, HMRC applies the Sufficient Ties Test. This counts how many of five connection factors you hold — the more ties, the fewer days you can spend in the UK before becoming resident:

- Family tie – spouse/civil partner or minor child resident in UK

- Accommodation tie – available UK accommodation for 91+ days, at least 1 night spent there

- Work tie – 40+ days of UK work (3+ hours per day)

- 90-day tie – 90+ days spent in the UK in either of the 2 previous tax years

- Country tie – more days in the UK than any other single country (only for "leavers")

Dual Residency: When You're Tax-Resident in Two Countries

It is possible to be tax-resident in both the UK and another country simultaneously under each country's domestic rules. When this occurs, DTA tie-breaker rules apply to determine which country is your "treaty residence" and therefore which has primary taxing rights.

DTA tie-breaker hierarchy (applied in order):

- Permanent home – where you have accommodation "always available" for personal use

- Centre of vital interests – where social, domestic, political, and cultural links are greater

- Habitual abode – where you live "regularly, normally or customarily"

- Nationality – if none of the above resolves the question

Residency vs. Domicile: Understanding the Difference

These two concepts are easy to conflate but carry very different tax consequences:

| Concept | What It Means | Key Tax Impact |

|---|---|---|

| Residency | Annual status set by the SRT based on days and ties | Determines which income streams are taxable in the UK each year |

| Domicile | Long-term concept tied to your permanent, intended home country | UK-domiciled individuals remain liable for UK tax on worldwide income and assets — even during stretches of non-residence |

The difference is especially significant for inheritance tax and the tax treatment of foreign trusts or estates.

What Happens If No UK Double Taxation Agreement Exists?

If no DTA exists between the UK and the country where income was earned, you may still claim Foreign Tax Credit Relief under UK domestic provisions—provided the foreign tax is broadly comparable to UK Income Tax or Capital Gains Tax.

Conditions for unilateral relief (TIOPA10/S9):

- The foreign tax must be charged on income or chargeable gains

- It must correspond to UK Income Tax, Corporation Tax, or Capital Gains Tax

Numerical example:

- You earn £8,000 from a country with no UK DTA

- That country taxes it at 15% = £1,200

- UK tax on that £8,000 at 20% = £1,600

- Unilateral credit relief = £1,200

- You owe HMRC £400

- Total tax paid = £1,600 (the higher UK rate)

This relief only applies when the foreign tax closely mirrors a UK tax. When it doesn't, the picture changes significantly.

Limitation: What If the Foreign Tax Is Not Comparable?

HMRC guidance confirms that turnover taxes, wealth taxes, transaction taxes, and stamp duties do not correspond to UK taxes and are not eligible for unilateral relief.

If the foreign tax paid is not comparable, you will face genuine double taxation with no automatic relief available. In that situation, options are limited: you may be able to claim a deduction (rather than a credit) for the foreign tax against your UK taxable income, or restructure how income flows to avoid the exposure altogether. A cross-border tax adviser can assess which approach applies to your specific circumstances.

Frequently Asked Questions

What is the double tax relief in the UK?

Double taxation relief (DTR) is a mechanism under UK law and bilateral treaties that prevents the same income from being fully taxed in both the UK and another country. Relief is available either as a tax credit (reducing UK tax by the amount paid abroad) or via exemption under a DTA.

Who is eligible for tax relief in the UK?

UK residents who have paid tax on foreign income are generally eligible, as are non-residents with UK-source income seeking relief in their home country. Key conditions include meeting residency criteria under the Statutory Residence Test and having UK-assessable income.

How do I apply for double taxation relief in the UK?

Declare foreign income and foreign tax paid on the SA106 supplementary pages of your UK Self Assessment return. For residents of certain countries — including Australia, Canada, France, Germany, Ireland, Japan, the Netherlands, New Zealand, South Africa, Spain, Sweden, Switzerland, and the USA — you must first submit a country-specific DT Individual form to the foreign tax authority before HMRC can grant relief.

How to avoid double taxation in the US and UK?

The UK-US DTA allows US citizens living in the UK to claim a foreign tax credit on their US return for UK taxes paid, and UK residents with US-source income can claim relief in the UK. However, the saving clause means the US may still tax US citizens on certain income regardless of the treaty. A qualified cross-border tax adviser can help you navigate which income types are affected.

Do Americans pay double tax in the UK?

The US-UK DTA and the Foreign Tax Credit generally prevent actual double taxation for most income types. US citizens must still file a US return on worldwide income, but the treaty and Foreign Tax Credit together typically reduce any additional US tax liability to zero or near zero on UK-earned income.

How do I claim tax relief if I leave the UK?

Notify HMRC of your change of residency using Form P85 and confirm your non-resident status under the SRT. Then check the DTA between the UK and your new country to establish taxing rights over UK-source income (such as pensions or rental income) — you can typically claim relief in your new country of residence under that treaty.