Introduction

Statutory audits in Singapore come with real costs — both in fees and management time. Under Section 205 of the Companies Act 1967, all registered companies must appoint an auditor and have their financial statements audited annually.

Since 2015, however, smaller private companies have had a way out. The "small company" audit exemption, governed by Section 205C of the Companies Act and the Thirteenth Schedule, allows eligible private companies to skip this requirement entirely — potentially saving thousands of dollars in annual compliance costs.

If you're a business owner, foreign investor, or finance professional managing a Singapore-incorporated company, this guide covers exactly what you need: the qualifying criteria, how to apply the tests correctly, and what compliance obligations remain even after exemption.

Pay particular attention if you're managing a foreign-owned subsidiary within a multinational group structure. Both individual company-level and group-level tests must be satisfied — and missing either one disqualifies the exemption.

Key Takeaways

- Private companies qualify for audit exemption by meeting at least two of three "small company" thresholds under the Companies Act

- The three thresholds: annual revenue ≤ SGD 10 million, total assets ≤ SGD 10 million, and ≤ 50 employees for two consecutive prior financial years

- Group companies must satisfy the criteria both individually and on a consolidated group basis

- Exemption removes the audit requirement — financial statement preparation and ACRA filing obligations still apply

- ACRA is reviewing the revenue and asset limits as of early 2026; higher thresholds may follow

What Is Audit Exemption in Singapore?

For many private companies in Singapore, audit exemption can mean thousands of dollars in saved compliance costs each year. Under Section 205C of the Singapore Companies Act, eligible companies are relieved from the statutory obligation to appoint a registered public accountant and have their financial statements formally audited annually. Companies must actively qualify for it each year — it is not granted by default, and eligibility is assessed based on specific criteria.

Historical Context and Evolution

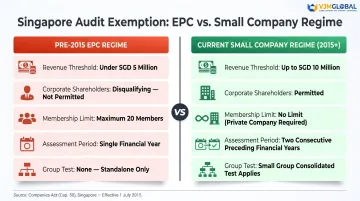

Before July 2015, only "exempt private companies" (EPCs) with annual revenue below SGD 5 million qualified for audit exemption. The structure was highly restrictive: no more than 20 members, and no corporation could hold any beneficial interest in shares.

This meant any company with corporate shareholders was automatically disqualified — regardless of size or revenue.

The 2014 amendment to the Companies Act introduced the broader "small company" concept, which took effect for financial years beginning on or after 1 July 2015. This reform expanded the pool of eligible businesses by:

- Doubling the revenue threshold from SGD 5 million to SGD 10 million

- Removing the corporate shareholder restriction entirely

- Adding asset and employee thresholds to create a more comprehensive size assessment

- Requiring a two-year consecutive assessment period to prevent opportunistic timing

Policy Rationale

Singapore's audit exemption framework serves three clear goals: lower compliance costs for SMEs, reduced administrative burden for qualifying companies, and alignment with international regulatory practices. According to ACRA's February 2026 press release, the framework balances easing that burden with preserving adequate corporate governance oversight.

The statutory audit requirement for larger companies remains fully intact, maintaining accountability where broader public interest and a larger stakeholder base warrant external scrutiny.

Who Qualifies for Audit Exemption: The Small Company Criteria

The Two-Part Qualification Test

To qualify for audit exemption, a company must satisfy two conditions simultaneously:

- Be a private company during the financial year in question

- Meet at least two of three quantitative criteria for the immediate past two consecutive financial years

Both conditions are mandatory. A company that satisfies the quantitative thresholds but ceases to be a private company at any point during the financial year loses its exemption eligibility entirely.

The Three Quantitative Criteria

Under the Thirteenth Schedule of the Companies Act, the three thresholds are:

| Criterion | Threshold |

|---|---|

| Total annual revenue | Not more than SGD 10 million |

| Total assets (year-end) | Not more than SGD 10 million |

| Number of employees (year-end) | Not more than 50 |

Revenue: Measured per financial statements prepared under applicable Singapore accounting standards, covering all operating revenue recognized during the financial year.

Total assets: The balance at year-end calculated under applicable accounting standards, including all current and non-current assets before deduction of liabilities.

Employees: Full-time headcount at year-end. Part-time and contract workers should be assessed based on their classification under applicable accounting standards — companies with significant variable workforce should verify their count carefully.

The Two-Year Consecutive Rule

A company must satisfy at least two of the three criteria in each of the two financial years immediately before the current year. Failing to meet the criteria in even one of those two years disqualifies the company.

Practical Example:

To assess eligibility for audit exemption in FY2024:

- Review FY2022 results: Does the company meet 2 of 3 criteria?

- Review FY2023 results: Does the company meet 2 of 3 criteria?

- If yes to both, the company qualifies as a small company for FY2024

- If no to either year, the company does not qualify for FY2024

Newly incorporated companies face a different situation — they simply don't have two years of history to evaluate.

Special Rules for Newly Incorporated Companies

The Thirteenth Schedule accounts for companies without a two-year track record:

- First or second financial year: Qualifies if the company is private and meets at least 2 of 3 criteria for that year alone

- Third financial year onwards: The standard two-year consecutive rule applies

ACRA's 2026 Threshold Review

On 26 February 2026, ACRA announced a review of the audit exemption framework, with industry consultations running from March 2026. The review focuses on two areas:

- Raising revenue and asset thresholds — as company asset values and revenues have grown since the framework launched in 2015, the current SGD 10 million limits may no longer reflect market reality

- Subsidiary eligibility — exploring whether subsidiaries could qualify even if their consolidated group exceeds the thresholds

ACRA requested public feedback by 17 April 2026. No revised figures have been announced yet, but the review signals potential expansion of exemption eligibility in the near term.

Group Companies and Special Scenarios

The Dual Test for Group Companies

Even if a Singapore subsidiary individually qualifies as a small company, it only receives audit exemption if the entire group also qualifies as a "small group." Both conditions must be met simultaneously.

This dual test prevents large multinational corporations from structuring small Singapore subsidiaries to avoid audit requirements while maintaining substantial consolidated operations elsewhere.

The Small Group Test

Under Section 205C(3)-(4) and the Thirteenth Schedule, Paragraph 2, the group (including foreign parent and all subsidiaries) must meet at least two of the same three criteria on a consolidated basis for two consecutive preceding financial years:

- Consolidated revenue ≤ SGD 10 million

- Consolidated total assets ≤ SGD 10 million

- Consolidated employees ≤ 50

Consolidation follows Singapore Financial Reporting Standards (SFRS) or IFRS, as applicable. If the parent company prepares consolidated financial statements, use those figures. If not, manually total the assets, revenue, and employee count of all group members.

Foreign Holding Company Scenario

The small group test applies regardless of where the parent is incorporated. When a parent company is based outside Singapore — in the USA, UK, or Australia, for instance — the Singapore subsidiary must still assess whether the overall group qualifies as a small group.

Key steps:

- Obtain consolidated financial statements from the foreign parent if available

- If consolidated statements are not prepared, aggregate:

- Total revenue of parent and all subsidiaries

- Total assets of parent and all subsidiaries

- Total employee count across all entities

- Apply the two-of-three test to these consolidated figures

- Check if the criteria are met for each of the two preceding financial years

Corporate Shareholders Are Now Permitted

Under the current small company framework (effective from 2015), companies with corporate shareholders still qualify for audit exemption. This is a critical distinction from the old exempt private company (EPC) regime, which excluded companies with any corporate shareholders.

Many foreign-owned subsidiaries overlook this change and incorrectly assume that a corporate parent automatically disqualifies them.

It does not. Under the current framework, only the quantitative thresholds and group-level tests matter — corporate ownership structure has no bearing on eligibility.

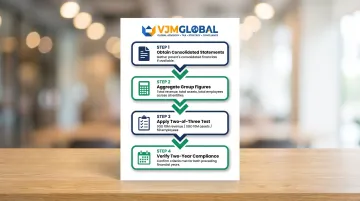

How to Assess and Maintain Your Audit Exemption Status

Determining Eligibility: A Step-by-Step Approach

Step 1 — Confirm private company status

Verify the company is a private company (as defined under the Companies Act) throughout the financial year. Public companies and certain listed entities do not qualify regardless of size.

Step 2 — Gather the two preceding years' financial data

Collect for each of the two financial years immediately before the current year:

- Total annual revenue

- Total assets (year-end)

- Full-time employee count (year-end)

Use figures from financial statements prepared under applicable Singapore accounting standards.

Step 3 — Apply the two-of-three test

Check if the company meets at least two of the three quantitative criteria in each of those two preceding years:

- If yes in both years → qualifies as a small company for current year

- If no in either year → does not qualify

Step 4 — Check group status if applicable

If the company is part of a group, repeat the two-of-three test using consolidated group-level figures for the same two preceding years. Only if both the company individually and the group collectively pass does the exemption apply.

Maintaining or Losing the Exemption

Passing the eligibility assessment is only part of the equation. Companies must also track their status year on year, since both growth and structural changes can affect the exemption going forward.

Once a company qualifies as a small company, it retains the exemption in subsequent years automatically; no reapplication is required. That said, eligibility must be monitored each year.

Disqualification triggers:

A company loses its small company status if:

- It ceases to be a private company at any time during a financial year, OR

- It fails to meet at least two of the three quantitative criteria for each of the two most recent consecutive financial years

- One year of threshold breach is not enough — two consecutive years of failing are required before disqualification takes effect

For companies managing multi-entity group structures or cross-border operations, tracking consolidated figures across two financial years adds meaningful complexity — and getting those calculations wrong can trigger an unexpected audit requirement.

What Audit Exemption Does Not Remove: Remaining Obligations

Financial Statement Preparation and Filing

Audit exemption only removes the requirement to appoint a registered public accountant and have accounts formally audited. It does not remove the obligation to prepare annual financial statements.

Exempt companies must still:

- Prepare financial statements in accordance with prescribed Singapore accounting standards

- File unaudited financial statements with ACRA

- Submit annual returns accompanied by financial statements

- Maintain proper accounting records under Section 199 of the Companies Act

The distinction matters: "audit exemption" means "exemption from external audit," not "exemption from accounting and financial reporting."

Shareholders' Override Right

Under Section 205B(6), shareholders holding 5% or more of voting rights can require the company to conduct a formal audit even if it qualifies for exemption. This must be done by written notice during a financial year but not later than one month before the end of that year.

Companies should be aware this right exists and plan accordingly if significant minority shareholders are present.

ACRA's Compliance Oversight

Shareholder rights aside, ACRA also retains independent authority to intervene. The Registrar conducts periodic spot checks on financial statements of all companies, including exempt ones. Under Section 205D, ACRA may require any exempt company to lodge audited financial statements if:

- There has been a breach of Section 199 (accounting records) or Section 201 (financial statements)

- It is otherwise in the public interest to do so

In cases involving legal disputes or regulatory concerns, ACRA may appoint an auditor regardless of exempt status.

This means the quality of your bookkeeping affects more than compliance — it determines how exposed you are if ACRA ever takes a closer look.

Common Misconceptions About Audit Exemption in Singapore

"Audit Exemption Means Informal Accounting"

The most common misconception is that audit exemption allows companies to be informal or imprecise about their accounting. In reality, exempt companies must still maintain proper accounting records and prepare financial statements that comply with applicable standards. The only thing removed is the formal external audit requirement.

That said, the compliance obligations remain real. Companies must retain accounting records for at least 5 years under Section 199(2), and directors must confirm in the annual return that records have been kept in accordance with Section 199. Non-compliance can result in penalties and potential loss of exemption.

Confusion Between EPC and Small Company Regimes

Many business owners operating through corporate structures still assume they're disqualified from exemption — but this confusion stems from outdated rules. Corporate shareholders were disqualifying under the old exempt private company (EPC) framework, but the small company criteria introduced in 2015 changed that entirely.

Key differences:

| Feature | Pre-2015 EPC Regime | Current Small Company Regime |

|---|---|---|

| Revenue threshold | < SGD 5 million | ≤ SGD 10 million (2 of 3 test) |

| Corporate shareholders | Disqualifying | Not disqualifying |

| Max shareholders | 20 members | No limit (must be private company) |

| Assessment period | Single financial year | 2 immediately preceding FYs |

| Group test | Not applicable | Small group test on consolidated basis |

"Qualifying Once Means Permanent Exemption"

A company that qualifies this year can lose exemption the next if revenue or assets spike — eligibility is re-evaluated against the two immediately preceding consecutive financial years, every year. Assuming continued exemption without checking is one of the most common compliance gaps.

To stay ahead of this:

- Monitor revenue, assets, and employee headcount against thresholds quarterly

- Flag any year where two of the three criteria approach the upper limits

- Build threshold checks into the annual return preparation process

- Reassess group-level eligibility if the company is part of a corporate group

Frequently Asked Questions

What is the audit exemption threshold in Singapore?

The current thresholds are total annual revenue ≤ SGD 10 million, total assets ≤ SGD 10 million, and total employees ≤ 50. A company must meet at least two of these three criteria for the two immediately preceding consecutive financial years. ACRA is reviewing these thresholds as of 2026.

How to apply for audit exemption in Singapore?

There is no formal application process — a company self-assesses whether it meets the small company criteria each year and, if eligible, simply does not appoint a statutory auditor for that financial year.

What is the 2-year rule for audit exemption?

The 2-year rule requires a company to satisfy at least two of the three quantitative criteria (revenue, assets, employees) in each of the two financial years immediately preceding the current year. Missing that threshold in even one of those two years disqualifies the company.

Can a company with corporate shareholders qualify for audit exemption in Singapore?

Yes, under the current small company framework (effective from 2015), the presence of corporate shareholders does not disqualify a company. This is a key difference from the previous exempt private company (EPC) regime, which excluded companies with any corporate beneficial interest.

Do audit-exempt companies still need to prepare and file financial statements?

Yes, audit exemption does not remove the requirement to prepare and file annual financial statements with ACRA. Exempt companies must still file unaudited accounts prepared in accordance with Singapore accounting standards and maintain proper accounting records.

When does a company lose its audit exemption status in Singapore?

A company loses its exemption if it ceases to be a private company, or if it fails to meet at least two of the three quantitative criteria across the two most recent consecutive financial years. One underperforming year does not trigger disqualification — two consecutive years of missing the criteria do.