Whether you're a foreign entrepreneur setting up a Singapore subsidiary, a CFO managing cross-border operations, or a director of a small private company trying to understand your obligations, navigating Singapore's statutory audit regime can feel complex. This guide breaks down exactly what a statutory audit is, who must comply, when exemptions apply, what the audit process involves, and the serious consequences of non-compliance — giving you a clear roadmap to stay compliant and leverage audits as a strategic asset.

Key Takeaways

- Statutory audits are legally required for most Singapore companies under the Companies Act, conducted by an ACRA-registered Public Accountant

- Small companies passing the 2-of-3 test (revenue, assets ≤S$10M; ≤50 employees) for two consecutive years can claim audit exemption

- Auditors must be appointed within 3 months of incorporation; failure to appoint can result in fines up to S$5,000

- Missing filing deadlines triggers penalties from S$300 upward, with directors facing personal liability and disqualification for repeat offences

- Clean audit reports strengthen investor confidence, support loan applications, and are mandatory for SGX listing

What Is a Statutory Audit in Singapore?

A statutory audit is a legally mandated, independent examination of a company's financial records conducted by a qualified Public Accountant registered with the Accounting and Corporate Regulatory Authority (ACRA). The auditor's task is to determine whether the financial statements present a "true and fair view" of the company's financial position in accordance with Singapore Financial Reporting Standards (SFRS).

Legal Framework and Governing Authority

The Companies Act 1967 (Cap. 50) establishes the statutory audit requirement. Unless specifically exempted under Sections 205B or 205C, every Singapore-incorporated company must have its financial statements audited annually by a registered Public Accountant.

ACRA oversees the entire framework, administering the registration of Public Accountants under the Accountants Act. The Public Accountants Oversight Committee (PAOC) provides independent oversight (most PAOC members are not practicing accountants, ensuring impartiality). As of March 2024, Singapore had 1,531 registered Public Accountants and 761 accounting entities.

Financial Reporting Standards

Companies must prepare financial statements using Singapore Financial Reporting Standards (International) — SFRS(I), which are essentially identical to IFRS as confirmed by the IFRS Foundation. Singapore adopted this IFRS-converged framework for annual periods beginning on or after 1 January 2018.

Under Section 201(2) of the Companies Act, financial statements must comply with Accounting Standards and give a true and fair view. Where strict compliance would distort the true financial position, Section 201(13) permits a "true and fair view override" — allowing limited departure from the standard to the extent necessary.

Types of Audit Opinions

Under Singapore Standards on Auditing (SSA) 705 (Revised), auditors may issue four types of opinion:

- Unqualified (unmodified) opinion — financial statements are free from material misstatement

- Qualified opinion — misstatements are material but not pervasive

- Adverse opinion — misstatements are both material and pervasive

- Disclaimer of opinion — insufficient evidence obtained to form an opinion

Beyond Legal Compliance

A statutory audit does more than satisfy a legal obligation. It provides an independent check that strengthens investor confidence, deters financial misconduct, and upholds Singapore's corporate governance standards. For multinationals operating across jurisdictions, a clean Singapore audit report carries weight in global financial reporting — lenders, regulators, and parent companies in other markets frequently rely on it.

Who Is Required to Undergo a Statutory Audit in Singapore?

Under the Companies Act, most Singapore-incorporated companies must appoint an auditor within three months of incorporation. Under Section 173A(1), auditor appointment details must be notified to the Registrar within 14 days.

Entities Mandated to Audit

The following categories cannot claim exemption and must undergo a full statutory audit every year:

- Private limited companies that exceed the "small company" thresholds (detailed in the next section)

- Public companies, including those listed on the Singapore Exchange (SGX)

- Foreign companies and branch offices operating in Singapore that file financial statements with ACRA

- Charities and non-profit organisations whose gross annual receipts or total expenditure reach S$500,000 or above, and all Institutions of a Public Character (IPCs) regardless of size

- Companies regulated by the Monetary Authority of Singapore (MAS), such as licensed financial institutions and banks

Foreign-Owned and Multinational Entities

Foreign companies expanding into Singapore should note that even if their home jurisdiction offers audit exemptions, their Singapore operations may still be subject to full audit requirements. For instance, a UK-based holding company might qualify for audit exemption under UK small company rules, but its Singapore subsidiary may still require a statutory audit if the broader group exceeds Singapore's small group thresholds.

Confirming which rules apply before incorporation — rather than after — avoids compliance gaps that can prove costly to unwind.

Consequences of Missed Auditor Appointment

If a company fails to appoint an auditor within the required timeframe, shareholders may appoint one at a general meeting. If that doesn't happen, ACRA may step in and appoint an auditor on the company's behalf — with penalties and potential enforcement action to follow. Failure to appoint an auditor carries a fine of up to S$5,000 plus default penalties for continued non-compliance.

Audit Exemptions: Small Company and Small Group Criteria

The Companies (Amendment) Act 2014 introduced the small company and small group audit exemptions, effective for financial years starting 1 July 2015 or later. This reform aimed to reduce regulatory burden on smaller entities while preserving financial accountability.

Small Company Exemption

To qualify as a "small company" and claim audit exemption, a private limited company must satisfy at least 2 of the following 3 quantitative criteria for the immediately preceding two consecutive financial years:

| Criterion | Threshold |

|---|---|

| Total annual revenue | S$10 million or less |

| Total assets | S$10 million or less |

| Number of employees | 50 or fewer |

Employee count is based on full-time staff at the financial year end.

Example: A private company with revenue of S$8 million, total assets of S$11 million, and 45 employees would qualify (meeting 2 of 3 criteria: revenue and employees).

Newly Incorporated Companies

Since a newly incorporated company has no two-year history, it assesses eligibility year by year. Meeting the 2-of-3 criteria in year one grants immediate qualification. Missing it in year one allows another attempt in year two. Once two consecutive qualifying years are achieved, the company establishes its exemption status.

Small Group Exemption

If a company is part of a group (under common control with other entities), exemption requires the entire group to qualify as a "small group" on a consolidated basis. The parent and all subsidiaries must collectively meet at least 2 of the same 3 thresholds.

This consolidated requirement is where many foreign-owned subsidiaries run into difficulty. A Singapore subsidiary with revenue of only S$3 million cannot claim exemption if its overseas parent group has combined revenue of S$50 million — the entire consolidated group must qualify.

When Exemption Status Changes

A company loses small company status if:

- It ceases to be a private company at any point during the financial year

- It fails to meet at least 2 of the 3 criteria across the previous two consecutive financial years

Directors should review exemption status annually. Inadvertent non-compliance — operating on the assumption of exemption when the company has outgrown the thresholds — is a common trigger for ACRA enforcement.

Dormant Company Exemption

A dormant company — one with no accounting transactions since incorporation or since the end of the previous financial year — is also exempt from audit under Section 205B.

Certain activities do not count as accounting transactions:

- Taking of subscriber shares

- Appointment of a company secretary or auditor

- Maintenance of a registered office

- Keeping statutory registers

- Payment of statutory fees, penalties, or nominal sums

Dormant companies must still file annual returns and maintain basic accounting records with ACRA.

Note that shareholders holding at least 5% of issued shares retain the right to require an audit — provided they give written notice at least one month before the financial year end.

The Statutory Audit Process: A Step-by-Step Overview

The statutory audit is a structured, multi-phase engagement designed to verify accuracy, assess internal controls, and issue an independent opinion. Directors bear legal responsibility for the accuracy of financial statements, not just the accountants preparing them.

Preparation of Financial Statements

Before the audit begins, directors must prepare:

- Financial statements compliant with SFRS (or SFRS for Small Entities, if eligible)

- Accurate bookkeeping records maintained throughout the financial year

- XBRL format submissions via ACRA's BizFinx system (required since 2018 for most companies)

Late or incomplete XBRL filings can result in penalties and audit delays. ACRA's filing requirements specify different templates based on company size: simplified XBRL applies when both revenue and assets fall below S$500,000, while larger entities must use the full XBRL format.

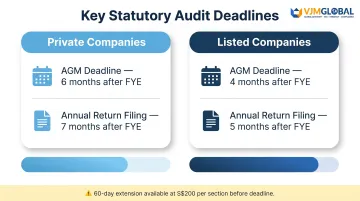

Appointment of Auditors and Key Deadlines

Auditor appointment: Within 3 months of incorporation

Key filing deadlines:

| Requirement | Private Companies | Listed Companies |

|---|---|---|

| Hold AGM | Within 6 months of FYE | Within 4 months of FYE |

| File Annual Return (AR) | Within 7 months of FYE | Within 5 months of FYE |

Companies can apply for a 60-day extension for a fee of S$200 per section, but the application must be submitted before the deadline. Early auditor appointment prevents rushed reporting and avoids late filing penalties.

What the Auditor Reviews

During the engagement, auditors examine:

- Revenue and expense recognition accuracy

- Asset valuations and liabilities

- Tax compliance with IRAS standards

- Internal control systems and fraud prevention risk

- Overall compliance with SFRS

Findings are consolidated in the Auditor's Report, which expresses whether accounts give a "true and fair view." Under Singapore Standards on Auditing, the report specifies the type of opinion issued and highlights any significant matters.

Compilation Reports vs. Audit: When Exempt Companies Still Need Help

Audit-exempt companies still need to prepare compliant financial statements. Many engage accounting firms to produce a compilation report — governed by Singapore Standard on Related Services (SSRS) 4410 (Revised).

A compilation report organizes financial data into properly formatted statements but provides no independent assurance. It is not a substitute for an audit. That said, it helps directors meet their statutory responsibilities and supports common stakeholder needs:

- Bank loan applications requiring structured financials

- Shareholder reporting and internal management review

- Regulatory submissions where full audit is not mandated

VJM Global supports clients through both audit preparation and compilation engagements. Services cover financial record organization, workpaper preparation, trial balance reconciliation, and control checks — helping businesses across jurisdictions stay compliant and audit-ready.

Key Benefits of a Statutory Audit Beyond Compliance

While many business owners view audits as a regulatory burden, they deliver tangible strategic value.

Credibility Signal for Banks and Investors

Lenders routinely require audited financial statements from SMEs seeking credit facilities — particularly for term loans and trade financing. Verified financials give banks and investors confidence in your numbers, which typically translates to faster approvals and better lending terms.

Fraud Detection and Operational Insight

Auditors often identify weaknesses in internal controls and issue a Management Letter with recommendations to improve financial workflows. For many companies, that letter is where the real value lies — a structured blueprint for tightening controls and reducing financial risk.

ACRA's 2024 Audit Regulatory Report found approximately 15% of non-PIE public accountants rated "Not Satisfactory" during Practice Monitoring Programme inspections. That figure matters when choosing an auditor — a quality firm does more than sign off; it flags issues your internal team may have missed.

IPO Readiness and Business Valuation

That governance track record built through annual audits pays dividends when it counts most. Clean audited financials directly strengthen your position in three high-stakes scenarios:

- Business sale: Buyers price risk into offers — verified accounts reduce that discount

- IPO application: Audited records demonstrate operational maturity to underwriters

- Investor fundraising: Due diligence moves faster when financials are already verified

SGX Mainboard Rule 210(4)(d) requires that audited financial statements submitted with a listing application must not be subject to an adverse opinion, qualified opinion, or disclaimer of opinion, and must not include a going-concern material uncertainty statement. This makes voluntary audits a smart long-term strategy even for exempt companies with growth ambitions.

Penalties for Non-Compliance with Audit Requirements

ACRA actively enforces compliance under the Companies Act, and directors are held personally accountable.

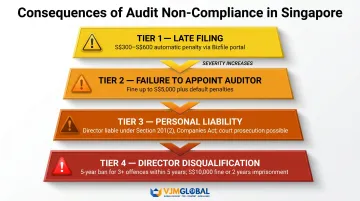

Late Filing Penalties

| Delay Duration | Penalty Amount |

|---|---|

| Up to 3 months after deadline | S$300 |

| More than 3 months after deadline | S$600 |

The Bizfile portal applies these penalties automatically at the point of submission. ACRA's revised penalty framework became effective 30 April 2021, standardising late filing fees.

Failure to Appoint Auditor

Failure to appoint an auditor within the required timeframe or deliberate/repeated non-compliance can lead to:

- Fines up to S$5,000 plus default penalties

- Court prosecution under Section 197(1B)

- Personal liability for directors under Section 201(2)

Director Disqualification

Repeated violations carry the most severe consequence. Under Section 155 of the Companies Act, a director can be disqualified for 5 years if found guilty of 3 or more offences related to filing or delivery requirements within a 5-year period.

A disqualified person who acts as a director without court permission faces a fine of up to S$10,000, imprisonment of up to 2 years, or both.

Cascading Operational Consequences

Non-compliance records on ACRA's public registry can:

- Hinder loan approvals

- Disqualify companies from government tender eligibility

- Affect license renewals

- Damage investor confidence

Because ACRA's registry is publicly searchable, lenders, government agencies, and potential partners can all see a company's compliance history — making a clean record a practical business asset.

Frequently Asked Questions

What does a statutory audit mean?

A statutory audit is a legally required, independent examination of a company's financial records by a qualified Public Accountant, mandated under Singapore's Companies Act, to verify that financial statements present a true and fair view of the company's financial position.

What is the difference between FRS and SFRS?

FRS refers to the broader international standards framework, while SFRS (Singapore Financial Reporting Standards) is Singapore's locally adapted version, closely aligned with IFRS. All Singapore-incorporated companies must apply SFRS when preparing financial statements for statutory audit.

Is a statutory audit mandatory for all companies in Singapore?

Not all companies require a statutory audit. Private limited companies qualifying as "small companies" or "small groups" — meeting 2 of 3 thresholds (revenue, assets ≤S$10 million; staff ≤50) for two consecutive years — are exempt. Public companies, MAS-regulated firms, and foreign branch offices are not.

Who can perform a statutory audit in Singapore?

Only a Public Accountant or accounting firm registered with ACRA is authorised to perform statutory audits in Singapore. Companies cannot use an unregistered accountant or internal staff to satisfy this requirement.

What is the difference between a statutory audit and a compilation report?

A statutory audit involves independent verification of financial statements through testing and assessment, whereas a compilation report simply organises a company's financial data into formatted statements without providing any independent assurance or verification.

What are the penalties for failing to comply with statutory audit requirements in Singapore?

Penalties include late filing fines (S$300–S$600), fines up to S$5,000 for failure to appoint an auditor, potential personal liability and director disqualification under the Companies Act, and reputational harm through ACRA's public compliance records.

Need Expert Support for Your Singapore Statutory Audit?

VJM Global supports multinational businesses with cross-border compliance advisory, audit preparation, and accounting services across Singapore and India. Our Chartered Accountants and compliance specialists help you navigate statutory obligations accurately and on time.

Contact us at info@vjmglobal.com or call +91 9213397070 to discuss your audit and compliance needs.