Introduction

Singapore companies are increasingly establishing entities in UAE free zones to access the Middle East and Africa markets. Bilateral trade between the two nations reached SGD 26.37 billion in 2025, and DMCC alone recorded a 13% rise in Singapore company registrations that same year, with approximately 400 Singapore companies now operating in that zone.

The GCC-Singapore Free Trade Agreement (GSFTA) has further reduced trade barriers — but with easier market access comes a compliance obligation many owners overlook: mandatory annual audits.

Many Singapore company owners assume that low-activity or remotely managed UAE free zone entities are exempt from annual audits. They're not. Audit obligations apply regardless of the owner's country of incorporation or residence, and non-compliance carries significant consequences.

This guide covers the legal basis for UAE free zone audits, free zone-specific requirements, what Singapore companies must prepare, key deadlines, and consequences of non-compliance.

Key Takeaways

- Audits are mandatory for virtually all UAE free zone entities, including those owned by Singapore companies

- UAE audits must comply with IFRS — Singapore companies using SFRS need to verify full IFRS alignment before filing

- Missing an audit blocks license renewals, freezes banking access, and triggers penalties

- Deadlines vary by free zone, from 90 days to 6 months post-year-end

- Only UAE-registered, free zone-approved auditors can sign off on these audits

Why Singapore Companies Establish UAE Free Zone Entities

Singapore companies are attracted to UAE free zones for several strategic reasons:

Key advantages include:

- 100% foreign ownership without local sponsor requirements

- 0% corporate tax for qualifying free zone persons

- Full repatriation of capital and profits

- Customs duty exemptions on imports and exports

- UAE's strategic location bridging South Asia, Africa, and Europe

Singapore businesses often use UAE free zones as a regional holding or trading base, using the UAE's position as a major trade hub. The UAE's total foreign trade reached AED 5.23 trillion in 2024, accounting for 41% of Middle East exports.

The GCC-Singapore Free Trade Agreement (GSFTA) has reduced trade barriers between the two regions, encouraging Singapore businesses to formalize their UAE presence. As more entities establish a registered footprint in UAE free zones, they become subject to local audit and compliance obligations — which is precisely what this guide addresses.

UAE Free Zone Audit Obligations: The Legal Framework

UAE free zone companies — regardless of shareholder nationality or country of incorporation — are governed by their specific free zone authority's regulations. Almost all major free zones mandate annual external audits. Singapore companies, in particular, face two distinct compliance layers that can both independently require audited financials:

Two audit triggers apply:

- Free zone licensing: Most free zones require audited financial statements to renew your annual trade license

- UAE Corporate Tax Law requirement — Federal Decree-Law No. 47 of 2022 makes audited financials effectively mandatory for entities seeking 0% qualifying free zone person tax status

IFRS Compliance Requirement

All UAE free zone audits must be prepared according to International Financial Reporting Standards (IFRS). While Singapore's Financial Reporting Standards (SFRS) align closely with IFRS, the two are not identical — and UAE regulators require full IFRS compliance, not SFRS compliance.

Key differences to check with a UAE-registered auditor:

- Listed Singapore companies use SFRS(I), adopted in 2018, which mirrors IFRS closely but with transitional differences

- Non-listed companies may still use SFRS or SFRS for Small Entities — both carry potential gaps

- Revenue recognition and financial instruments are the most common areas where SFRS and IFRS diverge

Approved Auditor Requirement

UAE free zone audits must be conducted by an auditor approved by the relevant free zone authority. A Singapore-based CPA or audit firm cannot sign off on UAE free zone financial statements. Key requirements for the appointed auditor:

- Registered under the UAE Ministry of Economy with a valid professional license

- Approved by the specific free zone authority where your entity is licensed

- Familiar with both IFRS and the free zone's reporting format requirements

Record Retention Obligation

Companies in UAE free zones must maintain financial records for a minimum of 7 years under the Corporate Tax Law. Singapore companies should ensure their UAE entity maintains these records locally at the registered office or an agreed location — not solely in Singapore.

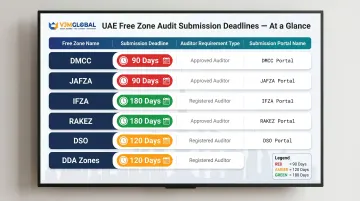

Audit Requirements by Major UAE Free Zone

Each UAE free zone sets its own audit rules, deadlines, and approved auditor requirements. The table below gives Singapore companies a quick reference before the detailed breakdown.

| Free Zone | Submission Deadline | Auditor Requirement | Submission Portal |

|---|---|---|---|

| DMCC | 180 days after year-end | DMCC Approved Auditor List | DMCC Member Portal |

| JAFZA | 90 days after year-end | DET-licensed auditor | Dubai Trade Portal |

| IFZA | ~3 months before renewal | IFZA Approved Auditor List | IFZA Portal |

| RAKEZ | 180 days after year-end | Ministry of Economy licensed | RAKEZ Portal |

| DSO | 120 days after year-end | DSO-approved auditor | DSO Portal |

| DDA Zones | 180 days after year-end | DDA-registered auditor | AXS Portal |

| Shams/Meydan | Verify with authority | Varies | Varies |

DMCC (Dubai Multi Commodities Centre)

DMCC is one of the most popular free zones for Singapore trading and commodities companies. Key requirements include:

- Annual audit mandatory for all DMCC entities including dormant companies

- Audited financial statements must be submitted through the DMCC Member Portal before license renewal

- DMCC rejects renewals if financials are incomplete or incorrectly formatted

- Deadline: 180 days (6 months) after financial year-end

- Only auditors from DMCC's Approved Auditor List accepted

JAFZA (Jebel Ali Free Zone)

JAFZA is popular for Singapore logistics, trading, and manufacturing companies due to its proximity to Jebel Ali Port:

- Audited financial statements mandatory for FZE and FZCO structures

- Both single-owner (FZE) and multi-owner (FZCO) setups require mandatory audits

- Auditor must be licensed by Dubai Economy and Tourism (DET)

- Deadline: 90 days after financial year-end

- Submission through the Dubai Trade portal

IFZA (International Free Zone Authority)

IFZA has grown popular with Singapore SMEs and startups due to lower setup costs:

- Audited financial statements required at every annual renewal

- Zero-revenue or dormant companies must file a Zero-Activity Audit

- Deadline: Prepare financials at least 3 months before renewal to avoid delays

- Approved auditor list maintained by IFZA

RAKEZ (Ras Al Khaimah Economic Zone)

RAKEZ is a cost-effective option favored by Singapore manufacturing and trading companies:

- Audited statements required for all entity types

- Deadline: 180 days (6 months) after financial year-end

- Trading companies must provide customs and shipment records as supporting documents

- Ministry of Economy issues licenses; compliance follows Federal Law No. 12 of 2014

DSO and Other Dubai Free Zones

Dubai Silicon Oasis (DSO):

- Audited statements required within 4 months of year-end

- DSO-approved auditor list must be consulted

DDA-governed free zones (Dubai Internet City, Dubai Media City, etc.):

- Mandate audits for all FZ-LLCs and branch offices

- 6-month submission deadline

- Submission through AXS Portal

- Covers 9 different free zones under DDA authority

Shams and Meydan:

- Annual audits required for license renewal

- Documentation requirements vary by entity type

- Verify current deadlines directly with the authority before filing

What UAE Auditors Review: Documentation Checklist

UAE auditors require detailed documentation maintained at the UAE entity level — not just at the Singapore parent level:

Core financial documents:

- Bank statements (both UAE accounts and international accounts used for entity transactions)

- Sales invoices and purchase orders

- Expense receipts and payment vouchers

- Contracts and agreements with clients and suppliers

- Memorandum and articles of association

- Current trade license

- Proof of share capital

Beyond the core document set, auditors dig into three areas that consistently create issues for Singapore-owned free zone entities.

Cross-Border Transaction Scrutiny

Auditors closely examine related-party transactions between the Singapore parent company and its UAE free zone subsidiary. These transactions must be documented at arm's length pricing. The UAE Federal Tax Authority actively enforces transfer pricing rules under corporate tax regulations, and any transaction with the Singapore parent must demonstrate fair value with supporting documentation.

VAT and Corporate Tax Alignment

Auditors verify:

- VAT registration status is correct (mandatory registration threshold: AED 375,000)

- VAT returns reconcile with financial statements

- Entity qualifies for 0% corporate tax as a Qualifying Free Zone Person

Singapore companies that co-mingle mainland UAE activities with free zone activities risk losing qualifying status, triggering a 9% corporate tax rate.

Multi-Currency Considerations

UAE free zone entities owned by Singapore companies often transact in SGD, USD, and AED simultaneously. Auditors require:

- Proper currency conversion documentation

- Reconciliation of multi-currency transactions

- Accurate exchange rate records for payments processed through PayNow, SWIFT transfers, or digital payment processors

Missing or inconsistent exchange rate records are a common audit flag — gaps here can trigger adjustments to reported revenue and tax liability.

Submission Deadlines and Non-Compliance Consequences

Key Submission Deadlines by Free Zone

| Free Zone | Deadline After Financial Year-End |

|---|---|

| JAFZA, DWC, SAIF Zone | 90 days |

| DSO | 4 months |

| DMCC, RAKEZ | 6 months (180 days) |

| DDA Zones | 6 months |

Financial year-end is flexible in UAE free zones but must be at least 6 months and no more than 18 months from incorporation. Many Singapore companies align with Singapore's December 31 fiscal year for consolidated reporting convenience. Getting this alignment right matters — missing a submission deadline by even a few weeks can trigger the consequences below.

Consequences of Non-Compliance

Financial penalties:

- Commercial free zones: AED 2,500 to AED 5,000

- Financial free zones (DIFC, ADGM): Up to USD 25,000

Operational impacts:

- Trade license renewal blocked without audit submission

- Visa issuance and renewals for employees and dependents frozen

- UAE bank accounts flagged or closed when audited statements are requested

- Inability to repatriate funds or service contracts

Tax audit exposure:

- The UAE Federal Tax Authority (FTA) can initiate independent tax audits with as little as 10 business days' notice

- Standard audit limitation period is 5 years — but extends to 15 years where tax evasion is suspected

- Non-compliant entities face back assessments, penalties, and potential license cancellation across that entire window

Practical Steps to Prepare for Your UAE Free Zone Audit

Preparation checklist for Singapore companies:

- Appoint a UAE-registered auditor 2-3 months before the deadline

- Maintain IFRS-compliant bookkeeping for 12 months at the UAE entity level

- Reconcile intercompany transactions with the Singapore parent

- Confirm VAT filing status and registration threshold

- Gather all required documentation including bank statements, invoices, contracts, and corporate registration documents

Remote Audit Option

Singapore companies do not need to send representatives to the UAE for the audit. All documents can be shared securely via cloud platforms. However:

- Auditors will still require original or certified copies of certain documents

- Singapore companies should have a local UAE contact (company secretary or PRO) to liaise with the auditor and free zone authority

Working with a Cross-Border Advisory Firm

Managing Singapore-side obligations (ACRA, IRAS) alongside a UAE free zone audit at the same time creates real coordination demands. A cross-border advisory firm handles both sides under one roof.

VJM Global supports Singapore companies through this dual compliance process, including:

- Coordinating with UAE-registered auditors on document requirements and timelines

- Reconciling intercompany accounts between the Singapore parent and UAE entity

- Ensuring UAE audit outputs align with Singapore parent company financial reporting

As a member of EAI International — a network of independent accounting firms operating across 50+ countries — VJM Global is positioned to manage multi-jurisdictional requirements without the back-and-forth of working with separate local firms.

Frequently Asked Questions

Is audit mandatory for a UAE free zone company fully owned by a Singapore company?

Yes, audit is mandatory for virtually all UAE free zone entities regardless of where the shareholder is incorporated. Ownership by a Singapore entity creates no exemption, and most free zones require annual audited financial statements for license renewal.

Can a Singapore company use its SFRS-compliant accounts for a UAE free zone audit?

No. UAE free zone audits must comply with IFRS, not SFRS. While SFRS largely aligns with IFRS, Singapore companies must appoint a UAE-registered auditor to prepare and certify IFRS-compliant financial statements for the UAE entity.

Which UAE free zones are most commonly chosen by Singapore companies, and how do their audit deadlines differ?

DMCC, IFZA, JAFZA, and RAKEZ are popular choices for Singapore businesses. Deadlines range from 90 days (JAFZA) to 180 days (DMCC, RAKEZ) after financial year-end. Deadlines do change, so verify the current requirement directly with your free zone authority before planning your audit timeline.

Does a UAE free zone subsidiary's audit need to be consolidated into the Singapore parent company's group accounts?

Yes. If the Singapore parent prepares consolidated group accounts under SFRS (IFRS-aligned), the UAE subsidiary's audited IFRS financials will need to be incorporated. Having a UAE audit completed on time directly supports the Singapore parent's group reporting timeline.

What happens if a Singapore company misses the UAE free zone audit submission deadline?

Trade license renewal is blocked, penalties of AED 2,500–5,000 (or higher in financial free zones) apply, visas sponsored by the entity may be frozen, and banking relationships can be affected.

Can a Singapore company complete a UAE free zone audit entirely remotely?

Yes. Audits can be fully facilitated remotely, with documents shared via secure cloud platforms. The UAE-registered auditor handles all free zone submissions on your behalf.