Introduction

Singapore businesses expanding into the UAE step into a jurisdiction that shares IFRS-aligned accounting standards with Singapore—but layers on a distinct set of obligations that catch many finance teams off guard. Both jurisdictions use IFRS-aligned accounting standards, but the UAE layers on distinct compliance obligations—corporate tax at 9%, VAT at 5%, mandatory audit requirements, and strict record-retention rules—that differ significantly from Singapore's IRAS and ACRA frameworks.

The structural choice between mainland and free zone entities matters more than most businesses expect. The Qualifying Free Zone Person (QFZP) regime can reduce corporate tax to 0%, but qualifying requires meeting specific substance and revenue conditions. Get it wrong, and the standard 9% rate applies retroactively.

Singapore businesses also benefit from a UAE–Singapore Double Taxation Avoidance Agreement (DTAA) that caps withholding rates and eliminates double taxation. Even so, UAE tax and accounting processes must be built separately—they cannot simply be extensions of existing Singapore infrastructure.

This guide covers the UAE's IFRS framework, financial reporting and audit obligations, corporate tax and VAT rules, free zone versus mainland accounting differences, and how Singapore's SFRS aligns with UAE practice. The goal is to give Singapore CFOs and finance teams a clear starting point for UAE compliance—before costly mistakes are made.

Key Takeaways

- The UAE mandates IFRS under the Commercial Companies Law; SMEs with revenue up to AED 50 million may use IFRS for SMEs.

- Corporate tax of 9% applies to taxable income above AED 375,000; qualifying free zone entities may access a 0% rate.

- VAT at 5% requires mandatory registration if taxable supplies exceed AED 375,000 annually.

- Audit requirements vary by entity type, but most free zone companies and all QFZPs must maintain audited financials.

- The UAE–Singapore DTAA caps withholding rates on dividends (5%), interest (7%), and royalties (5%).

UAE Accounting Standards at a Glance: The IFRS Framework

The UAE's primary accounting standard is International Financial Reporting Standards (IFRS), mandated under Article 27 of Federal Decree-Law No. 32 of 2021 (Commercial Companies Law). This provision requires all companies to prepare annual accounts in accordance with IFRS to give a true and fair view of profits and losses—making IFRS the sole accounting framework in the UAE, with no separate national GAAP.

What IFRS means in practice:

- Accrual basis accounting is mandatory: revenues and expenses must be recognised when incurred, not when cash changes hands.

- Financial statements must include a balance sheet, income statement, cash flow statement, and statement of changes in equity.

- Full IFRS compliance is required for calculating taxable income under corporate tax regulations, making accounting standard compliance directly tied to tax obligations.

IFRS for SMEs Pathway

Under Ministerial Decision No. 114/2023, businesses with annual revenues up to AED 50 million may apply the simplified IFRS for SMEs framework. This pathway:

- Reduces disclosure requirements and compliance costs.

- Maintains the same accrual basis and core financial statement requirements.

- Is particularly relevant for Singapore SMEs entering the UAE market.

- Automatically reverts to full IFRS if revenue exceeds the AED 50 million threshold.

Businesses with revenue below AED 3 million can also use the cash basis of accounting, subject to Federal Tax Authority (FTA) approval.

Regulatory Bodies Overseeing Accounting in the UAE

Singapore businesses should be familiar with three main bodies — plus free zone authorities if operating within a designated zone.

| Body | Primary Role | Key Powers |

|---|---|---|

| Ministry of Finance (MOF) | Policy authority for corporate tax | Issues ministerial decisions (MD 114/2023, MD 84/2025); oversees Economic Substance Regulations |

| Federal Tax Authority (FTA) | Administers and enforces corporate tax and VAT | Issues accounting and transfer pricing guidance; approves cash basis applications; penalises non-compliance |

| Securities and Commodities Authority (SCA) | Regulates listed companies | Enforces financial reporting and disclosure for public joint stock companies |

| Free zone authorities (DMCC, JAFZA, DIFC, ADGM) | Zone-level compliance | DMCC requires IFRS-compliant audited financials within 90 days of year-end; JAFZA requires audited statements for all FZE, FZCO, and branch entities |

Financial Reporting and Compliance Requirements in the UAE

Bookkeeping and Record Retention Obligations

UAE businesses face dual record-retention requirements:

- Commercial Companies Law (Article 26): Minimum 5 years from end of fiscal year.

- Corporate Tax Law (Article 56): Minimum 7 years following end of Tax Period.

The 7-year tax requirement effectively overrides the 5-year commercial requirement, applying to both Taxable Persons and Exempt Persons. All records must be maintained in accordance with IFRS and local laws.

Fiscal Year Flexibility

Under Article 28 of the Commercial Companies Law, the first fiscal year can range from 6 to 18 months from the registration date. Key points for Singapore businesses:

- Subsequent fiscal years must be consecutive 12-month periods.

- Many UAE companies align with the calendar year (ending 31 December).

- Different group reporting periods are accommodated — confirm alignment with your Singapore parent entity early.

Annual Financial Statement Requirements

Companies must prepare at year-end:

- Balance sheet

- Income statement

- Cash flow statement

- Statement of changes in equity (full IFRS) or simplified disclosures (IFRS for SMEs)

Electronic records are expressly permitted under Article 26(3) of Federal Decree-Law No. 32/2021, provided they meet ministerial controls for storage and distribution.

Audit Requirements: Who Must Be Audited

Mainland entities:

- Limited Liability Companies (LLCs): Article 102 requires annual appointment of one or more independent auditors.

- Public and Private Joint Stock Companies: Articles 244 and 260 mandate annual audit.

- Other company types may voluntarily appoint auditors.

Free zone entities:

Ministerial Decision No. 84 of 2025, effective for financial years beginning on or after 1 January 2025, requires:

- Audited financial statements for Taxable Persons (not part of a Tax Group) with revenue exceeding AED 50 million.

- All Qualifying Free Zone Persons (QFZPs) must maintain audited financial statements regardless of revenue to preserve the 0% corporate tax rate.

- Tax Groups must prepare audited special-purpose financial statements regardless of revenue.

Free zone-specific rules:

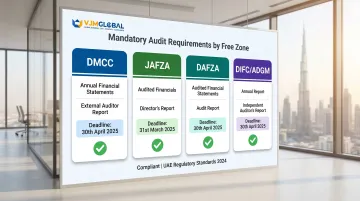

| Free Zone | Audit Requirement | Submission Deadline |

|---|---|---|

| DMCC | Mandatory for all entities (including dormant); IFRS required | 90 days from year-end |

| JAFZA | Mandatory for all FZE, FZCO, and branches; no exemptions by size | Required for licence renewal |

| DAFZA | Mandatory for all entities | Required for licence renewal |

| DIFC/ADGM | Mandatory per DFSA/FSRA regulations; IFRS required | Per regulatory category |

Practical implication for Singapore businesses:

A small UAE entity may still face mandatory audit requirements — either through free zone licensing rules or to qualify for the 0% QFZP corporate tax rate. Engaging a UAE-registered auditor before operations begin prevents compliance gaps that can affect both your licence and your tax position.

VJM Global supports foreign businesses in mapping cross-border audit and compliance obligations across multiple jurisdictions. Reach out to confirm your specific audit requirements before commencing UAE operations.

UAE Corporate Tax, VAT, and Other Key Tax Obligations

UAE Corporate Tax Framework

Introduced under Federal Decree-Law No. 47 of 2022, effective for fiscal years starting on or after 1 June 2023:

- Standard rate: 0% on taxable income up to AED 375,000; 9% on taxable income above AED 375,000.

- QFZP rate: 0% on Qualifying Income; 9% on non-qualifying income.

- Filing and payment deadline: Within 9 months from end of the relevant Tax Period (e.g., 30 September for 31 December year-end).

- Transfer pricing documentation must be submitted with the corporate tax return.

Qualifying Free Zone Person (QFZP) Regime

Free zone entities that meet seven mandatory conditions may benefit from a 0% corporate tax rate on qualifying income:

- Maintain adequate substance in a Free Zone (employees, assets, expenditure).

- Derive Qualifying Income (transactions with Free Zone Persons, qualifying activities, qualifying IP).

- Not have elected to be subject to standard CT rates.

- Comply with the arm's length principle.

- Maintain Transfer Pricing documentation.

- Maintain audited Financial Statements (regardless of revenue).

- Meet the de minimis requirement: non-qualifying revenue must not exceed the lower of 5% of total revenue or AED 5 million.

Failure results in loss of QFZP status from the beginning of that Tax Period plus a five-year lockout from re-qualifying. For Singapore businesses using a free zone structure, that lockout period alone makes ongoing compliance non-negotiable.

VAT Obligations

The UAE introduced VAT in January 2018 at a standard rate of 5%:

- Mandatory registration: If taxable UAE supplies and imports exceed AED 375,000 annually.

- Voluntary registration: Available above AED 187,500.

- Filing frequency: Quarterly for most taxpayers; monthly for businesses with annual turnover of AED 150 million or above.

- Filing due date: 28th day following end of VAT return period.

Designated Zones — a key exception for goods: Specific fenced geographic areas with customs controls are treated as outside the UAE for VAT purposes. Supplies of goods within a Designated Zone are outside the scope of UAE VAT unless consumed within the zone. Services, however, remain subject to standard VAT rules regardless of zone status.

UAE–Singapore Double Taxation Avoidance Agreement (DTAA)

Beyond VAT and corporate tax, the bilateral tax treaty between the two countries provides structural protection against double taxation. The UAE–Singapore DTAA, in force since 30 August 1996, caps withholding tax rates:

- Dividends: 5% of gross amount.

- Interest: 7% of gross amount (0% if paid to government/central bank).

- Royalties: 5% of gross amount.

Since the UAE currently does not levy withholding tax on outbound payments, the treaty's immediate value is as insurance against future UAE tax policy changes. The more practical benefit is Article 7's PE-based business profits allocation, which prevents double taxation where a Singapore parent operates through a UAE permanent establishment.

Free Zone vs. Mainland UAE: Accounting Implications for Singapore Businesses

Singapore businesses enter the UAE via a mainland LLC, a free zone company (FZ-LLC or branch), or an offshore entity. Each has different accounting, audit, and tax obligations.

Structural comparison:

| Structure | Accounting Standard | Annual Audit | QFZP Eligible | Key Consideration |

|---|---|---|---|---|

| Mainland LLC | IFRS (mandatory) | Mandatory (Art 102) | No | Full access to UAE domestic market; 100% foreign ownership permitted |

| Free Zone FZ-LLC/FZE | IFRS (mandatory) | Mandatory per free zone authority + MD 84/2025 if QFZP | Yes | Potential 0% CT on qualifying income; limited mainland trade |

| Branch of foreign company | IFRS for branch accounts | Required by most free zones; mainland branches by law | Possible if in free zone | Simplified setup; parent company liability; IFRS reconciliation needed |

| Offshore company | IFRS if generating UAE-source income | Typically not required unless tax-relevant | No | Limited to holding activities; no physical office requirement |

Key accounting differences:

- Mainland entities must meet FTA reporting requirements and commercial law audit obligations under Article 102.

- Free zone entities must satisfy both their respective free zone authority's rules — which vary by zone — and FTA regulations.

- Confirm your chosen free zone's bookkeeping deadlines and financial statement submission requirements before incorporation.

VAT treatment across structures:

VAT obligations follow a consistent rule regardless of structure. VAT at 5% applies to both mainland and standard free zone entities. The only exception is Designated Zones, where goods transactions fall outside UAE VAT scope — provided specific fencing and customs controls are in place.

Key Differences Between Singapore and UAE Accounting Standards

Framework Comparison

Singapore: Uses Singapore Financial Reporting Standards (International) - SFRS(I) - which are word-for-word equivalent to IFRS Standards as stated by ACRA. SFRS for Small Entities (SFRS for SE) is available for smaller, non-publicly accountable entities.

UAE: Mandates IFRS and IFRS for SMEs directly (not a local adaptation). In practice, Singapore businesses familiar with SFRS(I) will find UAE IFRS broadly compatible, but should note UAE-specific regulatory overlays:

- Mandatory accrual basis under corporate tax law (with narrow AED 3 million cash basis exception).

- AAOIFI Shari'ah standards formally adopted by the Central Bank for Islamic financial institutions.

Tax Reporting Differences

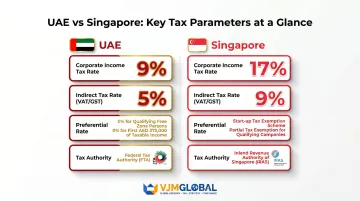

| Parameter | UAE | Singapore |

|---|---|---|

| Corporate income tax rate | 9% (on income above AED 375,000) | 17% (flat rate) |

| Indirect tax (VAT/GST) | 5% VAT | 9% GST (from 1 January 2024) |

| QFZP preferential rate | 0% on qualifying income | N/A |

| Tax authority | Federal Tax Authority (FTA) | Inland Revenue Authority of Singapore (IRAS) |

Singapore businesses are accustomed to IRAS reporting under the Income Tax Act. In the UAE, the FTA administers both corporate tax and VAT — and compliance cycles, formats, and penalties differ significantly. Build UAE-specific compliance processes from the ground up rather than adapting your existing Singapore setup.

AML and Economic Substance Obligations

The UAE has robust Anti-Money Laundering (AML) laws administered by the Central Bank and Economic Substance Regulations (ESR) that apply to businesses in certain sectors (banking, insurance, IP holding, etc.). Singapore businesses in these sectors must be aware of ESR filing obligations:

- ESR Notification: Due within 6 months of fiscal year-end.

- Economic Substance Report: Due within 12 months of fiscal year-end.

Non-compliance triggers escalating penalties — starting at AED 20,000 for missed notifications and rising to AED 400,000 for repeat failures. Singapore has no equivalent regime, so businesses expanding to the UAE should factor ESR into their compliance calendar from day one.

Frequently Asked Questions

What accounting standard is used in the UAE?

The UAE mandates International Financial Reporting Standards (IFRS) under Article 27 of Federal Decree-Law No. 32 of 2021. IFRS for SMEs is permitted for businesses with annual revenue up to AED 50 million per Ministerial Decision No. 114/2023.

Which is better: IFRS or GAAP?

The UAE does not use GAAP—IFRS is the applicable standard. Both aim for financial transparency, but IFRS is principles-based and internationally recognised, making it the standard of choice for international financial centres like the UAE. Singapore's SFRS(I) is also IFRS-aligned, so the transition for Singapore businesses is relatively smooth.

Is a US CPA recognised in the UAE?

The UAE has no single national CPA licence requirement — auditors must register with the relevant emirate authority or free zone regulator. International qualifications such as ACCA, ICAEW, and CPA Australia are widely accepted, though engaging a UAE-licensed auditor is often required in practice.

What are basic accounting rules in the UAE?

Businesses must follow IFRS (or IFRS for SMEs where eligible), use accrual-basis accounting, and prepare annual financial statements. Records must be retained for 7 years under the Corporate Tax Law, and FTA reporting requirements apply for both VAT and corporate tax.

Does the UAE have a tax treaty with Singapore?

Yes, the UAE and Singapore have a Double Taxation Avoidance Agreement (DTAA) in force, which caps withholding taxes on dividends (5%), interest (7%), and royalties (5%) between the two countries, helping Singapore businesses avoid being taxed twice on the same income.

Do Singapore companies need a local accountant in the UAE?

There is no statutory requirement for a UAE-based accountant across all functions, but audit rules require a UAE-registered independent auditor. Local accounting expertise is strongly recommended for FTA filings, free zone compliance, and corporate tax obligations.