Introduction

When UK companies establish operations in India — whether as a wholly-owned subsidiary, branch office, or liaison office — they become subject to Indian corporate law, including mandatory filings with the Registrar of Companies (ROC) under the Companies Act, 2013. This regulatory framework operates entirely independently of UK Companies House requirements.

Many UK business owners familiar with annual Confirmation Statements and accounts filings at Companies House are caught off guard by India's ROC system. The forms are different, deadlines are tighter, and governance procedures follow Indian corporate law — not UK norms.

The stakes for missing deadlines are also steeper. The Indian financial year runs April to March, the AGM must typically be held by September 30, and late filing attracts daily penalties of ₹100 per form. Left unaddressed, those penalties escalate into director disqualification and company strike-off.

This guide covers what ROC filing involves, which forms apply to UK-owned Indian entities, key deadlines, and the compliance traps most likely to catch UK companies off guard.

Key Takeaways

- ROC filing is mandatory for all Indian entities — including subsidiaries and branches owned by UK companies

- Two core forms: AOC-4 (financial statements, due 30 days post-AGM) and MGT-7/MGT-7A (annual return, due 60 days post-AGM)

- India's financial year runs April–March; AGMs must be held by September 30, making October–November the key filing window

- UK directors need a Class 3 Digital Signature Certificate (DSC) to file electronically on the MCA portal

- Penalties start at ₹100/day per form; three consecutive years of non-filing triggers a five-year director disqualification

What Is ROC Filing and Why Does It Apply to UK Companies?

The ROC System Under Indian Law

The Registrar of Companies (ROC) is the government body under the Ministry of Corporate Affairs (MCA) responsible for registering and regulating all companies incorporated in India under the Companies Act, 2013. This includes not just domestic companies, but every Indian entity formed by foreign investors.

When a UK company enters India — as a Private Limited subsidiary, joint venture, branch office, or liaison office — the Indian entity must comply with ROC filing obligations. UK Companies House filings satisfy UK law; ROC filings satisfy Indian law. The two systems do not cross-recognise each other's submissions.

Why UK Companies Must File Separately

According to Section 92 and Section 137 of the Companies Act, 2013, every company incorporated in India must file an annual return and financial statements with the ROC, regardless of foreign ownership. Deadlines are fixed: 60 days from the AGM for the annual return, and 30 days from the AGM for financial statements.

ROC filing serves three purposes:

- Maintains the Indian entity's registration and legal standing

- Gives Indian regulators, investors, and creditors financial visibility into the company

- Enables government monitoring of foreign-owned corporate activity under FDI policy

Consequences Beyond Financial Penalties

Missing ROC deadlines carries consequences that go well beyond fines:

- Disqualification of directors — including UK-based directors named on the Indian company's board

- Blocked profit repatriation and dividend distributions

- Adverse impact on future FDI approvals or regulatory clearances

- Company strike-off from the register, ending the entity's legal existence

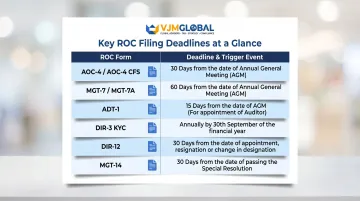

Key ROC Forms and Deadlines UK Companies Must Know

ROC filings fall into two categories: annual recurring filings (tied to the financial year and AGM) and event-based filings (triggered by specific corporate actions). UK companies must manage both.

Annual Forms — Core Compliance

Form AOC-4: Financial Statements

Files the audited balance sheet, profit & loss account, and cash flow statement — due within 30 days of the AGM. Companies with subsidiaries or associates must also file Form AOC-4 CFS for consolidated financial statements.

Form MGT-7 / MGT-7A: Annual Return

Covers shareholding pattern, director details, registered office, and company activity summary — due within 60 days of the AGM.

- MGT-7A applies to One Person Companies and small companies (paid-up capital up to ₹4 crore, turnover up to ₹40 crore)

- MGT-7 applies to all others, including UK-owned subsidiaries

The AGM Deadline and Filing Window

Under Section 96 of the Companies Act, companies must hold their AGM within six months of the financial year end. For the standard April–March year, this means by September 30.

Typical filing window:

- AGM deadline: September 30

- AOC-4 deadline: approximately October 29 (30 days after AGM)

- MGT-7 deadline: approximately November 28 (60 days after AGM)

FY 2024-25 Extension: MCA extended deadlines to January 31, 2026 due to the V3 portal transition. This was a one-time relief measure — plan for standard deadlines in future years.

Event-Based Forms UK Companies Frequently Encounter

These forms activate when a specific corporate event occurs — not on a fixed annual schedule. Missing these deadlines is a common compliance gap for UK-owned subsidiaries.

| Form | Trigger Event | Deadline | Key Note |

|---|---|---|---|

| ADT-1 | Auditor appointment/reappointment | 15 days from AGM | Filed at each AGM |

| DIR-3 KYC | Annual/triennial KYC for DIN holders | June 30 (triennial from April 1, 2026) | Applies to UK-based directors; see Amendment Rules, 2025 |

| DIR-12 | Director appointment, resignation, or designation change | 30 days from event | Required for any board-level change |

| MGT-14 | Board/shareholder resolutions, including financial statement approval | 30 days from resolution | UK-owned private subsidiaries of public companies are not exempt |

Quick Reference Summary

| Form | Purpose | Deadline |

|---|---|---|

| AOC-4 / AOC-4 CFS | Financial statements | 30 days from AGM |

| MGT-7 / MGT-7A | Annual return | 60 days from AGM |

| ADT-1 | Auditor appointment | 15 days from AGM |

| DIR-3 KYC | Director KYC | June 30 (triennial from April 2026) |

| DIR-12 | Director appointment/resignation | 30 days from event |

| MGT-14 | Board/member resolutions | 30 days from resolution |

Step-by-Step ROC Filing Process for UK Companies

ROC filing follows a coordinated sequence that begins weeks before submission. Each step below maps the process so UK decision-makers and India-based teams can stay aligned throughout.

Step 1: Conduct the First Board Meeting

The board of directors (which may include UK-based directors) convenes to authorise the statutory auditor to prepare financial statements per Schedule III of the Companies Act, 2013, and to prepare the Board's Report and Annual Return.

Step 2: Conduct the Second Board Meeting for Approval

A subsequent board meeting reviews and formally approves the draft financial statements, Board's Report, and Annual Return before they are placed before shareholders at the AGM.

Step 3: Hold the Annual General Meeting (AGM)

Shareholders approve the financial statements at the AGM. Only after shareholder approval do the financial statements become final and legally ready for ROC submission. UK parent companies holding majority shares typically pass these resolutions.

Step 4: Prepare and Upload Forms on the MCA Portal

Once the AGM concludes, the company downloads prescribed e-forms — AOC-4, MGT-7, ADT-1, and others — from the MCA V3 portal, completes them, and uploads them to the portal. UK-based directors must hold a valid Class 3 Digital Signature Certificate (DSC) to sign these forms, so arranging this ahead of time is essential.

Step 5: Payment, SRN Generation, and Tracking

After upload, the portal generates a Service Request Number (SRN) used to track the filing. Fees are paid online and calculated based on authorised share capital under the Companies (Registration Offices and Fees) Rules, 2014. Use the SRN to monitor whether your filing is approved, pending, or queried.

Special Considerations for UK Companies Managing ROC Compliance

Digital Signature Certificate (DSC) for UK Directors

Any UK-based director named on the Indian company's board must obtain a Class 3 DSC from a licensed Certifying Authority in India. This requires coordination with a local professional and submission of identity documents (passport, address proof, email, mobile, and video verification). Without a valid DSC, the director cannot sign or file forms — a common bottleneck for UK companies.

Licensed CAs include eMudhra, Sify Safescrypt, (n)Code Solutions, and Capricorn Identity Services. The full list is maintained at CCA's official website.

The Role of a Company Secretary or Authorised Representative

UK companies with a Private Limited subsidiary in India meeting certain thresholds must appoint a full-time Company Secretary. Others engage a practising Company Secretary (PCS) to manage and certify ROC filings.

This local professional coordinates all compliance activities between UK owners and the Indian regulatory system. VJM Global's Company Law team handles annual filings, director disclosures, statutory register updates, and all MCA portal interactions on behalf of UK-based directors.

FEMA and RBI Reporting Overlap

ROC filings for UK-owned Indian companies often coincide with Foreign Exchange Management Act (FEMA) obligations:

- Form FC-GPR: Reports FDI received; due within 30 days of share allotment via the RBI FIRMS portal

- FLA Return: Annual return on foreign liabilities and assets; due 15 July via the RBI FLAIR portal

Missing FEMA filings attracts separate penalties (up to three times the sum involved) even if ROC filings are timely. UK companies need to coordinate both compliance calendars — VJM Global manages ROC and FEMA filings together, so no deadline falls through the gap between two separate regulatory systems.

Common Mistakes and Penalties UK Companies Should Avoid

The Cascading Deadline Risk

The AGM is the trigger for most ROC deadlines. UK companies that delay approving financial statements — often due to time zone coordination or slower international audit processes — can inadvertently push the AGM past September 30.

Missing that date attracts its own penalty and simultaneously causes all downstream ROC filing deadlines to breach.

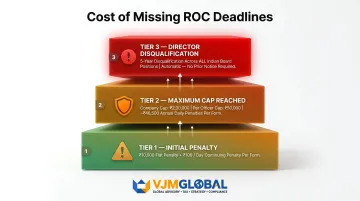

Penalty Structure

Late filing of Form AOC-4 and Form MGT-7 each attract:

- Initial penalty: ₹10,000

- Continuing penalty: ₹100 per day of delay

- Maximum cap: ₹2,00,000 for the company; ₹50,000 per officer in default

Even with caps, a full year of delay accumulates approximately ₹46,500 in daily penalties per form. Additional filing fees under Section 403 apply separately.

Beyond monetary penalties, persistent non-filing (typically over two consecutive financial years) triggers director disqualification under Section 164(2). This is a five-year disqualification affecting all Indian companies on whose board that director sits, not just the defaulting entity. Disqualification is automatic and requires no prior notice.

Strike-Off and Reputational Risk

The ROC has authority under Section 248 to strike off a company's name from the register for sustained non-compliance. For UK companies that have invested in Indian market entry, this is a costly outcome that compliance discipline can prevent entirely.

Reactivation is possible through the National Company Law Tribunal under Section 252(3). However, it involves formal legal proceedings and must be pursued within 20 years of the strike-off notice.

Frequently Asked Questions

What is ROC filing in India?

ROC filing is the mandatory submission of annual financial statements, annual returns, and other regulatory documents by companies registered in India to the Registrar of Companies under the Ministry of Corporate Affairs, as required by the Companies Act, 2013.

Is ROC filing mandatory every year?

Yes, ROC filing is mandatory every financial year for all registered Indian companies — including subsidiaries and branch offices of UK companies. Failure to file annually results in penalties, director disqualification, and eventual strike-off of the company.

What is the last date for ROC filing for FY 2024-25?

For FY 2024-25, the MCA extended deadlines to 31 January 2026 due to the V3 portal transition. Under normal conditions, AOC-4 falls due approximately 29 October and MGT-7 approximately 28 November, following the 30 September AGM deadline. Always verify current dates on the MCA portal directly.

Who is responsible for filing ROC?

The directors of the Indian company are legally accountable for ensuring timely and accurate filings. In practice, filings are carried out by a Company Secretary or practising professional, but directors — including UK-based directors — remain personally liable for non-compliance.

What happens if a UK company misses the ROC filing deadline in India?

Missing the deadline triggers a daily late fee of ₹100 per delayed form, potential disqualification of directors from serving on any Indian company's board, and risk of the company being struck off the register — disrupting business operations and complicating future investment or profit repatriation.

Does a UK company need to file separately in both India and the UK?

Yes. A UK company with an Indian subsidiary must fulfil filing obligations in both jurisdictions independently — annual ROC filings with the MCA in India for the Indian entity, and separate Confirmation Statements and Annual Accounts with Companies House for the UK parent. Neither system accepts the other's filings as a substitute.

ROC compliance is manageable with the right partner on the ground. With over 30 years of experience and a dedicated team supporting 250+ UK businesses, VJM Global handles the full ROC filing cycle — from DSC procurement and board meeting coordination to MCA portal submissions and FEMA reporting. Our experts ensure you never miss a deadline, avoid penalties, and maintain full compliance across both the UK and Indian regulatory calendars. Contact us at info@vjmglobal.com or call +91 9213397070 to learn how we can support your Indian operations.