That reaction is common, but the audit process is far less adversarial than most business owners assume. At its core, an audit is a tool for transparency, financial accuracy, and business credibility. Whether you are running a UK company, a US business with an Indian subsidiary, or a multinational operating across multiple jurisdictions, understanding what an audit actually involves — and why it matters — is essential knowledge for any director or finance lead.

This guide breaks down what an audit is, the main types, who needs one, and how the process works from start to finish.

Key Takeaways

- An audit is an independent examination of financial statements to provide reasonable assurance they present a true and fair view.

- Four main audit types exist: financial (statutory), compliance, operational, and internal — each serving a distinct purpose.

- In the UK, companies meeting two of three size thresholds require a statutory audit from financial years beginning on or after 6 April 2025.

- In India, every registered company must appoint an auditor under the Companies Act 2013 — regardless of size.

- Audited financials carry more weight with lenders and investors than unaudited ones.

- Independent review surfaces internal control gaps before they become serious problems.

What Is an Audit?

An audit is a professional, independent examination of a company's financial records and statements. The objective, as set out under SA 200 (Standards on Auditing issued by ICAI) and equivalent international standards (ISA 200), is for the auditor to obtain reasonable assurance — a high level of confidence, not an absolute guarantee — that the financial statements are free from material misstatement and present a true and fair view. That distinction matters: an audit is not a forensic investigation of every transaction, and it does not certify that a company is fraud-free.

What "Materiality" Actually Means

Auditors do not chase every minor discrepancy. Under SA 320 (and ISA 320 internationally), a misstatement is material if it could reasonably be expected to influence the economic decisions of users relying on those financial statements.

Two key points follow from this:

- A misstatement can be material by nature (for example, evidence of fraud) even if the monetary value is small

- Auditors concentrate effort on areas where material misstatement is most likely — this is the risk-based approach

Who Conducts an Audit?

The auditor must be independent — meaning no financial, personal, or professional connection to the company being examined. In India, auditors are Chartered Accountants (CAs) registered with the Institute of Chartered Accountants of India (ICAI), which governs eligibility, conduct, and disciplinary standards. Foreign companies operating in India — including those from the UK, USA, and Australia — are subject to audit requirements under the Companies Act, 2013, and must engage an ICAI-registered auditor for statutory purposes.

Three Foundational Principles

Every audit, regardless of type, rests on:

- Independence — the auditor must be, and must be perceived as, free from bias

- Professional scepticism — a questioning mindset that evaluates evidence critically rather than accepting management explanations at face value

- Risk-based approach — audit effort is directed toward areas with the highest likelihood of material misstatement

External vs. Internal Audit

These are distinct functions and should not be confused:

- External audit: Conducted by an independent third party, providing an opinion to shareholders and external stakeholders

- Internal audit: Conducted by the company's own team or an outsourced function, providing assurance to management on controls, risk, and governance — not for external publication

What Are the Main Types of Audits?

Financial (Statutory) Audit

The most common type. An independent firm examines a company's annual accounts to confirm they have been properly prepared, comply with applicable accounting standards (UK GAAP, IFRS, or India's Ind AS), and present a fair view of financial position. This is the type legally required for companies above certain size thresholds.

Compliance Audit

Reviews whether a business adheres to specific regulatory requirements, laws, or internal policies. Examples include tax compliance reviews, GST audits in India, and sector-specific regulatory audits in financial services or insurance. As noted in ACCA guidance, auditors consider whether client non-compliance with laws and regulations could affect the financial statements.

Operational Audit

Evaluates internal processes, procedures, and efficiency — not just financial accuracy. The goal is to identify redundancies, inefficiencies, or control weaknesses and recommend practical improvements. This type is particularly useful for companies scaling rapidly or operating in new markets.

Internal Audit

The IIA defines internal auditing as "an independent, objective assurance and consulting activity designed to add value and improve an organisation's operations", using a systematic approach to evaluate risk management, control, and governance.

In larger organisations, internal audit operates as a dedicated function — either in-house or outsourced. VJM Global's outsourced internal audit service covers:

- Risk management frameworks and controls assessment

- Asset safeguarding and compliance review

- Organisational efficiency analysis

This helps companies surface weaknesses before external auditors do.

Forensic Audit

A specialised investigation triggered by suspected fraud, financial crime, or disputes. According to ACCA, forensic auditing involves specific procedures to identify and gather evidence relevant to fraud or court proceedings. Unlike a statutory audit, findings are often prepared to meet the evidential standards required in legal proceedings.

Why Is an Audit Important for Your Business?

Stakeholder Trust and Access to Finance

Audited financial statements signal transparency to investors, lenders, and business partners. Research by Minnis (2011) found that audited private firms have a significantly lower cost of debt, with lenders placing greater weight on audited financial information when setting interest rates. A World Bank study on SMEs reached a similar conclusion: better-quality financial statements correlate with lower borrowing costs.

For companies seeking funding, entering new markets, or bidding on contracts, clean audited accounts are often a prerequisite.

Fraud Detection and Risk Management

Audits are not the primary fraud-detection mechanism — the ACFE's 2024 Report to the Nations found that tips (43%), internal audit (14%), and management review (13%) detect far more occupational fraud cases than external audit (3%). But that does not diminish the value of independent scrutiny.

An external auditor brings a fresh perspective. They can identify patterns, control gaps, and account anomalies that familiarity and routine can blind an internal team to. Catching a control weakness early, before it becomes a regulatory issue or a financial loss, is where audits pay for themselves.

Business Insights Beyond Compliance

A well-executed audit surfaces more than financial accuracy. It reveals:

- Operational inefficiencies and process gaps

- Weaknesses in internal control systems

- Areas of financial vulnerability or regulatory risk

- Recommendations for improving how the business manages its data and reporting

For international companies operating in India, this dimension is particularly valuable. VJM Global's statutory audit process includes a dedicated step for identifying compliance and operational gaps, with clear recommendations for correction, going beyond a simple pass/fail verdict on the accounts.

Legal and Regulatory Consequences of Non-Compliance

For companies legally required to be audited, non-compliance carries real consequences. Directors are personally responsible for ensuring audit obligations are met.

Under India's Companies Act 2013, failure to comply with statutory audit requirements can attract significant penalties for both the company and its officers. For foreign companies operating in India, this includes consequences that extend to the Indian subsidiary's directors. Similarly, under UK company law, failure to file acceptable accounts is a criminal offence — carrying a criminal record and potentially unlimited fines for directors, separate from late filing penalties of up to £1,500 (private companies) or £7,500 (public companies) when accounts are more than six months overdue, doubling on successive failures.

Who Needs an Audit?

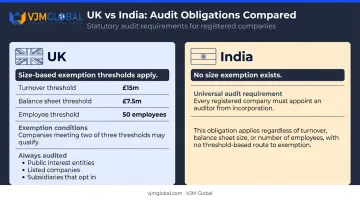

UK Thresholds (From 6 April 2025)

Under the GOV.UK audit exemption guidance, a company qualifies for the small-company audit exemption if it meets at least two of three criteria:

| Criterion | Threshold |

|---|---|

| Annual turnover | Not more than £15 million |

| Balance sheet total | Not more than £7.5 million |

| Employees | 50 or fewer |

Companies exceeding two or more of these limits are generally required to have a statutory audit.

Certain categories always require an audit, regardless of size:

- Public companies (unless dormant)

- Authorised insurance companies

- Banking companies

- E-money issuers and MiFID investment firms

- UCITS management companies

- Scheme funders of master trust pension schemes

UK Exemptions Worth Knowing

Even eligible companies may lose their exemption:

- Shareholders holding at least 10% of issued share capital can demand an audit by written request to the registered office — delivered at least one month before the financial year end

- Subsidiary exemption (s479A): Available where subsidiaries meet certain conditions, including inclusion in parent consolidated accounts and a parent guarantee

- Dormant company exemption (s480): Available if the company has been dormant since formation or since the end of the previous financial year

India: No Size Exemption

Unlike the UK's size-based thresholds, India has no audit exemption for small companies. Under the Companies Act 2013, every registered company must appoint an auditor at its first AGM under s139 — and only a Chartered Accountant in practice, or a qualifying firm, can fill that role.

For foreign companies setting up Indian subsidiaries, this frequently surprises first-time entrants. The obligation begins at incorporation, not once revenue scales. VJM Global's ICAI-qualified Chartered Accountants work with international businesses from day one to ensure auditor appointment and first-year compliance are in place before they become urgent.

How Does the Audit Process Work?

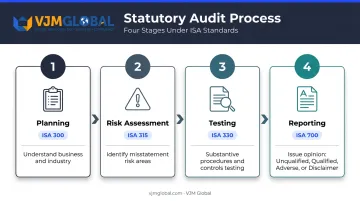

A statutory audit follows a defined sequence governed by International Standards on Auditing (ISAs):

Stage 1: Planning (ISA 300)

The auditor gains an understanding of the business, its industry, and the external factors that may have affected the reporting period. This includes reviewing accounting policies and identifying significant transactions.

Stage 2: Risk Assessment (ISA 315)

The auditor identifies where material misstatements are most likely to occur — by transaction type, business area, or account balance. This shapes where audit effort is concentrated.

Stage 3: Testing (ISA 330)

Substantive procedures and tests of controls are performed: examining financial records, verifying transactions against supporting documents, and assessing whether internal controls operated effectively. Businesses should expect requests for invoices, bank statements, contracts, and board resolutions during this phase.

Stage 4: Reporting (ISA 700)

The auditor issues an audit report with an opinion. There are four possible outcomes:

| Opinion Type | What It Means |

|---|---|

| Unqualified (clean) | Financial statements present a true and fair view |

| Qualified | Material issues exist but are not pervasive — specific limitations or disagreements noted |

| Adverse | Financial statements are materially misstated in a pervasive way |

| Disclaimer | Auditor was unable to obtain sufficient evidence to form an opinion |

For most businesses with well-maintained records, an unqualified opinion is the expected outcome. A qualified or adverse opinion is a significant signal to investors and lenders and warrants immediate management attention.

Auditor Access Rights Throughout the Process

Regardless of which stage the audit is in, auditors have statutory access rights to company books, accounts, and vouchers. In India, this is governed by Section 143 of the Companies Act 2013; in the UK, by Section 499 of the Companies Act 2006. Officers can be required to provide information and explanations at any point.

Maintaining organised, accurate financial records throughout the year — rather than scrambling at year-end — makes the entire process faster and reduces the risk of an adverse finding.

Frequently Asked Questions

What is an audit in the UK?

In the UK, an audit is an independent examination of a company's annual accounts conducted under the Companies Act 2006. It is required for companies exceeding two of three size thresholds (turnover, assets, employee count) or falling into regulated categories such as public companies and financial services firms.

What are the 4 types of audit?

The four main types are:

- Financial (statutory) audit — confirms the accuracy of annual accounts

- Compliance audit — checks adherence to laws and regulations

- Operational audit — evaluates process efficiency

- Internal audit — reviews controls and risk management for management's use

What is the difference between an internal and external audit?

An external audit is conducted by an independent third party and provides an opinion to shareholders and external stakeholders. An internal audit is performed by the company's own team or an outsourced function, reviewing internal controls and processes for management's use only.

What happens if a company does not get an audit when legally required?

Failure to comply can result in financial penalties, late filing fees, and reputational damage. Directors are personally responsible for meeting audit obligations, and non-compliance is a criminal offence under UK company law.

Can a small business be exempt from an audit?

Many small UK companies qualify for an audit exemption by meeting at least two of the three size criteria. However, public companies and regulated businesses must be audited regardless of size. In India, no equivalent size-based exemption exists. Check your eligibility with a qualified adviser.