Introduction

Miss a filing deadline or misclassify an expense, and Singapore's regulators won't wait — ACRA can strike off non-compliant companies, while IRAS and grant bodies like EnterpriseSG have the authority to demand clawbacks on approved funding.

Singapore audit claims cover the process of preparing, submitting, and supporting financial claims reviewed by these regulatory bodies. Many businesses — especially foreign-owned entities and growing SMEs — run into problems because the rules around statutory audits, exemptions, and grant documentation aren't straightforward.

This guide is for private limited companies, SMEs, and foreign-owned entities operating in Singapore. Here's what you'll learn:

- How the audit claims process works end to end

- What documentation auditors actually require

- Who qualifies for small company audit exemptions

- The most common mistakes that trigger penalties or clawbacks

Key Takeaways

- Singapore companies undergo statutory audit annually unless they qualify as small, small group, or dormant under the Companies Act

- Every claimed dollar requires traceable documentation—invoices, bank records, payroll evidence, delivery proof

- Audit exemption applies when two of three thresholds are met: revenue ≤ S$10M, assets ≤ S$10M, ≤ 50 employees

- Non-compliance can trigger penalties up to S$5,000 per breach, court summons, or grant programme blacklisting

- Exempt companies still must maintain proper records and file unaudited financial statements

What Are Singapore Audit Claims?

Singapore audit claims refer to the documentation and financial evidence a company submits to satisfy audit requirements. These requirements fall into two broad categories: statutory audits and grant claim audits. Each serves a distinct purpose and involves different stakeholders, standards, and documentation.

Two Types of Audit Claims:

- Statutory audits confirm that a company's overall financial statements—balance sheet, income statement, cash flow statement, and statement of changes in equity—are accurate and compliant with SFRS or SFRS for Small Entities

- Grant claim audits verify that individual cost items claimed under government grants from agencies like EnterpriseSG, IMDA, or NEA are documented, incurred within scope, and qualify under approved categories

Both processes deliver independent assurance to stakeholders—shareholders, creditors, regulators, and grant administrators—that reported financials and claimed costs are accurate and compliant.

Three regulatory bodies govern how these audits are conducted and enforced in Singapore:

Regulatory Oversight:

- ACRA administers the Companies Act, enforces financial reporting obligations, and regulates public accountants through the Public Accountants Oversight Committee (PAOC)

- IRAS collects tax and requires companies to file corporate income tax returns supported by financial statements; IRAS doesn't directly mandate audits but relies on audited or certified financial statements for tax assessments

- Grant administrators (EnterpriseSG, IMDA, NEA) oversee government grants requiring grant claim audits, with EnterpriseSG requiring all Enterprise Development Grant (EDG) claims to be audited by pre-qualified panel auditors

Financial statements must comply with Singapore Financial Reporting Standards (SFRS), which are converged with International Financial Reporting Standards (IFRS). Statutory audits must follow Singapore Standards on Auditing (SSAs) issued by the Institute of Singapore Chartered Accountants (ISCA).

How the Singapore Audit Claims Process Works

The audit claims process follows a defined sequence: appoint a qualified auditor (or receive a Letter of Offer for grant claims), complete evidence gathering and fieldwork, then receive the audit opinion or disbursement decision. Understanding each stage helps you avoid delays and document rejections.

What Goes Into the Process:

- Audited financial statements (balance sheet, income statement, cash flow statement, statement of changes in equity)

- Supporting source documents—invoices, contracts, bank statements, payroll records, CPF contributions

- Reconciliations between accounting records and external evidence

- Declarations of compliance with applicable standards and grant terms

Preparing Your Documentation

The foundation of any clean audit claim is day-one documentation discipline. Every transaction must be traceable through:

- An invoice or payslip

- A bank payment record

- Evidence of delivery or service completion

- Alignment with approved scope

Payment Method Requirements:

| Payment Method | Acceptability | Documentation Required |

|---|---|---|

| Bank transfer / GIRO | Fully accepted | Bank statement showing payment |

| Corporate credit card | Fully accepted | Corporate card bank statement |

| Personal credit card | Conditionally accepted | Requires company reimbursement to create corporate audit trail |

| Cash | Discouraged | Requires explanation, proof of cash flow from bank, payment vouchers |

EnterpriseSG explicitly states: "Cash payment has limited audit trail and is not encouraged." Payments made via cash or personal credit cards without proper reimbursement are typically rejected during audit.

Once your documentation package is complete and payment trails are confirmed, you're ready to submit.

Submitting the Claim

For statutory audits: The auditor reviews records and issues an opinion under Singapore Standards on Auditing (SSAs). The audit verifies the company's overall financial position and compliance with SFRS.

For grant claims: Submissions are made through the GoBusiness Business Grants Portal with supporting documents and a compliance declaration. Claims above S$100,000 typically require an auditor's report, though this threshold should be confirmed in your specific Letter of Offer.

Responding to Audit Findings

When discrepancies are identified, auditors may:

- Reduce disbursements to the supportable amount

- Issue clawback notices for amounts already paid

- Escalate to a broader compliance review

Responding within the auditor's stated timeframe with targeted supplementary documentation (revised reconciliations, missing receipts, or reimbursement records) resolves most findings before they escalate. Foreign-owned entities managing compliance across multiple jurisdictions often benefit from working with advisors who understand both Singapore's grant frameworks and the reporting requirements of their home jurisdiction — VJM Global, for instance, supports cross-border businesses with internal controls review, audit preparation, and regulatory representation.

Singapore Audit Exemptions: Criteria and Qualifications

Small Company Exemption

A private company qualifies if it meets at least two of three thresholds for the past two consecutive financial years:

- Total annual revenue ≤ S$10 million

- Total assets ≤ S$10 million

- ≤ 50 full-time employees

This exemption applies only to private companies—public or listed entities are excluded. ACRA confirms these criteria were last updated on 3 February 2026.

Small Group Exemption

If a company is part of a group, both conditions must be satisfied simultaneously:

- The individual company must qualify as a small company

- The entire group must meet the same two-of-three thresholds on a consolidated basis

This dual requirement is defined in Section 205C(3)-(4) of the Companies Act. Foreign-owned subsidiaries that are part of non-qualifying groups cannot claim exemption even if they individually meet the thresholds.

Dormant Company Exemption

A company qualifies if it has had no accounting transactions since incorporation or since the end of the previous financial year, and total assets do not exceed S$500,000. "No transactions" means no business activity whatsoever.

Dormant companies meeting the asset cap may be exempt from preparing financial statements under Section 201A and from audit under Section 205B.

What Audit-Exempt Companies Must Still Do

Exemption does not mean zero reporting obligations. Exempt companies must:

- Prepare unaudited financial statements (UFS) — including profit and loss account, balance sheet, cash flow statement, and director's statement

- Maintain proper accounting records per Section 199

- Hold AGM if required under the Act

- File annual returns with ACRA

Section 205D grants ACRA the power to require even exempt companies to lodge audited financial statements if there is a breach of the Act or if it is in the public interest.

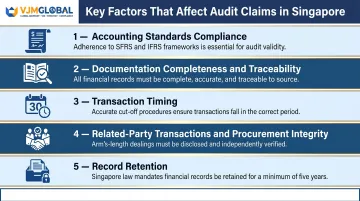

Key Factors That Affect Audit Claims in Singapore

Accounting standards compliance: Financial statements must adhere to SFRS or SFRS for Small Entities. Deviation from accrual-basis reporting or improper recognition of revenues and assets is the most common trigger for adverse audit opinions.

Documentation completeness and traceability: Every claimed cost must trace back to source documents — invoices, contracts, payslips, CPF records, and bank statements. Even minor gaps can trigger proportional disallowances across the entire claim.

Transaction timing: For grant claims, costs incurred before the Letter of Offer date or after the project completion deadline are automatically ineligible. For statutory audits, misclassifying accruals or prepayments into the wrong financial year is a common material misstatement.

Related-party transactions and procurement integrity: Vendor engagements must be at arm's length. Related-party costs face heightened scrutiny and are often disallowed unless independently benchmarked. Competitive procurement is required for grant-funded vendor engagements — confirm the exact number of quotes required in your Letter of Offer.

Retention of records: Section 199(2) of the Companies Act and IRAS both require a minimum of five years from the end of the relevant financial year. Grant-funded projects often require seven years (confirm in your Letter of Offer) — post-disbursement audits can revisit already-approved claims.

Common Issues and Misconceptions About Singapore Audit Claims

Misconception: Audit Exemption Means No Financial Obligations

Many business owners assume that qualifying as a small company eliminates all compliance requirements. In practice, unaudited financial statements must still be prepared, records must be maintained, and annual returns must still be filed. ACRA retains the authority to appoint an auditor if a company breaches any record-keeping or AGM obligation.

The Over-Claim and Double-Claim Problem

Businesses combining government grants with tax deductions sometimes unknowingly claim the same expenditure twice. IRAS explicitly states that tax deductions and capital allowances are no longer given on expenditure funded by government capital grants approved on or after 1 January 2021. The grant-supported portion of a cost cannot also be claimed as a tax deduction or capital allowance.

When stacking multiple grants on a single project, each agency applies its own stacking rules. Overlapping claims can trigger composite clawbacks — repayment demands spanning multiple agencies — so verifying eligibility before filing is essential.

Misconception: A Clean Audit Opinion Means Full Disbursement

A statutory audit and a grant claim audit are separate processes with separate standards. For grant claims, auditors specifically test:

- Existence — whether the asset or expense is real

- Occurrence — whether the transaction actually took place

- Completeness — whether all relevant costs are captured

- Accuracy — whether amounts are correctly recorded

- Ownership — whether the claimant holds the rights to the expenditure

A company can pass its statutory audit and still have grant claims partially disallowed due to unqualified costs or missing documentation.

Frequently Asked Questions

What qualifies a Singapore company as a "small company" for audit exemption?

A company must be a private company and meet at least two of three criteria for two consecutive financial years: annual revenue ≤ S$10 million, total assets ≤ S$10 million, and ≤ 50 full-time employees.

What documents are required to support an audit claim in Singapore?

Supporting documentation typically includes:

- Invoices from qualified vendors

- Bank payment records

- Payroll and CPF evidence for salary claims

- Delivery proof or service completion records

- Alignment with the approved scope or financial reporting period

What are the penalties for failing to comply with audit requirements in Singapore?

Late annual return filings can attract penalties of up to S$600. Breaches of the Companies Act can result in fines up to S$5,000 per offence. Failure to file tax returns for two or more years may result in a penalty of twice the tax assessed plus a fine of up to S$5,000 upon court conviction.

Can a dormant company be exempt from statutory audit in Singapore?

Dormant companies with no accounting transactions and total assets not exceeding S$500,000 qualify for audit exemption under Section 205B, but must still maintain records and file annual returns with ACRA.

How long must audit-related documents be retained in Singapore?

Singapore companies must retain accounting records for at least five years from the end of the relevant financial year under the Companies Act and IRAS requirements. Grant-funded projects may require up to seven years — confirm the exact period in your Letter of Offer.

What is the difference between a statutory audit and a grant claim audit in Singapore?

A statutory audit verifies the accuracy and compliance of a company's overall financial statements under the Companies Act. A grant claim audit is narrower — it tests whether individual cost items were incurred within scope, properly documented, and eligible under the grant's approved categories.