April 2025 brought the most significant revision to UK company size thresholds since 2013, with SI 2024/1303 raising monetary limits by roughly 50%. ICAEW estimates across three category migrations total 133,000 companies and LLPs affected — a figure that signals this isn't a minor administrative tweak.

This article explains exactly what the thresholds are, how they changed, the rules for applying them correctly, when size simply doesn't matter (because other overrides apply), and the group complications that catch companies — particularly foreign-owned UK subsidiaries — off guard most often.

Key Takeaways

- A UK private limited company qualifies as small by meeting at least 2 of 3 criteria: turnover, balance sheet total, and employee headcount

- From 6 April 2025, small company thresholds rose to £15 million turnover and £7.5 million balance sheet total

- Companies must meet size criteria for two consecutive periods, with a transitional provision for the first qualifying year under the new thresholds

- Group membership can override individual small company status and require a statutory audit regardless of size

- Qualifying for exemption doesn't automatically mean you should drop the audit — lenders, investors, and re-entry risk all factor in

What Is a UK Statutory Audit Threshold?

A statutory audit is an independent examination of a company's financial statements by a registered auditor, required under Companies Act 2006, Section 475 unless an exemption applies. The auditor's role is to form an opinion on whether those statements give a true and fair view.

The statutory audit threshold is the legal size boundary that determines whether a company must obtain that audit. Below the threshold — and subject to certain other conditions — a company can claim exemption. Above it, the audit is mandatory.

The threshold is not a single number. It's a composite test across three measures:

- Annual turnover

- Balance sheet total

- Average number of employees

A company must fail at least two of the three criteria to lose small company status. This flexibility is frequently misunderstood — a high-turnover company with modest assets and few employees may still qualify as small.

These thresholds sit within the Companies Act 2006 and are updated periodically. The April 2025 revision raised the limits to reflect inflation since 2013, reducing compliance obligations for businesses that had grown in revenue without materially changing in scale.

Factors Beyond Size

Individual size is only the starting point. These factors independently affect whether an audit is required:

- The company's position within a group — the group's aggregate size may override individual exemptions

- Whether any group member is an ineligible entity (bank, insurer, or MiFID investment firm)

- Shareholder requests under Section 476

- Type of business activity — certain regulated entities always require audit regardless of size

- Articles of association or loan covenants that contractually require an audit independent of statutory rules

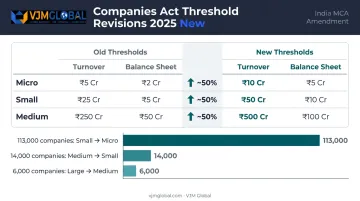

The Current UK Statutory Audit Thresholds: Old vs New (April 2025)

Two distinct regimes apply depending on when a company's financial year begins. Using the wrong set is a surprisingly common error.

Pre-April 2025 Thresholds (Financial Years Beginning 1 January 2016 to 5 April 2025)

Under the previous regime, a company qualified as small by meeting at least 2 of:

| Criterion | Threshold |

|---|---|

| Turnover | ≤ £10.2 million |

| Balance sheet total | ≤ £5.1 million |

| Average employees | ≤ 50 |

Post-April 2025 Thresholds (Financial Years Beginning on or After 6 April 2025)

ICAEW confirms the new limits effective from 6 April 2025:

Micro-entity

| Criterion | Old Threshold | New Threshold |

|---|---|---|

| Turnover | £632,000 | £1 million |

| Balance sheet | £316,000 | £500,000 |

| Employees | 10 | 10 |

Small

| Criterion | Old Threshold | New Threshold |

|---|---|---|

| Turnover | £10.2 million | £15 million |

| Balance sheet | £5.1 million | £7.5 million |

| Employees | 50 | 50 |

Medium

| Criterion | Old Threshold | New Threshold |

|---|---|---|

| Turnover | £36 million | £54 million |

| Balance sheet | £18 million | £27 million |

| Employees | 250 | 250 |

Note that employee headcount did not change at any tier. The 50-employee limit for small companies remains constant.

The scale of these migrations is significant. ICAEW estimates approximately 133,000 affected entities in total:

- 113,000 companies and LLPs moving from small to micro

- 14,000 moving from medium to small

- 6,000 moving from large to medium

The Transitional Provision

Normally, a company must meet the size criteria for two consecutive accounting periods before claiming exemption. SI 2024/1303 includes a specific shortcut: for the first financial year beginning on or after 6 April 2025, companies may treat the new thresholds as if they had also applied in the prior year. This bypasses the two-year rule for that first cycle, allowing immediate benefit from the higher limits.

How to Apply the Audit Threshold Correctly

Several technical rules determine whether a company genuinely qualifies for audit exemption. Errors in applying them are where compliance gaps most commonly arise.

The "2 of 3" Rule in Practice

A company must breach at least two of the three criteria to be classified as not-small. Exceeding only one metric does not disqualify it. For example:

- Turnover of £16 million, balance sheet of £6 million, and 30 employees → qualifies as small (only one criterion exceeded)

- Turnover of £16 million, balance sheet of £9 million, and 30 employees → does not qualify (two criteria exceeded)

The Two-Year Consecutive Rule

Status changes aren't immediate. The mechanism works like this:

- A company gains small status after meeting the criteria for two consecutive years

- A company retains small status for one year after failing to meet it, creating a one-year grace period

- Under the April 2025 transitional provision, the prior year can be treated as qualifying under the new thresholds for the first affected period

Turnover Pro-Rating

For accounting periods longer or shorter than 12 months, directors must proportionately adjust the turnover figure. A 15-month period's turnover is multiplied by 12/15 before comparison against the threshold.

For groups, both net (post-consolidation adjustments) and gross figures are available. Whichever method produces a more favourable result can be applied, or a combination used.

From 6 April 2025, the small group thresholds are £15 million net / £18 million gross for turnover and £7.5 million net / £9 million gross for balance sheet total.

The Balance Sheet Statement Requirement

Companies claiming audit exemption under Section 477 must include a specific statutory statement on the balance sheet confirming:

- The company is entitled to the Section 477 exemption

- Members have not required an audit under Section 476

- Directors acknowledge their responsibilities for the accounts

Omitting this statement invalidates the exemption claim. The accounts would technically require an audit regardless of whether the company meets the size criteria.

Given these layered rules, accurate assessment requires more than a single-year snapshot. VJM Global's audit and advisory team works with UK-based companies and foreign-owned subsidiaries on group-level testing, threshold monitoring across consecutive periods, and balance sheet statement compliance.

When a Small Company Still Cannot Claim Audit Exemption

Meeting the size thresholds is necessary but not sufficient. Several categories of companies cannot access audit exemption regardless of their size.

Mandatory Audit Categories

These company types always require a statutory audit:

- Public companies (unless dormant)

- Authorised insurance companies

- Banking companies

- E-money issuers

- MiFID investment firms

- UCITS management companies

- Companies with shares traded on a regulated market

- Funders of master trust pension schemes

For any company involved in regulated activities, check the exclusion list before running size calculations.

The Shareholder Override

Even a company that meets all size criteria can be required to have an audit. Under Section 476 of the Companies Act 2006, shareholders holding at least 10% of shares (by number or value) can demand a statutory audit by submitting a written request to the company's registered office no later than one month before the financial year-end. External investors, minority shareholders, and institutional backers all retain this right — independent of any decision made by directors.

Contractual Obligations

Statute is not the only source of audit obligations. A company can be contractually bound to audit even when the Companies Act permits exemption. Common sources include:

- Articles of association

- Loan covenants

- Investor or shareholder agreements

- Lender facility agreements

Review all of these documents before communicating any decision to stop auditing.

Group and Subsidiary Complications

Group structures create the most common — and costly — audit compliance errors, particularly for UK subsidiaries of international groups.

The Group-Level Size Test

A company within a group cannot simply look at its own numbers. It must assess the size of the worldwide group (aggregated). If the group as a whole exceeds the small thresholds on at least two of the three criteria, the individual UK subsidiary requires a statutory audit even if it is small on a standalone basis.

Under Section 383, the group test uses aggregate turnover, aggregate balance sheet total, and aggregate employee headcount across all group members. A UK subsidiary with £8 million turnover may still need an audit if its parent group turns over £500 million.

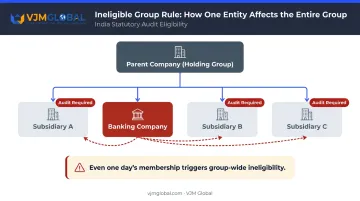

The Ineligible Group Rule

If any member of the group is one of the following entity types (including non-UK entities), the entire group is ineligible for small company audit exemption:

- Traded company

- E-money issuer

- Authorised insurer

- Banking company

- MiFID investment firm

- UCITS management company

All members lose access to small company audit exemption for any financial year in which they were part of that group. This applies even for a single day's membership.

In practice, a UK subsidiary can be entirely unregulated — yet lose its audit exemption simply because a sister entity in another jurisdiction holds a banking licence or e-money authorisation.

Section 479A: The Parental Guarantee Exemption

A UK subsidiary can claim audit exemption through a different route under Section 479A if:

- Its UK parent provides a statutory guarantee (Section 479C) over the subsidiary's liabilities

- The subsidiary is included in the parent's consolidated audited accounts

- Those consolidated accounts are filed on the UK public register

- All members of the subsidiary agree to the exemption

- The subsidiary's accounts disclose the arrangement

The critical limitation: this exemption is only available where the parent is established under UK law. Non-UK parents, including Indian, US, or EU-based parent companies, cannot use this route.

For international groups with UK operations, this is one of the most frequently misunderstood restrictions. Non-UK-parented subsidiaries must instead satisfy both standalone small company criteria and small worldwide group criteria — a bar that subsidiaries of large international groups typically cannot clear.

Voluntary Audits and Practical Considerations

Qualifying for audit exemption and deciding to stop auditing are two separate decisions. Many companies that legally qualify for exemption continue auditing voluntarily, and the reasons are often practical rather than ceremonial.

Common Reasons Companies Continue Auditing

- Lender requirements: Banks and other creditors routinely require audited accounts as a loan condition, regardless of legal exemption

- Investor expectations: PE-backed, VC-funded, or investor-held companies often face contractual or informal audit requirements

- Group parent requirements: Even where the UK subsidiary qualifies for exemption, the parent may require audited accounts for consolidation purposes

- M&A preparation: Companies considering sale or investment often maintain audit continuity to avoid due diligence complications

The Re-Entry Risk

If a company ceases auditing and later crosses back above the threshold, the absence of audited prior-year figures creates a specific problem. Auditors must obtain sufficient evidence that opening balances don't contain material misstatements.

Where inventory, fixed assets, leases, or revenue cut-off are material and unaudited, this can result in a qualified audit opinion that persists for up to three years. That is a significant reputational and compliance liability that many finance directors prefer to avoid altogether.

The FRS 102 Consideration

This re-entry risk becomes more acute given the upcoming FRS 102 changes. FRC amendments take effect for accounting periods beginning on or after 1 January 2026, introducing major changes to revenue recognition and lease accounting. Companies near audit thresholds face more complex reporting in these areas.

For companies with small finance teams or limited internal controls, maintaining a voluntary audit through the transition period provides an independent check on new accounting estimates and reduces the risk of material errors in the first FRS 102 year.

Frequently Asked Questions

What is the threshold limit for statutory audit?

From 6 April 2025, a company qualifies as small (and potentially audit-exempt) by meeting at least 2 of: turnover ≤ £15 million, balance sheet ≤ £7.5 million, or average employees ≤ 50. For financial years beginning between 1 January 2016 and 5 April 2025, the limits were £10.2 million turnover and £5.1 million balance sheet.

Who can carry out a statutory audit in the UK?

Only a registered auditor — an individual or firm regulated by a recognised supervisory body such as ICAEW, ACCA, or ICAS — can conduct a statutory audit. The auditor must be independent of the company and appointed in accordance with the Companies Act 2006.

Does the audit threshold apply to LLPs as well as limited companies?

Yes. SI 2024/1303 amends the LLP Regulations so the same April 2025 size threshold increases apply to Limited Liability Partnerships. The same size criteria, two-year rule, and exemption conditions apply to both LLPs and private limited companies.

Can shareholders force a company to get an audit even if it qualifies as small?

Yes. Under Section 476, shareholders holding 10% or more of shares (by number or value) can demand a statutory audit by delivering written notice to the company's registered address at least one month before the end of the relevant financial year.

What happens if a UK subsidiary's parent is based outside the UK?

Non-UK-parented subsidiaries cannot use the Section 479A parental guarantee exemption. They must meet both standalone small company criteria and small worldwide group criteria, which typically rules out audit exemption for subsidiaries of large international groups.

Does a company lose its audit exemption the moment it exceeds the threshold?

No. Under the two-year consecutive rule, a company retains its exemption for one year after first failing the size test, losing it only after failing for two consecutive years. The April 2025 transitional provision also allows the new thresholds to be treated as if they applied in the prior year for the first qualifying period.