Getting it wrong has real consequences. Choosing the wrong entity type, misunderstanding which sectors are restricted, or underestimating the document preparation timeline can result in months of delay, forced restructuring, or stranded capital.

This guide walks US business owners through the main legal structures available in China, the step-by-step registration process, post-incorporation compliance obligations, and the most common mistakes American companies make when entering the Chinese market.

Key Takeaways

- US companies can enter China through three primary structures: WFOE, Joint Venture, or Representative Office, each with different permitted activities and control levels

- WFOEs (Wholly Foreign-Owned Enterprises) are the most common choice for US companies that want full operational control

- China's 2024 Negative List (effective November 1, 2024) governs which sectors are open to 100% foreign ownership

- Registration spans two to four months across multiple agencies — document legalization is typically the slowest part

- Ongoing obligations cover annual audits, regular tax filings, and compliance with China's PIPL data protection rules

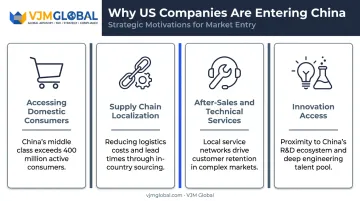

Why US Companies Are Setting Up in China

China's domestic consumer market remains one of the largest in the world. Total retail sales of consumer goods reached RMB 48.8 trillion in 2024, up 3.5% year over year — a scale that few other markets can match.

US companies pursue China operations for several distinct strategic reasons:

- Accessing domestic consumers — selling products or services directly to Chinese customers

- Supply chain localization — according to the 2024 USCBC member survey, 21% of respondents planned to localize regional supply chains in China specifically to reduce geopolitical and tariff exposure

- After-sales and technical services — supporting Chinese customers of products sold globally

- Innovation access — tapping into China's manufacturing ecosystem and domestic R&D base

These opportunities come with a compliance burden that US companies must plan for before entering — one that businesses from most other countries don't carry. FCPA anti-bribery obligations, OFAC sanctions screening, and US export control regulations (particularly relevant following BIS's December 2024 semiconductor equipment controls) all apply to American companies operating in China. Critically, these requirements follow the US parent entity regardless of where the Chinese operating entity is incorporated.

Business Structures Available to US Companies in China

Since the Foreign Investment Law took effect on January 1, 2020, the separate statutory forms for WFOEs, Equity Joint Ventures, and Cooperative Joint Ventures were replaced by a unified framework. Today, foreign-invested enterprises are organized under the Company Law, with ownership structure and governance terms negotiated within that framework.

Three practical arrangements remain relevant for US companies:

Wholly Foreign-Owned Enterprise (WFOE)

A WFOE is a Chinese Limited Liability Company with 100% foreign ownership. It is the most commonly chosen structure for US companies because it provides:

- Full management control without a Chinese partner

- Authority to issue RMB invoices and hire local staff directly

- Profit repatriation rights (subject to audit and tax compliance)

- Liability limited to registered capital

Three operating subtypes exist: trading WFOE, consulting/services WFOE, and manufacturing WFOE. The business scope approved on registration determines what the entity can legally do, so scoping this precisely at formation is essential to avoid costly amendments later.

Joint Venture (JV)

A JV involves partnering with a Chinese entity. Companies typically pursue a JV when:

- The target sector appears on China's Negative List and restricts foreign ownership percentages

- A local partner's distribution network, licenses, or regulatory relationships provide genuine strategic value

Key trade-offs include shared profits, reduced unilateral control, and IP transfer risk. Since the EJV and CJV statutes were repealed in 2020, new JVs are structured as Company Law entities with negotiated governance terms.

Representative Office (RO)

An RO is not a separate legal entity. Under China's RO regulations, it cannot conduct profit-making activities, cannot issue invoices, and cannot hire Chinese staff directly — personnel must be engaged through authorized service organizations.

Permitted activities are narrow: market research, liaison, promotion, and activities connected to the foreign parent's business. The parent company must have been in operation for more than two years to register an RO.

Structure selection in practice:

| Objective | Recommended Structure |

|---|---|

| Full operational presence, invoicing, hiring | WFOE |

| Sector requires Chinese partner or partial foreign ownership | Joint Venture |

| Market research or preliminary liaison only | Representative Office |

The Negative List is the critical filter — check it before selecting a structure.

Step-by-Step: How to Register a Company in China from the US

The registration process involves both US-side preparation and submission to Chinese authorities. The local Administration for Market Regulation (AMR) is the primary filing authority, but the State Taxation Administration (STA), State Administration of Foreign Exchange (SAFE), and customs authorities are also involved depending on the business type.

Step 1: Verify Sector Eligibility and Choose Your Structure

Cross-reference your intended business activity with the Special Administrative Measures for Foreign Investment Access, 2024 Edition (the current Negative List). This edition took effect November 1, 2024, contains 29 measures, and removed remaining manufacturing-sector access restrictions. Confirm whether your sector allows 100% foreign ownership before selecting a structure.

Step 2: Prepare and Legalize US-Side Documents

US-origin documents (including certificates of incorporation, shareholder identity documents, and board resolutions ) require notarization and apostille before submission to Chinese authorities. China joined the Hague Apostille Convention, with the Convention entering into force for China and the United States on November 7, 2023, replacing the previous consular legalization process.

Start this step early. It routinely takes the longest of any stage in the process.

Step 3: Reserve Company Name and Secure a Registered Address

Chinese company names follow a specific format: administrative division + trade name + industry/business characteristics + organizational form (typically "Co., Ltd."). The name must be approved by the local AMR before registration proceeds.

Simultaneously, secure a physical office lease. Proof of address is required for registration, and virtual offices are not universally accepted ; local AMR practice and the intended business activity govern what qualifies.

Step 4: Submit Registration Documents to the AMR

Core filing documents include:

- Articles of Association (in Chinese)

- Office lease agreement or property ownership documents

- Shareholder qualification certificate or identity documents

- Board resolutions and appointment letters for the legal representative, directors, and supervisors

- Sector-specific approvals (where required by law)

- Certified Chinese translations of all foreign-language documents

A feasibility study is not a universal requirement ; it applies only where the regulated sector or approving authority specifically requires one.

Step 5: Obtain Business License and Complete Post-Approval Registrations

Once the AMR approves the application, the company receives its Business License (the legal foundation for operations). From there, several registrations must follow:

- Company chop (official seal) — required for contracts and official correspondence

- Tax registration with the State Taxation Administration (STA) for a tax ID

- Corporate bank accounts — RMB Basic Account and Foreign Currency Capital Account

- Customs registration — required if import/export activities are planned

- Social insurance registration — required before hiring staff

Step 6: Inject Registered Capital

China operates on a subscribed capital model. There is no universal minimum capital requirement for most industries, but shareholders must declare a contribution schedule in the Articles of Association. Under the revised Company Law (effective July 1, 2024), all subscribed capital must be fully paid within five years of incorporation.

Two points to build into your plan from day one:

- Capital source: The Foreign Investment Law permits reinvestment of profits earned within China. China's cross-border RMB regime also allows qualifying RMB direct investment, so registered capital isn't limited to foreign-currency remittances from the US.

- Planning the timeline: The five-year deadline is binding; build the capital injection schedule into your Articles of Association deliberately, not left to a later amendment

Post-Registration Compliance: What US Companies Must Do After Incorporation

Accounting and Tax Obligations

Chinese entities must maintain books per Chinese Accounting Standards (CAS). Key ongoing obligations:

- VAT filings: Monthly or quarterly, at rates of 13%, 9%, or 6% depending on transaction type

- Corporate Income Tax (CIT): Standard rate is 25%; qualifying high and new technology enterprises (HNTEs) pay 15%. Annual CIT returns must be filed and tax settled within five months after year-end — for calendar-year taxpayers, by May 31

- Annual statutory audit: Required each year; prerequisite for dividend repatriation

Dividend payments to a US parent company are subject to 10% withholding tax. The US-China income tax treaty caps source-country tax on dividends at 10% — which aligns with China's generally applicable nonresident rate, so the treaty does not provide a further reduction in most cases.

US-Specific Compliance Overlays

Chinese domestic requirements are only part of the picture. US companies operating in China also carry home-country obligations that travel with the entity regardless of where it operates:

- FCPA: Anti-bribery provisions apply to US issuers and domestic concerns operating through a Chinese subsidiary — the mainland entity does not remove this exposure

- US export controls: BIS controls apply to exports, reexports, and in-country transfers to Chinese entities; the December 2024 semiconductor equipment controls added 24 equipment categories

- PIPL: China's Personal Information Protection Law requires lawful export mechanisms and separate consent for outbound personal data transfers; violations can result in fines up to RMB 50 million or 5% of prior-year turnover

Managing a Chinese subsidiary remotely means running five overlapping compliance tracks simultaneously: CAS accounting, Chinese tax filings, PIPL data governance, FCPA monitoring, and US parent reporting. Each has its own deadlines, regulators, and consequences for non-compliance.

VJM Global works with US-based businesses on cross-border compliance structures — covering tax advisory, financial reporting, and back-office operations — as part of broader international market entry support.

Common Misconceptions and Risks for US Companies

"A Representative Office is a low-risk trial run."

Not quite. ROs are subject to deemed-revenue taxation on expenditures even without generating income — Chinese tax authorities can convert an RO's expenses into taxable deemed revenue using a prescribed formula. They also cannot hire staff directly and cannot be converted to a WFOE. Moving from an RO to a WFOE requires full deregistration of the RO and new registration of the WFOE as separate AMR processes.

"Registered capital can be freely sent back to the US once deposited."

Registered capital injected into a Chinese entity cannot be repatriated without completing the annual audit, settling applicable taxes, and going through the bank's foreign-exchange review process. Routine dividend remittance is processed by authorized banks based on supporting documentation — but it is not a frictionless withdrawal. Restricted or abnormal transactions can still require SAFE involvement.

Sector Restrictions Still Apply

"Our sector is fine because manufacturing restrictions were removed."

The 2024 Negative List did remove remaining manufacturing restrictions, but several categories remain restricted or prohibited for foreign investors:

The 2024 Negative List did remove remaining manufacturing restrictions, but several categories remain restricted or prohibited for foreign investors:

- Telecommunications and media

- Certain financial services

- Internet-related businesses

- Defense-adjacent industries

US companies in technology, data, or dual-use sectors face additional scrutiny under China's expanded anti-espionage and data-security enforcement framework. Monitor MOFCOM updates and consult legal counsel before committing capital.

Frequently Asked Questions

How long does it take to register a company in China from the US?

The process typically spans two to four months, though timelines vary based on entity type, city, industry sector, and how quickly US-side document apostilles are completed. Document legalization is usually the longest single step and should be started before other registration steps.

Do US companies need a local Chinese partner to set up a business in China?

A local partner is only required if the sector appears on the Negative List. Most sectors now allow 100% foreign ownership through a WFOE; the 2024 update further opened manufacturing. A JV is required only in restricted or regulated industries.

What is the minimum registered capital for a US company to set up in China?

There is no universal minimum for most industries. The 2024 Company Law amendments require that all subscribed capital be fully injected within five years of incorporation. Regulated sectors like banking, insurance, and securities carry specific statutory minimums.

Can a US citizen serve as the legal representative of a Chinese company?

Yes. The Company Law places no nationality requirement on the legal representative role. However, the legal representative carries significant personal legal liability for the company's compliance — many US companies appoint a China-based individual for practical day-to-day legal responsibility.

What taxes does a US-owned company in China have to pay?

Core taxes include Corporate Income Tax at 25% (or 15% for qualifying HNTEs), VAT at 6–13% depending on business type, and a 10% withholding tax on profits repatriated to the US parent — a rate confirmed by the US-China tax treaty's dividend withholding cap.

Are there sectors where US companies cannot invest in China?

The 2024 Negative List specifies restricted and prohibited sectors. Telecommunications, media, certain financial services, and defense-adjacent industries remain restricted or prohibited. US companies in technology and data-intensive sectors also face heightened scrutiny under China's anti-espionage and data-security laws.