Hong Kong consistently ranks among the world's top financial centres. The Global Financial Centres Index 39 (March 2026) placed Hong Kong third globally, ahead of Singapore. For US founders targeting Asian markets, that positioning matters.

This guide covers everything you need to know: business structures, registration requirements, government fees, tax obligations, and the ongoing compliance responsibilities that follow incorporation.

Key Takeaways

- US citizens can own 100% of a Hong Kong private limited company with no residency requirement

- Online incorporation through the Companies Registry e-Services Portal is typically processed within 1 hour

- Government fees start at approximately HKD 3,895 (e-filing fee + 1-year Business Registration Certificate)

- Hong Kong taxes only Hong Kong-sourced profits, though US owners must separately address CFC obligations under US tax law

- Post-incorporation obligations include annual returns, audited financials, profits tax returns, and a Significant Controllers Register

Why US Entrepreneurs Register a Company in Hong Kong

Hong Kong's appeal as a business destination goes beyond low taxes. Its common law legal framework mirrors what US founders are familiar with, capital moves freely in and out, and the city sits at the geographic and economic gateway to Mainland China.

InvestHK reported that companies with Chinese Mainland or overseas parent companies reached 11,070 in 2025 — an 11% increase from 2024 — reflecting sustained confidence in Hong Kong as a regional business hub. The tax structure is a big part of that confidence.

The Tax Advantages

Hong Kong's tax structure is straightforward:

- No VAT or GST: sales and services are not subject to consumption tax

- No capital gains tax: profits from asset sales are not taxed at the entity level

- No withholding tax on dividends or interest: distributions to foreign shareholders pass through cleanly

- Two-tier corporate profits tax: 8.25% on the first HKD 2 million of assessable profits, 16.5% above that threshold

These rates apply only to profits sourced in Hong Kong — not global income. For US founders, this territorial tax system creates genuine planning opportunities — particularly for operations that serve Asian markets from a Hong Kong base. US-side reporting obligations still apply, and those are covered in the tax section below.

Business Structures Available to US Entrepreneurs

Three main options exist for US founders looking to establish a presence in Hong Kong:

| Structure | Liability | Profit-Making? | Best For |

|---|---|---|---|

| Private Limited Company | Limited to shareholders | Yes | Most US founders |

| Branch Office | Parent bears all liability | Yes | Extending an existing US entity |

| Representative Office | N/A | No | Market research / liaison only |

The private limited company is the default recommendation for most US founders. It's a separate legal entity from its owners, limits personal liability, and permits 100% foreign ownership. The US parent company can serve as the shareholder, making this structure clean for both standalone ventures and subsidiaries.

A branch office is not a separate legal entity: the US parent company is directly liable for all its debts and obligations. That's direct liability exposure most founders prefer to avoid. A representative office cannot engage in profit-making activities at all, so it's only suitable for preliminary market exploration.

Requirements for Hong Kong Company Registration

Directors and Shareholders

- At least one natural person must serve as director — a sole director can also be the sole shareholder

- No Hong Kong residency required for directors or shareholders

- Corporate shareholders (including a US parent company) are permitted

- Directors must be individuals; a company with only one director cannot use a corporate director

Company Secretary

A company secretary is mandatory and must be either a Hong Kong resident individual or a body corporate with a registered office or place of business in Hong Kong. A sole director cannot also serve as company secretary.

This is the one role US-based founders cannot fill themselves. Most professional incorporation services bundle a licensed company secretary with a registered address. Arrange this before filing, since company secretary details are required on the incorporation form.

Registered Office

Must be a physical Hong Kong street address — P.O. boxes are not accepted. Virtual office and registered address services are widely available and fully acceptable for this purpose.

Share Capital

There is no minimum paid-up share capital under the Companies Ordinance. Most founders start with a nominal amount. No stamp duty applies on share capital at incorporation.

Key Documents Required

- Form NNC1 — Incorporation form for companies limited by shares

- Articles of Association — Model articles are available from the Companies Registry

- Form IRBR1 — Notice to the Business Registration Office

- Identity particulars for all directors and shareholders (passport numbers and issuing country/region for non-Hong Kong residents)

Step-by-Step: How to Register a Hong Kong Company from the US

The entire process runs through the Companies Registry e-Services Portal. No travel required.

Step 1: Reserve Your Company Name

Check name availability on the e-Services Portal before filing. Key rules:

- English names must end with "Limited"

- No mixing English letters and Chinese characters in a single name

- No names identical to existing registered companies

- Certain words are restricted and require approval

If your application is rejected due to a name issue, the lodgement fee (HKD 265 for electronic applications) is non-refundable. Check availability thoroughly first.

Step 2: Appoint a Company Secretary and Registered Address

Arrange a TCSP-licensed company secretary and registered address service before you file, as their details go directly onto Form NNC1. VJM Global works with US entrepreneurs on cross-border business setup and can help you identify qualified local service providers in Hong Kong.

Step 3: Prepare and Submit Your Application

- Create a user account on the e-Services Portal (a director must be the registered account holder)

- Complete Form NNC1 online

- Upload required identity particulars

- Choose your Business Registration Certificate period (1 or 3 years)

- Sign electronically and submit

Step 4: Pay Government Fees

Current government fees for online incorporation:

- Companies Registry e-filing fee (NNC1): HKD 1,545

- 1-year Business Registration Certificate: HKD 2,350 (HKD 2,200 fee + HKD 150 levy, applicable for certificates issued in the 01.04.2026–31.03.2027 period)

- Total: approximately HKD 3,895

Payment is made through the e-Services Portal at submission.

Step 5: Receive Your Certificates

Electronic Certificates of Incorporation and Business Registration Certificates are issued in PDF format. For straightforward online applications, these are normally issued within 1 hour. Hard-copy applications take approximately 4 working days. Electronic certificates carry the same legal effect as paper certificates.

Step 6: Open a Business Bank Account

Your newly incorporated company needs a bank account to operate. Key considerations when choosing:

- Traditional Hong Kong banks have historically required in-person meetings, though the HKMA now encourages remote onboarding

- Some banks support remote account opening for eligible companies — research eligibility requirements before committing

- Fintech alternatives (multi-currency accounts, digital banking platforms) are a practical backup if traditional bank onboarding proves slow

Tax Implications for US Entrepreneurs with a Hong Kong Company

Hong Kong's Territorial Tax System

Hong Kong taxes only profits arising in or derived from Hong Kong. Income earned outside Hong Kong is not subject to Hong Kong profits tax. The two-tier rates: 8.25% on the first HKD 2 million, 16.5% on the remainder.

There is no capital gains tax, no dividend withholding tax, and no VAT — which makes Hong Kong particularly efficient for holding structures and trading companies with offshore operations.

The US Tax Dimension

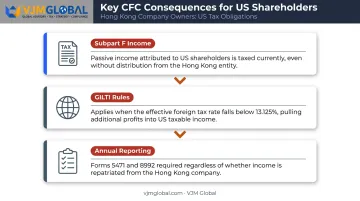

Hong Kong's tax efficiency doesn't eliminate US obligations. As a US person, owning a foreign corporation triggers additional requirements under the US Tax Code, most critically the Controlled Foreign Corporation (CFC) rules under Subpart F.

Under these rules, if US persons own more than 50% of a foreign corporation, key consequences include:

- Subpart F income (certain passive income) is attributed to US shareholders and taxed currently, even without a distribution

- GILTI (Global Intangible Low-Taxed Income) applies when the effective foreign tax rate falls below 13.125%, pulling additional profits into US taxable income

- Annual reporting obligations arise, including Forms 5471 and 8992, regardless of whether any income is repatriated

This is not a detail to figure out after incorporating. US entrepreneurs should consult qualified US international tax counsel before setting up a Hong Kong entity.

The FSIE Regime (2023–2024)

Hong Kong introduced a Foreign-Sourced Income Exemption (FSIE) regime, effective January 1, 2023, expanded further from January 1, 2024. Under this regime, certain passive income received in Hong Kong by MNE entities — including dividends, interest, and equity disposal gains — may be deemed taxable in Hong Kong unless the entity demonstrates economic substance or meets other qualifying conditions.

US founders with group structures involving passive income flows into Hong Kong should seek early tax advice on FSIE implications.

Post-Registration Compliance and Common Pitfalls

Ongoing Compliance Obligations

| Obligation | Deadline / Frequency | Notes |

|---|---|---|

| Annual Return (Form NAR1) | Within 42 days of incorporation anniversary | Late fees: HKD 870 to HKD 3,480 depending on delay |

| Audited Financial Statements | Annual | Required for all companies except dormant ones |

| Profits Tax Return | Annual (filed with IRD) | Triggered after first year of operations |

| Significant Controllers Register (SCR) | Ongoing | Must be kept at registered office; available for inspection by law enforcement on demand |

The 42-day annual return window catches founders off guard more than anything else. Missing it doesn't just create administrative hassle: the late filing penalties escalate quickly, from HKD 870 for minor delays to HKD 3,480 for significant ones.

For US founders, the compliance picture doesn't stop at Hong Kong. Obligations like Form 5471, CFC classification, and international tax structuring require attention on the US side as well. VJM Global works with 500+ American business owners on exactly these cross-border tax and compliance engagements, helping them manage the US-side reporting that kicks in once a foreign entity is established.

Common Mistakes to Avoid

- Missing the 42-day annual return window — set a calendar reminder the day you incorporate

- Failing to update the SCR — any change in significant controllers must be reflected promptly

- Assuming all offshore income is tax-exempt — the FSIE regime has narrowed this assumption for MNE entities

- Ignoring US CFC obligations — incorporate first, address US tax later is a costly sequence

What Registration Does Not Provide

- No right to live or work in Hong Kong — a separate visa or entry permit is required

- **No exemption from US tax reporting** — Form 5471 and other filings still apply

- No license for regulated activities — financial services, money services, and other regulated sectors require separate authorization from the SFC, HKMA, or other relevant authorities

Frequently Asked Questions

How do I register a company in Hong Kong?

Registration is completed online through the Companies Registry e-Services Portal by submitting Form NNC1, Articles of Association, and Form IRBR1, along with payment of the applicable government fees. A director must hold the portal account and sign the application electronically.

Can foreigners register a company in Hong Kong?

Yes. There are no foreign ownership restrictions. US citizens can own 100% of a Hong Kong private limited company and serve as sole director and shareholder without any residency requirement.

How long does it take to register a company in Hong Kong?

Online applications for private companies limited by shares are normally processed within 1 hour. Hard-copy applications take approximately 4 working days.

Is Hong Kong tax-free for foreigners?

Not exactly. Hong Kong taxes only profits sourced locally — not worldwide income — and levies no capital gains, dividend, or VAT. That said, US owners remain subject to US obligations, including potential CFC and GILTI rules on their Hong Kong company's income.

Do I need to travel to Hong Kong to register a company?

No. The entire incorporation process can be completed remotely from the US through the e-Services Portal. Document signing is handled electronically, and certificates are issued in PDF format.

What are the ongoing compliance requirements for a Hong Kong company?

Key annual obligations include:

- Filing Form NAR1 within 42 days of the incorporation anniversary

- Maintaining audited financial statements

- Filing a Profits Tax Return with the IRD

- Keeping the Significant Controllers Register current