The problem: Many foreign-owned companies operating in Singapore overpay for statutory audits they don't legally require, miss available tax exemptions worth up to SGD 21,250 annually, or misunderstand which compliance obligations remain even when exempt. A 2024 ACRA survey found that 40% of qualifying small companies were unaware they could claim audit exemption, resulting in unnecessary compliance costs.

This guide clarifies the three distinct categories of CPA exemptions in Singapore, explains who qualifies under each framework, and outlines the compliance obligations that persist regardless of exemption status.

Key Takeaways

- Small companies meeting two of three criteria (revenue ≤ SGD 10M, assets ≤ SGD 10M, ≤ 50 employees) for two consecutive years qualify for audit exemption

- Dormant companies with zero accounting transactions and assets under SGD 500,000 may skip both audit and financial statement preparation

- New start-ups get a 75% tax exemption on the first SGD 100,000 of income (effective rate: 6.375%) for three years under Singapore's Tax Exemption Scheme

- Qualifying subsidiaries and holding companies may also access audit exemptions if they meet group-level small company thresholds

- All exempt companies must keep SFRS (Singapore Financial Reporting Standards)-compliant records and file annual returns with ACRA within seven months of fiscal year-end

What Are CPA Exemptions in Singapore?

"CPA exemptions in Singapore" covers three distinct regulatory frameworks that often confuse foreign business owners:

- Audit exemptions for companies under the Companies Act (administered by ACRA)

- Corporate tax exemption schemes under the Income Tax Act (administered by IRAS)

- Module exemptions within the Singapore Chartered Accountant Qualification pathway (administered by ISCA under ACRA oversight)

Why ACRA's Exemption Framework Matters

The Accounting and Corporate Regulatory Authority (ACRA) serves as Singapore's central regulator for both public accountants and corporate compliance. It determines which companies must undergo statutory audits, sets financial reporting standards, and manages the professional qualification route for practicing accountants.

Foreign-owned companies operating in Singapore interact with ACRA across several compliance areas:

- Annual return filings and financial statement submissions

- Statutory auditor appointments

- Public accountant registrations for relevant accounting staff

Knowing which exemptions apply to your company can directly reduce compliance costs and administrative burden.

Exemptions Require Annual Assessment

These exemptions are not automatic or permanent — eligibility must be reassessed each financial year against specific quantitative thresholds. A company qualifying for the small company audit exemption in FY2024, for instance, may lose that status in FY2025 if revenue crosses SGD 10M or headcount exceeds 50 employees for two consecutive years.

Audit Exemption for Companies in Singapore

Small Company Audit Exemption

Under the Singapore Companies Act Section 205C, all private limited companies must appoint a qualified public accountant and undergo annual statutory audits—unless they qualify for exemption.

The three quantitative criteria define "small company" status:

| Criterion | Threshold |

|---|---|

| Total annual revenue | ≤ SGD 10 million |

| Total assets | ≤ SGD 10 million |

| Total employees | ≤ 50 (full-time, at FY end) |

The two-out-of-three rule: A company qualifies when it meets at least two criteria for the two immediately preceding consecutive financial years (ACRA - Audit Exemptions).

Example: A Singapore subsidiary of a US software company reports:

- FY2023: Revenue SGD 8.5M, Assets SGD 12M, Employees 45

- FY2024: Revenue SGD 9.2M, Assets SGD 11.5M, Employees 48

This company qualifies in both years (revenue ✓, employees ✓, assets ✗), meeting two of three criteria consecutively. It is exempt from statutory audit starting FY2024.

Small Group Exemption

When a company belongs to a corporate group, both individual and consolidated criteria must be satisfied:

- The individual company must qualify as a small company using its standalone figures

- The entire group must qualify as a "small group" using consolidated revenue, assets, and headcount

This prevents groups from artificially splitting operations across subsidiaries to stay below individual thresholds. If consolidated group revenue exceeds SGD 10M and consolidated assets exceed SGD 10M, the group fails two criteria. All member companies lose the exemption, regardless of their individual metrics (ACRA - Audit Exemptions).

Dormant Company Exemption

Singapore uses two different dormancy definitions that foreign owners must satisfy separately:

| Regulator | Definition | Source |

|---|---|---|

| ACRA (Companies Act S.205B(2)) | No accounting transaction occurs during the period. Administrative acts (e.g., paying ACRA fees, appointing a secretary) are excluded. | SSO - Section 205B |

| IRAS | Company does not carry on business and has no income for the entire basis period. | IRAS - Dormant Companies |

Watch out for the overlap: A company with minor bank charges may satisfy IRAS's test (no business conducted) but fail ACRA's test, since bank fees count as accounting transactions. Full dormancy relief requires satisfying both definitions independently.

Financial statement exemption threshold: Dormant non-listed companies with total assets ≤ SGD 500,000 are exempt from preparing financial statements under Section 201A.

Tax Exemption Schemes for Companies in Singapore

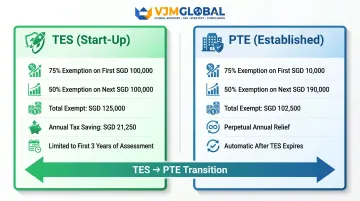

Tax Exemption Scheme (TES) for New Start-Up Companies

TES reduces the tax burden on newly incorporated Singapore companies during their critical early growth phase—the first three consecutive Years of Assessment.

Eligibility criteria (YA 2020 onwards):

- Incorporated in Singapore

- Singapore tax resident for that YA

- Maximum 20 individual shareholders throughout the basis period, with at least one individual holding ≥ 10% of issued ordinary shares

Excluded: Property development companies and investment holding companies cannot claim TES.

Tax relief structure:

| Income Band | Exemption Rate | Exempt Amount | Taxable Amount |

|---|---|---|---|

| First SGD 100,000 | 75% | SGD 75,000 | SGD 25,000 |

| Next SGD 100,000 | 50% | SGD 50,000 | SGD 50,000 |

| Total (SGD 200,000) | — | SGD 125,000 | SGD 75,000 |

Effective tax rate on SGD 200,000 chargeable income:

- Tax payable: SGD 75,000 × 17% = SGD 12,750

- Effective rate: 6.375%

- Standard rate tax: SGD 200,000 × 17% = SGD 34,000

- Annual tax saving: SGD 21,250 for three consecutive years

Partial Tax Exemption (PTE) Scheme

Companies not qualifying for TES—or those beyond their first three YAs—access PTE automatically.

Relief structure (YA 2020 onwards):

| Income Band | Exemption Rate | Exempt Amount | Taxable Amount |

|---|---|---|---|

| First SGD 10,000 | 75% | SGD 7,500 | SGD 2,500 |

| Next SGD 190,000 | 50% | SGD 95,000 | SGD 95,000 |

| Total (SGD 200,000) | — | SGD 102,500 | SGD 97,500 |

Effective tax rate on SGD 200,000: SGD 97,500 × 17% = SGD 16,575 (approximately 8.29% effective rate).

TES vs PTE comparison:

- TES: Deeper relief (SGD 125,000 exempt vs. SGD 102,500) but limited to three years

- PTE: Smaller relief but perpetual—applies annually for the life of the company

- Transition: After TES expires, companies automatically access PTE without separate election

Choosing between the two comes down to your time horizon. TES front-loads the savings—SGD 21,250 per year for three years—while PTE compounds steadily over the company's life. For most startups, TES produces the larger cumulative benefit through year six; after that, PTE's ongoing relief pulls ahead.

Singapore CA Qualification Module Exemptions

The Singapore Chartered Accountant (CA) Qualification, administered by the Institute of Singapore Chartered Accountants (ISCA) under ACRA's regulatory framework, offers module exemptions to candidates with qualifying degrees.

Exemption-Eligible Modules

The Professional Programme comprises six modules:

- Financial Reporting (FR) — Exemption available

- Taxation (TX) — Exemption available

- Assurance (AS)

- Business Value, Governance & Risk (BG)

- Ethics & Professionalism (EP)

- Capstone: Integrative Business Solutions (IB)

Qualifying universities and graduation years:

| Module | Universities | Bachelor's Graduation Year |

|---|---|---|

| Financial Reporting (FR) | NTU, NUS, SIT, SMU, SUSS | From 2022 onwards |

| Taxation (TX) | NTU, NUS, SIT, SMU, SUSS | From September 2020 onwards |

Candidates holding both FR and Tax exemptions complete only four modules (AS, BG, EP, IB) instead of six—saving roughly two full modules and cutting total exam load by 33%.

For those holding a US CPA rather than a local qualifying degree, the pathway looks quite different.

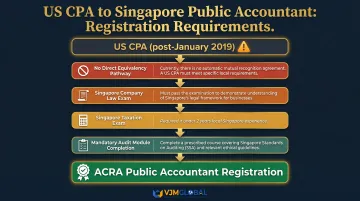

US CPA Recognition

US CPA (AICPA) qualification does not automatically confer Singapore CA status or audit signing rights. While Singapore acknowledges the US CPA as an international credential, holders wishing to conduct statutory audits or practice as public accountants must register with ACRA under Singapore's public accountant registration framework.

Registration barriers for US CPAs: ACRA recognizes AICPA qualification only under pre-2019 pathways. The 2019 rule change created concrete hurdles for anyone who passed the US CPA exam after 1 January 2019:

- No direct equivalency pathway under current ACRA rules

- Requirement to pass Singapore Company Law exam

- Requirement to pass Singapore Taxation and Tax Management exam (if less than two years local experience)

- Mandatory audit module completion

Singapore's framework aligns with Commonwealth accounting traditions and IFRS—not US GAAP—so US CPAs planning audit work here should begin the full SCAQ pathway before taking on statutory engagements.

Compliance Obligations That Remain Even When Exempt

Audit exemption does not equal compliance exemption. Qualifying for small company status removes the statutory audit requirement — it does not remove the obligation to maintain accurate records, file returns, or meet SFRS standards.

Mandatory Requirements for All Companies

Three obligations apply to every Singapore company regardless of audit exemption status:

- Accounting records must be maintained under Section 199 of the Companies Act — this applies universally, with no carve-outs for exempt entities

- Financial statements must comply with SFRS, SFRS(I), or SFRS for Small Entities; exempt companies file unaudited statements, but the accounting standards requirement remains fully in force

- Annual Returns must be filed with ACRA within seven months of fiscal year-end for non-listed companies; late filing carries penalties up to SGD 600

Shareholder Override Right

Section 205B(6) preserves minority investor protection: shareholders holding 5% or more of voting rights can require an audit by written notice, removing exemption for that financial year—even if the company otherwise qualifies.

ACRA's Financial Reporting Surveillance Programme

ACRA operates the Financial Reporting Surveillance Programme (FRSP), under which it selects and reviews filed financial statements for accounting standards compliance. Non-compliance can result in warning letters, composition sums, or prosecution.

Implication: Exempt companies must maintain audit-ready, SFRS-compliant records.

VJM Global's Support for Singapore Compliance

For foreign businesses managing both Singapore operations and India-side accounting obligations, VJM Global provides outsourced accounting and compliance support that keeps records organized and filings on time. VJM Global's team handles statutory filings and ensures financial statements meet applicable reporting standards — reducing the administrative load on founders and finance teams managing multi-jurisdiction obligations. The firm has served 250+ UK and Australian businesses across cross-border compliance engagements, with particular depth in India-entry and ongoing operational compliance.

Frequently Asked Questions

Are there any exemptions for CPA?

In Singapore, "CPA exemptions" cover three distinct areas:

- Audit exemptions for qualifying small companies (meeting two of three criteria: revenue, assets, employees) or dormant companies

- Corporate tax exemptions including the Tax Exemption Scheme (TES) for start-ups and Partial Tax Exemption (PTE) for established companies

- Module exemptions within the Singapore CA Qualification for graduates of accredited local Bachelor of Accountancy programmes

Does Singapore recognize US CPA?

Singapore recognizes the US CPA as a valid international qualification. However, US CPAs who wish to conduct statutory audits or practice as public accountants in Singapore must register with ACRA under Singapore's specific public accountant registration framework, which may require additional exams in Singapore Company Law and Taxation.

Is it mandatory to prepare consolidated financial statements in Singapore?

Under SFRS 10, holding companies are generally required to prepare consolidated financial statements. Exemptions apply to qualifying small groups meeting the two-out-of-three criteria on a consolidated basis, or where the parent is a subsidiary of another entity that already prepares publicly available consolidated financials.

Can a newly incorporated company qualify for audit exemption in Singapore?

New companies do not qualify for small company audit exemption immediately, since the two-out-of-three criteria must be met for two consecutive preceding financial years. However, a company that remains dormant (zero accounting transactions) from incorporation qualifies for dormant company audit exemption immediately.

What happens if an exempt company no longer meets the small company criteria?

If a company fails to meet at least two of the three small company criteria for two consecutive financial years, it loses its audit exemption. The company must then appoint a registered ACRA auditor to conduct a statutory audit for that financial year.

Do audit-exempt companies still need to file financial statements in Singapore?

Yes. Audit-exempt companies must prepare and file unaudited financial statements with ACRA as part of their Annual Return. These statements must comply with SFRS, SFRS(I), or SFRS for Small Entities, and are subject to ACRA's Financial Reporting Surveillance Programme review.