This guide covers everything Singapore businesses need to know about depreciation: the accounting methods available under Financial Reporting Standards (SFRS), how to calculate and record depreciation accurately, and — critically — how depreciation differs from capital allowances under IRAS rules. Many business owners miss this crucial distinction: while depreciation is not tax-deductible under IRAS rules, businesses can claim capital allowances instead. Understanding this difference is essential for effective tax planning and compliance.

Key Takeaways

- Depreciation spreads an asset's cost over its useful life, matching expenses with the revenue the asset generates

- Singapore follows SFRS for accounting depreciation, but IRAS does not allow it as a tax deduction — capital allowances under Sections 19 and 19A apply instead

- Three main methods are recognized under SFRS: straight-line, declining balance, and units of production

- Capital allowances offer three write-off schedules: 1-year (computers/automation), 3-year equal instalments, or prescribed working life of 6, 12, or 16 years

- Poor record-keeping risks IRAS audit exposure — accurate asset records are required for both financial reporting and capital allowance claims

What Is Depreciation and Why It Matters for Singapore Businesses

Depreciation is the systematic allocation of a tangible asset's cost over its useful life. Instead of recognizing the full purchase price as an expense in year one, depreciation spreads the cost across the years the asset generates value, reflecting wear, tear, and obsolescence.

Why it matters in practice:

- Accurate balance sheet values — Assets aren't overstated; their carrying value reflects actual current worth rather than original purchase price

- Matching principle — Expenses align with the revenue the asset helps generate, giving a true picture of profitability period by period

- Capital planning — Tracking depreciation helps forecast when assets need replacement, supporting better CAPEX budgeting

In Singapore, accounting depreciation is governed by SFRS(I) 1-16 (the Singapore Financial Reporting Standard equivalent of IFRS 16), which sets out how companies must recognize and measure property, plant, and equipment. Businesses filing with ACRA must apply these standards consistently. Note that accounting depreciation differs from IRAS capital allowances — the tax deduction mechanism under the Income Tax Act — which follows its own prescribed rates and rules.

This guide focuses on depreciation for tangible fixed assets like machinery, vehicles, and office equipment. Two related concepts apply to different asset types:

- Amortisation — For intangible assets (patents, software licences, trademarks)

- Depletion — For natural resources (mining rights, oil reserves)

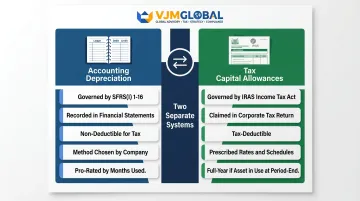

Accounting Depreciation vs IRAS Capital Allowances: The Critical Singapore Distinction

Singapore businesses must manage two separate systems that run in parallel:

| System | Purpose | Framework |

|---|---|---|

| Accounting depreciation | Recorded in financial statements | Singapore Financial Reporting Standards (SFRS) |

| Tax depreciation (capital allowances) | Claimed as tax deduction | IRAS / Income Tax Act |

The Non-Deductible Nature of Depreciation

Under Singapore's Income Tax Act, depreciation recorded in your accounts is a non-deductible expense. When preparing your corporate tax computation, depreciation must be "added back" to accounting profit. In its place, IRAS grants capital allowances on qualifying plant and machinery — this is your actual tax-deductible equivalent.

What Assets Qualify for Capital Allowances

Qualifying assets (plant and machinery):

- Computers, laptops, printers, and prescribed automation equipment

- Office equipment and furniture

- Commercial vehicles (excluding S-plated private cars)

- Industrial machinery and production equipment

- Tools and equipment used in the trade

Non-qualifying assets:

- Fixed partitions, walls, and wall tiles

- Floor tiles, raised floors, and flooring work

- False ceilings and ceiling works

- Doors, roller shutters, and gates

- General electrical fittings and lighting

- Designer's fees for renovation work

These items form part of the building's "setting" rather than functional plant. That said, not all renovation costs are lost from a tax perspective. They may instead qualify for deduction under Section 14N (renovation and refurbishment expenditure), claimed over 3 years with a cap of S$300,000 per three-year period.

The Practical Consequence

Your company's taxable income and accounting profit will differ because:

- Depreciation and capital allowances use different methods

- They apply different rates and timelines

- IRAS capital allowances are granted for the full year if the asset is in use at period-end (no pro-rata), while accounting depreciation is pro-rated by months

These differences must be reconciled in your annual tax computation (Form C or Form C-S).

Budget 2020 Capital Grant Rule

From 1 January 2021 onward, capital allowances cannot be claimed on any portion of expenditure funded by government or statutory board capital grants. Only the net expenditure (cost minus grant) qualifies.

This rule exists to prevent businesses from claiming both a government grant and a tax deduction on the same spending — effectively benefiting twice from public funds. Review your grant documentation before filing capital allowance claims.

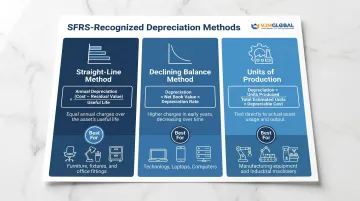

The 3 Main Depreciation Methods Used in Singapore

Singapore businesses must choose a depreciation method that reflects how each asset actually loses value — not just one that's convenient. Under SB-FRS 16 (Property, Plant and Equipment), three recognized approaches are available.

Four key inputs are needed before calculating:

- Cost of asset — Purchase price plus directly attributable costs

- Salvage/residual value — Expected value at end of useful life

- Useful life — Estimated years or units of production

- Depreciable base — Cost minus salvage value

Straight-Line Method (Most Common)

The cost less salvage value is spread equally over the asset's useful life. This method is ideal for assets that generate consistent value year over year, such as office furniture, fixtures, and general-purpose machinery.

Formula:

Annual Depreciation = (Cost − Salvage Value) ÷ Useful Life

Example:

A Singapore logistics company purchases a delivery van for S$60,000. The estimated residual value after 6 years is S$6,000.

- Depreciable base: S$60,000 − S$6,000 = S$54,000

- Annual depreciation: S$54,000 ÷ 6 years = S$9,000 per year

This method delivers predictable expense recognition each year and is the default choice for most Singapore SMEs.

Declining Balance Method

A fixed depreciation rate is applied to the asset's book value each year, resulting in higher depreciation charges early and decreasing amounts over time. This accelerated method suits assets that lose value quickly, such as technology equipment and computers.

Formula:

Depreciation Expense = Book Value at Start of Year × Depreciation Rate

Example:

A S$20,000 server has a 25% declining balance rate:

- Year 1: S$20,000 × 25% = S$5,000 (book value: S$15,000)

- Year 2: S$15,000 × 25% = S$3,750 (book value: S$11,250)

- Year 3: S$11,250 × 25% = S$2,813 (book value: S$8,437)

For assets that depreciate even faster, the double declining balance variant applies twice the straight-line rate — useful for short-lived tech assets or equipment with heavy early use.

Units of Production Method

Depreciation is tied directly to usage — hours operated or units produced — making it ideal for manufacturing equipment or assets whose wear is driven by output rather than time.

Formula:

Depreciation = (Cost − Salvage Value) ÷ Total Estimated Units × Units Produced in Period

Example:

A production machine costs S$100,000 with a S$10,000 salvage value and an estimated capacity of 450,000 units.

- Per-unit depreciation: (S$100,000 − S$10,000) ÷ 450,000 = S$0.20 per unit

- If 30,000 units are produced in Year 1: 30,000 × S$0.20 = S$6,000 depreciation

Depreciation charges will vary year to year with this method, so detailed production records are essential — but the trade-off is expense recognition that closely tracks real-world asset wear.

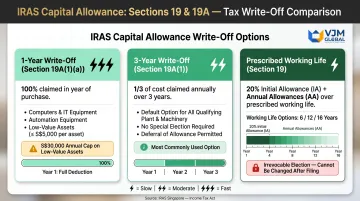

How IRAS Capital Allowances Work in Singapore (Sections 19 and 19A)

Singapore businesses can choose from three main write-off periods under the Income Tax Act 1947. All three apply to qualifying plant and machinery but differ in speed and eligibility. Choosing the right option depends on your cash flow needs, profitability, and tax planning strategy.

100% Write-Off in 1 Year (Section 19A)

Qualifying assets under this option include:

- Computers, laptops, printers, and prescribed automation equipment

- Low-value assets costing S$5,000 or less per item (capped at S$30,000 total per YA)

The full cost is claimed as an annual allowance in the year of purchase. For hire purchase assets, claims are based on the principal payments (deposit and instalments) made within that financial year, excluding the interest component.

The S$30,000 annual cap applies only to the low-value asset category. Computers and automation equipment have no cap.

3-Year Write-Off (Section 19A(1))

This is the default option for all qualifying plant and machinery. One-third of the asset's cost is claimed as an annual allowance each year over 3 years.

Example:

Office furniture costing S$12,000:

- Year 1: S$4,000

- Year 2: S$4,000

- Year 3: S$4,000

Flexibility: Businesses can defer claims (e.g., when the company is in a loss position or benefiting from tax exemptions) without losing entitlement. Unlike the 2-year accelerated write-off under Section 19A(1E), deferral is permitted.

Write-Off Over Prescribed Working Life (Section 19)

Capital allowances are granted over the asset's prescribed working life as per the Sixth Schedule. From YA 2023 onwards, the options are 6, 12, or 16 years.

Calculation:

- Initial Allowance (IA): 20% of capital expenditure, claimed in the YA relating to the basis period in which the expenditure was incurred

- Annual Allowance (AA): The remaining 80% is divided by the elected working life

Example:

Industrial machinery costing S$100,000 with a 12-year working life election:

- Year 1 IA: S$100,000 × 20% = S$20,000

- Remaining base: S$100,000 − S$20,000 = S$80,000

- Annual AA (Years 1-12): S$80,000 ÷ 12 = S$6,667 per year

- Total Year 1 claim: S$20,000 + S$6,667 = S$26,667

Critical: The election is irrevocable once made at the time of first tax filing for the asset.

Balancing Allowance and Balancing Charge on Disposal

When a qualifying asset is sold, scrapped, or transferred, tax consequences arise based on the sale proceeds relative to the tax written-down value (TWDV).

| Scenario | Tax Treatment |

|---|---|

| Sale Proceeds < TWDV | Balancing Allowance (additional tax deduction) |

| Sale Proceeds > TWDV | Balancing Charge (taxable income, capped at total CA previously claimed) |

Example — Balancing Charge:

A delivery van was purchased for S$60,000. Total capital allowances claimed over 4 years: S$40,000. TWDV at disposal: S$20,000. Sale proceeds: S$35,000.

- Excess: S$35,000 − S$20,000 = S$15,000

- Balancing charge (taxable): S$15,000

- The charge cannot exceed S$40,000 (total CA claimed)

This mechanism prevents taxpayers from claiming allowances during ownership and then realizing a tax-free gain on disposal.

How to Record Depreciation in Your Financial Statements

At each accounting period end, depreciation is recorded through a standard journal entry:

Debit: Depreciation Expense (income statement) Credit: Accumulated Depreciation (balance sheet contra-asset account)

Accumulated depreciation reduces the gross asset value to arrive at the net book value (carrying amount) shown on the balance sheet. The asset's original cost is preserved separately for transparency and disclosure purposes.

Impact Across the Financial Statements

Income Statement:

- Depreciation expense reduces operating profit and net income

- Non-cash expense that affects profitability but not cash flow

Balance Sheet:

- Gross asset value remains unchanged

- Accumulated depreciation (contra-asset) increases each period

- Net book value (cost minus accumulated depreciation) decreases

Cash Flow Statement:

- Under the indirect method, depreciation is added back to net income when reconciling to operating cash flow

- This add-back matters for EBITDA analysis and understanding true cash generation

Dual-Track Record Keeping

While accounting depreciation is recorded using your chosen method (straight-line, declining balance, etc.), the tax computation must separately track capital allowances.

Two parallel records are required:

- Fixed asset register — tracks accounting depreciation calculated per SFRS for financial reporting

- Capital allowance schedule — tracks tax depreciation calculated per IRAS rules for your Corporate Income Tax Return

Form C filers must submit the capital allowance schedule with their Corporate Income Tax Return. Form C-S filers must retain the schedule for at least 5 years and submit it upon IRAS request.

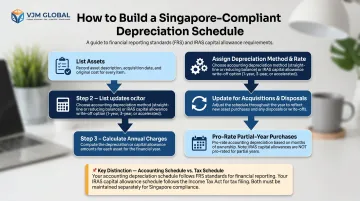

Building and Using a Depreciation Schedule for Singapore Compliance

A depreciation schedule is a structured, asset-by-asset table for tracking each fixed asset across its useful life. It records cost, purchase date, depreciation method, annual depreciation expense, accumulated depreciation, and net book value (or Tax Written Down Value for IRAS purposes).

Singapore businesses typically maintain two separate schedules:

- Accounting schedule — Based on SFRS methods and useful life estimates

- Tax schedule — Based on IRAS capital allowance rules

How to Build a Basic Schedule

Step-by-step process:

- List each qualifying asset with description, date acquired, and original cost

- Assign the applicable depreciation method and rate (accounting) or write-off option (tax)

- Calculate annual depreciation charges

- Update the schedule when assets are acquired or disposed of during the year

- For partial-year purchases, pro-rate accounting depreciation based on months of ownership (note: IRAS capital allowances are not pro-rated)

Sample 3-Year Depreciation Schedule (Straight-Line Method)

Asset: Office Furniture

Cost: S$12,000

Salvage Value: S$0

Useful Life: 6 years

Method: Straight-line

Annual Depreciation: S$2,000

| Year | Opening NBV | Depreciation Expense | Accumulated Depreciation | Closing NBV |

|---|---|---|---|---|

| 1 | S$12,000 | S$2,000 | S$2,000 | S$10,000 |

| 2 | S$10,000 | S$2,000 | S$4,000 | S$8,000 |

| 3 | S$8,000 | S$2,000 | S$6,000 | S$6,000 |

Beyond Compliance: Strategic Asset Planning

A current depreciation schedule does more than satisfy auditors — it gives you actionable data for three key business decisions:

- Forecasting capital expenditure: Identify assets nearing end of useful life so you can plan replacement timing and budget accordingly

- Timing asset disposals: Compare current book value against market value to assess whether repairing, replacing, or selling makes financial sense

- Detecting impairment: Flag assets where market value has fallen sharply below book value — under SFRS 36, an impairment loss must be recognized immediately in profit or loss when the carrying amount exceeds the recoverable amount (the higher of fair value less disposal costs and value in use)

Unlike systematic depreciation, impairment is not scheduled — it is triggered by specific indicators and recorded as soon as those indicators arise.

Frequently Asked Questions

Is depreciation deductible in Singapore?

No. Accounting depreciation is not tax-deductible under Singapore's Income Tax Act and must be added back in the tax computation. Instead, IRAS allows capital allowances on qualifying plant and machinery under Sections 19 and 19A, which serves as the tax-deductible equivalent.

How is depreciation recorded in accounting?

At the end of each accounting period, debit Depreciation Expense (income statement) and credit Accumulated Depreciation (balance sheet contra-asset account). Accumulated depreciation reduces the asset's carrying value while preserving the original cost.

What are the main types of depreciation methods?

Singapore SFRS recognizes three methods: straight-line (equal charges each year), declining balance (accelerated, higher early charges), and units of production (based on actual usage). Straight-line is the most commonly used.

What is the difference between depreciation and capital allowances in Singapore?

Depreciation is an accounting concept governed by SFRS and recorded in financial statements. Capital allowances are a tax concept governed by IRAS and claimed in the corporate tax return. Both systems operate independently and must be managed separately.

What assets qualify for capital allowances in Singapore?

Plant and machinery used in trade or business qualify — including computers, office equipment, commercial vehicles (not S-plated private cars), industrial machinery, and furniture. Renovation costs, fixed partitions, floor tiles, and assets purchased for donation do not qualify.

What happens to capital allowances when a qualifying asset is sold?

If sale proceeds exceed the tax written-down value (TWDV), a balancing charge (taxable income) arises, capped at the total allowances previously claimed. If proceeds are lower than TWDV, a balancing allowance (additional deduction) is granted.

Singapore's dual-track system — separate rules for accounting depreciation and tax capital allowances — requires careful record-keeping to stay compliant and avoid costly errors at year-end.

VJM Global provides accounting outsourcing, corporate tax preparation, and depreciation schedule management for businesses operating across international markets. With 30+ years of experience and a team of 100+ accounting professionals, the firm handles the technical detail so you can focus on operations. Reach out at info@vjmglobal.com or visit the accounting outsourcing services page to learn more.