Foreign businesses entering Singapore often face confusion around when to register for GST, how to maintain economic substance to avoid new capital gains exposure under Section 10L, and which accounting standards apply to their entity size. Penalties for non-compliance can be steep—up to SGD 10,000 for transfer pricing documentation failures, and automatic 5% surcharges on late GST returns—making early understanding essential.

This guide breaks down Singapore's major tax categories, accounting compliance requirements, and international tax considerations that every foreign business owner or investor should understand before establishing operations.

Key Takeaways

- Corporate tax is a flat 17%; new companies can qualify for effective rates as low as 4.25% on the first SGD 100,000 via the Start-Up Tax Exemption scheme

- Personal income tax runs 0–24% for residents; non-residents pay 15% on employment income

- GST stands at 9% and mandatory registration triggers at SGD 1 million taxable turnover

- Singapore's ~100 Double Tax Agreements cut withholding tax rates and support Certificate of Residence claims across major jurisdictions

- Companies follow Singapore Financial Reporting Standards (SFRS/FRS); entities under SGD 10 million revenue may use the simplified SFRS for Small Entities framework

Corporate Income Tax in Singapore

Singapore taxes companies on income accrued in or derived from Singapore, covering:

- Business profits and gains from trade

- Investment income (dividends, interest, rental)

- Royalties and intellectual property income

- Other revenue-nature gains

Foreign-sourced income becomes taxable when remitted to, transmitted to, or brought into Singapore. Qualifying foreign income (dividends, branch profits, service income) may be exempt under Section 13(8)/(9) if it was taxed in the foreign jurisdiction at a headline rate of at least 15%.

Single-Tier Tax System and Capital Gains Treatment

Since January 2003, Singapore applies a single-tier corporate tax: the 17% rate is final. Dividends distributed to shareholders—whether individuals or corporations—are tax-exempt with no withholding tax imposed.

Capital gains from selling fixed assets are generally not taxed. However, Section 10L, effective 1 January 2024, now taxes certain gains from disposal of foreign assets when received in Singapore.

Gains from foreign asset disposals (excluding intellectual property rights) remain non-taxable if the entity maintains adequate economic substance in Singapore. Entities may apply for an advance ruling on their economic substance adequacy, with rulings covering up to five years of assessment.

Basis of Assessment and Filing

Singapore uses a preceding year basis: companies file taxes for the financial year that ended in the prior calendar year. For example, YA 2026 covers income earned from 1 January to 31 December 2025.

Key deadlines:

- Estimated Chargeable Income (ECI): File within 3 months of financial year-end

- Corporate tax return (Form C/C-S/C-S Lite): Submit by 30 November each year via IRAS's myTax Portal

After review, IRAS issues a Notice of Assessment (NOA) confirming the final tax payable.

Tax Exemptions for Companies

Singapore offers two core exemption schemes:

Start-Up Tax Exemption (SUTE) — Available to qualifying newly incorporated companies for their first three consecutive Years of Assessment:

- 75% exemption on first SGD 100,000 of chargeable income (maximum exemption: SGD 75,000)

- 50% exemption on next SGD 100,000 (maximum exemption: SGD 50,000)

- Total maximum exemption per year: SGD 125,000

SUTE excludes investment holding companies and property developers. Eligible companies must be Singapore-incorporated, tax resident, and have no more than 20 shareholders who are all individuals (or at least one individual holding ≥10% of ordinary shares).

Partial Tax Exemption (PTE) — Applies by default to all companies not claiming SUTE. The thresholds are lower than SUTE but still meaningful:

| Income Band | Exemption Rate | Maximum Exemption |

|---|---|---|

| First SGD 10,000 | 75% | SGD 7,500 |

| Next SGD 190,000 | 50% | SGD 95,000 |

| Total per year | — | SGD 102,500 |

Budget 2026 Corporate Tax Rebate (YA 2026):

- Enhanced to 50% of corporate tax payable, capped at SGD 40,000

- Includes a SGD 2,000 minimum Cash Grant for active companies employing at least one local employee with CPF contributions in 2025

- Applies to all taxpaying companies regardless of tax residency status

Transfer Pricing and Record Keeping

Beyond exemptions and rebates, companies with related-party cross-border transactions face a separate compliance layer: Singapore's arm's length principle, aligned with the OECD Transfer Pricing Guidelines.

Mandatory documentation applies when:

- Gross revenue from trade or business exceeds SGD 10 million for the basis period; or

- Transfer pricing documentation was required in the immediately preceding basis period

Key obligations:

- Documentation must be completed by the tax return filing deadline and submitted within 30 days of an IRAS request

- Records retained for at least 5 years from the end of the basis period

- IRAS imposes a 5% surcharge on any transfer pricing adjustment made under Section 34D

- Penalty for non-compliance: fine not exceeding SGD 10,000

- Related Party Transaction (RPT) reporting required if RPT value exceeds SGD 15 million in financial statements

For stable, unchanged arrangements, documentation may be refreshed once every three years rather than annually — a practical concession worth tracking as part of your compliance calendar.

Personal Income Tax in Singapore

Singapore applies a territorial tax system to individuals. Tax residents are taxed on a progressive scale from 0% to 24% (from YA 2024 onwards), while non-residents pay a flat 15% on employment income or resident rates if higher.

Resident Tax Rates

The first SGD 20,000 of chargeable income is taxed at 0%, meaning individuals earning below this threshold owe no income tax. Anyone earning SGD 20,000 or more annually must file a return.

Progressive tax bands (YA 2024 onwards):

| Chargeable Income (SGD) | Tax Rate | Cumulative Tax (SGD) |

|---|---|---|

| First 20,000 | 0% | 0 |

| Next 10,000 | 2% | 200 |

| Next 10,000 | 3.5% | 550 |

| Next 40,000 | 7% | 3,350 |

| Next 40,000 | 11.5% | 7,950 |

| Next 40,000 | 15% | 13,950 |

| Next 40,000 | 18% | 21,150 |

| Next 40,000 | 19% | 28,750 |

| Next 120,000 | 20% | 52,750 |

| Next 160,000 | 22% | 87,950 |

| Next 200,000 | 23% | 133,950 |

| Above 1,000,000 | 24% | — |

Non-Resident Taxation

Non-residents are taxed at flat rates rather than the progressive scale. Key rates:

- Employment income: 15% flat rate or progressive resident rates, whichever is higher

- Director's fees: 24%

- Other income (rental, pension, consultation fees): 24%

- Non-resident professionals: 15% of gross income or 24% of net income

- Short-term employment (60 days or less): exempt (excludes directors, public entertainers, professionals)

Tax Residency Criteria

A foreigner qualifies as a tax resident if they have:

- Stayed or worked in Singapore for at least 183 days in the preceding calendar year; or

- Stayed or worked continuously for 3 consecutive years (even if less than 183 days in year 1 and/or year 3); or

- Worked for a continuous period straddling 2 calendar years with total stay of at least 183 days (employees only)

Auto-Inclusion Scheme (AIS)

From YA 2022, employers with five or more employees must register for AIS. Smaller employers may join voluntarily.

AIS employers submit employment income data electronically to IRAS, which uses this information to pre-fill individual tax returns, streamlining filing for over 2 million employees and reducing reporting errors.

Tax Clearance for Foreign Employees

When a foreign employee leaves Singapore permanently, goes on overseas posting, or departs for more than 3 months, specific employer obligations are triggered:

- File Form IR21 with IRAS at least one month before the employee's departure

- Withhold all monies due to the employee until IRAS grants tax clearance

- Applies to all work pass holders, including Personalised Employment Pass (PEP) holders

Failure to withhold or file on time can expose the employer to liability for any outstanding tax owed.

Goods and Services Tax (GST) in Singapore

GST is Singapore's consumption tax. The current rate stands at 9% (increased from 8% on 1 January 2024), charged by GST-registered businesses on top of the selling price.

Registration Triggers

GST registration is not automatic. A company must register when:

- Taxable turnover exceeds SGD 1 million at the end of a calendar year (retrospective view); or

- Taxable turnover is expected to exceed SGD 1 million in the next 12 months (prospective view)

Taxable turnover includes standard-rated and zero-rated supplies but excludes exempt supplies, out-of-scope supplies, and sale of capital assets.

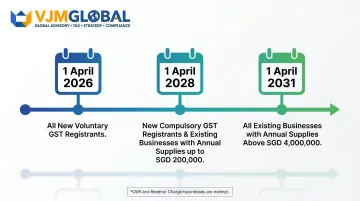

Voluntary registration is available for businesses below the threshold. However, from 1 April 2026, all new voluntary GST registrants must adopt InvoiceNow (Peppol-based e-invoicing) to transmit invoice data to IRAS electronically.

Filing and Compliance

GST-registered businesses must:

- File GST returns (Form GST F5) via myTax Portal within one month from the end of each accounting period (typically quarterly)

- Submit nil returns even when no transactions occurred

- Claim input tax credits on GST incurred on business purchases and expenses (subject to claiming conditions)

Penalties for late filing:

- IRAS may issue an estimated Notice of Assessment

- Automatic 5% late payment penalty on tax due

InvoiceNow (E-Invoicing) Rollout

These compliance obligations now extend to e-invoicing. Singapore is phasing in mandatory e-invoicing for GST-registered businesses:

| Implementation Date | Who Must Comply |

|---|---|

| 1 April 2026 | All new voluntary GST registrants |

| 1 April 2028 | All new compulsory GST registrants; existing businesses with annual supplies up to SGD 200,000 |

| 1 April 2031 | All existing businesses with annual supplies above SGD 4,000,000 |

Overseas vendors (OVR) and businesses liable solely under Reverse Charge are exempt.

GST vs. VAT/SST Clarification

Singapore uses GST (Goods and Services Tax), not VAT or SST. Singapore's GST functions as a broad-based consumption tax, much like VAT. Foreign businesses familiar with VAT systems will find it conceptually equivalent: input tax credits offset output tax collected, with quarterly reconciliation.

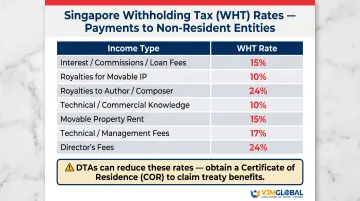

Withholding Tax and Other Business Taxes

Withholding Tax

When a Singapore-based company makes certain payments to non-resident entities, the payer must deduct withholding tax at the applicable rate and remit it to IRAS.

Standard WHT rates:

| Nature of Income | WHT Rate |

|---|---|

| Interest, commissions, fees for loans | 15% |

| Royalties for movable properties (e.g., IP) | 10% |

| Royalties to author/composer/choreographer | 24% |

| Technical/commercial knowledge use | 10% |

| Rent for movable properties | 15% |

| Technical assistance/management fees | 17% (prevailing CIT rate) |

| Director's fees (non-resident individuals) | 24% |

Singapore's DTAs can reduce these rates—taxpayers should verify the applicable rate under each treaty jurisdiction and obtain a Certificate of Residence (COR) to claim reduced rates.

Property Tax and Stamp Duty

Property tax is based on Annual Value (AV)—the estimated annual rent the property could reasonably command. Owner-occupied and non-owner-occupied residential properties are taxed on progressive scales. Non-residential properties (commercial, industrial) are taxed at a flat 10% of AV.

Stamp duty rates on property purchases:

- Buyer's Stamp Duty (BSD): Progressive scale from 1% to 6% of purchase price or market value

- Additional Buyer's Stamp Duty (ABSD) — on or after 27 April 2023:

- Foreigners buying any residential property: 60%

- Singapore Citizens — 2nd property: 20%

- Singapore PRs — 1st property: 5%; 2nd property: 30%

- Entities (non-individuals): 65%

The 60% ABSD rate for foreigners is among the highest globally. Foreign investors should note that commercial and industrial properties are not subject to ABSD, making them a more accessible entry point for property-related investment.

Pillar 2 Top-Up Tax

From financial years starting 1 January 2025, Singapore implemented the Domestic Top-up Tax (DTT) and Multinational Enterprise Top-up Tax (MTT) under the OECD's Pillar 2 framework.

Key parameters:

- Applies to MNE groups with annual consolidated revenue of at least EUR 750 million in at least 2 out of 4 preceding financial years

- Minimum effective tax rate: 15%

- DTT tops up the effective tax rate of Singapore-located entities to 15%

- MTT (Income Inclusion Rule) applies to Singapore-parented MNE groups regarding low-taxed foreign subsidiaries

This does not affect SMEs or standard foreign businesses below the EUR 750 million threshold. Only large multinational enterprises face this additional compliance layer.

For MNE groups with India-Singapore cross-border structures, Pillar 2 compliance intersects with transfer pricing obligations and FEMA requirements on the Indian side. VJM Global's international tax team advises on these multi-jurisdictional scenarios, helping businesses assess their DTT/MTT exposure alongside India-specific compliance.

Double Taxation Agreements and Accounting Standards in Singapore

Double Taxation Agreements (DTAs)

Singapore has concluded DTAs, limited DTAs, and Exchange of Information (EOI) arrangements with approximately 100 jurisdictions. These bilateral agreements prevent the same income from being taxed twice by defining which country has taxing rights over different income types—dividends, interest, royalties, capital gains, and employment income.

How DTAs work:

- Provide relief via the credit method (foreign tax paid is credited against Singapore tax on the same income) or exemption method

- Enable reduced withholding tax rates on cross-border payments

- Require proof of Singapore tax residency via a Certificate of Residence (COR) issued by IRAS

Tax residency determination: A company qualifies as tax resident in Singapore when the control and management of its business is exercised there (generally where board meetings are held and strategic decisions are made).

Companies can apply for a COR via mytax.iras.gov.sg. The COR is essential for claiming DTA benefits and reduced withholding tax rates with treaty partners.

Singapore Accounting Standards

All Singapore companies must follow Singapore Financial Reporting Standards:

SFRS(I) (Singapore Financial Reporting Standards - International):

- Mandatory for listed companies

- Substantially converged with IFRS Standards

- Required for entities with public accountability

FRS (Financial Reporting Standards):

- Used by unlisted companies

- Also aligned with IFRS

- Provides comparable quality reporting for private entities

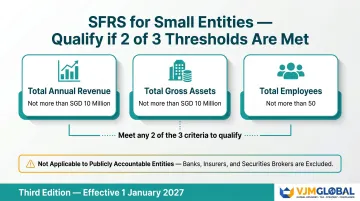

SFRS for Small Entities — A simplified alternative available to companies meeting at least 2 of 3 thresholds for the previous two consecutive reporting periods:

- Total annual revenue: not more than SGD 10 million

- Total gross assets: not more than SGD 10 million

- Total employees: not more than 50

The entity must also be not publicly accountable: it cannot have debt or equity instruments traded on a public market, nor hold assets in a fiduciary capacity for a broad group of outsiders as its primary business. This excludes banks, insurance companies, and securities brokers.

The SFRS for Small Entities is based on the IFRS for SMEs Accounting Standard. The Third Edition becomes effective from 1 January 2027.

Required Financial Statements

All companies must prepare and file annually with the Accounting and Corporate Regulatory Authority (ACRA):

- Statement of financial position

- Statement of profit or loss and other comprehensive income

- Statement of changes in equity

- Statement of cash flows

Records must be maintained in compliance with both ACRA and IRAS requirements, retained for at least 5 years, and annual returns filed on time — late filings attract penalties of up to SGD 600.

Frequently Asked Questions

How much do tax accounting services cost in Singapore?

Costs vary based on company size, transaction complexity, and service scope. Small companies with straightforward finances pay less for basic bookkeeping and tax filing, while MNEs with transfer pricing requirements face higher fees. GST-registered businesses also incur additional costs for quarterly return preparation.

How does Singapore's income tax system work?

Singapore uses a territorial tax system where individuals are taxed progressively (0–24%) on income earned in Singapore, while companies pay a flat 17% on chargeable income. Under the single-tier system in place since 2003, dividends distributed to shareholders are not taxed further at the shareholder level, avoiding double taxation.

Is Singapore tax free for foreigners?

Singapore is not entirely tax-free for foreigners. Non-resident individuals pay a flat 15% (or progressive resident rates if higher) on employment income and 24% on other income such as director's fees. Foreign companies pay the standard 17% corporate tax on Singapore-sourced income, though no capital gains tax or estate duty applies — making Singapore more attractive than many jurisdictions.

Does Singapore use GST (Goods and Services Tax) or VAT/SST?

Singapore uses GST (Goods and Services Tax), not VAT or SST. GST functions similarly to VAT as a broad-based consumption tax currently set at 9%. SST (Sales and Service Tax) is used in neighboring Malaysia—they are distinct systems in different countries.

What tax exemptions are available to companies in Singapore?

Newly incorporated companies can qualify for the Start-Up Tax Exemption (SUTE) for their first three Years of Assessment, exempting up to SGD 125,000 of chargeable income. All other companies benefit from Partial Tax Exemption (PTE), which exempts up to SGD 102,500. Additional sector-specific incentives are available through the Economic Development Board (EDB) for qualifying industries.

What accounting standards do companies in Singapore follow?

Singapore companies follow either Singapore Financial Reporting Standards International (SFRS(I)) for listed companies or Financial Reporting Standards (FRS) for unlisted companies—both aligned with IFRS. Smaller entities with revenue and gross assets each below SGD 10 million and fewer than 50 employees may use the simplified SFRS for Small Entities framework. All financial statements must be filed with ACRA annually.