Introduction

In FY2024/25, IRAS recovered S$507 million in penalties — most of it from avoidable errors in tax computation and filing.

Tax computation in Singapore is the annual process of calculating chargeable income from accounting profit or loss and submitting the result to the Inland Revenue Authority of Singapore (IRAS). It goes beyond applying the flat 17% corporate rate: it requires a detailed reconciliation that adjusts accounting figures to match IRAS-prescribed taxable income.

This guide is written for companies incorporated in Singapore, foreign businesses operating here (including those from the USA, UK, Australia, and Europe), and individuals earning Singapore-sourced income. Getting this right matters for three concrete reasons:

- Statutory compliance with the Income Tax Act 1947

- Accurate financial planning based on true tax liability, not estimated profit

- Penalty avoidance — IRAS enforcement is active and well-funded

This guide covers how tax computation works step-by-step under Singapore's single-tier system, the key adjustments involved, filing deadlines, and the most common mistakes that trigger IRAS scrutiny.

Key Takeaways

- Singapore's 17% corporate tax rate applies to chargeable income, calculated after IRAS-approved adjustments to net profit.

- Tax computation requires adding back non-deductible expenses, deducting exempt income and capital allowances, then applying reliefs.

- Companies must file Estimated Chargeable Income (ECI) within 3 months of their financial year-end, followed by annual returns by 30 November.

- Resident individuals face progressive rates from 0% to 24%; non-residents are taxed at 24% (15% concession for employment income).

- Late filings and misclassified expenses both trigger IRAS penalties and increased audit risk.

What Is Tax Computation in Singapore?

A tax computation is a formal statement that reconciles a company's or individual's accounting profit or loss with the amount chargeable to income tax under Singapore's Income Tax Act. It is not the same as a company's profit and loss account. While your financial statements reflect commercial performance according to accounting standards, the tax computation translates this figure into IRAS's definition of taxable income.

The goal is an accurate "chargeable income" figure — only the income IRAS considers taxable. This means removing exempt income, disallowing non-deductible expenses, and applying allowable deductions so the right amount of tax is paid.

Tax computation vs. related concepts:

- Bookkeeping and financial statements follow accounting standards (FRS, IFRS) and record all commercial transactions.

- ECI filing is an estimate submitted earlier in the tax cycle, before finalised accounts are available.

- Tax computation is the detailed supporting document that underpins the final income tax return and must be prepared even when not filed alongside the return.

IRAS defines it directly: a tax computation is "a statement showing the tax adjustments to the accounting profit to arrive at the income that is chargeable to tax." Companies filing Form C must submit their tax computation with their return. Those filing Form C-S or Form C-S Lite must prepare and retain it for IRAS inspection.

How Tax Computation Works in Singapore

Singapore's corporate tax computation follows a structured sequence: start with accounting profit, adjust for non-deductible expenses and non-taxable income, apply capital allowances and exemptions, then apply the 17% rate to the resulting chargeable income.

Singapore operates a single-tier corporate tax system, meaning profits are taxed once at the company level and dividends distributed to shareholders are exempt from further tax. This eliminates double taxation — so getting the chargeable income figure right is everything.

Step 1: Start with Accounting Profit or Loss

The starting point is the company's net profit or loss before tax as shown in audited or unaudited financial statements for the relevant basis period. The basis period is generally the 12-month financial year preceding the Year of Assessment (YA). For example, profits earned in FY2024 are assessed to tax in YA 2025.

If a company changes its financial year-end and creates a period exceeding 12 months, profits may need to be apportioned across two YAs using direct identification or time apportionment methods.

Step 2: Apply Tax Adjustments to Accounting Profit

Add back non-deductible expenses included in accounting profit:

- Fines and penalties

- Private and personal expenditure

- Non-business-related costs

- Accounting depreciation (replaced by capital allowances)

- Provisions that have not crystallised

Deduct income that is not taxable or assessed separately:

- Certain foreign-sourced income meeting Section 13(8) qualifying conditions

- One-tier exempt dividends

- Capital gains (Singapore does not impose capital gains tax on fixed asset disposals that are capital in nature)

IRAS also permits capital allowances on qualifying plant and machinery to replace accounting depreciation. Section 14N deductions for qualifying renovation and refurbishment expenditure — capped at S$300,000 per three consecutive years — may also apply at this stage.

Step 3: Apply Exemptions and Arrive at Chargeable Income

Once adjusted profit is calculated, companies deduct:

- Unutilised capital allowances, trade losses, and donations carried forward from prior YAs (subject to shareholding continuity tests)

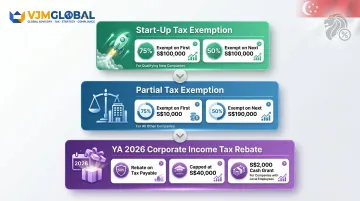

- Start-up tax exemptions (75% on first S$100,000 and 50% on next S$100,000 for qualifying new companies)

- Partial tax exemptions (75% on first S$10,000 and 50% on next S$190,000 for all other companies)

The remaining figure is the chargeable income, taxed at the flat 17% corporate rate. For YA 2026, additional relief applies:

- CIT Rebate: 50% of tax payable, capped at S$40,000

- CIT Rebate Cash Grant: S$2,000 for companies with at least one local employee

Key Tax Adjustments That Shape Your Chargeable Income

Non-Deductible (Disallowable) Expenses

IRAS requires that deductible expenses be "wholly and exclusively incurred in the production of income," be revenue (not capital) in nature, and not be prohibited under Section 15(1) of the Income Tax Act.

Common non-deductible items include:

- Fines and penalties (Section 15(1)(b)) – regulatory fines, traffic fines, late payment penalties

- Private and personal expenses (Section 15(1)(a)) – personal portion of mixed-use items

- Capital expenditure (Section 15(1)(c)) – claim capital allowances instead

- Accounting depreciation – replaced by IRAS capital allowances

- Provisions and unrealised losses – unless crystallised

- Private motor vehicle expenses – S-plated, Q-plated, RU-plated cars

- Income tax payments – corporate and personal tax

- Donations – claimed separately at 250% if to approved IPCs

Adding these back increases taxable income. Companies that fail to add back disallowable expenses risk IRAS assessment adjustments and penalties.

Exempt and Non-Taxable Income

Singapore does not impose capital gains tax. Gains from the disposal of fixed assets, shares, or financial instruments that are capital in nature are not taxable. However, gains from "trading" activities are revenue in nature and fully taxable.

Foreign-sourced income (dividends, branch profits, service income) remitted to Singapore is exempt under Section 13(8) if:

- The headline tax rate of the foreign jurisdiction is at least 15%

- The income has been subjected to tax in the foreign jurisdiction

- IRAS is satisfied the exemption is beneficial

Deducting exempt income from accounting profit reduces chargeable income.

Enhanced and Further Deductions

Singapore offers generous enhanced deductions to encourage specific business activities:

| Scheme | Deduction Rate | Cap/Period |

|---|---|---|

| R&D (Sections 14C/14D) – Singapore-based | 100% base + 300% additional on first S$400K; 150% on balance | YA 2024-2028 |

| Donations to approved IPCs | 250% of qualifying donation | Extended to 31 Dec 2026 |

| DTDi (Internationalisation) | 200% on eligible overseas expansion expenses | Qualifying expenses: 1 Jul 2015 – 31 Dec 2030 |

| Enterprise Innovation Scheme (EIS) | 20% cash payout (in lieu of deductions) | Up to S$100K expenditure = max S$20K payout per YA |

R&D enhanced deductions apply to staff costs (excluding directors' fees) and consumables. For outsourced R&D, the additional deduction applies to 60% of the fee paid. IRAS adjusted approximately 6% of SME R&D claims on review — claims that lacked adequate records of qualifying activities, staff time allocation, or consumable costs.

Capital Allowances: Replacing Depreciation

Accounting depreciation is not tax-deductible in Singapore. Instead, companies claim capital allowances on qualifying plant and machinery:

| Method | Write-Off Rate | Conditions |

|---|---|---|

| Prescribed working life (Section 19) | IA = 20% of cost; AA = 80% / working life | Election of 6, 12, or 16 years |

| 3-year write-off (Section 19A(1)) | 33.33% per year | All qualifying plant and machinery |

| 1-year write-off (Section 19A(2)/(10A)) | 100% in year 1 | Computers, automation equipment, low-value assets (cost ≤ S$5,000, capped at S$30,000/YA) |

| 2-year accelerated (Section 19A(1E)) | 75% year 1, 25% year 2 | Assets acquired for YA 2021, 2022, 2024 |

Non-qualifying items include S-plated private cars, Q-plated and RU-plated business cars, structural items (walls, floors, fixed partitions), and infrastructure (pipings, manholes).

When an asset is disposed of, a balancing adjustment arises: a Balancing Allowance (deductible) if Tax Written Down Value (TWDV) exceeds sale proceeds, or a Balancing Charge (taxable) if sale proceeds exceed TWDV.

Unutilised Items: Carry-Forward and Carry-Back

Unutilised capital allowances and trade losses can be carried forward indefinitely. Unutilised donations can be carried forward for up to 5 YAs. Loss carry-back relief allows up to S$100,000 of current-year unutilised capital allowances and trade losses to be carried back to the immediate preceding YA.

The shareholding continuity test requires that more than 50% of shares be held by the same shareholders at the relevant comparison dates. This test applies to carry-forward, carry-back, and group relief of unutilised items. Equity transactions (fundraising rounds, share transfers, restructurings) can extinguish accumulated tax losses if this test is not maintained.

Filing Your Corporate Tax Return with IRAS

Two-Stage Filing Obligation

Singapore companies face a dual filing requirement:

- Estimated Chargeable Income (ECI) – due within 3 months of financial year-end

- Annual income tax return – due by 30 November of the relevant Year of Assessment

ECI is an estimate of the company's chargeable income for the basis period, filed before finalised accounts are available. Companies that file ECI early and are on GIRO receive instalment benefits:

- 10 monthly instalments if filed within 1 month of FYE

- 8 instalments if filed within 2 months

- 6 instalments if filed within 3 months

A company qualifies for ECI waiver if both conditions are met:

- Annual revenue is S$5 million or below

- ECI is nil (calculated before deducting partial or start-up exemptions)

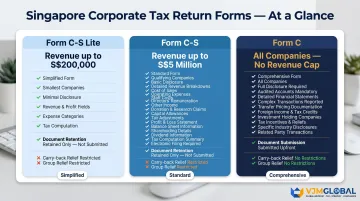

Form C, Form C-S, and Form C-S Lite

| Feature | Form C-S (Lite) | Form C-S | Form C |

|---|---|---|---|

| Revenue threshold | Up to S$200,000 | Up to S$5 million | All companies |

| Incorporation | Singapore only | Singapore only | Any |

| Fields required | 6 essential | 18 fields | Full disclosure |

| Documents submitted | Not required (retain for IRAS) | Not required (retain for IRAS) | Required |

| Restrictions | Cannot claim carry-back, group relief, investment allowance, FTC | Same restrictions | No restrictions |

Form C is the full return requiring submission of financial statements, tax computation, and supporting schedules. It is mandatory for companies deriving income at concessionary tax rates (tax incentives) and companies not meeting Form C-S criteria.

Form C-S is a simplified return for companies meeting qualifying criteria (revenue up to S$5 million). Supporting documents are not submitted upfront but must be prepared and retained for IRAS inspection.

Form C-S Lite is the most streamlined option for eligible smaller companies (revenue up to S$200,000). Only 6 essential fields are required. Approximately 88% of Singapore companies qualify for simplified filing.

Filing is mandatory by 30 November even if the company is dormant or loss-making.

Individual Income Tax Filing

Resident individuals file via the myTax Portal, with income taxed on a progressive scale from 0% to 24% (from YA 2024 onwards) after personal reliefs and deductions. Non-resident individuals are taxed at a flat 24%, with a 15% concession for employment income (whichever is higher). The e-filing deadline for individuals is 18 April of the Year of Assessment.

Foreign Companies and Multinational Complexity

Foreign companies and multinational groups operating in Singapore face additional compliance layers:

- Transfer pricing documentation – IRAS requires documentation prepared at the time of each transaction to demonstrate related-party dealings are conducted at arm's length. The reporting threshold is S$15 million, with a lower S$1 million threshold for specific transaction types. IRAS released the 8th edition of its Transfer Pricing Guidelines in November 2025.

- Functional currency translation – Financial statements prepared in non-SGD currencies must follow IRAS translation rules to ensure accurate chargeable income determination.

- Pillar 2 top-up tax obligations – Multinationals with consolidated revenue exceeding €750 million must prepare for OECD Pillar 2 reporting, which imposes a 15% global minimum tax rate.

For foreign companies navigating these requirements, professional advisory support can help manage documentation, translation compliance, and Pillar 2 obligations accurately. VJM Global's cross-border tax team assists multinational clients with transfer pricing documentation and international tax structuring across jurisdictions.

Common Mistakes and Misconceptions in Singapore Tax Computation

Assuming Net Profit Equals Chargeable Income

The most common misunderstanding among businesses is assuming that net accounting profit equals chargeable income and applying the 17% rate directly to financial profit. That assumption is wrong. The gap between accounting profit and chargeable income is precisely where most errors occur — and where most tax planning value resides.

When IRAS identifies this discrepancy during an audit, companies face assessment adjustments, penalties, and potential prosecution. In FY2024/25, IRAS audited over 8,600 cases and recovered S$507 million in taxes and penalties.

Misclassifying Expenses

Companies risk two types of expense classification errors:

- Failing to add back non-deductible items (understating taxable income) – depreciation, private car costs, uncrystallised provisions, personal expenses

- Incorrectly treating allowable expenses as disallowable (overstating taxable income and overpaying tax)

Documented, consistent classification is essential — IRAS penalties vary significantly based on intent:

| Scenario | Max Tax Penalty | Max Fine | Max Imprisonment |

|---|---|---|---|

| Error without intent to evade | 200% of tax undercharged | S$5,000 | 3 years |

| Wilful evasion | 400% of tax undercharged | S$50,000 | 5 years |

Assuming Loss-Making Companies Don't File

Under Singapore law, filing obligations apply regardless of profitability. Dormant companies and loss-making companies must still file by 30 November. Unutilised losses can only be carried forward or carried back if the company has met its filing requirements and maintained proper records.

Failure to file for 2 or more years triggers penalties of twice the tax assessed and fines up to S$5,000. Beyond fines, IRAS may also:

- Issue estimated Notices of Assessment

- Offer to compound the offence

- Issue Section 65B(3) notices to directors

- Pursue court summons

Frequently Asked Questions

How is tax computed in Singapore?

Singapore companies start with their accounting net profit or loss, then apply IRAS-prescribed adjustments — adding back non-deductible expenses, deducting exempt income, and applying capital allowances. The 17% corporate tax rate is applied to the resulting chargeable income. Individuals face progressive rates from 0% to 24% after personal reliefs.

What is a tax computation report?

A tax computation report is a formal statement that reconciles a company's accounting profit with its chargeable income for IRAS purposes, showing each adjustment made. It is a mandatory supporting document for Form C filers and must be retained by all companies even when not submitted with Form C-S or Form C-S Lite.

How to get income tax computation?

Companies have three preparation options: IRAS's free Basic Corporate Income Tax (BTC) Calculator (an Excel workbook on the IRAS website), a professional tax adviser, or compliant accounting software. The computation must be completed before filing the annual income tax return.

What is the corporate tax rate in Singapore?

Singapore's prevailing corporate income tax rate is 17% applied to chargeable income. New start-up companies and smaller companies may qualify for partial or full tax exemptions that reduce the effective rate on qualifying income bands—up to S$125,000 exemption for start-ups over three years.

What is the difference between Form C, Form C-S, and Form C-S Lite?

The three forms differ by revenue threshold: Form C is the full return (any revenue), Form C-S applies to companies below S$5 million, and Form C-S Lite covers companies up to S$200,000. All three require the underlying tax computation to be prepared, even when supporting documents aren't filed upfront.

What are the consequences of late or incorrect tax filing in Singapore?

IRAS imposes a 5% late payment penalty if full payment is not received within 1 month of the Notice of Assessment, plus 1% per month up to a 12% maximum. Persistent non-compliance can escalate to court summons or director notices. Companies that self-correct through the Voluntary Disclosure Programme before an audit is initiated face 0% penalty within the first year.