That time has a price. Every hour a founder or manager spends reconciling accounts is an hour not spent on customers, strategy, or revenue.

Outsourcing bookkeeping isn't a cost-cutting shortcut. Done right, it's a structural decision that improves financial accuracy, protects against IRS penalties, scales with business growth, and puts leadership attention back where it belongs. This article breaks down the key reasons US businesses choose to outsource—and what measurable outcomes they can realistically expect.

Key Takeaways

- Cuts the real cost of in-house bookkeeping — salary, benefits, software, and turnover included

- Gives you CPA-level expertise and current IRS knowledge without relying on a single generalist

- Team-based delivery means no disruption when staff changes—your books stay current regardless

- Accurate, timely financials enable better decisions on pricing, hiring, and growth investment

- Scales with your business as transaction volume and compliance complexity increase

What Is Outsourced Bookkeeping?

Outsourced bookkeeping means delegating your day-to-day financial record-keeping to an external accounting firm or specialist team rather than managing it with in-house staff. The scope typically includes:

- Transaction recording — capturing every sale, expense, and payment accurately

- Bank and credit card reconciliation — matching records to statements to catch discrepancies

- Accounts payable and receivable — managing what you owe and what you're owed

- Payroll support — processing pay runs, tax withholdings, and compliance filings

- Financial statement preparation — producing the P&L, balance sheet, and cash flow reports your business actually needs

These services aren't exclusive to large corporations. US startups, mid-sized businesses, and established enterprises across retail, healthcare, professional services, and e-commerce all rely on outsourced bookkeeping — because leadership wants accurate financial data without hiring and managing a full internal finance team.

VJM Global, for example, handles everything from daily transaction syncing in QuickBooks and Xero to multi-state sales tax compliance and year-end financial reporting for US clients.

Key Advantages of Outsourcing Bookkeeping for US Businesses

The advantages below are grounded in operational and financial outcomes US business owners track—cost, accuracy, compliance, and growth capacity. Each one connects directly to measurable business results.

Advantage 1: Significant Cost Reduction Compared to In-House Bookkeeping

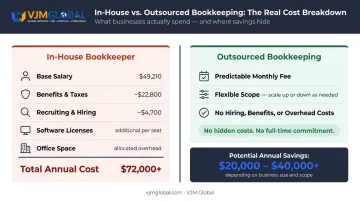

The salary on a job posting is the smallest part of what an in-house bookkeeper actually costs. The Bureau of Labor Statistics reports the median annual wage for bookkeeping, accounting, and auditing clerks at $49,210 as of May 2024. But wages are only part of the picture.

Applying BLS employer compensation data for office and administrative roles—where total compensation averages $36.20 per hour against $24.61 in wages—the salary-plus-benefits equivalent for a median bookkeeper exceeds $72,000 annually. That's before recruiting costs, software licenses, onboarding, ongoing training, or the physical office space to put them in.

SHRM puts the average cost per hire at nearly $4,700—and that's just to get someone in the seat.

Outsourcing restructures this entirely:

- Predictable monthly fee instead of variable employment costs

- Shared infrastructure — providers spread software and training costs across many clients, so you get enterprise-grade capability without enterprise-grade spend

- Adjustable scope — during seasonal slowdowns or business contractions, outsourced services flex down while in-house staff remain a fixed cost regardless of workload

The budget freed from payroll overhead can fund marketing, product development, or revenue-generating hires—areas that directly move the business forward.

Best fit for:

- Businesses with revenue under $5M where finance headcount decisions are premature

- Companies in retail, hospitality, or seasonal industries with fluctuating transaction volumes

- Businesses scaling rapidly where adding full-time finance staff would outpace actual need

KPIs affected: Total bookkeeping cost as a percentage of revenue, overhead cost per transaction, employee turnover cost in the finance function, annual software spend

Advantage 2: Access to Specialized Expertise and US Tax/Compliance Knowledge

A single in-house bookkeeper—even a good one—carries a knowledge ceiling. They know what they've encountered before. An outsourced team works across dozens of clients and industries simultaneously, which means they encounter compliance scenarios, IRS rule changes, and multi-state tax requirements frequently enough to develop genuine expertise.

For US businesses, the compliance stakes are concrete:

- IRS failure-to-file penalty: up to 5% of unpaid tax per month, capped at 25%

- Failure-to-deposit payroll taxes: 2% for deposits 1–5 days late, escalating to 15% after IRS notice

- Incorrect 1099 filings: up to $340 per return if not corrected by August 1; $680 for intentional disregard

- Multi-state sales tax exposure: CPA.com identifies over 13,000 tax jurisdictions in the US post-Wayfair—a compliance landscape no generalist bookkeeper can navigate alone

The 2024 NFIB Tax Survey found 88% of small business owners who use a tax professional do so because tax laws are too complex to handle themselves. The complexity isn't theoretical—it shows up in penalties, missed deductions, and year-end cleanup costs.

VJM Global's team of CPAs, Chartered Accountants, and US-compliant finance professionals brings 30+ years of experience to this challenge. Having served 500+ American business owners across 15+ industries, the team stays current on IRS regulations, GAAP standards, state income tax rules, and payroll compliance requirements—including multi-state severance tax filings across Texas, Oklahoma, and North Dakota.

When books are accurate and reviewed by qualified professionals, the downstream benefits compound:

- Tax penalties drop because filings are correct and on time

- Year-end reconciliation requires far less costly cleanup work

- Business owners can trust their financial reports when making pricing, hiring, and investment decisions

Who benefits most:

- Businesses operating across multiple US states

- Companies preparing for investor due diligence or SBA financing

- Businesses in regulated industries or those that have grown faster than their internal finance capability

KPIs affected: Bookkeeping error rate, tax penalty incidence, time spent on year-end adjustments, audit readiness, frequency of restatements

Advantage 3: Scalability, Business Continuity, and Reclaimed Leadership Focus

This advantage bundles three operational benefits that reinforce each other in practice.

Scalability without a hiring cycle

When transaction volume increases, a new business entity is added, or payroll expands to a new state, an outsourced team absorbs that complexity without a months-long hiring and training process. Services scale up or down as the business requires—no headcount decisions, no onboarding delays.

Continuity without depending on a single person

An in-house bookkeeper is a single person your books depend on entirely. Their sick day, resignation, or family leave can leave your books untouched for weeks while you recruit, hire, and retrain. An outsourced team operates with multiple people familiar with your account—VJM Global's model assigns dedicated account teams with a designated manager, so institutional knowledge stays with the engagement, not any individual.

BLS data projects employment of bookkeeping clerks to decline 6% through 2034, meaning the talent pool is tightening even as complexity grows. Outsourcing avoids that constraint entirely.

Leadership time recovered

A 2024 Intuit QuickBooks survey found businesses with 10–99 employees spend an average of **25 hours per week on manual data entry and reconciliation**. That's more than half a full-time role absorbed by financial admin. When business owners stop being the fallback for bookkeeping tasks, those hours redirect to the activities that actually grow the business.

The fraud risk angle

There's one more factor that rarely gets discussed: small businesses are disproportionately exposed to internal fraud. The ACFE's 2024 Report to the Nations found organizations with fewer than 100 employees had a median fraud loss of $141,000, and lack of internal controls was the primary contributing factor in 32% of occupational fraud cases.

When more than one person reviews transactions—standard in any outsourced team structure—the checks-and-balances mechanism reduces both the opportunity for fraud and the risk of undetected errors accumulating over time.

What to measure: Leadership hours recovered per month, service continuity rate, time-to-onboard new financial complexity, internal fraud incident rate

What Happens When Bookkeeping Is Handled Without the Right Support

Under-resourced bookkeeping doesn't announce itself — it shows up in penalties, rejected loan applications, and year-end cleanup bills. Here's what US businesses commonly run into:

- Inaccurate financial reports that lead to poor cash flow decisions and missed tax planning windows—because the numbers can't be trusted at the moment they're needed

- Compounding errors that become expensive at year-end — CPA firms charge billable hours just to untangle records before any advisory work can start

- Compliance failures—missed payroll tax deposits, incorrect 1099 filings, or sales tax miscalculations—that trigger IRS penalties or state audits

- Single point of failure in the finance function: no backup, no oversight, and no continuity when that person leaves

- Financing obstacles: disorganized or inaccurate financial statements that can't withstand lender or investor scrutiny, blocking access to SBA loans and growth capital

The 2024 U.S. Chamber survey found 51% of small business owners say navigating regulatory compliance negatively impacts their ability to grow. Bookkeeping is where that compliance burden either gets managed proactively or quietly grows into a larger operational problem.

How to Get Maximum Value from Outsourced Bookkeeping

Outsourcing delivers its full benefit only when treated as an ongoing partnership, not a one-time fix. Three conditions determine whether you extract full value:

1. Start with clean data and clear documentation

Provide organized historical records and document your current processes before transitioning. This reduces onboarding time, prevents gaps in the financial record, and lets the external team get to productive work faster. Businesses that hand over disorganized records create cleanup work that delays—and sometimes increases—the cost of the engagement.

2. Set your reporting cadence before day one

Establish monthly financial reviews, regular touchpoints for cash flow and tax position, and escalation protocols for time-sensitive compliance items. VJM Global builds client communication around consistent updates, dedicated account management, and responsiveness during US business hours.

This structure keeps both sides aligned and stops problems from surfacing only at quarter-end.

3. Act on the financial data produced

Outsourced bookkeeping only creates value if the insights it produces change decisions. Monthly financial statements should drive how you run the business — not wait in a folder until tax season. Put them to work by:

- Assessing whether your pricing covers actual costs

- Catching cost overruns before they compound

- Evaluating hiring or vendor decisions with real numbers

- Planning ahead for quarterly tax obligations

Conclusion

For US businesses managing cost pressure, compliance complexity, and growth simultaneously, outsourced bookkeeping delivers control and financial clarity that's difficult to replicate with a single in-house generalist—at lower total cost and with less operational risk.

The benefits compound over time. Accurate books feed better reporting, which sharpens decision-making and accelerates growth. Businesses that treat outsourced bookkeeping as ongoing financial infrastructure — not a temporary fix — build a foundation that holds up under investor scrutiny, IRS examination, and rapid scaling alike.

That foundation is worth building on solid ground. VJM Global's accounting professionals — with 30+ years of experience and 500+ US businesses served — offer a direct consultation to assess your current bookkeeping setup and identify where it can be stronger.

Frequently Asked Questions

Why should you outsource your bookkeeping?

Outsourcing gives US businesses access to CPA-level expertise, reduces the true all-in cost of financial record-keeping, and ensures compliance with IRS and state tax requirements. It also frees up the leadership time that in-house or DIY bookkeeping consumes—time better directed toward running and growing the business.

How much does outsourced bookkeeping cost for a US business?

Pricing depends on transaction volume, service scope, and complexity — Forbes Advisor cites starting prices ranging from $49 to $1,750 per month. Outsourcing typically costs less than the all-in expense of an in-house bookkeeper once salary, benefits, software, and hiring are factored in.

What tasks does an outsourced bookkeeper handle?

Most providers cover the full range of day-to-day and reporting tasks:

- Transaction recording and bank/credit card reconciliation

- Accounts payable and receivable management

- Payroll processing and financial statement preparation

- Tax filing support, including multi-state sales tax compliance

Is outsourced bookkeeping safe for sensitive financial data?

Reputable providers use bank-grade encryption, strict access controls, and established security frameworks. VJM Global, for example, holds ISO 27001 certification and follows SOC 2-compliant protocols. Before engaging any provider, verify their security certifications, data protection policies, and confidentiality agreements.

How is outsourced bookkeeping different from hiring in-house?

Outsourcing provides a team with layered expertise and CPA oversight rather than a single generalist. It eliminates fixed employment costs, ensures service continuity when staff changes occur, and scales with business growth without a new hiring cycle.

When is the right time to outsource bookkeeping?

Consider outsourcing when bookkeeping is consuming excessive leadership time, your growth has outpaced internal finance capacity, or your financials can't hold up to investor or lender scrutiny. A departing in-house finance team member is also a natural trigger to reassess.