Setting up a legal entity in India—whether a Private Limited Company or Branch Office—involves months of registrations, upfront costs, and ongoing expertise in navigating EPF, ESI, TDS, and the newly implemented Labour Codes. For many UK businesses testing the market, scaling quickly, or hiring small teams, this timeline and commitment don't make commercial sense.

This guide explains what an Employer of Record in India does, why it matters specifically for UK businesses, how the process works step by step, and what India-specific compliance factors UK employers must understand before engaging an EOR provider.

Key Takeaways

- An EOR in India legally employs your staff, managing payroll, taxes, and compliance whilst you direct the work

- Setup takes days rather than months, with no Indian legal entity required on your end

- Statutory costs include EPF (12% employer), ESI (3.25%), gratuity, and state-specific minimum wages

- Using an EOR reduces permanent establishment risk under the India-UK Double Taxation Treaty

- Most cost-effective for UK businesses hiring fewer than 15-20 employees in India

What Is an Employer of Record in India?

An Employer of Record in India is a locally incorporated third-party entity that legally employs workers on behalf of a foreign company, assuming all legal, tax, and administrative obligations whilst the client company directs day-to-day work.

In practice, the EOR takes on the full employment burden so you don't have to. That includes:

- Drafting and managing employment contracts under Indian law

- Registering employees for statutory schemes (EPF, ESI)

- Calculating and remitting monthly TDS

- Administering mandatory benefits and leave entitlements

- Assuming liability for wrongful dismissal or payroll errors

For UK companies, this means immediate access to Indian talent without dealing directly with India's labour laws, tax registrations, and statutory compliance requirements.

How EOR differs from related models:

- PEO (Professional Employer Organisation): Co-employs workers alongside your existing local entity. An EOR, by contrast, is the sole legal employer — no Indian entity required on your side

- Contractor arrangement: Contractors lack employee status and statutory protections. Misclassification exposes both parties to back-pay claims and unpaid contributions — EOR establishes true employment status with full rights under Indian labour law

Why UK Companies Are Turning to EOR in India

Access to a 616 Million-Strong Workforce

India's working-age population reached 61.6 crore (616 million) in 2025, with a Labour Force Participation Rate of 59.3% and unemployment among educated workers (secondary education and above) at just 6.5%, according to India's Periodic Labour Force Survey. For UK businesses, two figures stand out: 91% of Indian employers report that competitive roles demand English proficiency (vs. 81% globally), and India holds a 30% share of the global Engineering R&D outsourcing market, projected to reach 50% within a decade.

The UK-India FTA Strengthens Bilateral Ties

The UK-India Free Trade Agreement, concluded 6 May 2025 and signed 24 July 2025, is projected to increase bilateral trade by £25.5 billion and boost UK GDP by £4.8 billion annually. India will eliminate tariffs on 90% of product lines; the UK on 99% of Indian exports. The FTA is widely regarded as the UK's most significant trade deal since Brexit.

UK-India bilateral trade already totalled £47.4 billion in the four quarters to Q3 2025 — up 11.7% year-on-year. The UK is India's 6th largest investor with USD 36 billion in cumulative investment, whilst around 1,000 Indian companies now operate in the UK.

Substantial Salary Arbitrage

UK software engineers earn £40,000–110,000+ annually depending on experience, whilst comparable Indian roles command INR 5–25 lakh (approximately £4,700–29,500), according to PlugScale's 2026 Tech Compensation Benchmark. That translates to 60–80% cost savings on technology roles — savings that EOR makes accessible without triggering permanent establishment risk in India.

Mitigating Permanent Establishment Risk

Under the India-UK Double Taxation Avoidance Agreement (DTAA), Article 5(2)(k), two PE triggers are most relevant for UK companies:

- Service PE: Personnel providing services in India for 90+ days within any 12-month period

- Agency PE: A dependent agent habitually concluding contracts on behalf of the foreign enterprise

When UK employees regularly direct Indian operations or sign contracts locally, Indian tax authorities may treat a taxable permanent establishment as existing — creating Indian corporate tax obligations. An EOR mitigates this by holding the employment relationship within its own Indian entity, keeping UK personnel out of contract-concluding roles.

Speed and Cost vs. Entity Setup

Registering a Private Limited Company in India involves:

- Incorporation timeline: 10-20 days

- Post-incorporation registrations: EPFO, ESIC, GST (additional weeks)

- Incorporation cost: INR 5,100-25,000+ for stamp duty, DSC, and MCA fees

- Ongoing annual compliance: Approximately USD 1,700/year

Sources: TheNewsMinute, Healy Consultants

An EOR removes all of this overhead, charging a flat per-employee monthly fee (typically USD 199–1,200 depending on provider). For UK businesses running a pilot hire, building a small remote team, or needing someone operational within days, that's a meaningful difference.

VJM Global has guided over 250 UK businesses through India market entry — advising on when EOR is the right first step and when a permanent entity makes more strategic sense, particularly in fintech, ed-tech, gaming, and technology sectors.

How EOR Works in India: A Step-by-Step Process for UK Businesses

Once a UK company selects an EOR provider, the EOR uses its own registered Indian entity to onboard, employ, and pay your Indian staff. You retain operational control whilst the EOR handles all legal employer obligations and compliance responsibilities.

Step 1: Candidate Selection and Role Definition

The UK company identifies the candidate and defines role, salary, and working conditions. The EOR reviews proposed terms against Indian statutory minimums:

- State-specific minimum wage (rates vary by state, skill classification, and industry)

- Probation period limits (capped at 6 months)

- Notice period norms (minimum 30 days standard)

The EOR flags any non-compliant elements before issuing the offer, ensuring the employment contract meets Indian legal requirements.

Step 2: Employment Contract and Onboarding

The EOR generates a written employment contract under Indian law covering:

- Job title and reporting structure

- Compensation structure (basic salary, allowances, variable components)

- Probation period and confirmation terms

- Leave entitlements (earned leave, casual/sick leave)

- IP assignment and confidentiality

- Notice requirements and termination clauses

Documents required from the new employee:

- PAN card (permanent account number)

- Bank account details for INR salary payments

- EPF Universal Account Number (UAN)

- Identity and address proof

The EOR completes statutory registrations with EPFO and ESIC on behalf of the employee. Once registrations are in place, the EOR moves into ongoing payroll and compliance management.

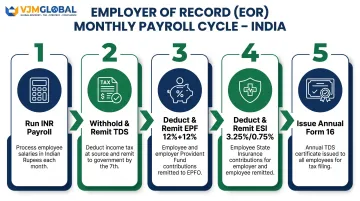

Step 3: Payroll, Tax, and Ongoing Compliance

Each month, the EOR:

- Runs payroll in Indian Rupees

- Withholds TDS (Tax Deducted at Source) under the Income Tax Act 1961, remitted by the 7th of the following month (30th April for March)

- Deducts and remits EPF contributions: 12% employer + 12% employee of basic salary

- Deducts and remits ESI contributions where applicable: 3.25% employer / 0.75% employee for employees earning under INR 21,000/month

- Issues Form 16 annually (TDS certificate)

The UK parent company pays the EOR a consolidated invoice covering:

- Gross salary

- Statutory on-costs (EPF, ESI, gratuity accrual, bonus)

- EOR management fee

This single monthly invoice removes the complexity of multi-line Indian payroll administration — no separate statutory filings, no local bank accounts, no in-country payroll team required.

India Compliance Requirements Every UK Employer Must Know

India's Layered Labour Law Structure

Employment obligations are governed by both central legislation and state-specific laws. The four Labour Codes (notified as effective law 21 November 2025) replaced 29 earlier central laws:

- Code on Wages, 2019

- Industrial Relations Code, 2020

- Code on Social Security, 2020

- Occupational Safety, Health and Working Conditions Code, 2020

Central rules remain in draft form (published 30 December 2025; finalisation expected April 2026). State-level implementation varies—states such as Madhya Pradesh, Uttar Pradesh, Gujarat, Karnataka, and Haryana have notified final rules, whilst Maharashtra, Tamil Nadu, and Kerala have published draft rules only.

UK employers accustomed to a single national framework should expect a layered system where both the central code and the relevant state rules apply simultaneously to each employee.

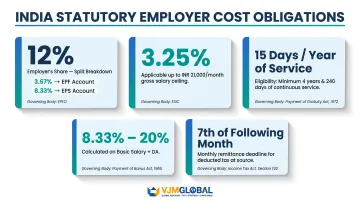

Key Statutory Employer Costs

| Obligation | Rate / Threshold | Authority |

|---|---|---|

| EPF - Employer contribution | 12% (split: EPF 3.67% + EPS 8.33% + EDLI 0.5%) | EPFO |

| EPF - Employee contribution | 12% of basic + DA | EPFO |

| EPF wage ceiling | INR 15,000/month (not applicable to International Workers) | EPFO |

| ESI - Employer contribution | 3.25% of wages | ESIC |

| ESI - Employee contribution | 0.75% of wages | ESIC |

| ESI wage ceiling | INR 21,000/month (INR 25,000 for PWD) | ESIC |

| Gratuity | 15 days' wages per year of service (payable after 4 years 240 days) | Payment of Gratuity Act 1972 |

| Statutory bonus | 8.33–20% of basic + DA (employees working 30+ days) | Payment of Bonus Act 1965 |

| TDS remittance | 7th of following month (30th April for March) | Income Tax Act 1961 |

Sources: EPFO Contribution Rate PDF, ESIC Coverage

Minimum Wage Complexity

India has no single national minimum wage. The Code on Wages 2019 establishes a "national floor wage" concept, but the specific rate remains pending notification. Rates are set state-by-state and vary by:

- Skill classification (unskilled, semi-skilled, skilled)

- Industry sector

- Geographic zone

A UK employer must ensure the EOR tracks the relevant state rate for each employee's location. Violations carry financial penalties.

Leave and Working Hours Entitlements

- Standard working hours: 8–9 hours per day, 48 hours per week

- Earned leave: 15–18 days per year (varies by state)

- Sick/casual leave: Varies by state and employer policy

- Public holidays: 3 national holidays mandatory for all employers; state public holidays vary

- Maternity leave: 26 weeks fully paid for the first two children, 12 weeks for subsequent children (Maternity Benefit Amendment Act 2017)

- Overtime: 2x wages for hours worked beyond the standard limit

These entitlements feed directly into termination obligations — unused earned leave, for instance, must be encashed on exit.

Termination Obligations UK Employers Must Understand

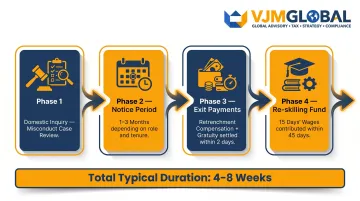

Under the Industrial Relations Code 2020 (effective 21 November 2025):

- Notice period: 1 month standard; 3 months for factories/mines with 300+ workers

- Retrenchment compensation: 15 days' average pay per completed year of service (or part exceeding 6 months)

- Worker Re-skilling Fund: Employer contributes 15 days' last drawn wages within 45 days of retrenchment

- Exit wages: Must be paid within 2 working days of exit

- Gratuity: Payable after 1 year of continuous service for fixed-term employees (Code on Social Security 2020)

- Wrongful dismissal: Industrial Tribunals may order reinstatement or impose penalties of INR 50,000 to INR 20,00,000

Dismissal based on caste, gender, maternity, or whistleblowing is explicitly illegal. A mandatory domestic inquiry is required for misconduct cases.

UK companies should not assume at-will termination norms apply here. Unlike UK practice, the domestic inquiry requirement and retrenchment compensation obligations mean terminations typically require 4–8 weeks of structured process — initiated well before the intended exit date.

EOR vs. Setting Up a Legal Entity in India

When EOR Is the Right Choice for UK Companies

EOR suits UK businesses that:

- Are hiring fewer than 10–15 employees

- Want to test the Indian market before committing to a permanent structure

- Need to hire within days rather than months

- Prefer to transfer compliance liability to a specialist provider

- Lack in-house expertise in Indian labour law

EOR is operationally faster, requires no upfront registration investment, and eliminates the need to build internal compliance infrastructure.

When a Permanent Entity Makes More Sense

A legal entity (Private Limited Company or Branch Office) becomes more cost-effective when:

- Headcount grows beyond 15-20 employees: Cumulative monthly EOR fees may exceed the cost of maintaining your own entity

- You need greater control over HR policy, company culture, and branding

- Your India operations involve sales, IP ownership, or regulatory licensing

- You're making a long-term strategic commitment to the Indian market

VJM Global has advised over 250 UK businesses on India market entry. The right choice depends on your operational scale, industry regulatory requirements, and long-term growth plans.

Comparison: EOR vs. Legal Entity

The table below summarises the key trade-offs at a glance.

| Factor | EOR | Private Limited Company |

|---|---|---|

| Setup timeline | Days (employee onboarding) | 10–20 days incorporation + weeks for post-registration |

| Upfront cost | None (management fee only) | INR 5,100–25,000+ |

| Compliance ownership | EOR manages all | Company must manage independently |

| Speed to first hire | Immediate | Weeks (post-registration) |

| Scalability | Cost per employee increases linearly | Fixed compliance cost spreads across headcount |

| Control | Limited (contractual relationship) | Full (direct employer-employee) |

| Annual compliance cost | Management fee per employee | Approx. £1,350/year ongoing |

Common Mistakes and Misconceptions About EOR in India

Misconception 1: "An EOR Removes All Compliance Responsibility from the UK Company"

Whilst the EOR assumes legal employer liability in India, the UK parent company retains several obligations:

- Transfer pricing compliance: Payments to Indian EOR providers must satisfy arm's length pricing under India's Income Tax Act 1961 (Sections 92-92F) and the UK's Corporation Tax Act 2010 (Part 4). Cost Plus benchmarking is standard for EOR and shared services arrangements.

- HMRC reporting: All compensation — wherever paid — must be reported for PAYE and NICs unless HMRC agrees a reduced basis. Benefits in kind require Form P11D. From April 2026, payroll reporting of all benefits becomes mandatory.

- Permanent establishment (PE) monitoring: If UK employees visit India and direct operations — or if Indian staff habitually conclude contracts on the UK entity's behalf — PE risk resurfaces regardless of the EOR arrangement.

Misconception 2: "All EOR Providers Offer the Same Level of Compliance in India"

Some EOR providers operate through third-party in-country partners rather than wholly owned entities. This introduces real risk:

- Inconsistent compliance standards

- Slower payroll processing

- Potential data security gaps

How to verify an Indian EOR provider:

Use India's Ministry of Corporate Affairs CIN lookup tool to check any Indian company's registration status. Every registered company receives a 21-digit alphanumeric CIN at incorporation — ask your provider whether they directly own their Indian entity, then confirm it yourself via this public database.

Misconception 3: "Hiring Through an EOR Is the Same as Hiring a Contractor in India"

Misclassifying an employee as a contractor in India exposes both parties to:

- Back-pay claims for unpaid statutory contributions

- Fines and penalties under Indian labour law

- Disputes over employment status that can escalate to litigation

EOR establishes genuine employment status with all associated rights and protections under Indian labour law. Contractor-of-record arrangements carry a different risk profile and are appropriate only for genuinely independent service relationships.

Frequently Asked Questions

What is an Employer of Record in India?

An EOR in India is a locally registered company that legally employs workers on behalf of a foreign business, handling employment contracts, payroll, TDS, EPF, ESI, and compliance under Indian law, whilst the foreign company manages day-to-day work direction.

What is the cost of EOR in India?

EOR costs cover the employee's gross salary, statutory on-costs (EPF, ESI, gratuity, bonus accrual), and a monthly management fee. Management fees typically range from approximately £160 to £950 per employee per month, with global platforms (Deel, Rippling) at the higher end and India-specialist providers at the lower end.

Is EOR legal in India?

Yes. EOR arrangements are entirely legal in India, operating under the Contract Labour (Regulation and Abolition) Act 1970, where the EOR functions as the "Contractor" and must hold a licence under Section 12. No legislation prohibits the model, provided the arrangement complies with applicable central and state labour laws.

Who can be an employer of record?

Any legally registered Indian company with the appropriate infrastructure to run payroll, administer statutory benefits, and comply with Indian labour law can act as an EOR. In practice, specialist global EOR platforms and India-focused business services firms fulfil this role for foreign companies.

What are the benefits of employer of record?

Core benefits include faster market entry without entity setup, full statutory compliance managed by the provider, reduced administrative burden for the UK HR team, access to India's 616 million-strong talent pool, and protection from misclassification and permanent establishment risk.