Introduction

US companies hiring in India face a compliance wall most don't see coming. Indian labor law requires a registered legal employer to run payroll, withhold TDS, and enroll workers in statutory schemes like Provident Fund (PF) and Employees' State Insurance (ESI). A US company cannot do any of this from abroad — not without either incorporating a local entity or working through an Employer of Record.

This guide covers what EOR is, how it works in practice, what compliance it handles, how it compares to setting up your own entity, and the most common — and costly — mistakes US companies make when hiring in India.

Key Takeaways

- An EOR is the legal employer on paper — handling payroll, taxes, PF/ESI, and compliance — while you direct the work

- India's employment rules differ by state — Bangalore, Mumbai, and Chennai each carry distinct obligations

- EOR gets an employee hired in days, not the months required to incorporate a local entity

- Mandatory statutory contributions add roughly 17–20% on top of base salary costs

- Contractor misclassification is the single most common compliance trap US companies fall into in India

What Is an Employer of Record (EOR) in India?

An EOR in India is a locally incorporated entity that becomes the legal employer for workers a foreign company wants to hire. It signs the employment contract under Indian law and takes on full compliance responsibility — while the US company directs the actual work. Specifically, the EOR:

- Registers the employee with EPFO and ESIC

- Withholds and remits TDS on salary payments

- Assumes liability for payroll errors, wrongful dismissal, and benefits shortfalls

This lets US companies legally employ workers in India, pay them in INR, and stay compliant with Indian labor law — without registering a Private Limited Company or Branch Office.

EOR vs. PEO — An Important Distinction

US companies sometimes encounter both terms. They are not interchangeable in India:

- EOR: Acts as the sole legal employer. The US company needs no existing Indian entity. This is the standard route for first-time India hiring.

- PEO: Co-employs workers and typically requires the client company to already have an Indian legal entity. As AZB & Partners notes, for legal purposes under a PEO model the PEO is still the employer and takes on employment-related obligations — but the client entity must exist.

No Indian entity? EOR handles that gap entirely, making it the default starting point for most US companies hiring in India for the first time.

Why US Companies Use EOR to Hire in India

The Talent and Cost Case

India's appeal for US companies comes down to three compounding factors:

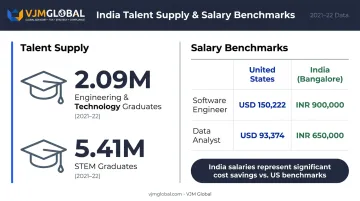

- Graduate output: AISHE data for 2021–22 shows India produced 2.09 million Engineering and Technology graduates and 5.41 million STEM graduates in a single academic year

- Professional workforce: NASSCOM cites over 9 million technology and customer experience professionals in India's services sector

- Salary benchmarks: Glassdoor 2026 data shows a Software Engineer averages USD 150,222/year in the US versus INR 900,000/year in Bangalore; a Data Analyst averages USD 93,374/year in the US versus INR 650,000/year in India

Applied across a team of 10 engineers, that differential is why companies from early-stage startups to Fortune 500s are actively building India teams.

Speed to Hire

A US company using an EOR can issue a compliant offer letter and onboard an employee within 48–72 hours. Compare that to incorporating independently: the MCA's SPICe+ process integrates company incorporation with GST, EPFO, ESIC, PAN/TAN registrations, and bank account setup — but in practice, the full preparation-to-completion window typically runs several weeks to months, depending on document readiness and approvals.

For companies that need to move fast — a key hire, a project deadline, a competitive window — that gap matters.

Compliance Offloaded

Indian payroll is not a single number. The EOR structures a Cost to Company (CTC) that includes:

- Basic salary

- HRA (House Rent Allowance)

- LTA (Leave Travel Allowance)

- Special Allowances

- Statutory deductions and employer contributions

Getting this wrong creates year-end TDS mismatches and underpaid statutory contributions — both of which fall on whoever is registered as the legal employer. That structural complexity is also what makes PE exposure a real concern.

PE and SEP Risk Mitigation

India has aggressive Permanent Establishment rules, and a US company directing employees on Indian soil can inadvertently create a taxable presence. India's Significant Economic Presence threshold sits at INR 2 crore in revenue or 300,000 users. An EOR provides a structural buffer because the EOR — not the US company — appears as the registered employer in all government databases (EPFO, ESIC). This does not eliminate PE risk entirely, but it removes one of the clearest triggers. A cross-border tax advisor should assess both PE and SEP exposure together before the first hire is made.

The Contractor Misclassification Trap

Many US companies start with "contractors" in India for speed. That approach carries serious risk. The Code on Social Security 2020 defines "employee" broadly to include persons employed through contractors. EPFO guidance makes clear there is no distinction between casual, contractual, and regular employees for PF coverage purposes.

Indian courts have reclassified independent contractors as employees for EPF purposes and directed retroactive PF benefits. Principal employers have been held liable for contractor PF defaults even when the contractor held a separate PF code. Reclassification triggers retroactive PF, ESI, gratuity, and TDS liabilities from day one of the engagement.

How EOR Services Work in India

Once a US company selects a candidate, the EOR takes over all employment formalities — contracts, registrations, payroll, and ongoing compliance. The process follows three distinct phases.

Step 1: Employment Contract and Statutory Registration

The EOR drafts an employment agreement under Indian law. A compliant contract must include:

- CTC structure: Under India's new Labor Codes (pending full implementation across states), if excluded pay components exceed 50% of total remuneration, the excess is added back to wages for PF calculation — so Basic salary must be structured with care

- Probation terms: Typically up to 6 months

- Notice period: Usually 30–90 days depending on role and seniority

- IP assignment: Employee-created IP does not automatically vest in the employer under all circumstances in India — explicit assignment clauses are essential

- NDAs: Must comply with the Indian Contract Act and IT Act 2000

After contract signing, the EOR registers the employee with EPFO (assigning a Universal Account Number), ESIC for eligible employees, and the relevant state's Professional Tax authority. Registration is a prerequisite before the first paycheck can legally be processed.

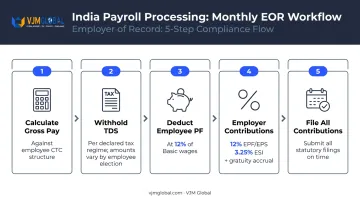

Step 2: Monthly Payroll Processing and Tax Withholding

With registrations in place, the EOR runs payroll each month. This involves:

- Calculates gross pay against the agreed CTC structure

- Withholds TDS based on the employee's declared tax regime (Old or New)

- Deducts the employee's PF contribution (12% of Basic wages)

- Calculates employer-side contributions: 12% employer EPF/EPS, 3.25% ESI for eligible employees, gratuity accrual, and statutory bonus where applicable

- Files all contributions on time to avoid penalties

Missing even one filing deadline can trigger penalties under the EPF Act or ESI Act — the EOR's role here is to absorb that risk entirely.

Step 3: Benefits Administration and Ongoing Compliance

Beyond payroll, Indian labor law requires continuous compliance activity. The EOR manages:

- Monthly PF Electronic Challan Cum Return (ECR) filings

- ESI contributions filed by the 15th of each month

- Form 16 issuance at financial year-end (April–March)

- Earned leave accruals per state-specific Shops and Establishments Act rules

- Professional Tax remittances per applicable state slabs

- Labor Welfare Fund contributions where required

- Monitoring legislative changes under India's four new Labor Codes

India-Specific Compliance: What Every US Company Must Know

Statutory Employer Contributions

These apply to all employers operating in India — Indian or foreign, no exceptions:

| Contribution | Rate | Notes |

|---|---|---|

| Employer EPF | 12% of Basic wages | INR 15,000/month wage ceiling; 8.33% to Pension Fund, 3.67% to EPF |

| Employee EPF | 12% of Basic wages | Deducted from salary |

| Employer ESI | 3.25% of wages | For employees below the ESI wage threshold |

| Employee ESI | 0.75% of wages | Deducted from salary |

| Gratuity | 15 days' wages per completed year | Payable after 5 years of continuous service |

| Statutory Bonus | 8.33%–20% of wages | Under the Payment of Bonus Act; calculation cap INR 7,000 or applicable minimum wage, whichever is higher |

Together, these add approximately 17–20% to the cost of an employee's Basic/Wage component.

State-Level Complexity

India is a federal system. Professional Tax slabs, Labor Welfare Fund rates, leave entitlement rules, and Shops and Establishments Act requirements differ by state:

- Maharashtra: Male employees earning above INR 10,000/month pay INR 2,500/year in Professional Tax; the Labor Welfare Fund employer contribution is INR 75 every six months (amended March 2024)

- Karnataka and Telangana: State-specific PT and LWF rates apply and require current official notifications to confirm — a generic EOR provider applying uniform templates will miss these

Without on-the-ground expertise, a US company risks applying outdated or incorrect state-level rates — exposing payroll to retroactive corrections and penalties.

The New Labor Codes

India consolidated 29 legacy labor laws into four codes. These codes have been notified at the central level; state-level adoption is ongoing, and implementation timelines vary by jurisdiction — confirm current status with official sources before finalizing your EOR setup. Key changes affecting US companies:

- Revised wage definition: If excluded components exceed 50% of total remuneration, the excess is added back to wages — directly impacting PF calculation

- Fixed-Term Employment: New contract type with pro-rated statutory benefits

- Gratuity eligibility: Changes under the Code on Social Security affect accrual rules

When evaluating an EOR provider, ask specifically how their payroll engine handles the 50% wage cap rule and whether their fixed-term employment contracts have been updated to include pro-rated statutory benefits.

Termination and Offboarding

The new Labor Codes reshape several compliance obligations — but the Industrial Disputes Act framework continues to govern termination for most workmen. Under the Industrial Disputes Act:

- Workers with at least 1 year of service cannot be retrenched without 1 month's notice or wages in lieu

- Retrenchment compensation equals 15 days' average pay per completed year of service

- Establishments with 100 or more workmen require 3 months' notice and prior government permission for retrenchment (Section 25N)

- All accrued earned leave, gratuity, and final settlements must be cleared at exit

The EOR handles these calculations and documentation, keeping the US company out of direct legal exposure.

EOR vs. Setting Up a Legal Entity in India

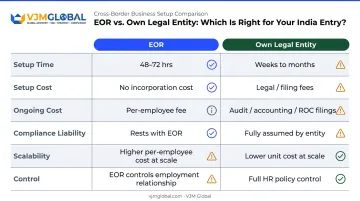

The Core Trade-Off

| Factor | EOR | Own Legal Entity |

|---|---|---|

| Setup time | 48–72 hours to first hire | Several weeks to months (SPICe+ process plus post-incorporation registrations) |

| Setup cost | No incorporation cost | Legal, professional, and filing fees for incorporation plus FEMA/RBI compliance for foreign-owned entities |

| Ongoing cost | Per-employee management fee | Statutory audit, accounting, annual ROC filings, local HR/legal team |

| Compliance liability | Rests with EOR | Fully assumed by the entity |

| Scalability | Higher per-employee cost at scale | Lower unit cost above a certain headcount |

| Control | US company directs work; EOR controls employment relationship | Full HR policy control |

When to Use EOR vs. When to Incorporate

EOR is typically the right choice when:

- Hiring 1–15 employees in India

- Testing the market before committing to a permanent presence

- You need to hire within weeks, not months

- You lack in-house India HR/legal expertise

Transitioning to your own entity makes sense when:

- Headcount grows beyond 15–25 employees, where EOR management fees begin to exceed entity operating costs

- Your India team requires custom HR policies you cannot implement through an EOR

- Indian revenues or operations approach India's Significant Economic Presence thresholds

- You need to hold Indian licenses or registrations (FEMA-regulated activities, financial services, government contracts)

Modeling the right transition point requires weighing your headcount trajectory, operational needs, and tax exposure. VJM Global's advisory team helps US companies work through this decision and select the right entry vehicle — Private Limited Company, Branch Office, or Liaison Office — based on their specific profile. For companies making the move, VJM Global also manages the full post-incorporation compliance stack: EPFO/ESIC registrations, statutory audit, ROC filings, and GST.

Common Mistakes US Companies Make When Using an EOR in India

1. Staying with Contractors Too Long

US companies often begin with contractors for speed, then extend engagements beyond 6–12 months without converting to employment. The risk compounds over time. Reclassification triggers retroactive PF, ESI, gratuity, and TDS liabilities back to day one, plus penalties. Review any contractor relationship before it crosses the 6-month mark.

2. Choosing EOR Providers Based on Price Alone

Global EOR platforms built primarily for European markets often handle India through standardized templates. These miss state-level nuances — Professional Tax slabs, DA calculations, Labor Welfare Fund contributions, and CTC structuring all require India-specific expertise. A generic template applied in Bangalore can expose you to back-tax assessments, penalties, and employee disputes that a compliant India-specific provider would have prevented.

3. Underestimating IP Protection Requirements

This is the most overlooked issue. Three critical points every US company must understand:

- Non-competes: Post-employment non-competes are largely unenforceable under Section 27 of the Indian Contract Act, 1872, which voids agreements restraining a person from a lawful profession

- Copyright: Employer ownership of employee-created work does vest under Section 17 of the Copyright Act — but only for copyright, not all forms of IP

- NDAs and trade secrets: These must be drafted to comply with both the Indian Contract Act and the IT Act 2000 to carry any post-employment weight

Ensure your EOR's employment contract explicitly includes IP assignment clauses, trade secret protections, and post-employment NDAs reviewed under Indian law.

Conclusion

EOR is the fastest, lowest-risk path for US companies to hire Indian talent compliantly. It removes the need for entity setup, offloads statutory registrations, payroll structuring, PF/ESI filings, and termination compliance to a local expert, and protects against the most common pitfalls: misclassification, PE risk, and incorrect payroll structure.

The value of EOR in India lies not just in speed of hire but in the depth of on-the-ground compliance expertise. That means knowing how to structure a CTC correctly, when ESI thresholds apply, and how to handle a termination without triggering a dispute.

VJM Global provides end-to-end EOR, payroll, and compliance support for US companies building India teams, backed by 30+ years of experience and a track record across 500+ American businesses. Reach out at info@vjmglobal.com or through the US office at 447 Broadway, 2nd Floor, New York, NY 10013.

Frequently Asked Questions

Can a US company employ someone in India?

Yes, but a US company cannot legally run Indian payroll or register statutory benefits without either a registered Indian legal entity or an Employer of Record. An EOR is the standard mechanism that enables this without requiring entity incorporation first.

What is the difference between EOR and setting up a legal entity in India?

An EOR acts as the legal employer on your behalf with no entity setup time or incorporation cost, while a legal entity requires several weeks to months to register and carries full ongoing compliance responsibility. EOR suits smaller or earlier-stage India hiring; a wholly owned entity makes sense at larger scale.

What statutory benefits are mandatory for employees in India?

Four statutory employer contributions apply to all employees in India, regardless of whether the employer is Indian or foreign:

- Provident Fund: 12% of basic wages

- ESI: 3.25% employer contribution (for eligible employees)

- Gratuity: 15 days' wages per completed year, payable after 5 years of service

- Statutory Bonus: 8.33%–20% under the Payment of Bonus Act

How long does it take to onboard an employee in India through an EOR?

An EOR can issue a compliant offer letter within 24–48 hours and complete EPFO/ESIC registration and first payroll setup within 1–2 weeks — compared to the weeks or months required for entity incorporation.

Does using an EOR in India protect a US company from permanent establishment risk?

An EOR provides a meaningful buffer: the EOR — not the US company — appears as the registered employer in all Indian government databases, reducing the risk of the Indian workforce triggering a taxable branch classification. That said, no official CBDT safe harbor for EOR arrangements currently exists, so independent tax counsel for your specific situation is advisable.

What happens if a US company misclassifies a worker as a contractor in India?

Reclassification by Indian authorities means retroactive liability for Provident Fund, ESI, gratuity, and TDS going back to the start of the engagement, plus potential penalties. Converting those contractors to employees through an EOR before enforcement risk materializes eliminates this exposure.