Introduction

Picture this: your business closes its books on 31st March, but a consignment worth ₹15 lakhs is somewhere on a truck between your Delhi supplier and your Mumbai warehouse. It hasn't been counted in your stock-take. Your supplier thinks they've already sold it. You haven't recorded a purchase yet. Both of you could be wrong.

This is the goods in transit problem — and it's one of the most common sources of year-end cut-off errors flagged during audits.

Getting this wrong means misstated inventory and incorrect profit figures — with GST mismatches compounding the problem. The fix starts with one principle: ownership determines who records the transaction, regardless of where the goods physically sit.

This article covers:

- What goods in transit (GIT) means in accounting

- How FOB, CIF, and FAS shipping terms determine ownership

- Journal entries for both buyer and seller

- Balance sheet classification under IAS 2 / Ind AS 2

- Year-end cut-off procedures and common mistakes

- GST compliance considerations for Indian businesses

Key Takeaways

- Goods in transit are inventory shipped but not yet received — ownership depends entirely on shipping terms, not physical location

- FOB Shipping Point: buyer takes ownership at shipment; buyer records inventory immediately

- FOB Destination: seller retains ownership until delivery; the sale is recorded only upon arrival

- Under Ind AS, Indian companies must disclose goods in transit as a separate line within inventory on the balance sheet — required under Schedule III, Division II

- Year-end cut-off review is essential — skipping it directly causes inventory misstatement and audit findings

What Are Goods in Transit?

Goods in transit (GIT) refers to inventory that has been dispatched by the seller but not yet physically received by the buyer. At any given moment, these goods exist in neither party's warehouse — sitting on a truck, at a port, or in a courier's possession.

That's precisely what makes them easy to miss during stock counts.

The core accounting challenge here is legal, not logistical. Ownership and financial responsibility follow the transfer of title, not the physical movement of goods. That gap means both buyer and seller can end up double-counting or entirely omitting the same inventory — distorting inventory values, cost of goods sold (COGS), and profit.

GIT is also referred to as "pipeline inventory" or "in-transit inventory." It arises in:

- Domestic transactions (supplier to buyer within India)

- Import/export transactions (cross-border shipments)

- E-commerce fulfilment operations where goods are continuously in movement

Determining ownership at the moment of transit is what drives the entire accounting treatment. Shipping terms — FOB Origin, FOB Destination, CIF, and similar — define exactly when title transfers, and therefore who records the inventory.

Shipping Terms That Determine Ownership

The sales contract or purchase order specifies shipping terms, which govern when title — and therefore accounting responsibility — transfers from seller to buyer.

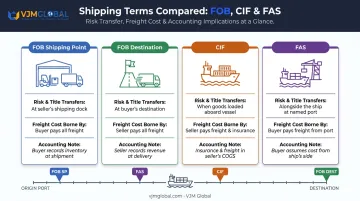

FOB Shipping Point

Under FOB Shipping Point (also called FOB Origin), ownership transfers the moment goods leave the seller's shipping dock. From that point:

- The buyer bears the risk of loss or damage during transit

- The buyer pays freight charges

- The buyer must record the goods in their inventory immediately, even before physical receipt

Example: A seller in Delhi ships goods on 28th March under FOB Shipping Point. The buyer in Mumbai receives them on 2nd April. As at 31st March, these goods legally belong to the buyer — and must appear in the buyer's closing inventory for the financial year ending 31st March.

FOB Destination

Under FOB Destination, ownership stays with the seller until goods physically arrive at the buyer's specified location. The seller:

- Bears all transit risk

- Typically pays freight

- Keeps the goods on their own balance sheet until delivery is confirmed

Same example, reversed: Under FOB Destination, the seller includes these goods in their 31st March inventory. The buyer records neither a purchase nor inventory until 2nd April when the goods arrive.

Other Shipping Terms

| Term | Risk Transfers When | Restricted To |

|---|---|---|

| FAS (Free Alongside Ship) | Goods placed alongside the vessel at named port | Sea/waterway only |

| CIF (Cost, Insurance and Freight) | Goods loaded onto vessel at port of shipment (despite seller paying freight to destination) | Sea/waterway only |

A common misconception with CIF: because the seller pays freight and insurance to the destination port, buyers assume risk only transfers on arrival. It doesn't. Under Incoterms 2020, risk transfers when goods are loaded at the port of shipment. The buyer holds the risk for the entire ocean voyage.

One further point worth separating: Incoterms 2020 govern international trade and define risk transfer, but they do not explicitly define legal title transfer, which the applicable contract law governs. For domestic Indian transactions, the sales contract terms and the Sale of Goods Act determine title. Always state clearly which framework applies.

Accounting Treatment for Goods in Transit

The principle is straightforward: passage of title triggers the accounting entry. Mis-timing these entries leads to incorrect revenue recognition, inventory misstatement, and audit findings. Under IFRS 15, Paragraph 38, revenue is recognised only when control transfers to the customer — with indicators including legal title, physical possession, and transfer of significant risks and rewards.

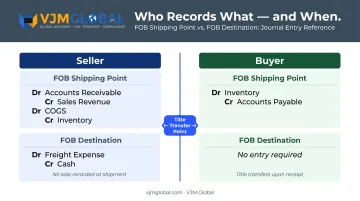

Accounting Entries for the Seller

Under FOB Shipping Point — record the sale at the point of shipment:

Dr Accounts Receivable ₹X

Cr Sales Revenue ₹X

(To record sale at point of shipment)

Dr Cost of Goods Sold ₹X

Cr Inventory ₹X

(To remove goods from inventory)

Under FOB Destination — do NOT record a sale until goods arrive at the buyer's location:

- Goods remain in seller's inventory until delivery

- No entry to Sales Revenue or COGS

- Any freight paid by the seller is debited to Freight/Delivery Expense:

Dr Freight/Delivery Expense ₹X

Cr Cash/Accounts Payable ₹X

The mirror treatment applies on the buyer's side — the same shipment date that triggers the seller's entry determines when the buyer records a purchase.

Accounting Entries for the Buyer

Under FOB Shipping Point — record the purchase on the shipment date, even before goods arrive:

Dr Inventory/Purchases ₹X

Cr Accounts Payable ₹X

(To record purchase as at shipment date)

These goods must be included in the buyer's closing inventory for the period, even if they haven't physically arrived.

Under FOB Destination — record nothing until goods are physically received:

- No purchase entry

- No payable

- No inventory addition

Any premature recording under FOB Destination inflates both inventory and liabilities. Under AS 9 (Indian GAAP), Paragraph 11, revenue from the sale of goods is recognised only when the seller has transferred property in goods or all significant risks and rewards of ownership. A FOB Destination shipment still in transit therefore cannot be recognised as a sale by either party.

How Goods in Transit Appear on Financial Statements

Balance Sheet Classification

Once title transfers to the buyer (FOB Shipping Point), goods in transit are classified as a current asset under Inventory on the buyer's balance sheet — regardless of physical location. This aligns with IAS 2, Paragraph 6, which defines inventories as assets held for sale in the ordinary course of business.

For Indian companies under Ind AS, there's an additional disclosure requirement: Schedule III, Division II of the Companies Act, 2013 explicitly requires that goods-in-transit be disclosed separately within the relevant inventory sub-head (e.g., "Raw Materials in Transit" or "Finished Goods in Transit"). Merging GIT into the general inventory line without disclosure is non-compliant.

For the seller under FOB Destination: goods in transit remain on the seller's balance sheet as inventory until delivery occurs. Removing them prematurely understates assets and inflates profit.

Impact on the Income Statement

Balance sheet misclassification rarely stays isolated — it flows directly into income statement errors. Recording a sale before title has transferred violates revenue recognition standards across frameworks: ASC 606 under US GAAP, IFRS 15 under international standards, and AS 9 under Indian GAAP. The result:

- Revenue and gross profit are overstated in the wrong period

- COGS is understated (goods not yet removed from inventory)

- Auditors flag this as a cut-off error — a high-risk area in inventory audits per PCAOB AS 2510

Common Mistakes and Year-End Accounting for Goods in Transit

The Inventory Cut-Off Problem

At month-end, quarter-end, or year-end, every pending shipment needs a deliberate review. The question for each open shipment is: based on the FOB terms, does this belong in the buyer's closing inventory, the seller's, or neither?

Skipping this review is one of the most common causes of inventory misstatement — not because accountants don't know the rule, but because the volume of shipments near a period close makes it easy to miss individual lines.

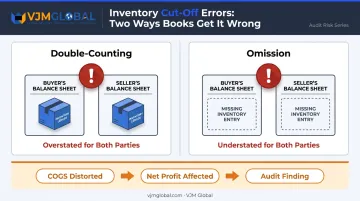

Double-Counting and Omission

If neither party confirms ownership under FOB terms:

- Double-counting: goods appear in both buyer's and seller's inventory simultaneously — overstated for both

- Omission: goods appear in neither party's inventory — understated for both

Both outcomes directly affect COGS and net profit calculations, and auditors will catch both.

Loss or Damage in Transit

Responsibility for loss follows the same ownership logic:

- FOB Shipping Point: the buyer absorbs the loss and must write off the inventory (Dr Loss on Inventory / Cr Inventory). If insured, the buyer files the insurance claim.

- FOB Destination: the seller absorbs the loss and records it accordingly.

For high-value shipments, the party bearing transit risk should carry in-transit insurance — it's the only reliable hedge against an unrecoverable write-off.

GST Compliance for Indian Businesses

Beyond ownership and loss, Indian businesses face a documentation layer that directly affects accounting records. Under Rule 138 of the CGST Rules, 2017, every registered person moving goods with a consignment value exceeding ₹50,000 must generate an e-way bill before movement commences. Key points:

- Consignment value includes central tax, State/UT tax, IGST, and cess

- Validity: 1 day per 200 km for normal cargo; shorter for over-dimensional cargo

- Exemptions apply for specific categories (LPG under PDS, currency, jewellery, postal baggage, and others listed in the Annexure)

Accounting records must align with GST documentation. Any mismatch between the point of supply recorded in books and the e-way bill date or delivery records can trigger notices during GST return scrutiny.

Best Practices for Managing Goods in Transit

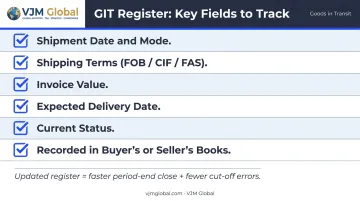

Maintain a GIT Register

A dedicated goods in transit tracker should capture, for every open shipment:

- Shipment date and mode

- Shipping terms (FOB Shipping Point / FOB Destination / CIF / FAS)

- Invoice value

- Expected delivery date

- Current status

- Whether recorded in buyer's or seller's books

This makes period-end reconciliations faster and significantly reduces cut-off errors.

Document Shipping Terms Consistently

- State FOB terms clearly on every purchase order and sales invoice

- Train the accounts team on how FOB rules apply — especially for international transactions where CIF or FAS may be used

- For cross-border shipments, specify whether Incoterms 2020 or domestic contract law governs title transfer

Work with Experienced Accounting Professionals

For businesses with frequent or high-value in-transit inventory, proper controls prevent cut-off errors that distort financial statements. An experienced accounting team will:

- Build cut-off procedures into the month-end close process

- Maintain the GIT register as a live reconciliation tool

- Ensure Ind AS / Schedule III disclosure requirements are met

- Handle GST reconciliation for cross-border shipments

VJM Global supports businesses from the US, UK, and Australia that operate in — or are entering — India. Their accounting outsourcing team manages journal entries, GST reconciliation, and period-end close processes, with specific experience establishing inventory recognition policies for companies setting up Indian operations for the first time.

Frequently Asked Questions

How do you account for goods in transit?

Accounting for GIT depends on shipping terms. Under FOB Shipping Point, the buyer records a purchase and adds goods to inventory on the shipment date. Under FOB Destination, neither party records a transaction until goods physically arrive at the buyer's location.

Are goods in transit an asset or a liability?

Goods in transit are a current asset (inventory) — never a liability. Under FOB Shipping Point, they appear on the buyer's balance sheet from the shipment date. Under FOB Destination, they remain on the seller's balance sheet until delivery.

What is the difference between FOB Shipping Point and FOB Destination?

FOB Shipping Point transfers title and risk when goods leave the seller's dock, so the buyer records inventory immediately. FOB Destination keeps ownership and risk with the seller until goods arrive, meaning the buyer records nothing until delivery.

What happens to goods in transit if they are lost or damaged?

Responsibility depends on the shipping terms. Under FOB Shipping Point, the buyer bears the loss and may file an insurance claim. Under FOB Destination, the seller is responsible for the loss. Carry in-transit insurance for high-value shipments regardless of FOB terms.

How should goods in transit be handled at year-end?

Perform an inventory cut-off review: confirm FOB terms for all open shipments and ensure GIT appears on the correct party's closing balance sheet. Indian companies must also disclose goods in transit separately within inventory per Schedule III requirements.