Introduction

Foreign companies entering the Indian market face a critical accounting challenge: they're familiar with IFRS but encounter a different regulatory framework — Indian GAAP — which affects asset valuation, revenue timing, and compliance obligations. A UK-based manufacturer setting up a subsidiary in Noida, or an Australian tech firm establishing operations in Bangalore, must navigate these divergences to avoid costly restatements.

Companies reporting under IFRS internationally still need to reconcile financials under Indian GAAP for local compliance — these are not interchangeable frameworks. Understanding the key differences prevents penalties and costly restatements before they happen.

This article breaks down the most consequential divergences: revenue recognition, lease accounting, financial instruments, and more. For any foreign business operating across multiple jurisdictions, this is where group consolidation accuracy either holds together or falls apart.

Key Takeaways

- Indian GAAP covers 27 Accounting Standards issued by ICAI; IFRS is used in 140+ countries

- Indian GAAP is rules-prescriptive and conservative; IFRS relies on judgment-based application

- IFRS allows asset revaluation and development cost capitalisation — Indian GAAP is more restrictive on both

- Key divergences span revenue recognition, lease accounting, and financial instrument measurement

- Companies above ₹250 crore net worth follow Ind AS (IFRS-converged); smaller entities use traditional Indian GAAP

IFRS vs Indian GAAP: Quick Comparison

| Aspect | IFRS | Indian GAAP |

|---|---|---|

| Governing Body | IASB | ICAI / MCA |

| Basis | Principles-based | Rules-based (prescriptive) |

| Inventory Methods | FIFO, Weighted Average (LIFO prohibited) | FIFO, Weighted Average (LIFO prohibited) |

| Asset Revaluation | Revaluation model allowed | Cost model primary; revaluation limited |

| Development Costs | Capitalisation mandatory if criteria met | Capitalisation permitted but not mandatory |

| Revenue Recognition | Five-step performance obligation model (IFRS 15) | Risks and rewards transfer (AS 9) |

| Lease Accounting | Single lessee model - all on-balance-sheet (IFRS 16) | Operating vs Finance lease distinction (AS 19) |

| Financial Instruments | Comprehensive framework - IFRS 9 with ECL model | Fragmented guidance - AS 13 primarily |

| Global Applicability | 140+ jurisdictions | India only |

This comparison covers traditional Indian GAAP (AS standards). Ind AS — India's IFRS-converged framework — sits between the two. We'll break down how it differs from both frameworks in the next section.

What is Indian GAAP?

Indian GAAP refers to the 27 active Accounting Standards (AS 1 through AS 29, with AS 6 and AS 8 withdrawn and merged into other standards) issued by the Institute of Chartered Accountants of India (ICAI) and notified under the Companies Act by the Ministry of Corporate Affairs (MCA).

This is the traditional framework still applicable to companies that don't qualify for Ind AS — smaller private companies, unlisted entities below the net worth threshold, and certain NBFCs.

The regulatory ecosystem works through a three-tier system: ICAI formulates the standards, MCA notifies them under Schedule III of the Companies Act 2013, and SEBI mandates compliance for applicable listed entities.

Indian GAAP is more conservative than IFRS. Where IFRS provides principles and lets preparers exercise professional judgment, Indian GAAP prescribes detailed rules with less flexibility. Key characteristics include:

- Prioritises historical cost accounting over fair value measurement

- Follows industry-specific prescriptive rules

- Limits management's discretion in accounting estimates

Important clarification: The often-cited "AS 1 through AS 32" is inaccurate. AS 30, 31, and 32 (Financial Instruments standards) were issued, but MCA never mandated them. ICAI formally withdrew all three in November 2016. The active framework contains 27 standards.

Use Cases of Indian GAAP

Indian GAAP applies to unlisted companies below the Ind AS threshold, certain partnership firms, proprietorships, and smaller private limited companies. The current MCA threshold criteria are:

Ind AS becomes mandatory when any of the following conditions apply:

- All listed companies (from April 2017 onwards, regardless of net worth)

- Unlisted companies with net worth ≥ ₹250 crore (from April 2018)

- Banks, NBFCs, and insurance companies meeting specified thresholds

- Subsidiaries, associates, and JVs of companies covered above

There is also a chain reaction rule: if Ind AS applies to a parent or holding company, it automatically extends to all subsidiaries, associates, joint ventures, and holding companies — regardless of their individual net worth.

Foreign companies setting up subsidiaries or joint ventures in India need to understand this classification. Your Indian entity's accounting obligations depend on its classification under Indian law, not on what the parent company uses globally. A wholly owned subsidiary of a US-based IFRS-reporting parent could still fall under Indian GAAP if its net worth stays below ₹250 crore and it's unlisted.

What is IFRS?

IFRS (International Financial Reporting Standards) is the global accounting framework developed by the International Accounting Standards Board (IASB), used in more than 140 jurisdictions worldwide. Unlike Indian GAAP's rule-based structure, IFRS is principles-based: it sets broad objectives and allows preparers to apply professional judgment in how those objectives are met.

The IASB Conceptual Framework (revised March 2018) establishes the qualitative characteristics of useful financial information through two tiers:

Fundamental Characteristics (2):

- Relevance – Useful only when it can influence a decision; predictive value, confirmatory value, or both

- Faithful Representation – Depicts the economic substance of transactions accurately, without bias or material omission

Enhancing Characteristics (4):

- Comparability – Enables users to identify trends across periods and benchmark against other entities

- Verifiability – Independent observers applying the same methods should reach substantially the same conclusions

- Timeliness – Stale information loses decision-usefulness; reporting must keep pace with events

- Understandability – Information is classified, characterized, and presented so that a reasonably knowledgeable user can interpret it

Knowing these characteristics matters in practice: when Indian financial statements are challenged or compared against IFRS-prepared group accounts, these are the benchmarks applied.

Use Cases of IFRS

IFRS is directly used in India in specific scenarios:

- Foreign companies filing with international regulators

- Indian companies listed on overseas exchanges

- Parent entities of Indian subsidiaries needing group consolidation under IFRS

India does not mandate full IFRS domestically. Instead, it uses Ind AS as the IFRS-converged alternative. The two are similar but not identical due to carve-outs and modifications made for Indian regulatory needs.

This creates a practical challenge for global MNCs: when an Indian subsidiary prepares Indian GAAP or Ind AS financials for local compliance but the parent consolidates under IFRS, reconciliation adjustments become necessary, adding compliance effort and cost that many foreign entrants underestimate.

Key Differences Between IFRS and Indian GAAP

Inventory Valuation

Convergence Point: Both IAS 2 (IFRS) and AS 2 (Indian GAAP) prohibit LIFO (Last-In, First-Out) and permit FIFO (First-In, First-Out) and Weighted Average Cost methods. Both frameworks measure inventory at the lower of cost and net realisable value. The practical impact is method selection: FIFO produces higher reported profits during rising input costs (lower COGS), while weighted average smooths volatility. For manufacturing, trading, or retail businesses, the available options are identical — the difference lies in what each company chooses.

Asset Revaluation and Impairment

IFRS (IAS 16 / IAS 36):

- Revaluation model permitted as a policy choice — assets can be written up to fair value

- Revaluation gains go to other comprehensive income (revaluation surplus)

- Impairment reversals permitted for all assets except goodwill

Indian GAAP (AS 10 / AS 28):

- Cost model is the standard basis; upward revaluation is technically permitted but restricted

- Revaluation gains go to revaluation reserve

- Depreciation on the revalued portion can be recouped from the revaluation reserve (unlike IFRS)

- Impairment reversals are permitted subject to specific conditions

- Goodwill impairment reversal allowed only if caused by a specific external exceptional event that won't recur

The practical impact: under IFRS, companies in asset-intensive industries can reflect current fair values on their balance sheets, potentially improving debt-to-equity ratios. Indian GAAP's cost-based approach keeps asset values conservative but may understate the company's true worth.

Development Costs

IFRS (IAS 38): Development costs must be capitalised as an intangible asset when all six criteria are demonstrated:

- Technical feasibility of completion

- Intention to complete and use/sell

- Ability to use or sell the asset

- How it will generate probable future economic benefits

- Availability of adequate resources

- Ability to measure expenditure reliably

Indian GAAP (AS 26): Development costs can be capitalised (permissive, not mandatory) when:

- Future economic benefits are probable

- Cost can be measured reliably

- Technological feasibility is established

- Only costs from the recognition point to readiness can be capitalised

- Rebuttable presumption of 10-year maximum useful life

Real impact for technology businesses: A software company developing a new platform might capitalise ₹5 crore in development costs under IFRS (if criteria are met), creating an intangible asset on the balance sheet. Under Indian GAAP, the same company might expense these costs, reducing reported profit by ₹5 crore in the development year but avoiding future amortisation charges.

Revenue Recognition

IFRS 15 — Five-Step Model:

- Identify the contract(s)

- Identify separate performance obligations

- Determine the transaction price

- Allocate price to performance obligations

- Recognise revenue when obligations are satisfied

Indian GAAP (AS 9): Revenue recognised when significant risks and rewards of ownership transfer — a single transaction-level assessment with no concept of "performance obligations" or multi-step allocation.

Software Revenue Example:

A company sells a software license bundled with 2 years of support for ₹10,00,000:

- Under IFRS 15: Separate into two performance obligations. If standalone selling prices are ₹7,00,000 (license) and ₹3,00,000 (support), allocate transaction price accordingly. Recognise ₹7,00,000 at contract inception (point in time) and ₹3,00,000 ratably over 24 months

- Under AS 9: Assess the entire bundle under risks/rewards transfer. No mandatory requirement to separate. Revenue could potentially be recognised earlier or as a lump sum when risks/rewards transfer

For businesses with bundled contracts or multi-year agreements, this timing gap can materially shift revenue between reporting periods — and change how investors or lenders read the financials.

Lease Accounting

IFRS 16 (effective 1 January 2019):

- Single lessee accounting model

- All leases on-balance-sheet as right-of-use (ROU) asset and lease liability

- Exceptions: short-term leases (<12 months) and low-value assets

- Eliminates operating/finance lease distinction for lessees

Indian GAAP (AS 19):

- Retains operating vs finance lease distinction

- Finance lease: On-balance-sheet (transfers substantially all risks/rewards)

- Operating lease: Off-balance-sheet — expense in P&L, asset stays with lessor

Balance Sheet Impact:

A 2016 PwC study analysed 3,199 listed IFRS organisations globally and found total assets rose by an average of 14% for airlines, retail/apparel, and shipping/transport sectors upon lease capitalisation under IFRS 16.

For a retail chain with ₹50 crore in annual operating lease commitments under Indian GAAP, transitioning to IFRS 16 could add ₹200-300 crore in ROU assets and lease liabilities to the balance sheet (depending on remaining lease terms and discount rates). This directly affects leverage ratios, debt covenants, and reported EBITDA.

Financial Instruments

IFRS 9: Three classification categories for financial assets:

- Amortised cost – held to collect contractual cash flows

- FVOCI (fair value through OCI) – held to collect and sell

- FVTPL (fair value through P&L) – all others

- Forward-looking Expected Credit Loss (ECL) model for impairment

Indian GAAP:

- AS 13 (Accounting for Investments) is the primary standard

- Current investments: lower of cost or fair value

- Long-term investments: cost less permanent diminution

- AS 30/31/32 (Financial Instruments) were withdrawn in 2016 — never made mandatory

- Non-Ind AS companies rely on AS 13 and ICAI guidance notes

Non-Ind AS companies have no forward-looking impairment model under Indian GAAP — losses are recognised only when they become apparent, not anticipated. For banks, NBFCs, and treasury-heavy businesses, this means credit risk is systematically underreported relative to IFRS 9 requirements.

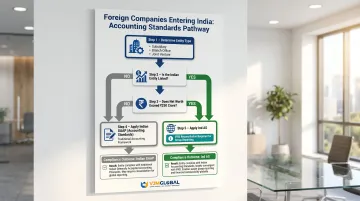

Which Accounting Framework Applies to Your Business in India?

The Ind AS Threshold Decision Tree

India's IFRS-converged standards (Ind AS) apply mandatorily based on these criteria:

| Entity Type | Net Worth Threshold | Effective Date |

|---|---|---|

| Listed companies (all) | Regardless of net worth | 1 April 2017 |

| Unlisted companies | ≥ ₹250 crore | 1 April 2018 |

| Banks, insurance | ≥ ₹500 crore | Phased 2018-2019 |

| NBFCs | ≥ ₹250 crore | 1 April 2019 |

Foreign Subsidiary Rule: Indian companies that are subsidiaries, associates, or JVs of foreign companies apply the same criteria based on their Indian entity's individual net worth and listing status.

For foreign companies entering India:

- Determine entity type — subsidiary, branch office, liaison office, or JV

- Assess whether the Indian entity will be listed or meets the ₹250 crore net worth threshold

- If below threshold: Indian GAAP (AS) applies

- If above threshold: Ind AS applies

- Group reporting: Parent may still need IFRS reconciliation regardless of which framework the Indian entity uses

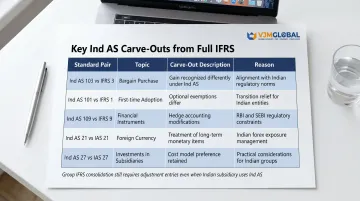

Ind AS Carve-outs from Full IFRS

Even companies using Ind AS (not traditional Indian GAAP) face differences from full IFRS. Key carve-outs include:

| Ind AS | IFRS | Carve-out | Reason |

|---|---|---|---|

| Ind AS 103 | IFRS 3 | Bargain purchase gain to OCI, not P&L | Prevents acquisition structuring for profit manipulation |

| Ind AS 40 | IAS 40 | Only cost model permitted for investment property | Lack of deep liquid markets; avoids unrealised P&L gains |

| Ind AS 19 | IAS 19 | Discount rate must use government bonds | Indian market-specific adaptation |

| Ind AS 101 | IFRS 1 | Additional option to use previous GAAP carrying values as deemed cost | Retrospective application difficult for older companies |

| Ind AS 16 | IAS 16 | Net sale proceeds from testing deducted from asset cost | Testing output not commercial |

These modifications mean that group IFRS consolidation still requires adjustment entries even when the Indian subsidiary uses Ind AS.

Strategic Guidance

If you're a foreign MNC setting up a wholly owned subsidiary in India with ambitions to scale, you'll likely transition to Ind AS as your entity grows. Build accounting systems and processes that are Ind AS-ready from the start, even if Indian GAAP applies initially. This reduces transition costs later.

The carve-outs above also have a direct operational implication: even after your Indian entity adopts Ind AS, your group consolidation team will need specific adjustment entries to reconcile to full IFRS. Factor that into your reporting workflows early.

For foreign companies managing framework transitions or group reconciliations, working with India-specialist accountants avoids misstatements that can trigger regulatory scrutiny. VJM Global's Chartered Accountants have supported 500+ American, 250+ UK, and 250+ Australian businesses through India entry — from choosing the right entity structure to managing ongoing statutory compliance under either framework.

Conclusion

IFRS is a global, principles-based framework built for cross-border comparability. Indian GAAP is a more conservative, rules-prescriptive system designed for India's regulatory environment. Which standard applies to your business depends on your entity type, size, and reporting purpose — there is no single right answer.

For foreign companies operating in India, three questions matter most:

- Which framework governs your Indian entity under local regulations

- Where IFRS reconciliation will be required for group reporting back to your parent

- How differences in asset valuation, revenue recognition, and lease accounting affect your reported financials

Getting this right early avoids costly rework, penalties, and restatements. VJM Global's cross-border accounting and India entry advisory team helps foreign businesses map these differences before they become reporting problems.

Frequently Asked Questions

What is the difference between IFRS and Indian GAAP?

IFRS is a global principles-based framework used in 140+ countries, while Indian GAAP refers to India's traditional Accounting Standards (AS), which are more rules-based and conservative. Key differences include asset revaluation approaches, development cost treatment, lease accounting (on vs off-balance-sheet), and revenue recognition models.

Does India follow IFRS or Ind AS?

India uses Ind AS (Indian Accounting Standards) — a version converged with IFRS but modified for domestic regulatory requirements, tax-accounting linkages, and local market conditions. Companies below the ₹250 crore net worth threshold continue using traditional Indian GAAP (AS).

Why is IFRS not implemented in India?

India chose convergence (Ind AS) over full adoption to accommodate its domestic regulatory framework, tax-accounting linkages, and the needs of smaller entities. Additional factors include disagreements with specific IFRS provisions, standard-setting sovereignty concerns, and limited deep liquid markets for fair value measurements.

Are US GAAP and Indian GAAP the same?

No. US GAAP is a rules-based system regulated by FASB and applicable only in the United States, while Indian GAAP is issued by ICAI under India's Companies Act. Both differ from IFRS in their own ways, but US GAAP and Indian GAAP are distinct frameworks with different governing bodies, standards, and regulatory contexts.

What are the 4 pillars of IFRS?

The IASB Conceptual Framework 2018 identifies two fundamental characteristics — relevance and faithful representation — along with four enhancing ones: comparability, verifiability, timeliness, and understandability. Together, these six characteristics guide how all IFRS standards are designed and interpreted.

Why was IAS replaced by IFRS?

IAS (International Accounting Standards) were issued by the IASC from 1973–2001. When the IASB replaced the IASC in April 2001, it began issuing new standards as IFRS while retaining and updating existing IAS standards. Today, both IAS and IFRS standards coexist under the same framework; IAS was not eliminated but absorbed and selectively updated.