Introduction

When costs and revenues are tied up in partially completed projects spanning multiple accounting periods, traditional cash-basis accounting simply falls short. Work In Progress (WIP) accounting exists to bridge that gap — but doing it accurately is harder than it looks.

Consider a construction firm midway through a £500,000 contract, or a consulting firm that has delivered 60% of a year-long engagement. Both face the same question: how do you report financial performance when the work is incomplete?

Getting it wrong has real consequences. Inaccurate WIP reporting can artificially inflate or deflate monthly profits, distort cash flow projections, and trigger audit flags during statutory reviews. According to the Financial Reporting Council's thematic review of IFRS 15 implementation, many companies' revenue disclosures failed to meet quality thresholds — with inadequate explanations of judgements and inconsistent reporting of contract balances.

This guide covers:

- What WIP accounting is and why it matters

- How to record it correctly using journal entries

- Where it appears on your balance sheet and P&L

- How to calculate it using the percentage-of-completion method

- Common pitfalls that create compliance risks under UK GAAP (FRS 102), IFRS, and Ind AS

TLDR: Key Takeaways

- WIP represents partially completed goods or services at a reporting date and sits as a current asset on your balance sheet

- WIP accounting applies across manufacturing, construction, and professional services — each with distinct recognition rules

- Percentage-of-completion method drives revenue recognition: % Complete = Costs Incurred ÷ Estimated Total Costs

- Underbilling creates a contract asset; overbilling creates a contract liability — both affect your balance sheet classification

- Key standards governing WIP recognition include IFRS 15, US GAAP ASC 606, and the revised FRS 102 Section 23 (UK GAAP, effective January 2026)

What Is Work In Progress (WIP) in Accounting?

WIP represents the intermediate stage between raw materials and finished goods — the value of partially completed products or services on which costs have been incurred but which are not yet ready for sale or delivery. Under IAS 2 paragraph 8, inventories encompass "work in progress being produced by the entity," and paragraph 37 classifies WIP as a current asset alongside materials and finished goods.

The Three-Stage Inventory Classification

Every manufacturing or production business tracks inventory through three distinct stages:

- Raw materials — inputs purchased but not yet used in production (timber in a warehouse)

- Work in progress — materials currently being converted into products (chairs being assembled on the factory floor, with legs attached but no upholstery)

- Finished goods — completed products ready for sale (fully assembled, upholstered chairs in the showroom)

Work In Progress vs Work In Process

You'll encounter both terms in practice, though no accounting standard formally distinguishes between them. Industry convention treats "work in process" as the term for short-cycle manufacturing environments where goods move quickly through production stages, while "work in progress" typically refers to longer-duration construction projects or professional service contracts. Both appear identically on the balance sheet as current assets. IAS 2 uses only "work in progress" throughout its text.

WIP Cost Components

Three categories of costs accumulate in the WIP account until goods or services are complete:

Direct materials (IAS 2 paragraph 11): Purchase price plus import duties, transport, handling, and other costs directly attributable to bringing materials to their present location and condition.

Direct labour (IAS 2 paragraph 12): Wages and salaries paid to workers directly involved in converting materials into finished goods.

Production overheads (IAS 2 paragraph 12): Fixed overheads (factory rent, equipment depreciation) are allocated based on normal capacity, while variable overheads (utilities, indirect materials) are allocated based on actual production facility use.

These three components — materials, labour, and overheads — flow into the WIP account as costs are incurred. When the project completes or goods are sold, the accumulated WIP balance transfers to Cost of Goods Sold (manufacturing) or gets matched against recognised revenue (construction and services).

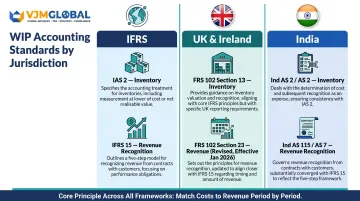

Accounting Standards Governing WIP

The regulatory framework varies by jurisdiction but shares core principles:

| Jurisdiction | Inventory Standard | Revenue Recognition |

|---|---|---|

| IFRS | IAS 2 — WIP valued at lower of cost and net realisable value | IFRS 15 — governs revenue on long-term contracts |

| UK & Ireland | FRS 102 Section 13 — inventory measurement including WIP | Revised Section 23 (effective 1 Jan 2026) — five-step model aligned with IFRS 15 |

| India | Ind AS 2 — converges with IAS 2; non-Ind AS entities use AS 7 | Ind AS 115 (aligned with IFRS 15); AS 7 uses percentage-of-completion for eligible entities |

Across all three frameworks, the underlying principle is the same: costs must be matched with the revenue they generate, period by period, so profit figures reflect actual production activity rather than cash timing.

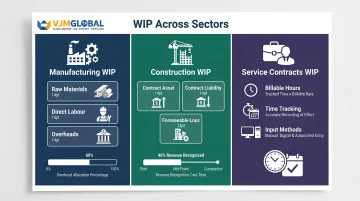

Types of WIP: Manufacturing, Construction, and Services

WIP accounting looks quite different depending on whether you're dealing with physical goods, long-term contracts, or billable hours. Ownership, valuation basis, and the timing of revenue recognition all shift depending on the sector.

Manufacturing WIP

In product-based businesses, WIP represents physical goods mid-production. The manufacturer retains legal title to materials throughout the production cycle and can assign a net realisable value to unfinished units based on current market conditions.

Key considerations for manufacturing WIP:

- Overhead allocation requires judgement — typically based on machine hours, labour hours, or production volume

- Normal capacity drives fixed overhead allocation rates under IAS 2 paragraph 12, meaning seasonal production dips don't inflate per-unit overhead costs

- Abnormal waste must be excluded from WIP costs and expensed immediately

A precision engineering firm producing custom machinery components would capitalise direct materials (metals, electronics) and direct labour (machinist wages) into WIP. Allocated overheads — equipment depreciation, factory utilities — are added until components are complete and transferred to finished goods.

Construction WIP

Construction contracts raise a fundamental question: who owns what, and when? The contractor generally doesn't own the asset being built. Ownership of incorporated materials often passes to the client as work progresses, so WIP here represents the contractor's contractual rights rather than a physical asset.

Under IFRS 15 paragraph 35(b), revenue can be recognised over time when "the entity's performance creates or enhances an asset that the customer controls as the asset is created." Most construction contracts meet this criterion, triggering over-time revenue recognition using the percentage-of-completion method.

Construction WIP involves three key balances:

- Contract asset (underbilling) — revenue recognised exceeds amounts invoiced to date

- Contract liability (overbilling) — amounts invoiced exceed revenue earned to date

- Foreseeable losses — when estimated costs to complete exceed expected revenue, the full loss must be recognised immediately under IAS 37

A civil engineering contractor building a ₹20 crore bridge would track costs incurred (concrete, steel, subcontractors, site overhead), calculate percentage complete using the cost-to-cost method, recognise revenue proportionally, and compare progress billings to determine contract assets or liabilities.

Service Contracts WIP

Professional services firms — accountants, consultants, lawyers, architects — carry WIP as the value of services rendered but not yet billed. Under FRS 102 Section 23 and IFRS 15, revenue on service contracts is recognised over time using input methods (cost-to-cost or time-based).

If an advisory project is 60% complete based on hours incurred, 60% of the contract value should be reflected as earned revenue, with the unbilled portion appearing as a contract asset.

Key considerations for service WIP include:

- Time tracking accuracy — hours recorded drive revenue recognition, so billing systems must align with accounting records

- Engagement stage reviews — periodic assessments of percentage complete prevent material misstatements at period end

- Multi-jurisdiction reporting — firms serving clients across borders may need to reconcile WIP under different standards simultaneously

Cross-border engagements add another layer of complexity. A UK-based firm providing outsourced accounting services to an Indian subsidiary, for instance, may need to maintain WIP records under both FRS 102 (for UK statutory accounts) and Ind AS 115 (for Indian reporting).

The two standards can diverge on timing and cost allocation, requiring careful reconciliation at each reporting date — a challenge VJM Global manages routinely for international clients operating across jurisdictions.

How to Record WIP in Accounting: Journal Entries Explained

WIP accounting follows a fundamental principle: costs are debited to the WIP account as incurred and only transferred to Cost of Goods Sold or revenue when the contract or production run completes. The entries below walk through each stage — from recording direct costs to closing out a completed project — followed by a worked example showing underbilling and overbilling in practice.

Core Journal Entries Step-by-Step

Entry 1: Recording Direct Costs

When you purchase materials, pay labour, or engage subcontractors:

Debit: WIP – Direct Costs

Credit: Cash / Accounts Payable

This capitalises costs into the WIP asset rather than expensing them immediately.

Entry 2: Applying Production Overheads

Overheads are allocated to WIP based on a predetermined rate:

Debit: WIP – Overheads Applied

Credit: Manufacturing Overhead Control

The overhead control account accumulates actual overhead costs separately; any difference between applied and actual creates an under/over-applied variance cleared at period-end.

Entry 3: Recognising Revenue (Percentage-of-Completion)

As the project progresses, revenue is recognised even if no invoice has been issued:

Debit: Contract Asset (Accounts Receivable if billed)

Credit: Revenue

Entry 4: Recording Underbilling

When earned revenue exceeds amounts billed to date:

Debit: Contract Asset – Underbilling

Credit: Revenue (or Revenue Adjustment)

Underbilling represents money owed to you — the client has received value (your work) but hasn't been invoiced yet. This appears as a current asset.

Entry 5: Recording Overbilling

When invoiced amounts exceed revenue earned:

Debit: Cash / Accounts Receivable

Credit: Contract Liability – Overbilling (Deferred Revenue)

Overbilling represents money you owe in future performance — you've been paid for work not yet completed. This appears as a current liability.

Entry 6: Closing WIP at Project Completion

When work finishes, accumulated WIP transfers to cost of sales:

Debit: Cost of Goods Sold

Credit: WIP

This matches the full cost against the full revenue recognised across all periods.

Understanding Underbilling vs Overbilling

The distinction comes down to whether your invoicing is ahead of or behind your actual progress:

| Underbilling | Overbilling | |

|---|---|---|

| Situation | Work done exceeds amounts invoiced | Amounts invoiced exceed work done |

| Example | Earned ₹80,000; invoiced ₹60,000 — ₹20,000 gap | Invoiced ₹1,00,000; earned ₹70,000 — ₹30,000 gap |

| Balance Sheet | Current asset (contract asset) | Current liability (deferred revenue) |

| Meaning | Client owes you for completed work | You owe future performance to the client |

Worked Example: ₹20,00,000 Construction Contract

Contract details:

- Total contract value: ₹20,00,000

- Estimated total costs: ₹14,00,000

- Costs incurred to date: ₹5,60,000

- Progress billings issued: ₹6,00,000

Step 1: Calculate percentage complete

% Complete = ₹5,60,000 ÷ ₹14,00,000 = 40%

Step 2: Calculate revenue to recognise

Revenue = 40% × ₹20,00,000 = ₹8,00,000

Step 3: Determine billing position

Revenue recognised (₹8,00,000) exceeds billings (₹6,00,000) by ₹2,00,000 — this is underbilling.

Journal entries:

1. Record costs incurred:

Debit: WIP ₹5,60,000

Credit: Cash/Payables ₹5,60,000

2. Recognise revenue:

Debit: Accounts Receivable ₹8,00,000

Credit: Revenue ₹8,00,000

3. Record cash from [progress billing](/service/construction-bookkeeping-services):

Debit: Cash ₹6,00,000

Credit: Accounts Receivable ₹6,00,000

4. Resulting balance:

Contract Asset (Underbilling) = ₹2,00,000

The ₹2,00,000 contract asset appears on the balance sheet, representing work performed but not yet billed.

Accounting Policy Consistency

Once you choose between the completed-contract method (revenue only at project end) and the percentage-of-completion method (revenue as work progresses), you must apply it consistently across similar contracts.

Both IFRS 15 and Ind AS 115 require the over-time recognition method when contracts meet specific criteria — making the completed-contract approach increasingly rare, except for very short-duration work.

Where Does WIP Appear on Financial Statements?

WIP on the Balance Sheet

WIP sits as a current asset under the inventory section, alongside raw materials and finished goods. IAS 1 paragraph 54 lists inventories as one of the minimum required line items on the statement of financial position, and IAS 2 paragraph 37 recommends sub-classification into materials, work in progress, and finished goods where relevant.

Balance sheet presentation:

Current Assets:

Inventory

Raw Materials ₹45,000

Work in Progress ₹56,000

Finished Goods ₹78,000

Contract Assets (Underbilling) ₹20,000

Trade Receivables ₹1,20,000

Lower of cost and NRV: WIP must be measured at the lower of cost and net realisable value under IAS 2 paragraph 9 (Ind AS 2 for Indian entities). If estimated costs to complete a contract exceed expected revenue — creating a foreseeable loss — the full loss must be recognised immediately as a provision under IAS 37 paragraph 68, not deferred in WIP.

Contract assets (underbilling) and contract liabilities (overbilling) appear as separate line items under IFRS 15 / Ind AS 115 paragraphs 105-108, distinct from inventory. UK entities under FRS 102 may label these "amounts due from/to customers for contract work."

WIP on the Profit and Loss Account

WIP does not appear as a standalone line item on the P&L. This surprises many practitioners, but the mechanics become clear once you trace the two routes through which WIP affects reported results.

WIP's impact flows through the P&L indirectly via two routes:

- Revenue line: Under percentage-of-completion (IFRS 15 / Ind AS 115), revenue is recognised as work progresses regardless of billing timing. A ₹2,00,000 contract that's 40% complete shows ₹80,000 revenue even if only ₹60,000 has been invoiced.

- Cost of sales line: When WIP completes and transfers to COGS, accumulated costs hit the P&L. Manufacturing entities may show "changes in inventories of finished goods and WIP" as a separate line under the nature-of-expense method permitted by IAS 1.

Example P&L extract:

Revenue ₹12,00,000

Cost of Goods Sold (₹8,40,000)

Opening WIP ₹1,20,000

Costs Incurred ₹8,90,000

Closing WIP (₹1,70,000)

Gross Profit ₹3,60,000

The increase in WIP (₹50,000) reduces the cost of sales charge for the period, because those costs remain capitalised rather than expensed.

The Matching Principle

The purpose of WIP accounting is ensuring revenues and costs appear in the same period — not when cash is received or paid. A construction firm recognising ₹50,00,000 revenue on an 18-month project cannot wait until completion to expense ₹35,00,000 in costs; those costs must be matched to the revenue recognised each period.

Without WIP accounting, monthly profits become wildly distorted: massive losses in early project months (costs incurred, no revenue) followed by artificial profits at completion (full revenue, no costs).

How to Calculate WIP: Formula and Step-by-Step Walkthrough

Standard WIP Inventory Formula

The ending WIP balance for any period follows this cost accounting relationship:

Ending WIP = Beginning WIP + Costs Incurred During Period − Cost of Goods Completed

Example:

- Beginning WIP (1 January): ₹45,000

- Manufacturing costs incurred (January): ₹1,20,000

- Cost of goods completed and transferred (January): ₹1,10,000

- Ending WIP (31 January): ₹45,000 + ₹1,20,000 − ₹1,10,000 = ₹55,000

This formula applies to manufacturing environments where discrete units move through production. For long-term contracts, the percentage-of-completion method provides more precise tracking.

Percentage-of-Completion Calculation

The cost-to-cost input method, described in IFRS 15 paragraphs B14-B19, is the most widely used approach for construction:

% Completion = Costs Incurred to Date ÷ Estimated Total Contract Costs

Revenue to Recognise = % Completion × Total Contract Value

Step-by-step process:

- Determine total contract price — ₹50,00,000 for a commercial fit-out

- Estimate total expected costs — ₹38,00,000 (materials ₹18,00,000, labour ₹14,00,000, overheads ₹6,00,000)

- Track costs incurred to date — ₹19,00,000 spent by end of period

- Calculate percentage complete — ₹19,00,000 ÷ ₹38,00,000 = 50%

- Calculate cumulative revenue — 50% × ₹50,00,000 = ₹25,00,000

- Subtract previously recognised revenue — if ₹10,00,000 was recognised in prior periods, recognise ₹15,00,000 this period

- Compare to billings — if you've invoiced ₹22,00,000 total, you have underbilling of ₹3,00,000 (₹25,00,000 revenue − ₹22,00,000 billed)

Critical Exclusions Under IFRS 15

IFRS 15 paragraph B19 requires excluding costs that don't contribute to progress:

- Wasted materials from errors or inefficiencies

- Significant rework costs

- Materials purchased but not yet installed

A contractor who orders ₹5,00,000 of steel delivered to site but not yet incorporated into the structure cannot include that ₹5,00,000 in "costs incurred" for percentage-of-completion purposes — only costs representing actual progress count.

Estimation Risk and Regular Updates

If your total cost estimate proves wrong — say, ₹38,00,000 budgeted but ₹42,00,000 actual — both your percentage-complete figure and recognised revenue will be materially misstated. WIP accuracy depends entirely on the quality of the estimates beneath it.

Best practice requires revisiting total cost estimates at each reporting period as:

- Site conditions change (ground works, access delays)

- Material prices shift with market conditions

- Scope variations are agreed mid-contract

- Labour productivity diverges from original assumptions

Any change in estimate should be applied prospectively (adjusting future periods) and disclosed in the accounts. This is where auditor scrutiny is heaviest. The PCAOB has noted that auditors frequently fail to adequately test management's cost-to-complete assumptions — meaning businesses that cannot support their estimates with documented evidence face real audit risk. Keep contemporaneous records of every cost revision and the reasoning behind it.

WIP Accounting Best Practices and Common Mistakes

Most Common WIP Accounting Errors

1. Confusing billings with revenue

Issuing an invoice does not mean you've earned revenue. A contractor who bills 30% upfront but has completed no work has created a contract liability (overbilling), not revenue. Revenue recognition depends on performance, not payment terms.

2. Failing to update cost estimates regularly

Using a six-month-old cost estimate to calculate percentage complete produces unreliable figures. Material price increases, scope changes, and productivity variations all affect total expected costs. Update estimates at minimum quarterly — monthly for large or volatile contracts.

3. Ignoring foreseeable losses

When a contract becomes loss-making (total expected costs exceed contract value), you must recognise the full expected loss immediately under IAS 37 (Ind AS 37 for India-based entities), not defer it. A ₹20,00,000 contract with revised cost estimates of ₹23,00,000 requires a ₹3,00,000 provision in the current period.

4. Inconsistent overhead allocation

Applying different overhead rates to similar contracts, or switching allocation bases mid-project, distorts cost accumulation and percentage-of-completion calculations. Establish overhead rates at the start of each period and apply consistently.

Key Best Practices

Effective WIP management requires disciplined processes, not just technical knowledge:

- Update WIP schedules monthly — treat reconciliation as a standard month-end close activity, not a year-end exercise. Monthly updates catch errors early.

- Align project managers and finance teams — cost data quality depends on timely input from site managers. Set clear submission deadlines and standardised capture formats.

- Maintain separate WIP accounts per project — pooling contracts into a single account masks over/underbilling and distorts percentage-of-completion calculations.

- Document all change orders — reflect approved variations in total contract value before they affect revenue recognition, and maintain an audit trail linking each change order to value adjustments.

Regulatory Review Findings

The FRC's third thematic review of IFRS 15 (September 2020) — a useful international benchmark given IFRS 15's alignment with Ind AS 115 — examined 72 companies and found significant disclosure deficiencies:

- Performance obligations and timing of recognition not clearly described

- Significant judgements inadequately explained

- Movements in contract balances not sufficiently identified

- Inconsistency between strategic report and financial statement revenue information

These findings show that WIP errors often stem from inadequate documentation and governance, not technical misapplication of standards.

When to Outsource WIP Accounting

For businesses managing multiple concurrent projects — particularly those operating across jurisdictions — outsourcing WIP accounting eliminates errors and ensures compliance. Foreign companies entering India face dual-framework challenges: maintaining WIP records under Ind AS 2 and Ind AS 115 for statutory purposes while supporting parent-entity reporting under UK FRS 102 or IFRS 15.

A firm with cross-border expertise handles the full scope of WIP accounting across frameworks, including:

- Project-level WIP schedules and period-end journal entries

- Percentage-of-completion calculations under Ind AS 115

- Reconciliation across multiple reporting standards (IFRS, FRS 102, Ind AS)

- Audit-ready documentation and contract balance disclosures

This ensures cost data accuracy and timely revenue recognition without diverting management attention from core operations.

Frequently Asked Questions

What is work in progress in accounting?

Work in progress represents the value of partially completed goods or services sitting between raw materials and finished goods. It's classified as a current asset on the balance sheet and includes all accumulated costs — direct materials, direct labour, and allocated overheads — incurred to date on incomplete production or contracts.

How do you record a WIP in accounting?

WIP is recorded by debiting the WIP account as costs are incurred — materials, labour, and overheads — and crediting it when the project completes, transferring the balance to Cost of Goods Sold or finished goods. For long-term contracts, revenue is recognised using the percentage-of-completion method, with the gap between recognised revenue and billings creating either contract assets (underbilling) or contract liabilities (overbilling).

Where does WIP go on P&L?

WIP does not appear as a standalone line item on the profit and loss statement. Its effect flows through via the revenue line (as earned revenue is recognised using percentage-of-completion) and the cost of goods sold line (when completed WIP transfers out). The change in WIP balances indirectly reflects in gross profit, but WIP itself is a balance sheet account.

What is the equivalent of GAAP in the UK?

UK GAAP is governed by FRS 102, with larger listed companies using IFRS instead. For WIP, FRS 102 Section 13 covers inventory measurement, while the revised Section 23 (effective 1 January 2026) governs contract revenue recognition using a five-step model aligned with IFRS 15.

What is the difference between work in progress and work in process?

The distinction is industry convention, not regulatory requirement. "Work in process" typically refers to manufacturing environments where goods move quickly through production stages, while "work in progress" covers construction projects, service contracts, and longer-duration work. Both appear on the balance sheet as current assets and include the same cost components — labour, materials, and overhead.

What is the formula to calculate ending WIP inventory?

Ending WIP = Beginning WIP + Costs Incurred During Period − Cost of Goods/Contracts Completed. For construction and service contracts, apply the percentage-of-completion method: divide costs incurred to date by total estimated costs to get % complete, then multiply by contract value to determine revenue to recognise. The gap between recognised revenue and billings creates contract assets (underbilling) or contract liabilities (overbilling).