Introduction

Singapore businesses expanding into India often encounter references to "sales tax" in older contracts, due diligence documents, or conversations with Indian partners. This terminology causes real confusion — India no longer operates a sales tax system. On July 1, 2017, India replaced a fragmented network of central and state taxes with the Goods and Services Tax (GST).

For Singapore companies, this distinction matters. India's GST framework is far more complex than Singapore's single 9% GST rate administered by IRAS — it involves multiple tax components (CGST, SGST, IGST), four primary rate slabs (0%, 5%, 12%, 18%), and compliance obligations that vary based on transaction type, location, and business structure.

Misunderstanding these requirements leads to real consequences: registration delays, blocked input tax credits, and unexpected penalties.

This guide clarifies what sales tax meant historically in India, explains how the current GST system works, breaks down the September 2025 rate reforms, and details exactly what Singapore businesses must do to maintain compliance when operating in or selling to India.

Key Takeaways

- India abolished its fragmented sales tax system on July 1, 2017, replacing VAT, CST, excise, and service tax with GST

- GST operates through three components: CGST (central), SGST (state), and IGST (inter-state/imports)

- September 2025 reforms simplified rates to four slabs: 0%, 5%, 18%, 40%

- Singapore businesses must register for GST from their first taxable supply — no turnover threshold applies

- Digital service providers (SaaS, apps, streaming) must register and charge 18% IGST regardless of revenue

From Sales Tax to GST: Understanding India's Tax Transformation

Before 2017, India ran one of the most fragmented indirect tax systems in the world. The Central Sales Tax (CST) Act, 1956 governed inter-state trade, while 29+ states each administered separate Value Added Tax (VAT) regimes for intra-state transactions. This created a cascading tax problem — businesses paid tax on previously taxed inputs, with no unified mechanism to claim credits across state borders.

Why "Sales Tax" Still Appears

On July 1, 2017, GST replaced CST, VAT, service tax, central excise duty, and octroi through the 101st Constitutional Amendment. These taxes no longer exist in law.

Yet Singapore businesses still encounter "sales tax" references because:

- Legacy contracts drafted before 2017 retain the old terminology

- ERP systems in Indian companies sometimes preserve historical tax categories

- Informal usage persists among vendors unfamiliar with current GST nomenclature

What GST Did Not Replace

Three categories remain outside GST:

| Category | Tax Treatment | Relevance to Singapore Businesses |

|---|---|---|

| Petroleum products | Five items (crude oil, petrol, diesel, ATF, natural gas) remain under state VAT and central excise | Energy sector companies and logistics firms face dual tax regimes |

| Alcohol for human consumption | Continues under state excise laws | F&B importers and hospitality businesses must track separate compliance |

| Electricity | Exempt from GST via notification; states retain taxing rights | Manufacturing operations require separate state-level tax management |

Singapore businesses operating in these sectors should verify which tax regime applies. Legacy structures are still active and carry their own compliance obligations.

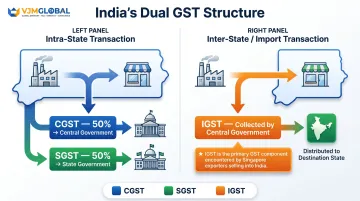

How India's GST Works: The CGST, SGST, and IGST Framework

India adopted a unique dual GST model where both central and state governments levy tax simultaneously on the same transaction.

Intra-State Transactions: CGST + SGST

When a supplier and buyer are located in the same Indian state:

- Central GST (CGST) is collected by the central government

- State GST (SGST) is collected by the state government

- Both are levied at equal rates, splitting the total GST burden 50:50

Example: An 18% GST on an intra-state sale becomes 9% CGST + 9% SGST.

Inter-State and Import Transactions: IGST

Integrated GST (IGST) applies when:

- Goods or services move between different Indian states

- Goods are imported into India from Singapore or any foreign country

- Services are supplied from outside India to Indian customers

IGST is collected by the central government and then shared with the destination state. This is the primary GST component Singapore exporters and service providers will encounter.

Destination-Based Taxation

Unlike the old origin-based CST, GST follows a consumption principle: tax revenue flows to the state where goods or services are consumed, not where they originate. For Singapore businesses structuring India supply chains, this means:

- Tax liability depends on the customer's location, not your warehouse/office location

- Multi-state operations require tracking IGST vs. CGST/SGST based on delivery addresses

- E-commerce and digital services always attract IGST when the customer is in India

Input Tax Credit (ITC)

Registered businesses can offset GST paid on purchases against GST collected on sales, preventing tax cascading. However, ITC is only available when:

- You hold a valid tax invoice from the supplier

- The invoice appears in GSTR-2B (auto-populated from the supplier's GSTR-1 filing)

- Your supplier has actually paid the tax to the government (verified via GSTR-3B)

Watch out for vendor compliance risk here: if your Indian supplier fails to file their GSTR-1 or doesn't pay tax via GSTR-3B, your ITC claim is blocked — even when you hold a valid invoice. This exposure is unique to India's GST system and catches many Singapore businesses off guard.

Reverse Charge Mechanism (RCM)

Beyond ITC risk, there's another compliance layer to account for. In certain transactions, the recipient — not the supplier — must pay GST directly. This applies when:

- You purchase goods or services from an unregistered Indian vendor

- You engage in specific notified service categories (legal services from advocates, director services, etc.)

Singapore businesses sourcing from small or informal Indian suppliers must self-assess and remit GST under RCM, then issue a self-invoice. Missing this obligation counts as non-compliance, even when the supplier is unaware of their own tax duties.

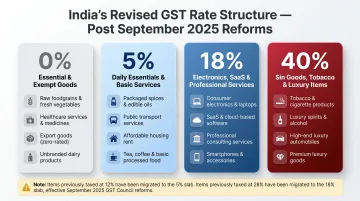

GST Rates in India After the 2025 Reforms

The 56th GST Council meeting on September 3, 2025 approved major rate simplification, effective September 22, 2025. The previous six-slab structure (0%, 5%, 12%, 18%, 28%, plus cess) was consolidated into four primary rates.

Current GST Rate Structure

| Rate | Category | Common Examples | |------|----------|-----------------|| | 0% (Nil/Exempt) | Essential food, healthcare, education, exports | UHT milk, paneer, life-saving drugs (33 types), exercise books, individual health insurance premiums | | 5% | Daily essentials, basic services | Soaps, toothpaste, packaged food, Ayurvedic medicines, hotel stays ≤ ₹7,500/night, tractors, spectacles | | 18% | Standard rate for most goods and professional services | TVs, ACs, dishwashers, cement, SaaS/digital services, professional services, electronics | | 40% | Sin/luxury goods | Tobacco, pan masala, aerated drinks, high-end cars, yachts, online gaming |

Migration impact: ~99% of items previously at 12% moved to 5%; ~90% of items at 28% moved to 18%. It's a meaningful simplification — but accurate HSN/SAC classification still determines which rate applies to your specific goods or services.

What Singapore Businesses Need to Know

Three rate scenarios apply most often to Singapore businesses dealing with India:

- Professional services (consulting, accounting, IT, design supplied to Indian clients) — 18% IGST

- Digital/SaaS products (subscriptions, streaming, app-based services to Indian customers) — 18% IGST, regardless of where your company is based

- Exported goods — zero-rated, meaning no GST is charged and exporters can claim ITC refunds on inputs

GST Exemptions

Certain supplies are entirely outside GST scope:

- Unprocessed agricultural products

- Healthcare services from registered medical practitioners

- Educational services from recognised institutions

- Specific financial services (insurance premiums, certain banking transactions)

Exempt suppliers cannot claim ITC on related purchases, creating a hidden cost. Singapore businesses acquiring exempt services in India should factor this into vendor pricing.

Zero-Rating for Exports

Exemption and zero-rating sound similar but work differently. Exempt supplies sit outside GST entirely; zero-rated supplies are taxed at 0% but remain within the GST system — meaning exporters keep their ITC entitlement.

Section 16 of the IGST Act provides that goods or services exported from India are zero-rated. This means:

- No GST is charged on the supply

- Exporters can claim refunds of accumulated ITC on inputs

- Alternatively, exporters may pay IGST upfront and claim a refund later

For Singapore importers purchasing from India, ensure your Indian supplier correctly zero-rates the export invoice — otherwise you may face double taxation.

OIDAR: Foreign Digital Service Providers

Online Information and Database Access or Retrieval (OIDAR) services supplied by foreign providers to Indian consumers require mandatory GST registration under Section 24(xi) of the CGST Act, regardless of turnover.

Who this affects:

- SaaS companies offering subscriptions to Indian users

- Streaming platforms (video, music, gaming)

- Cloud storage providers

- App-based services with Indian customers

Compliance requirements:

- Register for GST before making the first supply

- Charge 18% IGST on all B2C sales to Indian customers

- File GSTR-5A returns quarterly

- No ITC eligibility — non-resident OIDAR providers cannot claim input tax credits

Many Singapore tech companies miss this requirement entirely. Registration must be completed before your first supply to an Indian customer — not after your first tax period. Late registration typically triggers retrospective tax demands covering all prior sales, plus interest and penalties.

GST Registration and Compliance Obligations for Singapore Businesses in India

Who Must Register

Resident Indian businesses:

- Goods suppliers: ₹40 lakh annual turnover threshold

- Service providers: ₹20 lakh annual turnover threshold

- Special category states: ₹10 lakh threshold

Non-Resident Taxable Persons (NRTPs) — including Singapore companies:

- No turnover threshold — registration required from the first taxable supply

- Applies whether you have a physical presence in India or not

- OIDAR providers fall under Section 24(xi) with the same no-threshold rule

This is a critical difference from Singapore's S$1 million GST registration threshold. Every Singapore business making taxable supplies in India must register immediately.

Registration Process for Singapore Businesses

Singapore companies have two pathways:

1. Non-Resident Temporary Registration (NRTP):

| Requirement | Detail |

|---|---|

| Form | GST REG-09 via gst.gov.in |

| Lead time | Minimum 5 days before commencing business |

| Validity | 90 days, extendable once for another 90 days |

| Authorized signatory | Must be a resident Indian with valid PAN |

| Advance deposit | Estimated GST liability for registration period, paid in INR |

| Returns | GSTR-5 (monthly for NRTPs) or GSTR-5A (quarterly for OIDAR) |

Documentation required:

- Certificate of Incorporation (Singapore company)

- Tax Identification Number (UEN from ACRA)

- Passport/visa of authorized signatory

- PAN of Indian signatory

- Authorization letter

- Proof of principal place of business in India

- Indian bank account details

- Indian mobile number and email

2. Permanent Establishment (Subsidiary/Branch/LLP):

If establishing a legal entity in India, you'll obtain a permanent GSTIN and file regular returns (GSTR-1, GSTR-3B, GSTR-9).

Return Filing Obligations

Regular taxpayers (permanent establishments):

| Return | Frequency | Due Date | Purpose |

|---|---|---|---|

| GSTR-1 | Monthly | 11th of following month | Outward supply details |

| GSTR-3B | Monthly | 20th of following month | Summary return and tax payment |

| GSTR-9 | Annual | 31st December of following financial year | Annual consolidation |

QRMP scheme (for businesses with turnover ≤ ₹5 crore) allows quarterly filing with later due dates.

Penalties for non-compliance:

- Late tax payment: 18% per annum interest on net liability

- Late return filing: ₹50/day per return (₹25 CGST + ₹25 SGST); caps at ₹500-₹10,000 depending on turnover

- Non-filing consequences: Supplier's non-filing blocks customer's ITC, creating downstream compliance issues

GST-Compliant Invoicing

Staying current on returns is only half the equation — every taxable supply also requires a compliant invoice. Each invoice must show:

- Supplier's GSTIN and recipient's GSTIN (if registered)

- Invoice date and unique serial number

- HSN code (for goods) or SAC code (for services)

- Item description, quantity, and value

- Applicable tax rate (CGST/SGST/IGST percentages)

- Tax amount charged

- For exports: endorsement stating "SUPPLY MEANT FOR EXPORT"

Singapore businesses must ensure their Indian operations or vendors issue compliant invoices to preserve ITC eligibility. Missing or incorrect HSN/SAC codes can trigger notices.

VJM Global's GST Compliance Support

For Singapore businesses navigating India's GST complexity, working with an India-based advisor helps avoid costly errors. VJM Global has supported foreign companies entering India for over 30 years across 15+ industries, covering:

- GSTIN registration for non-residents and permanent establishments

- Return filing management (GSTR-1, GSTR-3B, GSTR-5, GSTR-5A, GSTR-9)

- ITC reconciliation and optimization

- RCM advisory for transactions with unregistered suppliers

- Vendor compliance monitoring to prevent ITC blocks

- HSN/SAC classification support to ensure correct rate application

Record Retention Requirements

Section 36 of the CGST Act mandates 72 months (6 years) of record retention from the annual return due date. If involved in an appeal or investigation, records must be kept for one year after final disposal or 72 months, whichever is later.

Singapore businesses must implement document management systems capable of supporting this requirement — significantly longer than most regional compliance requirements.

E-Way Bill Requirement

Inter-state movement of goods exceeding ₹50,000 requires an e-way bill generated via the e-way bill portal before transport. Singapore exporters shipping goods within India must integrate e-way bill generation into logistics workflows — a compliance step with no Singapore equivalent.

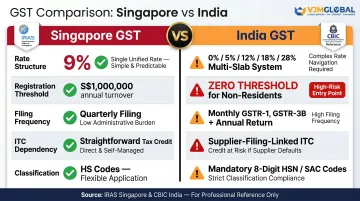

Singapore GST vs India GST: Key Differences to Know

Singapore businesses accustomed to IRAS's streamlined GST system face a steep learning curve in India.

Rate Structure Comparison

| Dimension | Singapore | India |

|---|---|---|

| Rate structure | Single uniform rate: 9% | Multiple slabs: 0%, 5%, 12%, 18%, 28% |

| Authority | IRAS (single national authority) | CBIC (central) + 28+ state tax departments |

| Classification | HS codes for goods | HSN codes (goods) + SAC codes (services) — 8-digit classification required |

| Registration threshold | S$1 million annual turnover | ₹40 lakh (goods) / ₹20 lakh (services) for residents; zero for non-residents |

| Return frequency | Quarterly (GST F5) | Monthly (GSTR-1, GSTR-3B) + annual (GSTR-9) |

Critical Operational Differences

Four differences catch Singapore businesses off guard most often:

- HSN/SAC classification is mandatory — every product and service needs an 8-digit code. Incorrect classification triggers rate mismatches and penalties. Singapore's HS code system for goods doesn't prepare businesses for this level of granularity.

- ITC depends on your supplier's compliance — India's GSTR-2B auto-population means your input tax credit claims are only as good as your vendor's filing discipline. If a supplier skips GSTR-1 or GSTR-3B, your claim is blocked.

- Each state has its own GST authority — audits and disputes involve state-level departments, not a single IRAS-equivalent touchpoint.

- E-way bills are required for inter-state goods movement — real-time electronic documentation with no Singapore parallel, adding logistics overhead.

Practical Implications for Singapore Businesses

These structural differences translate into concrete operational costs:

- Budget 3-5x your Singapore compliance spend — monthly filings, classification work, and vendor monitoring add up fast.

- Screen suppliers before onboarding — verify GST registration and filing history upfront. A non-compliant vendor blocks your ITC with no recourse after the fact.

- Invest in GST-compliant ERP or outsource — manual compliance at India's filing frequency is not viable at scale. Most Singapore businesses entering India work with a local compliance partner rather than building the capability in-house.

- Get India-specific GST expertise early — the classification and reconciliation requirements are distinct enough that general tax knowledge doesn't transfer directly. VJM Global works with international businesses across this transition, with a 95% client retention rate across the firms it supports.

Frequently Asked Questions

What is the sales tax rate in India?

India no longer has a "sales tax" — it was replaced by GST on July 1, 2017. Current GST rates are 0%, 5%, 18%, and 28% depending on the product or service category. The applicable rate requires correct HSN/SAC classification.

Is there VAT or GST in India?

India replaced VAT, service tax, excise duty, and CST with a unified GST system on July 1, 2017. VAT no longer applies to most goods and services, except items outside GST like alcohol for human consumption and petroleum products.

What is sales tax in India?

"Sales tax" referred to the Central Sales Tax (CST) on inter-state transactions and state-level VAT on intra-state sales. Both were absorbed into GST in 2017 and no longer apply to most businesses operating in India today.

Do Singapore businesses need to register for GST in India?

Yes. Non-resident businesses, including Singapore companies, must register for GST from their first taxable supply in India with no turnover threshold. Digital service providers selling to Indian consumers face mandatory registration regardless of revenue.

How does IGST apply to goods imported into India from Singapore?

Imports are subject to Integrated GST (IGST) levied at customs clearance, in addition to customs duty. Registered importers can claim IGST paid as Input Tax Credit if the goods are used for taxable business activities.

What GST returns must be filed by businesses operating in India?

Three primary returns apply: GSTR-1 (outward supplies, due the 11th), GSTR-3B (summary and tax payment, due the 20th), and GSTR-9 (annual return, due December 31). All are filed electronically — late filing triggers penalties and blocks your customers' ITC claims.

Need help with GST registration, return filing, or ITC claims in India? VJM Global's India tax specialists work with Singapore businesses on every stage of GST compliance — from initial registration through monthly filings, ITC optimization, and advisory. Reach out at info@vjmglobal.com or +91-9213397070 to get your India operations fully compliant from day one.