Introduction

Every UK business with employees carries a financial liability that too often goes unrecorded until an auditor flags it: earned but untaken annual leave. Holiday accrual accounting is how UK businesses calculate and record the monetary value of that untaken leave as a balance sheet liability. The obligation applies regardless of company size — yet finance managers, business owners, and HR professionals across UK-based companies, including foreign firms operating here, routinely overlook or miscalculate it.

The consequences extend beyond accounting accuracy. Errors in holiday accrual create compliance risk under both employment law and FRS 102 — the Financial Reporting Standard applicable to most UK companies since FRSSE was abolished in January 2016.

This guide covers:

- The legal basis for holiday pay entitlement in the UK

- How to calculate the accrued liability accurately

- The correct accounting treatment under FRS 102

Key Takeaways

- UK workers receive 5.6 weeks (up to 28 days) paid leave annually under the Working Time Regulations 1998

- Businesses must recognise earned but untaken holiday as a short-term employee benefit liability at financial year-end

- FRS 102 (paragraph 28.5) requires this liability to be recorded where it is material to the financial statements

- Calculate the accrual: multiply each employee's untaken earned days by their daily pay rate

- Even smaller businesses with modest accruals must calculate and disclose the liability at year-end

Why UK Businesses Must Account for Holiday Pay Accruals

The Legal Foundation

The Working Time Regulations 1998 establish that all workers — full-time, part-time, irregular hours, and agency — are entitled to paid statutory leave. Regulation 13 grants 4 weeks, while Regulation 13A provides an additional 1.6 weeks, totalling 5.6 weeks (28 days) for a five-day-per-week worker. This creates an ongoing employer obligation — one that qualifies as a financial liability the moment leave is earned.

The Accounting Obligation

FRS 102, which replaced FRSSE in January 2016, requires entities to measure short-term employee benefit obligations at the undiscounted amount (the full face value, without adjusting for the time value of money) expected to be paid. Paragraph 28.5 specifically addresses accrued but untaken holiday, mandating recognition when the liability exists. This applies to most UK companies regardless of size, though micro-entities following FRS 105 are not required to recognise this accrual in the same way.

Understanding Materiality

The accrual must be recorded if the value of untaken leave is materially significant relative to the company's overall financial position. Materiality exists when omitting, misstating, or obscuring information could reasonably influence decisions of primary users of financial statements. Determining materiality is a judgement call made in consultation with an auditor. Businesses should maintain accurate holiday records year-round to support that assessment.

Consequences of Non-Compliance

Getting this wrong carries real consequences. Failure to record holiday accruals can result in:

- Misrepresenting financial health to stakeholders, auditors, and HMRC

- Complications during audits or when seeking external investment

- Compounding adjustments when multiple years of unrecorded accruals surface at once — eroding stakeholder confidence at the worst possible time

How Holiday Accrual Is Calculated in the UK

The calculation follows a consistent three-step process. Before working through it, gather these inputs for each employee:

- Annual leave entitlement (statutory minimum or contractual)

- Leave year dates (which may not align with the financial year)

- Days of leave taken to date

- Daily pay rate (annual salary ÷ working days in the year)

For irregular hours and part-year workers in leave years beginning on or after 1 April 2024, a different rule applies: these workers accrue leave at 12.07% of hours worked in each pay period, rather than a fixed annual entitlement.

Step 1: Determine Days Earned to the Financial Year-End

Calculate what proportion of the leave year has elapsed by the financial year-end date.

Example: If the leave year runs April to March and the financial year ends December, 9 out of 12 months have elapsed = 75% of annual entitlement has been earned.

Multiply this percentage by the employee's full annual entitlement to get days earned.

Step 2: Subtract Days Already Taken

Deduct the number of leave days the employee has already taken during the current leave year from the days earned figure calculated in Step 1. The result is the number of accrued but untaken days at the financial year-end — the "holiday accrual deficit."

Step 3: Calculate the Monetary Value of the Accrual

Multiply each employee's accrued untaken days by their daily pay rate. For standard full-time employees, the daily rate = annual salary ÷ 260 working days (52 weeks × 5 days).

Sum the figures across all employees to arrive at the total holiday pay accrual liability.

Worked Example:

Greenfield Consulting Ltd has a financial year ending 31 December. Its holiday year runs 1 April to 31 March.

Employee: Sarah Thompson

- Annual salary: £36,000

- Annual leave entitlement: 28 days

- Leave year progress by 31 December: 9 months (75%)

- Days earned: 28 × 75% = 21 days

- Days taken: 14 days

- Accrued untaken days: 21 – 14 = 7 days

- Daily rate: £36,000 ÷ 260 = £138.46

- Accrual value: 7 × £138.46 = £969.22

Repeat this calculation for all employees and sum the totals to determine the company-wide holiday pay accrual liability.

How to Record Holiday Pay Accruals Under FRS 102

The Journal Entry

The holiday pay accrual is recorded as:

- Debit: Staff costs (wages/salaries expense) in the profit and loss account

- Credit: Accruals (a current liability) on the balance sheet

This ensures the cost is matched to the period in which the employee earned the leave, consistent with the accruals basis of accounting required under FRS 102.

Reversal and Re-Measurement

At the start of the next financial year, the accrual is reversed when leave is actually taken and paid out. Both steps — reversal and re-measurement — are part of the same standard cycle:

- Record accrual at year-end (31 December)

- Reverse accrual on 1 January when new year begins

- Record actual holiday pay as employees take leave

- Re-assess and record new accrual at next year-end

Disclosure Requirements

Where the accrual is material, businesses must describe their accounting policy for holiday pay in the notes to the financial statements. Auditors typically check for:

- Consistent application of the policy year on year

- Clear justification for any changes in methodology

- Adequate disclosure of those changes in the notes

Outsourcing and Data Integration

For UK businesses using outsourced accounting or payroll providers, the key risk is a disconnect between HR holiday records and the finance team's year-end figures. Accurate accruals depend on both sides sharing current data.

VJM Global's UK accounting outsourcing services help businesses maintain FRS 102 compliance by integrating payroll data with year-end reporting — so holiday balances are captured accurately before accounts are finalised.

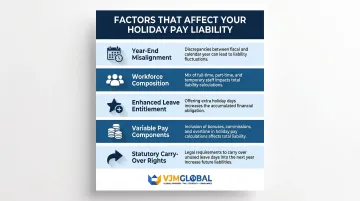

Factors That Affect Holiday Accrual Calculations in UK Businesses

Holiday accrual is rarely straightforward. Several factors — from your workforce structure to how your leave year aligns with your financial year — can materially change the liability figure on your balance sheet:

Year-end misalignment increases accrual exposure. A December financial year-end against an April holiday year-end creates a 9-month accrual window — three times larger than the reverse scenario.

Workforce composition drives calculation complexity. Irregular hours workers accrue at 12.07% of hours worked under rules effective from April 2024, while full- and part-time staff use the proportional entitlement method.

Enhanced leave entitlement raises the liability ceiling. If your contracts offer 30 days rather than the statutory 28, the full 30 days must feed into your accrual — not just the legal minimum.

Variable pay components must be included in holiday pay calculations. Under Bear Scotland v Fulton and subsequent UK case law, regular overtime, commission, and certain allowances apply to at least the first 4 weeks of leave — meaning base salary alone understates your true liability.

Statutory carry-over rights can inflate the following year's liability. Employees on maternity, paternity, adoption, or long-term sick leave may carry untaken leave forward, and balances brought from prior years compound the accrual further.

Each of these factors can shift your holiday pay liability by thousands of pounds. Getting the calculation right means identifying which applies to your workforce — and adjusting your accrual method accordingly before year-end.

Common Mistakes and Misconceptions in Holiday Accrual Accounting

"Only Large Companies Need to Record Accruals"

Many small businesses assume holiday accrual accounting only applies to large companies or listed firms. Since the abolition of FRSSE in January 2016, FRS 102 applies to most UK companies. The accrual obligation exists regardless of company size if the amount is material — a threshold that depends on the company's specific financial position, not its headcount.

Calculating Holiday Pay Using Base Salary Only

A critical error is excluding variable pay elements from the calculation. Following the Bear Scotland v Fulton employment tribunal ruling, UK employers must include the following in holiday pay for at least the 4 weeks of EU-derived leave:

- Regular overtime (both compulsory and sufficiently regular voluntary overtime)

- Commission and results-based payments

- Other payments received regularly as part of normal remuneration

Excluding these elements understates the accrual. It also creates retrospective liability, potentially exposing the business to backdated claims — subject to the three-month gap rule for series of underpayments.

"Aligning Holiday Year and Financial Year Eliminates the Accrual"

While aligning the holiday year with the financial year reduces timing differences, employees may still have untaken leave at the year-end that must be assessed. Leave management — sending reminders, capping carry-over contractually — can reduce but not always eliminate the need for an accrual entry. At year-end, the materiality check should confirm whether the value of untaken leave across the workforce crosses the threshold to warrant a balance sheet entry — regardless of how well leave has been managed during the year.

Frequently Asked Questions

How does holiday accrual work in the UK?

Holiday entitlement accrues based on time worked throughout the leave year. Full-time workers receive 5.6 weeks (28 days) annually; part-time workers receive a pro-rata amount, and irregular hours workers accrue at 12.07% of hours worked.

How much holiday do you accrue in 3 months in the UK?

After 3 months, a full-time worker accrues approximately 7 days of statutory leave — calculated as 28 days × 3 ÷ 12. Part-time workers receive a proportional amount based on their working pattern.

What are the rules for holiday pay in the UK?

Holiday pay must reflect the worker's normal pay, including regular overtime and commission for the first 4 weeks of leave. Workers must be paid during leave (not after), and rolled-up holiday pay is only permitted for irregular hours and part-year workers from April 2024.

Do you accrue holiday whilst on holiday in the UK?

Yes, Statutory holiday entitlement continues to accrue during annual leave, maternity, paternity, adoption leave, and sick leave. Workers cannot lose entitlement that built up during these protected periods, which can inflate accrual liabilities at year-end.

What is a holiday pay accrual under FRS 102?

Under FRS 102 paragraph 28.5, UK businesses must recognise the undiscounted cost of earned but untaken employee leave as a short-term benefit liability on the balance sheet at financial year-end, if the amount is material to the overall financial position.

Can unused holiday be carried over to the next leave year in the UK?

Workers can carry over up to 4 weeks of untaken statutory leave if they were unable to take it due to sickness or statutory leave (such as maternity leave), and must use it within 18 months. Employers may also permit additional carry-over through contractual agreement.