Introduction

Many UK SaaS founders discover—often too late—that standard accounting rules don't fit their business model. A customer paying £12,000 upfront for an annual subscription doesn't mean £12,000 in profit on day one. Recurring billing, advance payments, subscription upgrades, and multi-year contracts create timing complexities that generic bookkeeping simply cannot handle.

Misrecognised revenue triggers real consequences: P&L misstatements, incorrect corporation tax filings, failed audits, and investor distrust during fundraising.

This guide covers the essential pillars of UK SaaS accounting — the right revenue recognition standard (FRS 102 vs IFRS 15), deferred income mechanics, VAT classification, investor-grade metrics, and cost capitalisation rules. Whether you're pre-revenue or approaching Series A, you'll leave with a clear picture of what compliant, investor-ready SaaS books actually look like.

Key Takeaways

- UK private SaaS companies typically use FRS 102 Section 23; listed companies must apply IFRS 15

- Deferred revenue is mandatory under accrual accounting—cash received upfront sits as a liability until earned

- SaaS is classified as an electronically supplied service subject to 20% UK VAT (B2B uses reverse charge; B2C sales into the EU require OSS registration post-Brexit)

- Key investor metrics include ARR, net revenue retention, churn rate, and LTV:CAC ratio (minimum 3:1)

- Development costs can be capitalised under IAS 38/FRS 102 if six criteria are met

- SaaS subscription costs paid to vendors are typically expensed, not capitalised

What Makes SaaS Accounting Different in the UK

SaaS businesses sell access to a service over time, not a product handed over at a single point. That creates the central accounting challenge: cash receipt and revenue recognition are decoupled. When a UK customer signs a 12-month contract for £12,000 and pays upfront, only £1,000 is earned in month one.

The remaining £11,000 sits on the balance sheet as deferred revenue — a liability representing services not yet delivered.

UK limited companies must use accrual accounting under FRS 102; HMRC's cash basis is available only to sole traders and partnerships. This means deferred revenue treatment is mandatory from incorporation, not optional. Many founders accustomed to simple cash accounting find this jarring: £12,000 in the bank, £1,000 on the P&L.

SaaS-specific complexities that go beyond basic deferred revenue:

- Mid-contract subscription upgrades or downgrades require immediate revenue adjustments

- Bundled contracts (software + onboarding + support) must be decomposed into separate performance obligations

- Multi-year contracts create current and non-current deferred revenue splits

- Promotional discounts and usage-based pricing make calculating the transaction price harder than it looks

The cost of getting revenue recognition wrong:

- HMRC assesses corporation tax at 25% on accounting profit — incorrect revenue recognition creates tax exposure

- Investors conducting due diligence scrutinise revenue recognition policies; inconsistencies raise red flags

- The FRC's 2024/25 annual review identified revenue recognition as a persistent quality concern across UK corporate reporting

Revenue Recognition for UK SaaS: FRS 102 vs IFRS 15

Which Standard Applies

| Entity Type | Required Standard | Revenue Section |

|---|---|---|

| UK-listed companies (Main Market, AIM) | UK-adopted IFRS | IFRS 15 |

| Private companies (default) | FRS 102 | Section 23 |

| Large private companies (voluntary) | FRS 102 or IFRS | Section 23 or IFRS 15 |

| Small companies | FRS 102 Section 1A | Section 23 (simplified) |

Most UK SaaS companies are private and report under FRS 102. Listed groups must apply IFRS. Companies with international parent entities or those preparing for an IPO often adopt IFRS 15 proactively.

IFRS 15 Five-Step Model

IFRS 15 uses a detailed, prescriptive framework:

- Identify the contract – Signed agreement or accepted terms of service with commercial substance

- Identify performance obligations – Software access, onboarding, and training may each be distinct promises

- Determine transaction price – Include variable elements (usage fees), exclude taxes, adjust for discounts

- Allocate price across obligations – Use standalone selling prices; if unavailable, estimate using cost-plus or residual methods

- Recognise revenue – When (or as) each obligation is satisfied—monthly for subscriptions, at point of delivery for one-time services

Example: A £15,000 annual contract bundles software (£12,000 standalone price) + onboarding (£3,000 standalone price). Revenue is split proportionally: £12,000 recognised monthly over 12 months (£1,000/month); £3,000 recognised at go-live.

FRS 102 Section 23 Approach

For most private UK SaaS companies, FRS 102 sets the rules — and its approach differs in key ways.

FRS 102 uses a stage of completion method for service contracts. For standard SaaS subscriptions, this means recognising revenue evenly (ratably) over the service period — one-twelfth per month for annual contracts. The standard is less prescriptive than IFRS 15 but reaches similar outcomes for straightforward subscriptions.

Key points to know:

- Simpler framework: FRS 102 does not require the same level of performance obligation analysis as IFRS 15

- Policy choice on costs: Entities may capitalise or expense certain development costs if recognition criteria are met — a flexibility IFRS 15 does not offer on revenue treatment

- Amended FRS 102 (effective January 2026): Section 23 moves closer to IFRS 15 principles, particularly for multi-element contracts — early preparation is strongly advised

Multi-Element Arrangements

Bundled contracts are a common audit finding. Under IFRS 15, each promise must be assessed:

- Distinct: Customer can benefit from it separately (or with readily available resources) and it's separately identifiable

- Not distinct: Must be combined with other promises

Implementation fees are particularly tricky. If onboarding is essential for the customer to use the software (inseparable), revenue must spread over the subscription term. If the customer could use the software independently, implementation revenue is recognised at go-live.

Getting the distinction right matters at contract design stage, not just at audit. VJM Global works with UK SaaS businesses on accounting outsourcing that addresses multi-element contract treatment before it becomes a compliance finding.

Deferred Revenue and Accrual Accounting Explained

What is Deferred Revenue?

Deferred revenue (also called deferred income or unearned revenue) is a balance sheet liability representing cash received for services not yet delivered.

Concrete example: A customer pays £12,000 upfront for an annual subscription on 1 January.

- Day 1 journal entry:

- Debit: Cash £12,000

- Credit: Deferred Revenue £12,000

- Monthly recognition (each month-end):

- Debit: Deferred Revenue £1,000

- Credit: Revenue £1,000

By December 31, the full £12,000 has moved from deferred revenue (liability) to revenue (P&L).

Balance Sheet Classification

| Period | Classification | Amount |

|---|---|---|

| Revenue recognised within 12 months | Current liability | Pro-rata portion |

| Revenue recognised after 12 months | Non-current liability | Remainder |

For a 3-year contract billed £36,000 upfront: £12,000 current liability, £24,000 non-current liability at year-end.

Cash vs Accrual: Why Accrual is Mandatory

HMRC cash basis accounting is not available to limited companies—only sole traders and partnerships qualify. Every incorporated SaaS business must use accrual accounting under FRS 102 from day one.

Why this matters:

- Investor readiness: Cash accounting misrepresents business performance; investors expect accrual-basis financials showing deferred revenue growth

- Tax compliance: Corporation tax at 25% is assessed on accounting profit; deferred revenue correctly defers tax liability

- Audit requirement: Companies exceeding small company thresholds (£10.2M turnover, £5.1M balance sheet, 50 employees) must prepare audited accrual accounts

Getting the compliance foundation right also unlocks a strategic advantage — one that matters well beyond the tax return.

Strategic Value of Deferred Revenue

Beyond compliance, a growing deferred revenue balance signals:

- Customer confidence: Long-term commitments indicate product-market fit

- Cash flow strength: Upfront payments fund operations before services are delivered

- Forward revenue visibility: Investors view deferred revenue as contracted, pre-funded future revenue

For SaaS businesses seeking investment, a consistently growing deferred revenue balance is one of the clearest signals of recurring demand — it tells investors that future revenue is already contracted and funded.

Setting Up Deferred Revenue Correctly

Implementation checklist:

- Create dedicated liability accounts (current and non-current)

- Record advance payments to deferred revenue, not revenue

- Set up automated monthly deferral schedules

- Reconcile monthly: Opening Balance + New Billings – Recognised Revenue = Closing Balance

A deferred revenue reconciliation that doesn't tie is the first thing auditors scrutinise. Maintain contract-level schedules to support every balance sheet balance.

VAT and Tax Considerations for UK SaaS Companies

SaaS Classification: Electronically Supplied Services

HMRC classifies SaaS as an electronically supplied service (ESS) subject to 20% standard-rate VAT. The "minimal human intervention" test applies: if the service is delivered automatically over the internet (software access, updates, hosting), it qualifies as an ESS.

B2B vs B2C distinction:

| Customer Type | VAT Treatment | Who Accounts for VAT |

|---|---|---|

| B2B (UK) | Standard rate 20% | Supplier charges VAT |

| B2B (outside UK) | Reverse charge | Customer accounts for VAT in their country |

| B2C (UK) | Standard rate 20% | Supplier charges VAT |

| B2C (EU post-Brexit) | Local VAT rate | Supplier via OSS or local registration |

Post-Brexit EU VAT Obligations

UK SaaS companies are now non-EU businesses. For B2C digital service sales to EU consumers, you must either:

- Register for Non-Union OSS (One Stop Shop) in a single EU member state—file one quarterly return covering all EU B2C sales

- Register for VAT individually in every EU member state where you have consumers

OSS is the practical choice for most SaaS companies. Failure to register creates backdated VAT liabilities.

International sales: Non-EU international customers (such as those in the USA and Australia) generally fall outside UK VAT scope, but local digital services taxes may apply depending on jurisdiction.

R&D Tax Relief: Merged Scheme (April 2024 onwards)

| Scheme | Rate | Eligibility | Net Benefit |

|---|---|---|---|

| Merged RDEC | 20% expenditure credit | All trading companies | ~15p per £1 (net of 25% CT for profitable companies) |

| ERIS | Additional 86% deduction + 14.5% payable credit | Loss-making SMEs with R&D ≥ 30% of total expenditure | Higher net benefit for R&D-intensive startups |

Qualifying SaaS development activities:

- Building novel algorithms or architectures involving technical uncertainty

- Developing platform features not achievable using publicly available methods

- Solving scalability or security challenges beyond the capability of competent professionals

- Creating bespoke integration layers

Cloud and data costs became claimable from April 2023. For context, SaaS companies in the Information & Communication sector account for roughly 22% of all UK R&D claims — with the average claim reaching £57,000. That figure gives a useful benchmark when assessing whether a formal claim is worth pursuing.

R&D relief also feeds directly into your corporation tax position, which makes understanding CT timing equally important.

Corporation Tax Timing

SaaS revenue is taxed when earned (per FRS 102 recognition), not when cash is received. For companies collecting large annual prepayments, this directly reduces current-year taxable profit — only the monthly earned portion counts.

HMRC alignment: Corporation tax follows accounting profit. Incorrectly recognising annual contracts upfront (mimicking cash basis) can trigger HMRC enquiries and backdated assessments.

VJM Global works with UK-based SaaS businesses on VAT compliance across jurisdictions and R&D relief claims — a practical combination given how closely these obligations interact at the year-end.

Key SaaS Financial Metrics to Track

Foundation Metrics: MRR and ARR

Monthly Recurring Revenue (MRR): Sum of all recurring subscription revenue in a given month

Annual Recurring Revenue (ARR): MRR × 12

Critical distinction: ARR excludes one-time fees (setup, consulting, hardware). Statutory turnover under UK GAAP includes all income sources. ARR is typically lower than statutory turnover but is the metric investors use for valuation multiples.

Customer-Level Metrics

| Metric | Calculation | Healthy Benchmark |

|---|---|---|

| CAC (Customer Acquisition Cost) | Total sales & marketing spend ÷ new customers acquired | Varies by segment |

| LTV (Lifetime Value) | ARPU × gross margin ÷ churn rate | 3× to 5× CAC |

| LTV:CAC Ratio | LTV ÷ CAC | Minimum 3:1; target 5:1 |

| Churn Rate (monthly) | Churned MRR ÷ Starting MRR | <3.7% at £1M–£3M ARR |

| NRR (Net Revenue Retention) | (Starting MRR + Expansion – Contraction – Churn) ÷ Starting MRR | Above 100%; best-in-class 120%+ |

Churn Benchmarks by Stage

Data from ChartMogul's SaaS benchmarks report shows median monthly customer churn decreases as companies scale:

| ARR Range (£) | Median Monthly Churn | Top Quartile |

|---|---|---|

| Below £230k | 6.5% | 3.2% |

| £770k–£2.3M | 3.7% | 2.2% |

| £6M–£11.5M | 3.1% | 2.0% |

Source data originally in USD; figures converted to GBP at approximate rate.

Early-stage churn above these medians signals product-market fit risk. Passive churn from failed payments can account for up to one-third of total churn.

Bookings vs Billings vs Revenue

Common confusion point:

- Bookings: Total contract value signed (£36,000 for a 3-year deal signed today)

- Billings: Invoiced amounts (£12,000 if billed annually)

- Revenue: What's recognised in the P&L (£1,000 per month under FRS 102)

Only revenue appears in statutory accounts. Mixing these metrics in board packs or investor updates creates confusion and can undermine trust with investors or board members.

Series A Due Diligence Expectations

Investors typically expect:

- ARR: £1.2M–£2.3M baseline

- YoY growth: 2×–3×

- Gross margin: 70%+

- NRR: Above 100%

- LTV:CAC: Above 3:1

- CAC payback: Below 18 months

Deferred revenue growth trends, revenue recognition policy documentation, and contract-level schedules are scrutinised during due diligence. Have these prepared at least six months before you begin fundraising conversations — investors will ask for them in the first data request.

Can You Capitalise SaaS Costs in the UK?

For SaaS Vendors: Internally Developed Software

IAS 38 / FRS 102 Section 18 allows capitalisation of development-phase costs if all six criteria are met:

| Criterion | Requirement |

|---|---|

| Technical feasibility | Can you complete the asset so it's available for use/sale? |

| Intention | Do you intend to complete and use/sell it? |

| Ability | Can you actually use or sell it? |

| Future economic benefits | How will it generate probable future benefits? |

| Resources | Do you have adequate technical, financial, and other resources? |

| Reliable measurement | Can you reliably measure expenditure during development? |

Research-phase costs must always be expensed. Only development-phase costs meeting all six criteria qualify for capitalisation.

Documentation requirement: Contemporaneous evidence of each criterion is mandatory. Auditors will challenge capitalisation without robust support.

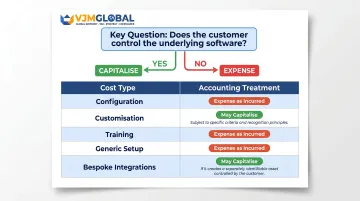

For SaaS Customers: Subscription Costs Paid to Vendors

IFRIC (IFRS Interpretations Committee) 2019 and 2021 agenda decisions clarified: SaaS arrangements where the customer does not control the underlying software are service contracts. Configuration and customisation costs are typically expensed, not capitalised.

The control test: Can the customer move the software on-premise or obtain it independently of the vendor?

- No: Service contract → expense costs as incurred

- Yes: Intangible asset → may qualify for capitalisation under IAS 38

Most SaaS customers fail this test. Hosted, subscription-based access gives you no ownership or control over the underlying code.

Implementation Costs: Line-by-Line Assessment

| Cost Type | Treatment |

|---|---|

| Configuration (setting flags/switches) | Expense as incurred |

| Customisation (modifying code you control) | May capitalise if control test met |

| Training | Always expense |

| Generic setup | Expense as incurred |

| Bespoke integrations (customer controls code) | May capitalise if distinct from SaaS access |

KPMG UK guidance: The right to move software must be substantive — assessed against financial feasibility (low costs, no penalties), operational impact (no functionality loss), and resource availability (qualified IT personnel). This requires significant professional judgment; involve auditors early when significant sums are at stake.

That judgment also carries real commercial consequences. Capitalisation increases EBITDA (costs hit the balance sheet, not P&L); expensing reduces EBITDA immediately. This distinction matters during M&A valuations.

Frequently Asked Questions

Can you capitalise SaaS costs in the UK?

UK SaaS vendors may capitalise internally developed software costs during the development phase under FRS 102 Section 18 or IAS 38 if all six mandatory criteria are met. SaaS subscription costs paid to third-party vendors are generally expensed as incurred unless the customer controls the underlying software—a test most SaaS customers fail.

Is SaaS taxable in the UK?

Yes. SaaS is treated as an electronically supplied service subject to UK VAT at the standard rate of 20%. B2B supplies typically use the reverse charge (customer accounts for VAT); B2C supplies require the vendor to charge VAT based on customer location. Corporation tax applies to accounting profit in the normal way.

What is the difference between FRS 102 and IFRS 15 for UK SaaS companies?

FRS 102 is the default UK GAAP standard for private companies, using a simpler "stage of completion" approach for service revenue. IFRS 15 applies to listed or international groups and uses a detailed five-step model with explicit performance obligation identification. For standard SaaS subscriptions, both standards typically produce the same result: monthly ratable revenue recognition.

What is deferred revenue and why does it matter in SaaS?

Deferred revenue is the portion of upfront cash received that hasn't yet been earned. It sits as a liability on the balance sheet, released into revenue as the service is delivered. Accurate treatment affects P&L reporting, corporation tax timing, and investor confidence in forward revenue visibility.

When should a UK SaaS startup switch from cash to accrual accounting?

This is largely moot for incorporated SaaS businesses—UK limited companies cannot use cash basis and must use accrual accounting from incorporation. The practical trigger is incorporation itself, not an ARR milestone. Delaying proper accrual implementation requires costly restatement work during fundraising or audit preparation.

What SaaS metrics do UK investors look at most closely?

ARR, MRR, net revenue retention (NRR), monthly churn rate, and LTV:CAC ratio are primary metrics. Investors expect LTV:CAC above 3:1, NRR above 100%, and gross margins of 70%+. Deferred revenue growth is also viewed as a positive signal of business health and customer commitment.