Introduction

In September 2014, Tesco announced a profit overstatement that would become one of the most significant accounting scandals in UK retail history. The FCA's final notice confirmed a total overstatement of £284 million across multiple periods, principally caused by the accelerated recognition of commercial income — payments from suppliers for promotions and rebate arrangements — and delayed accrual of costs. The Serious Fraud Office imposed a £129 million fine, whilst the FCA required approximately £85 million in investor redress. For UK finance teams managing supplier and customer rebate agreements, this case demonstrates the material consequences of rebate accounting failures.

Those consequences make the accounting treatment of rebates a compliance priority, not just a technical footnote. This guide covers the essential procedures under UK-applicable standards — IFRS 15 for listed companies and FRS 102 for smaller entities — along with the most common challenges UK businesses face and practical steps to improve accuracy.

Whether you manage volume-based supplier agreements, tiered customer incentives, or product mix rebates, getting the treatment right is essential to avoid audit exposure, HMRC complications, and financial misstatement.

TLDR:

- Rebates are recognised when earned — customer rebates reduce revenue; supplier rebates reduce cost

- IFRS 15 and revised FRS 102 both require the "highly probable" constraint for variable consideration, with mandatory reassessment at each reporting date from January 2026

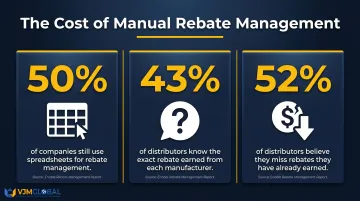

- 50% of companies still use spreadsheets for rebate management, creating material risk of missed accruals

- VAT treatment under HMRC Brief 6/2019 requires actual refunds before VAT adjustments, with credit notes issued within 14 days

- Robust documentation of rebate terms and accrual methodology is the first line of defence in any HMRC or audit review

What is Rebate Accounting and Why Does It Matter for UK Businesses?

Rebate accounting is the process of recording, tracking, and reporting financial incentives paid to customers or received from suppliers after transactions occur. Unlike straightforward discounts applied at the point of sale, rebates are retroactive — they depend on conditions met after the initial purchase, such as volume thresholds or spending targets. This timing difference creates distinct accounting treatment requirements.

UK Standards Context

UK accounting treatment for rebates depends on the reporting framework:

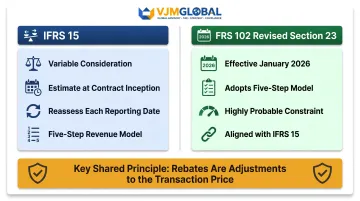

IFRS 15 (Revenue from Contracts with Customers): UK-listed companies follow IFRS 15, which treats rebates as variable consideration. Rebates must be estimated at contract inception, with revenue or cost adjusted accordingly. The standard requires reassessment at each reporting date.

FRS 102 (Revised Section 23): Smaller UK entities follow FRS 102. The revised Section 23, effective for accounting periods beginning on or after 1 January 2026, adopts the same five-step revenue recognition model and "highly probable" constraint as IFRS 15, eliminating previous differences.

Both frameworks require rebates to be treated as **adjustments to the transaction price** — not standalone expenses or income — and recognised when the underlying sale occurs, not when cash changes hands.

Why Accurate Rebate Accounting Is Non-Negotiable

Misstated rebate figures distort revenue, affect profit margins, and create audit exposure. The scale of this problem is significant: 50% of companies still rely on spreadsheets for rebate management (Enable's 2025 State of Volume Rebates report), and 52% of distributors believe they don't receive all rebates they actually earn.

Getting it wrong carries real consequences:

- Investor misleading: Overstated revenue or understated costs misrepresent business performance

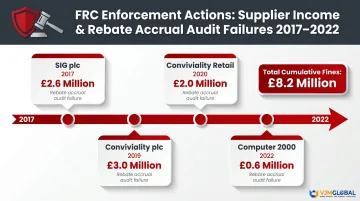

- FRC enforcement exposure: Four cases since 2017 have resulted in fines totalling £8.2 million for audit failures on supplier rebates

- HMRC compliance risk: Incorrectly treated rebates can trigger VAT adjustment requirements

Types of Rebates and How Each Is Treated in UK Accounting

Customer Rebates

Customer rebates are post-purchase incentives given to buyers, typically to drive volume or loyalty. Under IFRS 15, these constitute variable consideration — the seller must estimate the rebate amount at the time of sale and reduce revenue accordingly.

Accounting treatment:

- Debit revenue (or create a contra-revenue account)

- Credit a rebate liability account

- When the customer claims the rebate, settle the liability

- If unclaimed after the expiry period, reverse the liability back to revenue

The liability sits on the balance sheet until the rebate is paid or the claim window closes.

Supplier/Vendor Rebates

Supplier rebates are incentives received by a business from its supplier for meeting purchase milestones. These reduce the cost of goods sold (COGS) — not revenue — and must be accrued in the period they are earned, not when cash is received.

Accounting treatment:

- Debit rebate receivable (asset)

- Credit cost of goods sold (reducing purchase costs)

- When cash is received, debit cash and credit the receivable

- Note: The rebate reduces purchase cost — booking it as income is a misclassification

The IFRIC's November 2004 agenda decision confirms that rebates received as a purchase price reduction must be deducted from inventory cost, not recognised as income.

Volume and Tiered Rebates

Volume and tiered rebate structures reward higher purchase quantities. UK finance teams encounter two main calculation approaches:

- Retroactive tiers: The highest rate achieved applies to the total volume once the threshold is crossed. A small volume increase can trigger a significant liability adjustment.

- Progressive tiers: Each spending band earns a different rate, with lower bands locked in as higher tiers are achieved.

Retroactive structures create substantially more accounting complexity because crossing a tier threshold can suddenly increase the total rebate liability across all purchases.

Value Incentive and Product Mix Rebates

Two additional rebate types require separate accrual approaches:

- Value incentive rebates: Based on total spend value rather than volume; the accrual rate must be recalculated each period as cumulative spend grows.

- Product mix rebates: Reward purchasing specific product combinations or maintaining a target portfolio mix; each product line may carry a different rebate rate.

For UK finance teams, correctly classifying the rebate type before setting up accruals matters. A supplier rebate coded as income rather than a COGS reduction, for example, inflates gross profit and distorts margin reporting across every affected period.

Step-by-Step Rebate Accounting Procedures

Accounting for Customer Rebates

Journal entry process:

At point of sale:

- Debit: Revenue (or Rebate Expense)

- Credit: Rebate Liability

- Amount: Estimated rebate based on expected volume/value

When customer claims rebate:

- Debit: Rebate Liability

- Credit: Cash (or Accounts Payable)

If rebate goes unclaimed:

- Debit: Rebate Liability

- Credit: Revenue

- Timing: Once claim window closes per documented policy

Accounting for Supplier Rebates

With customer rebate entries established, supplier-side accounting follows a parallel structure — but with one important distinction in how the rebate is classified.

Journal entry process:

When rebate is earned (purchase milestone met):

- Debit: Rebate Receivable

- Credit: Cost of Goods Sold (reducing purchasing costs)

When rebate is received:

- Debit: Cash

- Credit: Rebate Receivable

Important: The rebate must not be recorded as income. It is a cost reduction that lowers COGS — misclassifying it inflates revenue and distorts gross margin reporting.

Inventory Rebate Accounting

When a rebate is earned at the point of purchase, it reduces the cost basis of inventory held. This reduction cannot flow through to the profit and loss statement until the relevant stock is sold.

Example — UK distributor:

A distributor purchases £100,000 of goods and receives a 5% supplier rebate (£5,000). Inventory is recorded at £95,000. If only 60% of the stock is sold during the period:

- Inventory on balance sheet: £38,000 (40% × £95,000)

- COGS recognised: £57,000 (60% × £95,000)

- Rebate benefit in P&L: £3,000 (60% × £5,000)

Recording the full £5,000 rebate as income immediately — before the stock is sold — is a common error that distorts profit and violates IAS 2 requirements.

Accrual Recalculation Throughout the Year

Inventory treatment connects directly to how accruals are managed across the year. Multi-tier rebate agreements require ongoing recalculation as purchase volumes shift — not a single year-end adjustment.

Finance teams should reassess accruals at each reporting period to comply with IFRS 15 paragraph 59 and FRS 102 paragraph 23.55. Key triggers for recalculation include:

- Crossing a new volume or spend threshold

- Receiving updated forecasts from suppliers or customers

- Quarter-end and half-year reporting periods

- Material changes in purchasing patterns mid-year

Documentation Requirements

Accurate accruals mean little without supporting evidence. To satisfy UK GAAP or IFRS and maintain an audit trail, retain:

- Rebate agreements (signed contracts with clear terms)

- Purchase records showing progress toward thresholds

- Accrual calculations with methodology notes

- Claim evidence (invoices, credit notes, payment confirmations)

Rebate Accruals and Year-End Considerations in the UK

A rebate accrual is the amount of rebate earned but not yet received (supplier side) or owed but not yet paid (customer side). Under both IFRS 15 and FRS 102, accruals must reflect the economic reality of when the rebate is earned, not when cash moves. This makes accurate forecasting essential for UK finance teams preparing year-end accounts.

Over Accruals and Under Accruals

Both directions of error carry consequences:

- Over accruals: Finance teams set aside too much, inflating liabilities and overstating expenses in the current period

- Under accruals: Recording too little artificially boosts short-term profits but forces reversals in the next period

Under accruals in one period create a catch-up adjustment in the next. Auditors scrutinise patterns that suggest intentional manipulation, and in extreme cases, systematic under-accrual can lead to earnings restatements and regulatory action.

Between 2017 and 2022, the FRC imposed fines totalling £8.2 million across four enforcement cases (SIG plc, Conviviality plc, Conviviality Retail, and Computer 2000) for audit failures specifically related to supplier income and rebate accruals.

Year-End Revenue Recognition Challenges

Rebate-heavy industries — building supplies, wholesale distribution, buying groups — face particular year-end pressure. Finance teams must:

- Close the year with accurate rebate income and liability balances

- Reconcile all outstanding rebate agreements

- Ensure variable consideration estimates under IFRS 15 are defensible and well-documented

- Review whether the "highly probable" constraint still holds for each individual estimate

46% of manufacturers spend one month or more on year-end reconciliation for rebate reporting — a figure that underscores how far manual processes still dominate this area.

VAT Implications for UK Businesses

HMRC guidance affects both VAT recovery and accounting entries. Under Revenue and Customs Brief 6/2019, a price decrease (rebate as a reduction in the original supply price) is recognised for VAT purposes only when a refund is actually made to the customer.

Key requirements:

- VAT adjustment occurs in the period when the refund takes place

- Credit notes must be issued within 14 days of the refund

- Both supplier and customer must adjust VAT by the same amount

- Exception: Fully taxable businesses may mutually agree not to adjust VAT (VAT Notice 700, Section 18)

This timing rule means rebate accruals for accounting purposes may not align with VAT adjustments, requiring period-by-period reconciliation.

Common Challenges in Rebate Accounting for UK Businesses

Complexity of Tracking and Accruals Management

Rebate agreements often span multiple tiers, timeframes, and product categories. Finance teams managing these manually — typically via spreadsheets — face high risk of miscalculation, missed milestones, and incorrect period allocation.

The scale of manual management remains significant: 50% of companies still rely on spreadsheets for rebate management, whilst 33.3% of manufacturers use Excel to administer rebate programmes.

In sectors like building materials, large distributors may manage agreements with over 600 different suppliers. One retailer discovered £154,000 in unaccrued rebates within eight weeks of digitising their process.

Communication Breakdowns and Agreement Ambiguity

Sales teams negotiate rebate deals, but accounting teams must execute them. When contract terms are unclear or not shared promptly with finance, accruals are set up incorrectly from the start.

In the UK, this is compounded by multi-party agreements common in wholesale and distribution — particularly where buying groups pool volume across members. The downstream effect on finance teams is measurable:

- Only 43% of distributors know the exact rebate amount earned from each manufacturer

- Incorrect accrual set-up at contract stage compounds errors throughout the financial year

- Delayed contract sharing between sales and finance means adjustments are reactive, not planned

Balance Sheet and Audit Risks

Unclaimed customer rebates sit as liabilities indefinitely unless actively managed, whilst unrecorded supplier rebate receivables understate assets — both distort the balance sheet in ways that trigger audit queries and can affect creditworthiness or investor confidence.

FRC enforcement actions have repeatedly cited auditor failures to challenge rebate accruals and supplier income recognition. UK businesses facing audit should expect direct questions on accrual methodology, supporting documentation, and how period-end estimates were derived.

How to Improve Your Rebate Accounting Processes

Establish Clear Internal Procedures

Document a written rebate accounting policy that defines:

- How each rebate type is classified (customer vs. supplier, revenue vs. cost)

- When accruals are created and reversed

- Who is responsible at each stage (commercial, finance, operations)

- Review frequency and approval requirements

This eliminates subjective decision-making and creates consistency across reporting periods.

Centralise and Standardise Rebate Agreements

Ensure all rebate deals are documented in a central system (even a structured template) before accounting entries are made. Finance teams should be involved at the agreement stage — not just at month-end — so accrual logic aligns with commercial terms from day one.

For UK businesses managing a high volume of supplier or customer agreements, outsourcing rebate accounting can significantly reduce errors, missed accruals, and audit exposure. VJM Global works with 250+ UK businesses on accounting solutions covering IFRS 15, FRS 102, and HMRC compliance, helping finance teams maintain accurate rebate positions year-round.

Consider Specialist Software or Expert Support

Rebate management software handles several time-consuming tasks that are easy to get wrong manually:

- Calculates accruals automatically as deal terms change

- Tracks progress against volume or spend thresholds in real time

- Produces structured reports ready for internal review or external audit

For businesses not yet investing in dedicated tools, working with an experienced accounting firm achieves the same outcome — compliant procedures and a year-end position that holds up under scrutiny.

Given that 87% of distributors report rebates are critical to profitability, the cost of poor rebate accounting — in errors, delays, and audit exposure — typically far exceeds the cost of getting the right systems or support in place.

Frequently Asked Questions

How do you account for rebates in accounting?

Rebates are recorded as a liability (for customer rebates) or a receivable/cost reduction (for supplier rebates) at the time the underlying transaction occurs. Adjustments are made when rebates are claimed, paid, or expire unclaimed, so accruals match when the obligation or entitlement arises — not when cash moves.

Is a rebate an asset or a liability?

It depends on perspective: a supplier rebate receivable is an asset on the buyer's books, whilst a customer rebate owed to buyers is a liability on the seller's books. Both must be recognised when earned, not when cash is exchanged.

How to account for supplier rebates?

Debit the rebate receivable and credit COGS when the purchase milestone is met, then reverse this entry against cash on receipt. The rebate reduces cost of goods — it must also reduce inventory value if the related stock remains unsold.

What is the difference between a rebate and a discount in UK accounting?

A discount reduces the price at the point of sale and is recorded immediately as a revenue reduction. A rebate is a retroactive payment made after purchase conditions are met, requiring separate liability or receivable recognition and accrual treatment until conditions are fulfilled.

How does IFRS 15 affect rebate accounting in the UK?

Under IFRS 15, rebates are variable consideration — UK businesses must estimate the amount at contract inception, reduce revenue or COGS accordingly, and reassess at each reporting date. Recognition is constrained until a significant reversal becomes highly improbable.