Introduction

India has emerged as one of the world's fastest-growing major economies, recording 6.5% GDP growth in FY24-25 and projected to become the 3rd-largest economy by 2031. For UK entrepreneurs, the opportunity is compelling: a market of 1.4 billion people, a rapidly expanding middle class, and government-driven reforms that have removed barriers to foreign investment.

UK businesses also bring natural advantages: shared common law legal traditions, English as the primary business language, and the landmark UK-India Comprehensive Economic and Trade Agreement (CETA) signed in July 2025, which eliminated tariffs on 99% of Indian goods and opened public procurement worth £38 billion annually.

Despite these tailwinds, entering the Indian market means navigating regulatory, structural, and compliance requirements that are specific to the country.

This guide gives UK entrepreneurs a practical, step-by-step resource for legally structuring, registering, and operationalising a business in India — covering everything from choosing the right entity type to meeting ongoing compliance obligations.

Key Takeaways

- India permits 100% foreign direct investment (FDI) in most sectors under the automatic route — no prior government approval needed

- UK entrepreneurs can choose from Private Limited Company, Limited Liability Partnership (LLP), Branch Office, or Liaison Office — each with different control and compliance implications

- Company registration via the Ministry of Corporate Affairs (MCA) typically takes 10–20 working days when documents are in order

- Ongoing compliance covers GST, Income Tax (including TDS), FEMA reporting, and annual MCA filings — plan for these from day one

- An India-based advisory partner reduces setup time and helps avoid costly compliance errors — VJM Global has guided 250+ UK businesses through this process

Why UK Entrepreneurs Are Choosing India Right Now

India offers UK businesses an unusual convergence: a fast-growing economy, a rapidly expanding consumer base, and now a free trade agreement that reduces the cost of entry. Each of these factors is significant on its own. Together, they make 2025 a particularly practical moment to act.

GDP Growth and Economic Scale

India's 6.5% GDP growth in FY24-25 outpaces all other major economies. Currently the 6th-largest economy globally at approximately USD 4.15 trillion, the IMF projects India will retake the 4th position in 2027 and become the world's 3rd-largest economy by 2031. For context, that trajectory puts India ahead of Japan and Germany within a decade.

Consumer Class Expansion

By 2036, India's middle class and affluent consumers will account for 93% of all spending, up from 80% in 2026. India will have 499 "consumer cities" by 2035 — more than double the 2026 figure — and 149 cities with at least half a million consumers each, surpassing Europe (112) and the US (53). That scale of urban consumer growth has no equivalent in any other emerging market right now.

UK-India Bilateral Trade Momentum

That consumer base is now more accessible to UK businesses than ever. Total UK-India trade reached £47.4 billion for the four quarters ending Q3 2025, up 11.7% year-on-year. The UK-India CETA, signed in July 2025, eliminated tariffs on 99% of Indian goods and reduced UK tariffs on 90% of lines. Whisky tariffs dropped from 150% to 75% immediately, declining to 40% over 10 years. The deal is projected to increase bilateral trade by £25.5 billion and boost UK GDP by £4.8 billion.

Established UK Investment Corridors

The UK ranks 6th among FDI source countries for India, with cumulative FDI equity inflow of USD 34.81 billion (January 2000 – December 2023). UK investment concentrates in chemicals (17%), services (15%), and pharmaceuticals (13%), with Maharashtra (51%), Delhi (15%), and Karnataka (10%) as top receiving states. Entering a market where UK companies already have an operational track record means regulatory pathways, local partnerships, and sector norms are relatively well-documented.

Sectoral Opportunities

UK businesses see the strongest traction in:

- Technology and IT services — 100% FDI under automatic route

- Financial services — 49% FDI in insurance, 74% in private banking

- Professional services — full FDI eligibility

- Manufacturing — 100% FDI across most categories

- Pharmaceuticals — 100% FDI (greenfield), 74% automatic (brownfield)

- Education and retail — liberalised FDI policies post-2020

What UK Entrepreneurs Must Know Before Entering the Indian Market

India's regulatory environment is multi-layered, and the rules that apply to your business depend heavily on your structure and sector.

Company law sits under the Companies Act 2013. Foreign investment is governed by FEMA (Foreign Exchange Management Act), with oversight from the Reserve Bank of India (RBI), SEBI, and the Department for Promotion of Industry and Internal Trade (DPIIT) depending on the activity. Your first step is knowing which of these bodies governs your entry route.

Automatic Route vs Government Approval for FDI

India's FDI regime operates on two tracks:

Automatic Route: No prior government approval required. Investors comply with sectoral caps and file post-investment reports. Most sectors allow 100% foreign ownership automatically.

Government Approval Route: Requires prior clearance via the Foreign Investment Facilitation Portal (FIFP), managed by DPIIT. Required when sector restrictions, investment thresholds, or investor origin apply — for example, companies from countries sharing a land border with India.

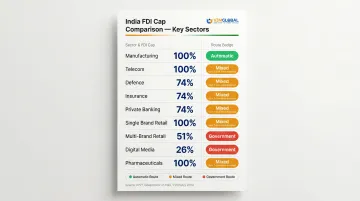

Key Sectoral FDI Caps (2026):

| Sector | FDI Cap | Route |

|---|---|---|

| Manufacturing | 100% | Automatic |

| Telecom | 100% | Automatic up to 49%; Government above |

| Defence | 100% | Automatic up to 74%; Government above |

| Insurance | 49% | Automatic |

| Private Banking | 74% | Automatic up to 49%; Government above |

| Multi-Brand Retail | 51% | Government |

| Single Brand Retail | 100% | Automatic |

| Digital/Print Media (news) | 26% | Government |

| Pharmaceuticals (greenfield) | 100% | Automatic |

Prohibited sectors: Lottery businesses; tobacco or tobacco substitutes manufacturing.

Source: DPIIT Consolidated FDI Policy

Practical Realities UK Entrepreneurs Often Underestimate

Beyond FDI rules, three operational factors consistently catch UK founders off guard once they move from planning to execution.

Corporate Bank Account Timelines

Opening a bank account for a foreign-owned entity typically takes 4–8 weeks, even when documentation is complete. Delays stem from embassy attestation requirements, complex ownership analysis, and AML compliance verification. International banks with India presence — HSBC and Standard Chartered, for instance — may offer faster onboarding for UK clients.

Resident Director Requirement

Every Indian company must have at least one director who has stayed in India for 182+ days in the financial year (Section 149(3), Companies Act 2013). UK entrepreneurs without a local co-founder or India-based employee typically appoint a nominee director through a business advisory firm.

FEMA Repatriation Rules

Dividends declared by an Indian subsidiary to a UK parent are freely repatriable after payment of applicable Indian taxes — no prior RBI approval required. Authorised Dealer banks process the outward remittance directly.

Beyond dividends, other repatriation mechanisms include:

- Royalty payments

- Technical service fees

- Inter-company loan interest

Each carries its own FEMA pricing guidelines and transfer pricing obligations, so structuring these correctly from the outset matters.

Choosing the Right Business Structure in India

The right structure depends on your intent — whether you want full operational presence, an exploratory entry, or a representative function. The wrong choice creates tax inefficiencies or compliance obligations that are costly to unwind later.

Before diving into the details of each option, here's a quick comparison to orient your decision:

| Structure | Generates Revenue | Separate Legal Entity | FDI Route | Best For |

|---|---|---|---|---|

| Private Limited (WOS) | ✓ Yes | ✓ Yes | Automatic (most sectors) | Full operations, hiring, contracts |

| LLP | ✓ Yes | ✓ Yes | Automatic (limited sectors) | Professional services, consulting |

| Branch Office | ✓ Yes | ✗ No (parent liable) | RBI approval required | Established UK firms extending operations |

| Liaison Office | ✗ No | ✗ No (parent liable) | RBI approval required | Market testing, pre-entry research |

Private Limited Company (Wholly Owned Subsidiary / WOS)

Most common structure for UK businesses seeking full operational control in India.

Key Features:

- Separate legal entity with limited liability

- 100% FDI permitted in most sectors under automatic route

- Can hire staff, sign contracts, open bank accounts, and generate revenue

- Minimum 2 directors (at least one India-resident) and 2 shareholders

- No minimum paid-up capital requirement (though adequate working capital essential)

Advantages:

- Shareholder liability limited to subscribed shares

- Perpetual existence (unaffected by ownership changes)

- Easier to raise equity funding (viewed as trustworthy by investors)

- Flexible share transferability

Limited Liability Partnership (LLP)

If a fully incorporated company feels like more than you need at the outset, an LLP offers a lighter compliance footprint — though with narrower FDI eligibility.

Popular for professional services and consulting businesses.

Key Features:

- FDI permitted only in sectors where 100% FDI is allowed under automatic route with no FDI-linked performance conditions

- Simpler compliance and lower costs than Private Limited Company

- Partners have shared liability (unlike company shareholders)

Works well for small professional teams that want cost-effective operations and flexible profit-sharing. The trade-offs: FDI restrictions limit eligible sectors, and shared partner liability may not suit all UK investors.

Branch Office

For established UK companies that want to extend existing operations into India — rather than build a new entity — a Branch Office is worth considering, provided you can meet the parent-company eligibility thresholds.

Allows UK company to conduct business in India as an extension of the parent.

Key Features:

- Not a separate legal entity — parent company bears liability

- Requires RBI approval

- Parent must have 5 consecutive years of profitability and net worth of at least USD 100,000

- Permitted activities: export/import (wholesale), professional/consultancy services, research, IT services, technical support

Profits are freely remittable to the UK (subject to tax). The key drawback: the parent company carries full liability exposure, with no separate legal entity to ring-fence India-side risk.

Liaison Office (Representative Office)

At the lightest end of the spectrum, a Liaison Office suits UK businesses that want a presence in India without committing to full operations. It's specifically designed for market testing.

Lightest entry structure — cannot generate revenue in India.

Key Features:

- Parent must have 3 consecutive years of profitability and net worth of at least USD 50,000

- Requires RBI permission (typically granted for 3 years, extendable)

- Permitted activities: representing parent company, promoting export/import, promoting technical/financial collaborations

- Cannot engage in commercial activities or generate revenue

Compliance is minimal, making it a practical first step before committing to a full structure. Constraints to note: no revenue generation is permitted, operational lifespan is limited, and an annual Activity Certificate filing is required.

VJM Global has guided 250+ UK businesses through structure selection, matching each decision to sector, FDI eligibility, and long-term India strategy — before the registration process begins, not after.

How to Set Up a Business in India: Step-by-Step Guide

This section walks through establishing a Private Limited Company — the most common and versatile structure for UK entrepreneurs.

Step 1 – Obtain a Digital Signature Certificate (DSC) and Director Identification Number (DIN)

Digital Signature Certificate (DSC): A Class 3 DSC is required for all directors to sign electronic filings.

Required Documents:

- Passport (self-attested)

- Address proof (bank statement or utility bill, not older than 2 months)

- Passport-size photograph

- Video verification

Process:

- Documents must be apostilled (Hague Convention — applicable to UK)

- Apply through licensed Certifying Authorities (eMudhra, Capricorn, V-Sign, Pantasign, Safescrypt/Sify)

- Turnaround: 24–48 hours after document submission; apostille process in UK takes 3–10 days

Director Identification Number (DIN): Now integrated directly into the SPICe+ form. Up to 3 directors can apply for DIN within SPICe+ without filing separate DIR-3 forms.

Resident Director Requirement: At least one director must have resided in India for 182+ days during the financial year. UK entrepreneurs typically appoint a nominee local director through a business advisory firm.

VJM Global handles DSC and DIN applications for UK clients and verifies that all documents meet Indian regulatory standards. Typical turnaround is 2 days for DSC and 1 day for DIN, excluding apostille time.

Step 2 – Reserve a Company Name and Prepare Incorporation Documents

RUN (Reserve Unique Name): Apply via MCA portal for name reservation. MCA holds the reservation for 60 days.

Naming Rules:

- Must not be identical or too similar to existing company/LLP

- Must not violate trademarks

- Must not contain restricted words requiring prior approval ("National," "Republic")

Memorandum of Association (MoA) and Articles of Association (AoA):

- MoA defines company's main objects

- AoA governs internal management rules

Common Miss: UK entrepreneurs often list overly narrow business objects in MoA, requiring amendments when activities expand. Draft broadly within permitted scope.

Step 3 – File for Incorporation with the Ministry of Corporate Affairs (MCA)

SPICe+ (Simplified Proforma for Incorporating Company Electronically Plus): Single integrated form covering:

- Company incorporation

- PAN (Permanent Account Number) and TAN (Tax Deduction and Collection Account Number)

- GSTIN (optional at incorporation stage)

- EPFO and ESIC registration

- Bank account opening request

Turnaround: Typically 7–10 working days when all documents correctly submitted. Certificate of Incorporation (CoI) issued digitally.

MCA Incorporation Fees: Based on authorised capital. Verify current fee schedule at the MCA fee calculator.

For UK clients, VJM Global manages SPICe+ filing from document preparation through submission. Observed turnaround is 5 days for Certificate of Incorporation once documents are in order.

Step 4 – Open a Corporate Bank Account and Receive Foreign Investment

Bank Account Opening:

Company must open an Indian bank account to receive FDI from UK parent or shareholders.

Required Documents:

- Certificate of Incorporation

- MoA/AoA

- PAN card

- Board resolution

- Registered office address proof

- KYC for signatories (passport, address proof, photographs)

- Parent company shareholding documents

- AML/beneficial ownership declarations

Timeline: Can take 4–8 weeks even with complete documents. International banks with India presence (HSBC, Standard Chartered) may offer faster onboarding for UK clients.

FC-GPR (Foreign Currency - Gross Provisional Return):

Must be filed within 30 days of share allotment to foreign investor, through the RBI FIRMS portal. Includes details of Indian company, foreign investor, shares allotted, consideration received, and sectoral classification.

Step 5 – Register for Tax Compliance: GST, Income Tax (PAN/TAN), and Payroll

Once capital is received, tax and payroll registrations follow. Here's what applies:

GST Registration Thresholds:

- ₹20 lakh aggregate turnover for service providers

- ₹40 lakh for goods suppliers (most states)

- ₹10 lakh in special category states (northeastern states, Himachal Pradesh, Uttarakhand)

- Where a business supplies both goods and services, the ₹20 lakh threshold applies

PAN and TAN: Issued as part of SPICe+ process.

Payroll Registrations:

- EPFO: Mandatory for establishments with 20+ employees (automatically registered via SPICe+ for all new companies)

- ESIC: Mandatory for establishments with 10+ workers earning up to ₹21,000 per month (₹25,000 for employees with disability)

- Professional Tax: State-level tax; not all states levy it (for example, maximum ₹2,500 per annum in Maharashtra)

VJM Global manages GST registration, PAN/TAN confirmation, and payroll compliance setup — covering EPFO, ESIC, and Professional Tax — so UK entrepreneurs meet every statutory deadline from day one.

Post-Setup Compliance: What UK-Owned Companies in India Must Manage

Ongoing compliance for a UK-owned Private Limited Company spans four layers: MCA filings, income tax, GST returns, and FEMA/RBI reporting.

MCA Annual Filings

| Filing | Deadline | Description |

|---|---|---|

| Form AOC-4 (financial statements) | Within 30 days of AGM | Typically 30 October (for 31 March year-end) |

| Form MGT-7 (annual return) | Within 60 days of AGM | Typically 29 November |

| AGM (Annual General Meeting) | Within 6 months of financial year-end | By 30 September for 31 March year-end |

| Board Meetings | Minimum 4 per financial year | Not more than 120 days gap between consecutive meetings |

Income Tax Compliance

| Obligation | Deadline | Notes |

|---|---|---|

| Corporate ITR Filing | 31 October (assessment year) | For audited accounts |

| Advance Tax — 15 June | 15 June | 15% of estimated annual liability |

| Advance Tax — 15 September | 15 September | 45% cumulative |

| Advance Tax — 15 December | 15 December | 75% cumulative |

| Advance Tax — 15 March | 15 March | 100% cumulative; 1% per month interest on shortfall |

| TDS Return Q1 (Apr–Jun) | 31 July | Quarterly TDS filing |

| TDS Return Q2 (Jul–Sep) | 31 October | Quarterly TDS filing |

| TDS Return Q3 (Oct–Dec) | 31 January | Quarterly TDS filing |

| TDS Return Q4 (Jan–Mar) | 31 May | TDS payment due 7th of following month; 30 April for March |

GST Returns

Regular Taxpayers (Monthly):

- GSTR-1 (outward supplies): 11th of following month

- GSTR-3B (summary return with tax payment): 20th of following month

QRMP Scheme (Quarterly): Taxpayers with turnover up to ₹5 crore (approximately £480,000) may opt for quarterly GSTR-1 and GSTR-3B, with monthly tax payments via PMT-06 by 25th of following month.

FEMA/RBI Reporting

Foreign investment into an Indian company triggers specific RBI reporting obligations. Missing these deadlines carries compounding penalties, so they warrant close attention from UK shareholders.

| Report | Deadline | Description |

|---|---|---|

| FC-GPR | Within 30 days of share allotment | Foreign investment reporting |

| FC-TRS | Within 60 days of share transfer | Share transfer between resident and non-resident |

| APR (Annual Performance Report) | 31 December each year | Mandatory for all Indian companies with foreign investment |

UK-India Double Taxation Avoidance Agreement (DTAA)

The UK-India DTAA ensures profits earned in India are not taxed twice and defines withholding tax rates:

| Income Type | DTAA Withholding Rate |

|---|---|

| Dividends | 10% / 15% |

| Interest (paid to bank) | 10% |

| Interest (other cases) | 15% |

| Royalties | 10% / 15% |

| Fees for Technical Services | 10% / 15% |

Note: The lower of the domestic rate or treaty rate applies. Specific conditions apply to each category — consult a qualified tax advisor.

Managing these four compliance layers simultaneously is where most UK entrepreneurs hit friction. VJM Global handles MCA filings, GST returns, income tax, FEMA reporting, and payroll for 250+ UK businesses in India, with a 95% client retention rate across that client base.

Frequently Asked Questions

Can an Indian citizen start a business in the UK?

Yes, Indian citizens can start a business in the UK. Similarly, UK entrepreneurs can set up a business in India, typically through a Private Limited Company or LLP, with 100% ownership permitted under the FDI automatic route in most sectors.

Which Indian products are in demand in the UK?

High-demand categories include textiles and garments, pharmaceuticals, IT/software services, gems and jewellery, and food products (spices, ready-to-eat goods). These are worth considering if your India entry strategy involves export, sourcing, or trade partnerships.

What is the minimum capital required to set up a company in India?

There is no mandatory minimum paid-up capital for a Private Limited Company in India. That said, adequate working capital to fund early operations and meet RBI compliance requirements is essential before commencing business.

Can a UK company own 100% of an Indian subsidiary?

Yes, 100% foreign ownership is permitted in most sectors under India's FDI automatic route, meaning no prior government approval needed. Certain sectors like multi-brand retail (51% cap), insurance (49% cap), and banking (74% cap for private banks) have equity caps or require government approval.

How long does it take to register a company in India from the UK?

With all documents in order, incorporation via MCA typically takes 10–20 working days. Factor in time for DSCs, DINs, and bank account opening — full setup including an active bank account generally takes 6–10 weeks end-to-end.

What are the ongoing compliance requirements for a UK-owned company in India?

Four main compliance areas: annual MCA filings (AOC-4, MGT-7), income tax and TDS returns, GST returns (monthly or quarterly), and FEMA/RBI reporting for cross-border transactions (FC-GPR, FC-TRS, APR). Non-compliance carries significant penalties.