Introduction

You can register and operate a US business from Singapore without ever relocating — but the process looks nothing like what a US resident follows. Singapore-based founders, SMEs, and investors regularly discover that a wrong entity choice or a missed compliance filing can cost tens of thousands of dollars in penalties and restructuring fees.

If you're looking to raise venture capital, serve American customers, or grow into new markets, this guide covers what you actually need: which business structure to choose, how to register remotely, and the Singapore-specific tax, banking, and visa considerations you cannot afford to overlook.

Key Takeaways

- Singapore residents can legally set up an LLC or C-Corporation in the US without living there or holding a US Social Security Number

- Delaware and Wyoming are the top states for non-resident incorporation, with filing fees of $109–$110 and no physical presence requirements

- An Employer Identification Number (EIN) is required for US banking and tax filing; non-residents obtain one by fax or phone through the IRS

- No US-Singapore income tax treaty exists; expect 30% withholding on dividends with no treaty reduction

- Singapore's E-2 treaty status allows active business investors to apply for a US work visa through their qualifying investment

Why Singapore Entrepreneurs Are Setting Up Businesses in the USA

Americans spent nearly $19 trillion on goods and services in 2023, roughly 32% of global consumer spending. For Singapore-based tech, e-commerce, or service businesses, a US entity opens access to American customers, US payment processors (Stripe, PayPal), and global investors who typically require a US-incorporated company before writing a check.

The venture capital factor: Stripe Atlas data shows that Southeast Asian startups regularly incorporate in both Singapore and the US because many US investors require a US parent company before committing capital. 81.4% of US-based IPOs in 2024 chose Delaware as their corporate home, and 66.7% of Fortune 500 companies are incorporated there. Y Combinator and major US venture funds routinely require a Delaware C-Corp structure.

The US-Singapore Free Trade Agreement (USSFTA): Entered into force on January 1, 2004, this was the first FTA the United States signed with an Asian nation. The agreement provides Singapore businesses with:

- National treatment for investors

- Elimination of tariffs on qualifying goods

- Access to US federal government procurement

- Negative-list approach for services (all sectors open unless specifically excepted)

- 5,400 H-1B1 visas reserved annually for Singaporean professionals—a dedicated quota rarely exhausted, unlike the standard H-1B lottery

These advantages make the US a logical expansion market for Singapore companies seeking scale beyond Southeast Asia.

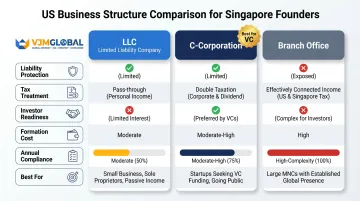

Best Business Structures for Singapore-Based Founders

Non-US residents can form only two entity types: an LLC or a C-Corporation. S-Corporations are explicitly prohibited to non-resident aliens under IRS rules—many Singaporean founders mistakenly assume S-Corps are available, only to discover this restriction during formation.

LLC (Limited Liability Company)

Best for: Consulting, services, e-commerce, or smaller-scale operations not seeking US venture capital.

Key features:

- Limited personal liability protection

- Pass-through taxation—profits taxed only at the member level

- Flexible management structure

- Lower formation costs ($100-$110)

Tax implications for Singapore residents: As a foreign member of a US LLC, your share of effectively connected income (ECI) faces 37% withholding tax for non-corporate partners. The LLC's pass-through income may also trigger Singapore tax obligations under foreign income rules, creating potential double taxation without careful structuring.

C-Corporation

Best for: Tech startups, businesses raising US venture capital, or companies planning eventual IPO.

Key features:

- Unlimited shareholders allowed

- Multiple share classes (common, preferred)

- Industry standard for US investors

- 21% federal corporate tax rate plus potential state taxes

Trade-off: Double taxation risk—corporate profits taxed at 21%, then dividends face 30% withholding when distributed to Singapore shareholders (no treaty reduction available). Retained earnings can be reinvested in the business without triggering dividend withholding, which gives C-Corps a meaningful structural advantage for growth-stage companies.

Branch Office (Foreign Corporation Registration)

A less common option: register your Singapore Pte. Ltd. as a foreign corporation doing business in a specific US state.

Key limitations:

- The parent Singapore company remains fully liable for all branch obligations

- Exposes your Singapore entity to US litigation and regulatory risk

- Requires multi-jurisdiction compliance (Singapore + US state laws)

- Poor fit for most Singapore founders unless operating at multinational scale with dedicated legal teams

Decision Framework

| Factor | LLC | C-Corporation | Branch Office |

|---|---|---|---|

| Liability Protection | Yes (separate entity) | Yes (separate entity) | No (parent liable) |

| Tax Treatment | Pass-through (37% withholding on US-source income) | Corporate + dividend (21% + 30%) | Corporate tax + full parent liability |

| Investor Readiness | Poor (VCs rarely accept) | Excellent (industry standard) | Not applicable |

| Formation Cost | $100-$110 | $109 | Varies by state |

| Annual Compliance | Moderate | Higher | Complex (multi-jurisdiction) |

| Best For | Service businesses, solo ventures | VC-backed startups, scaling tech | Multinational subsidiaries |

How to Register a US Business from Singapore: Step-by-Step

The entire process can be completed remotely from Singapore—no physical US presence required—and typically takes 2-4 weeks. Working with a professional service or registered agent is strongly recommended for first-time foreign founders to avoid costly mistakes.

Step 1: Choose Your State of Incorporation

For Singapore founders with no physical US operations, two states dominate:

Delaware advantages:

- 81.4% of 2024 IPOs chose Delaware

- Established Court of Chancery with 200+ years of corporate case law

- Investor familiarity and credibility

- No sales tax

- No minimum capital requirement

- Cost: LLC formation $110; C-Corp incorporation $109

- Annual franchise tax: $300 for LLCs

Wyoming advantages:

- Lower ongoing costs ($60 annual report vs. $300 Delaware)

- No state corporate income tax (Delaware has 8.7%)

- Enhanced privacy—member names not publicly disclosed

- Cost: LLC or C-Corp formation $100

- Annual report: $60 minimum

Rule of thumb: Choose Delaware if you plan to raise US venture capital (investor preference is near-universal). Choose Wyoming if you're running a profitable service business or holding company focused on minimizing ongoing costs and protecting owner privacy.

Note: If you plan to hire employees or open a physical office in a specific state, you must also register (foreign qualify) in that state, regardless of where you initially incorporate.

Step 2: Select a Business Name and File Formation Documents

Name availability: Search the chosen state's business registry online (Delaware registry at corp.delaware.gov; Wyoming at wyobiz.wyo.gov) to ensure your desired name is available.

Required filings:

- For LLC: File Articles of Organization with state filing fee

- For C-Corp: File Articles of Incorporation (Certificate of Incorporation in Delaware)

Mandatory requirement: Appoint a Registered Agent—a person or service with a physical US address in your state of incorporation who receives official legal documents on behalf of your company. Annual registered agent fees range from $49-$125 depending on provider and state.

Step 3: Obtain an EIN from the IRS

The Employer Identification Number (EIN) is a 9-digit federal tax ID required to open a US bank account, hire employees, and file taxes. For Singapore founders, this step is often the most frustrating part of the process.

Critical limitation: The IRS online EIN application is restricted to applicants whose principal place of business is in the US. Singapore residents without a US Social Security Number cannot use the online system.

Non-resident application methods:

| Method | Contact | Processing Time |

|---|---|---|

| Phone (international) | +1-267-941-1099 (Mon-Fri, 6am-11pm ET) | Immediate (during call) |

| Fax (from outside US) | +1-304-707-9471 | Approximately 4 business days |

| IRS, Attn: EIN International Operation, Cincinnati, OH 45999 | Approximately 4 weeks |

Application form: Complete IRS Form SS-4. The application is free of charge. Avoid third-party services that charge for EIN acquisition. They're simply filing the same form you can submit directly.

Time zone consideration: The IRS international phone line operates 6am-11pm Eastern Time. From Singapore (GMT+8), this translates to 6pm-11am Singapore time (depending on US daylight saving time).

Step 4: Open a US Business Bank Account Remotely

With your EIN in hand, you can move to banking — but this is where most Singapore founders hit a wall. Traditional US banks (Chase, Bank of America, Wells Fargo) require in-person visits for foreign-owned entity accounts, which rules them out for remote applicants.

Remote banking alternatives:

Mercury (strongest option for non-residents)

- Explicitly states "You do not need to be a U.S. citizen or resident to apply"

- Requirements: US-formed entity, US EIN, valid business purpose

- Application entirely online

- No physical US presence required

- Offers USD accounts, debit cards, and wire transfer capabilities

Brex and Relay are often mentioned as alternatives but rarely work for Singapore-based founders. Brex requires a US physical address and verifiable US operations. Relay requires a Social Security Number for all beneficial owners — which excludes most non-residents entirely.

Documentation typically required:

- Certified copy of formation documents (Articles of Organization/Incorporation)

- EIN confirmation letter from IRS

- Operating Agreement (LLC) or Bylaws (C-Corp)

- Proof of business address (registered agent address acceptable)

- Passport copies for all beneficial owners

- Description of business activities

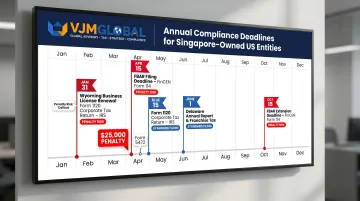

Step 5: Register for State Taxes, Permits, and Ongoing Compliance

After federal registration, you must fulfill state-level requirements:

Delaware annual obligations:

- Annual Report: Due by June 1 each year

- Franchise Tax: $300 for LLCs (due June 1); varies for corporations based on authorized shares or assumed par value capital method

- Late filing penalty: $200 + $0.02/month interest

Wyoming annual obligations:

- Annual Report: $60 minimum (due by the anniversary of formation)

- Business License: $100 (due January 31 annually)

Multi-state considerations: If you conduct business activities (have employees, physical offices, or significant sales) in states other than your formation state, you may need to foreign qualify and register for state taxes in those jurisdictions.

Critical compliance warning: Non-compliance with annual filings leads to penalties, interest charges, and eventual administrative dissolution of your entity. Once dissolved, you lose liability protection, and reinstating the entity requires back fees plus reinstatement fees.

VJM Global provides continuous US tax compliance and accounting support for Singapore-owned US entities, handling Form 1120, Form 5472, annual state reports, and Delaware franchise tax filings — so founders can prioritize building their business rather than tracking filing deadlines.

Singapore-Specific Considerations: Visas, Taxes, and Banking

Visa Requirements for Managing from the US

You can legally own and manage a US LLC or C-Corporation from Singapore without any US visa. However, if you intend to physically work in the US or take up residence, a valid US work visa becomes mandatory.

E-2 Treaty Investor Visa: Singapore is a designated E-2 treaty country under the USSFTA (effective January 1, 2004). Eligible Singapore citizens who invest a "substantial amount" in a US enterprise and intend to develop and direct it can apply for the E-2 visa.

What qualifies as "substantial investment"?

- No fixed minimum dollar amount exists

- USCIS applies a proportionality test: "The lower the cost of the enterprise, the higher, proportionately, the investment must be"

- Capital must be "at risk" in a commercial sense

- Enterprise must be real and operating (not a paper organization)

- Business must not be "marginal"—must generate more than minimal living for the investor

- Investor must own at least 50% or possess operational control

E-2 advantages: Renewable indefinitely in two-year increments; spouse receives work authorization; allows investor to live in the US while actively managing the business.

US-Singapore Tax Treaty Status—Critical Finding

There is no comprehensive bilateral income tax treaty between the United States and Singapore. This is the single most consequential tax fact for Singapore founders.

Immediate implications:

- Standard US withholding tax of 30% applies to dividends, interest, and royalties paid from US sources to Singapore residents

- No treaty-based reduction available

- No foreign tax credit relief coordination between jurisdictions

- Higher complexity in structuring cross-border payments

The two countries do have a limited agreement regarding taxation of income from international operation of ships and aircraft, and a FATCA intergovernmental agreement, but neither constitutes a comprehensive income tax treaty.

In practice, the missing treaty creates different exposure depending on your entity type.

US C-Corporation owned by Singapore resident:

- Corporate profits taxed at 21% federal rate (plus any state taxes)

- Dividends distributed to Singapore shareholder face 30% withholding

- Singapore may tax the same dividend income under its foreign income rules

- Potential double taxation: 21% + 30% withholding + potential Singapore tax

The LLC picture is similarly unforgiving:

US LLC owned by Singapore resident:

- Share of effectively connected income (ECI) subject to 37% withholding (non-corporate partners)

- Must file Form 1040-NR (US non-resident tax return)

- Singapore may tax the same income as foreign-source income

- No treaty relief to eliminate or reduce double taxation

Careful structuring can reduce this exposure. VJM Global's CPAs and Chartered Accountants work with Singapore founders on approaches such as timing of distributions, debt vs. equity financing mix, and transfer pricing documentation — each of which can affect the effective tax burden meaningfully.

FBAR and FATCA Reporting Obligations

Singapore-resident owners of US business entities face two commonly overlooked reporting requirements:

FBAR (FinCEN Form 114):

- Required if you have financial interest in or signature authority over US financial accounts exceeding $10,000 aggregate value at any time during the calendar year

- Filing deadline: April 15, with automatic extension to October 15

- Penalties for non-filing:

- Non-willful violations: up to $16,117 per violation

- Willful violations: up to the greater of $161,166 or 50% of account balance

- Criminal penalties: fines up to $250,000 and imprisonment up to 5 years

FATCA (Form 8938):

- Applies to US persons (citizens, green card holders) living in Singapore who hold specified foreign financial assets above the reporting thresholds

- Thresholds for taxpayers living abroad: $200,000 on last day of tax year or $300,000 at any time during the year

- Different thresholds apply for unmarried US taxpayers living in the US

Your US business bank account counts toward these thresholds. A Singapore founder with a Mercury account holding $15,000 must file FBAR — and penalties apply automatically, even if no tax is owed.

These filings are easy to miss because they sit outside the standard tax return process. VJM Global helps Singapore-resident US entity owners track these obligations and file on time.

Currency and International Payments

Beyond tax and compliance, the day-to-day mechanics of running a US account from Singapore add another layer of friction:

Key pain points:

- Currency conversion costs (SGD to USD and back)

- International wire fees (typically $25–$50 per transaction)

- 2-3 day delays for international transfers

- Unfavorable exchange rates from traditional banks

Solutions:

- Multi-currency accounts (Wise Business, Mercury) that hold both USD and SGD

- USD-denominated corporate cards for US expenses

- Payment processors like Stripe that allow USD collection with multi-currency payout

- Regular currency hedging for businesses with significant USD exposure

Common Mistakes Singapore Founders Make When Setting Up a US Business

Choosing the Wrong Entity Type

Many Singapore founders default to an LLC without understanding that it's unsuitable for raising US venture capital. Conversely, some attempt to set up an S-Corp without realizing it's restricted to US citizens and permanent residents.

Restructuring from an LLC to a C-Corp later creates a taxable event and real legal complexity. According to Stripe Atlas, a "corporate flip" can cost $20,000+ due to anti-inversion regulations.

If there's any chance you'll raise institutional venture capital in the next 3-5 years, incorporate as a Delaware C-Corp from day one.

Ignoring Ongoing Compliance After Formation

Registering the company is only the beginning. Many Singapore founders miss:

Form 5472 filing — 25% foreign-owned US corporations and single-member LLCs must file annually, attached to a pro forma Form 1120. Non-filing carries a $25,000 penalty, even with no US-source income. Reportable transactions include initial capitalization, expense payments by the foreign owner, and any monetary transfers between the entity and related parties.

Other deadlines that frequently catch founders off guard:

- Delaware annual report and franchise tax (due June 1)

- Form 1120 corporate tax return (15th day of the 4th month after tax year end)

- State sales tax registration (if selling taxable goods or services)

- Business license renewals

Budget at least $2,000–$5,000 annually for compliance costs — accounting fees, franchise taxes, registered agent, and professional filings — before generating any US revenue.

Underestimating Banking Challenges

A US EIN gets you closer, but it won't open a bank account on its own. Traditional banks require:

- In-person visits (impossible from Singapore)

- Proof of US business activity or existing customers

- Multiple rounds of KYC documentation

- Physical US address (virtual addresses often rejected)

Plan for banking during the entity formation stage — not after. Research Mercury, Relay, or Brex requirements before filing formation documents, and prepare all documentation (operating agreement, EIN letter, passport copies) in advance. Skipping this step can delay business operations by 6-8 weeks, blocking payments and vendor relationships before you've even started.

Frequently Asked Questions

Can a foreigner set up a business in the US?

Yes, non-US citizens and non-residents (including Singapore citizens) can form a US LLC or C-Corporation without a visa or US Social Security Number. You can manage the business remotely from Singapore, though physical work in the US requires appropriate work authorization.

How much does it cost to start a business in the USA?

Typical first-year costs for Singapore founders:

- Delaware LLC formation: $110 | C-Corp: $109

- Registered agent service: $49–$125/year

- EIN application: free

- State annual fees: $60–$300

- Total first-year cost (including basic compliance): $1,500–$3,000

Add $1,000–$2,000 for professional incorporation services if needed.

Is owning an LLC worth it?

An LLC is worth it for Singapore founders focused on service businesses, e-commerce, or solo ventures without US venture funding goals. However, if you plan to raise US venture capital or pursue rapid scaling with institutional investors, a Delaware C-Corp is the better choice from day one.

Can an LLC get grant money?

LLCs can apply for certain federal and state small business grants listed on Grants.gov, but foreign-owned LLCs face eligibility restrictions in most programs. Most federal programs require at least 51% US citizen or permanent resident ownership, so foreign-owned entities have limited options.

How to get $50,000 to start a business?

Singapore founders have several realistic paths to startup funding:

- Personal savings — the most accessible starting point

- Angel investors and global accelerators (Y Combinator, Techstars)

- Crowdfunding platforms open to US-registered entities (Kickstarter, Republic)

- Friends and family investment rounds

Note: Most SBA loan programs require 51% US citizen ownership, making them unavailable to foreign-owned businesses.

Ready to set up your US business from Singapore? VJM Global's US CPAs and Chartered Accountants handle the full process — entity formation, EIN acquisition, and ongoing compliance filings including Form 5472, Form 1120, and state requirements. Our team has supported 500+ American business owners over 30+ years, with specific experience in cross-border tax structuring for foreign-owned US entities. Reach us at info@vjmglobal.com or +91 98915 76441 to book your consultation.