from Singapore: Key Steps and Considerations](https://file-host.link/website/vjmglobal-l8s6go/assets/blog-images/7c5587d4-27a0-4620-8367-776331a11361/1778194469475199_91f35473d0d64443b35ad77e18ebaa75/360.webp)

This guide is for Singapore-registered companies, NRIs/OCIs based in Singapore, and Singapore-based founders looking to establish operations in India. You'll learn which business structure minimizes tax liability, the step-by-step registration process (which takes a minimum of 6–8 weeks), FDI and FEMA compliance requirements, and ongoing obligations that keep your Indian entity in good standing.

Key Takeaways

- The India-Singapore CECA and DTAA cut withholding tax on dividends, interest, and royalties — reducing cross-border tax friction significantly

- Choose a Private Limited Company over a Branch Office: effective tax rate is 25.17% vs. 36.40–38.22%

- Expect 6–8 weeks minimum for full incorporation — apostille processing is typically the main bottleneck

- Most sectors allow 100% FDI via automatic route, but you must file FC-GPR with the RBI within 30 days of share allotment

- Budget for ongoing compliance: MCA filings, quarterly advance tax, monthly TDS, and GST returns all kick in post-registration

Why Singapore Businesses Are Expanding into India

Strategic FDI Corridor Between Singapore and India

Singapore holds a dominant position in India's foreign investment landscape. During April-December FY26, Singapore emerged as the top source of FDI equity inflows into India, contributing USD 17.6 billion.

The India-Singapore Comprehensive Economic Cooperation Agreement (CECA) provides structural advantages unavailable to other foreign investors:

- Tariff elimination on 81% of Singapore's exports to India

- 3,000+ tariffs zeroed and another 2,000+ tariffs reduced

- Preferential access for Singapore service providers in engineering, banking, telecommunications, and real estate

- 35% originating content requirement from Singapore or India to qualify for concessions

These treaty benefits translate into real cost savings on trade transactions and reduced market entry barriers for Singapore companies.

India's Economic Growth Trajectory

India's real GDP grew 6.5% in FY 2024-25, with Q4 recording 7.4% growth. The IMF projects India's GDP growth at 6.5% for both 2026 and 2027, positioning India on track to become the world's third-largest economy by 2030.

For Singapore businesses, this growth creates opportunities in:

| Sector | Singapore FDI (2000-2024) | % of Total |

|---|---|---|

| Services (financial, banking, R&D) | USD 31.27 billion | 18.19% |

| Computer Software & Hardware | USD 28.78 billion | 16.74% |

| Trading | USD 22.91 billion | 13.32% |

| Construction Infrastructure | USD 14.42 billion | 8.39% |

| Telecommunications | USD 8.99 billion | 5.23% |

Tax Treaty and Capital Flow Advantages

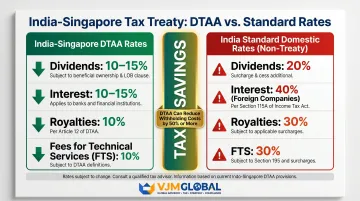

These sectors become even more attractive when paired with India's tax treaty framework. The India-Singapore Double Taxation Avoidance Agreement (DTAA) prevents double taxation and caps withholding rates well below India's standard domestic rates:

- Dividends: 10% (if beneficial owner holds ≥25% shares) or 15%

- Interest: 10% (if paid to a bank) or 15%

- Royalties and Fees for Technical Services: 10%

For comparison, non-treaty investors face India's standard 20% withholding on dividends and 40% on interest (for foreign companies). The DTAA can reduce these costs by half or more, directly improving after-tax returns for Singapore parent companies repatriating profits.

Choosing the Right Business Structure for Singapore Investors

Four Main Entity Options

Singapore investors entering India can choose from:

- Private Limited Company: A wholly-owned subsidiary, eligible for 100% FDI and offering complete operational flexibility

- Limited Liability Partnership (LLP): Tax-efficient for partnerships, but limited fundraising options

- Branch Office: An extension of the Singapore entity; higher tax rates apply

- Liaison Office: For representational activities only; cannot earn revenue in India

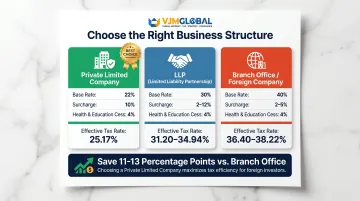

Why Private Limited Company Is the Preferred Structure

A Private Limited Company offers the lowest corporate tax burden and greatest operational flexibility:

| Entity Type | Base Rate | Effective Rate |

|---|---|---|

| Domestic Pvt Ltd (Sec 115BAA) | 22% | 25.17% |

| Foreign Company / Branch Office | 35% | 36.40–38.22% |

| LLP | 30% | 31.20–34.94% |

Tax savings of 11–13 percentage points make the Private Limited Company structure far more attractive than a Branch Office.

Additional advantages:

- Qualifies for 100% FDI via automatic route in most sectors

- Allows fundraising from Indian and foreign investors

- Provides legal separation between Singapore parent and Indian operations

- Reduces permanent establishment (PE) risk

Automatic Route vs. Government Approval Route

100% FDI under the automatic route is available in most sectors including manufacturing, IT services, e-commerce, construction, telecom services, and industrial parks. No prior government approval is required—only post-investment reporting to the RBI.

Sensitive sectors (defence, broadcasting, multi-brand retail) require government approval before investment.

Ownership Structure: Corporate vs. Individual Shareholders

Once you've chosen a Private Limited Company, how you structure shareholding matters just as much. Singapore investors typically set up their Indian subsidiary with two corporate shareholders (both group entities) rather than individual shareholders.

Indian company law does not permit virtual participation in shareholder meetings, meaning individual shareholders must attend in person. Corporate shareholders, by contrast, can send authorized representatives — so Singapore-based principals don't need to travel to India for every AGM.

Step-by-Step Process to Register a Business in India from Singapore

Total timeline: 6–8 weeks minimum, with the apostille and notarization process in Singapore being the primary delay factor.

Step 1: Reserve the Company Name and Prepare Board Resolutions

File SPICe+ Part A for name reservation (government fee: INR 1,000 / approximately USD 12). If the majority shareholder is a Singapore corporate entity, the parent company's Board must pass a resolution approving the name reservation—adding 1–2 working days before submission.

Step 2: Obtain DIN and DSC for Proposed Directors

Every proposed director (including foreign directors) must obtain:

- Director Identification Number (DIN): Required for all directors; INR 500 per director

- Digital Signature Certificate (DSC): Required to sign and submit incorporation documents electronically

Foreign directors must submit passport copies, address proof, photographs, and specimen signatures—all notarized and apostilled in Singapore. This apostille requirement is typically the single biggest timeline bottleneck.

Step 3: Prepare and Notarize Incorporation Documents

Required documents:

- Memorandum of Association (MOA)

- Articles of Association (AOA)

- KYC documents for all directors and shareholders (passport, address proof, photos)

- Singapore parent company's Certificate of Incorporation

Singapore acceded to the Hague Apostille Convention on January 18, 2021, with the Convention entering force on September 16, 2021. All Singapore-origin documents must be apostilled for use in India. Delays in obtaining apostilled documents add 2–3 weeks to the incorporation timeline.

Step 4: File Incorporation Form with the Registrar of Companies (ROC)

SPICe+ Part B is a single integrated form covering:

- Company incorporation

- PAN and TAN issuance

- Optional registrations (EPF, ESIC, professional tax)

Government fee for companies with nominal share capital up to INR 10 lakh (approximately USD 12,000): NIL. Upon approval, the ROC issues the Certificate of Incorporation (COI) alongside PAN and TAN numbers—typically within 5 days.

Step 5: Open an Indian Business Bank Account and Infuse Capital

Post-incorporation requirements:

- Open an Indian business bank account (most banks require at least one resident Indian director to be present)

- Transfer the subscribed share capital into the account within 180 days

- File Form INC-20A (Certificate of Commencement of Business) with proof of capital credit

The company cannot legally commence operations until the COC is received. Fee for INC-20A: INR 200–600 (approximately USD 2–7).

Step 6: Obtain Additional Registrations and File RBI Compliance Forms

Once operations begin, these registrations and filings are triggered:

- GST registration: Mandatory once turnover crosses INR 40 lakh (for goods) or INR 20 lakh (for services); immediately required for inter-state suppliers

- Import Export Code (IEC): Required if the company will import or export goods

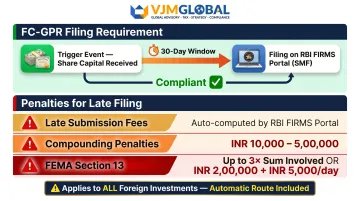

- FC-GPR filing with RBI: Mandatory within 30 days of share capital receipt to report foreign investment under FEMA; late filing attracts compounding penalties ranging from INR 10,000 to INR 5,00,000

VJM Global manages the full sequence—from bank account opening and INC-20A filing through FC-GPR reporting and GST registration—so no compliance deadline is missed during this critical post-incorporation window.

Tax and FDI Considerations for Singapore Founders

How the India-Singapore DTAA Reduces Tax Liability

The DTAA provides reduced withholding tax rates on cross-border payments:

| Income Type | DTAA Rate | Conditions |

|---|---|---|

| Dividends | 10% | If beneficial owner holds ≥25% shares |

| Dividends | 15% | All other cases |

| Interest | 10% | If paid to a bank |

| Interest | 15% | All other cases |

| Royalties | 10% | Beneficial owner requirement applies |

| Fees for Technical Services | 10% | Beneficial owner requirement applies |

For shares acquired before April 1, 2017, capital gains are generally exempt from tax in India (taxable only in Singapore), subject to the Limitation of Benefits clause. Shares acquired on or after April 1, 2017 are taxable in India at domestic rates.

Corporate Tax Rates for Indian Subsidiaries

Current corporate tax rates for AY 2026-27:

- Domestic Private Ltd (Section 115BAA): 22% base rate + 10% surcharge + 4% cess = 25.17% effective

- New manufacturing companies (Section 115BAB): 15% base rate + 10% surcharge + 4% cess = 17.16% effective

These rates are significantly lower than Branch Office rates (36.40–38.22%), creating a tax premium of 11–13 percentage points for choosing a branch structure.

GST Compliance and Export Zero-Rating

Beyond corporate tax, GST is the other major ongoing obligation to plan for from day one.

India's GST operates on a four-tier rate structure: 5%, 12%, 18%, 28%, with essential items at 0%. Exports are zero-rated under Section 16 of the IGST Act—exporters can claim full refund of input tax credits, a significant cash flow advantage for Singapore companies using India as a service delivery or manufacturing base.

Registration thresholds:

- Goods suppliers: INR 40 lakh (normal states) / INR 20 lakh (special category states)

- Service suppliers: INR 20 lakh (normal states) / INR 10 lakh (special category states)

- Inter-state suppliers: Mandatory regardless of turnover

FEMA Compliance and FC-GPR Filing

All inbound FDI must be reported to the RBI via Form FC-GPR within 30 days of share allotment. The filing is made through the RBI FIRMS portal under the Single Master Form (SMF) system.

Penalties for late filing:

- Late Submission Fees (LSF) computed automatically by RBI portal

- Compounding penalties: INR 10,000 to INR 5,00,000 depending on delay

- Under FEMA Section 13: Up to three times the sum involved, or INR 2,00,000 plus INR 5,000 per day for continuing contravention

Missing the 30-day window is one of the most common compliance errors for first-time India entrants. Working with an advisor who handles FC-GPR filings routinely—such as VJM Global's FEMA team—removes that risk entirely.

Limitation of Benefits (LoB) Clause

To qualify for DTAA treaty benefits, Singapore entities must demonstrate genuine operational substance. A Singapore resident entity is deemed not to be a shell/conduit company if:

- It is listed on a recognized stock exchange; OR

- Its total annual expenditure on operations in Singapore is at least SGD 200,000 in the 24 months immediately preceding the date the gains arise

In practice, tax authorities look beyond the SGD 200,000 threshold—factors like local employees, office space, and board decisions made in Singapore all strengthen a substance case during scrutiny.

Post-Registration Compliance Obligations

MCA Annual Filing Requirements

| Compliance | Deadline | Legal Basis |

|---|---|---|

| AGM (Annual General Meeting) | Within 6 months of FY end (by Sept 30) | Section 96, Companies Act 2013 |

| Form AOC-4 (Financial Statements) | Within 30 days of AGM (by Oct 30) | Section 137, Companies Act 2013 |

| Form MGT-7 (Annual Return) | Within 60 days of AGM (by Nov 29) | Section 92, Companies Act 2013 |

| Board Meetings | Minimum 4 per year; max 120 days gap | Section 173, Companies Act 2013 |

| DIR-3 KYC (Director KYC) | By September 30 each year | Rule 12A, Directors Rules |

Penalties for late filing: ₹100 per day of delay with no upper limit. Directors may face disqualification for persistent defaults.

Income Tax and TDS Compliance

Advance Tax Payment Schedule:

| Installment | Due Date | Cumulative % |

|---|---|---|

| 1st | June 15 | 15% |

| 2nd | September 15 | 45% |

| 3rd | December 15 | 75% |

| 4th | March 15 | 100% |

TDS (Tax Deducted at Source):

- Payment due by 7th of the following month

- March TDS payments due by April 30

- Quarterly TDS returns (Form 26Q) filed for each quarter

GST Return Filings

Frequency depends on turnover:

- Monthly: For regular taxpayers

- Quarterly: For small taxpayers under the QRMP scheme

Late filing attracts interest and penalties, with potential blocking of input tax credits.

Managing MCA filings, advance tax schedules, TDS returns, and GST filings simultaneously is where most Singapore founders hit their first compliance delays. VJM Global handles each of these tracks — from Form AOC-4 and MGT-7 filings through to quarterly TDS returns and GST reconciliations — so your India operations stay current without pulling focus from the business itself.

Common Mistakes Singapore Businesses Make When Entering India

Choosing Branch Office Over Private Limited Company

Singapore businesses sometimes choose a Branch Office assuming it's simpler, without realizing:

- Higher tax rates: 36.40–38.22% vs. 25.17% for a Private Ltd company

- Limited activities: Branch Offices face restrictions on permissible business activities

- Greater PE risk: Liaison Offices and Branch Offices create permanent establishment exposure, particularly when activities extend beyond preparatory functions

A KPMG analysis of the Mitsui & Co. Ltd case demonstrated that tax authorities frequently assess Liaison Offices as constituting a PE, triggering Indian tax liability on global income attributable to the PE.

Underestimating the Apostille Timeline

Many Singapore founders assume apostille and notarization is quick. In practice, gathering apostilled documents for foreign directors and shareholders can add several weeks to the incorporation timeline.

Required documents typically include:

- Passports and address proofs for all foreign directors

- Parent company incorporation certificate

- Board resolutions authorizing the India entity

Start this process before filing SPICe+ Part A — delays here push back every subsequent step.

Missing the FC-GPR Filing Deadline

Singapore businesses sometimes assume that because their sector allows FDI via the automatic route, there is no RBI-related paperwork. FC-GPR filing is mandatory within 30 days of capital credit — this applies to all foreign investments, regardless of the entry route.

Late filing attracts compounding penalties ranging from INR 10,000 to INR 5,00,000, with penalties under FEMA Section 13 potentially reaching three times the sum involved.

Frequently Asked Questions

Can someone in Singapore set up a business in India?

Yes, Singapore citizens and Singapore-registered companies can set up a business in India. Most sectors permit 100% FDI via the automatic route. Indian company law requires at least one director who has been resident in India for a minimum of 182 days in the preceding calendar year.

How much does it cost to set up a business in India?

Typical costs include SPICe+ Part A name reservation (INR 1,000 / USD 12), incorporation (NIL for companies with share capital up to INR 10 lakh), additional registrations like GST and IEC (USD 80–180), and first-year compliance costs (USD 85–250). Professional advisory fees are separate and vary based on service scope.

What is the Rs 20 lakh grant for startups in India?

India's Startup India programme offers various support schemes including seed funding and grants. However, DPIIT startup recognition requires Indian promoters to hold at least 51% shareholding, and holding/subsidiary companies are not permitted for recognition. Singapore-incorporated parents with majority-owned Indian subsidiaries cannot obtain DPIIT startup recognition.

Does India require a local resident director for foreign companies?

Yes, Section 149(3) of the Companies Act, 2013 mandates at least one director who has stayed in India for not less than 182 days during the preceding calendar year. This requirement applies to all companies including wholly-owned foreign subsidiaries. Penalty for non-compliance: INR 50,000 to INR 5,00,000.

What is the India-Singapore DTAA and how does it benefit Singapore businesses?

The India-Singapore DTAA prevents double taxation and offers reduced withholding tax rates on dividends (10–15%), interest (10–15%), and royalties (10%). It also provides capital gains relief for shares acquired before April 1, 2017, subject to the Limitation of Benefits clause (SGD 200,000 annual expenditure threshold).

How long does it take to register a company in India from Singapore?

The process typically takes 6–8 weeks minimum for foreign entities. Apostille and notarization in Singapore (2–3 weeks) is the largest variable, with bank account opening, capital infusion, and RBI filings adding time post-incorporation. Preparing documents in advance is the single most effective way to shorten the timeline.

Setting up a tax-efficient business in India from Singapore involves multiple regulatory layers — entity structure, MCA filings, FEMA compliance, and ongoing tax obligations. VJM Global's end-to-end service covers incorporation, RBI filings, GST registration, and first-year compliance support, so Singapore founders can focus on building their business rather than tracking deadlines. Contact VJM Global at info@vjmglobal.com or +91 98915 76441 to discuss your India market entry.