Yet convergence doesn't mean identical. Effective dates can differ, Malaysian terminology replaces IASB nomenclature, and private companies have access to a simplified alternative framework entirely. For finance teams and advisors navigating Malaysian reporting obligations, understanding these distinctions matters.

This article covers Malaysia's IFRS journey, the regulatory bodies behind it, how MFRS compares to IFRS, framework selection between MFRS and MPERS, sustainability reporting under IFRS S1 and S2, and key practical considerations for foreign companies.

Key Takeaways

- MFRS is substantively word-for-word identical to IFRS, allowing companies to assert compliance with both standards simultaneously

- Private entities (Sdn Bhd) may use the simpler MPERS framework instead of full MFRS

- The MFRS Framework took effect 1 January 2012; Transitioning Entities in agriculture and real estate adopted by 1 January 2018

- Malaysia adopted IFRS S1 and S2 via the National Sustainability Reporting Framework (NSRF) (September 2024), following a phased, climate-first rollout

- The IFRS Foundation's June 2025 profile classified Malaysia as adopting ISSB Standards with limited transition

Malaysia's IFRS Journey: From Convergence to Full Adoption

The Path to 2012

Malaysia's financial reporting history traces back to 1997, when the Malaysian Accounting Standards Board (MASB) was established under the Financial Reporting Act 1997 (Act 558). On 29 December 2004, MASB announced that existing standards would be renamed Financial Reporting Standards (FRS), effective 1 January 2005.

The decisive step came on 1 August 2008, when MASB announced a roadmap for full IFRS convergence by 1 January 2012. On 19 November 2011, MASB issued the MFRS Framework, applicable for annual periods beginning 1 January 2012.

Convergence, Not Adoption — Why the Distinction Matters

Malaysia uses the term "convergence" rather than "adoption" because MASB follows its own due process and domestic legislation before issuing standards. The substance, however, is near-identical: MFRS reproduces IFRS Standards word-for-word, preserves all IFRS accounting policy options, and requires financial statements to include an explicit, unreserved statement of compliance with IFRS Standards under MFRS 101 paragraph 16AA.

For multinational groups reviewing Malaysian accounts, the distinction carries no practical weight. MFRS and IFRS compliance can be asserted simultaneously.

Transitioning Entities

Not all companies adopted MFRS in 2012. Entities in specific sectors — along with their parents, significant investors, and joint venture partners — were permitted to defer. The two qualifying categories were:

- MFRS 141 Agriculture — entities involved in agricultural activity

- IC Interpretation 15 — real estate developers recognising revenue from construction agreements

Several deadline extensions followed, tied to the IASB completing IFRS 15 (revenue recognition) and amendments to IAS 41 (bearer biological assets). The mandatory effective date for all remaining Transitioning Entities was ultimately set at 1 January 2018.

Since then, MASB has tracked IASB pronouncements closely — meaning companies reporting under MFRS today are working with standards that mirror current global IFRS, with no material lag for most practical purposes.

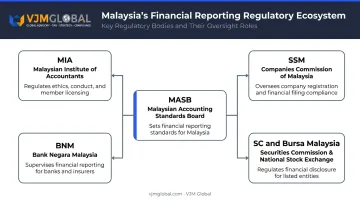

Key Regulatory Bodies Governing Financial Reporting in Malaysia

MASB: The Standard-Setter

The Malaysian Accounting Standards Board is the independent authority empowered under Section 7 of the Financial Reporting Act 1997 to issue, review, and revise approved accounting standards. MASB participates in IASB consultations and is a member of the Asian-Oceanian Standard-Setters Group (AOSSG).

Its due process includes local comment periods, typically timed so that Malaysian responses are submitted approximately one month before IASB deadlines — not a fixed 90–120 day window.

The Broader Regulatory Ecosystem

| Body | Role |

|---|---|

| MIA (Malaysian Institute of Accountants) | Sets ethical standards; regulates 41,000+ registered members |

| SSM (Companies Commission of Malaysia) | Registers companies; enforces financial statement filing via MBRS |

| BNM (Bank Negara Malaysia) | Financial reporting oversight for licensed banks, insurers, and holding companies |

| SC (Securities Commission Malaysia) | Oversees listed corporations; enforces compliance with approved standards |

| Bursa Malaysia | Imposes continuing reporting obligations on listed issuers |

Legal Force

Section 26D of the Financial Reporting Act 1997 requires financial statements lodged with BNM, the SC, or the Registrar of Companies (SSM) to comply with approved accounting standards. This gives MFRS the force of law — non-compliance carries statutory consequences, not just technical shortcomings.

Are MFRS and IFRS the Same?

For current reporting purposes, the answer is yes in substance. MFRS reproduces IFRS Standards using Malaysian nomenclature (for example, "MFRS 15" instead of "IFRS 15"), preserves all IFRS accounting policy options, and aligns effective dates with IASB pronouncements.

MFRS 101 paragraph 16 requires an explicit compliance statement; paragraph 16AA additionally requires MFRS-compliant statements to assert compliance with IFRS Standards. A dual statement of compliance with both MFRS and IFRS is therefore valid.

That said, three operational differences matter in practice:

- Malaysian standard numbering uses "MFRS" prefix throughout

- MASB must formally announce each new or amended standard before it gains legal status under Malaysian law

- MASB must complete its own due process before a standard applies locally, which can result in minor timing differences relative to IASB issuance

None of these differences touch recognition, measurement, or disclosure requirements. Malaysia has not eliminated any accounting policy option permitted by IFRS — so for consolidation packages, investor reporting, and cross-border audits, MFRS-compliant statements carry the same weight as IFRS-compliant ones.

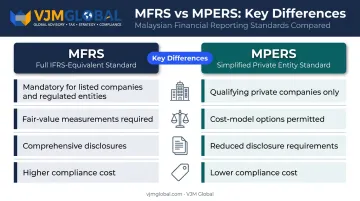

MFRS vs. MPERS: Choosing the Right Framework

Who Must Use MFRS

MFRS is mandatory for all non-private entities, specifically:

- Companies listed on Bursa Malaysia

- Financial institutions regulated by BNM

- Entities licensed by the Securities Commission

- Subsidiaries, associates, and jointly controlled entities of the above

Who Can Use MPERS

MASB issued MPERS on 14 February 2014, effective for periods beginning 1 January 2016. MPERS (2025), aligned with the IASB's third edition of IFRS for SMEs, replaces MPERS (2016) for periods beginning 1 January 2027.

An entity qualifies for MPERS if it is:

- A private company under the Companies Act

- Not required to prepare or lodge statements under SC- or BNM-administered law

- Not a subsidiary, associate, or jointly controlled entity of a MFRS-reporting entity

Key Simplifications Under MPERS

Compared to full MFRS, MPERS offers:

- Cost-model options for assets (no mandatory fair-value revaluation)

- Reduced disclosure requirements focused on material information

- Simplified financial instrument accounting

- A Malaysian-specific difference for property development activities

These simplifications meaningfully reduce compliance costs for smaller private companies, where the expense of full MFRS compliance — particularly fair-value measurements — may not be proportionate to user needs.

Switching Frameworks

Once a framework is selected, it must be applied in its entirety — mixing sections from MFRS and MPERS is not permitted. A private entity may voluntarily adopt full MFRS (for example, to align with a foreign parent or attract investment), but reverting to MPERS requires formal justification and both regulatory and auditor approval.

That asymmetry matters in practice: switching to MFRS is straightforward, but switching back is not. Entities should treat the initial framework decision as long-term.

IFRS S1 and S2: Malaysia's Sustainability Reporting Framework

The NSRF and Its Foundations

The Securities Commission Malaysia launched the National Sustainability Reporting Framework (NSRF) on 24 September 2024. Developed by the Advisory Committee on Sustainability Reporting (ACSR), chaired by the SC, the NSRF uses IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures) as its baseline.

Malaysia's approach is "climate-first" — entities prioritise IFRS S2 climate disclosures before full IFRS S1 implementation.

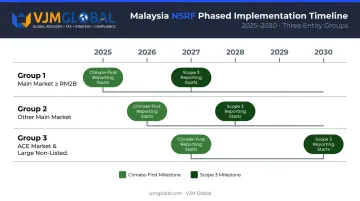

Phased Implementation Timeline

The NSRF phases in requirements across three entity groups:

| Group | Covered Entities | Climate-First Reporting Starts | Scope 3 GHG Starts |

|---|---|---|---|

| 1 | Main Market issuers with market cap ≥ RM2B at 31 Dec 2024 | 2025 | 2027 |

| 2 | Other Main Market issuers | 2026 | 2028 |

| 3 | ACE Market issuers and non-listed companies with annual revenue ≥ RM2B | 2027 | 2030 |

Broader IFRS S1 disclosures phase in after each group's climate-first period concludes.

Malaysia's Global Recognition

On 12 June 2025, the IFRS Foundation published its first 17 ISSB jurisdictional profiles, classifying Malaysia as "adopting ISSB Standards with limited transition." According to the Securities Commission's 13 June 2025 release, Malaysia is the only ASEAN jurisdiction to receive this recognition, confirming that the NSRF meets the IFRS Foundation's global sustainability reporting standards.

To support entities preparing for NSRF compliance, the ACSR introduced the PACE (Policy, Assumptions, Calculators, Education) initiative. PACE provides:

- GHG calculators for emissions measurement

- Guidance materials on disclosure requirements

- Training programs for reporting teams

Practical Implications for Foreign Companies in Malaysia

The Dual Reporting Reality

A Malaysian subsidiary of a foreign multinational must prepare standalone statutory financial statements under MFRS (or MPERS if eligible) for SSM filing purposes, while simultaneously providing data for group consolidation under the parent's reporting framework.

Where the parent reports under IFRS, the alignment is straightforward — MFRS and IFRS are substantively identical. For US GAAP parent companies, reconciliation will be required, particularly for differences in:

- Revenue recognition (timing and performance obligation treatment)

- Lease accounting (right-of-use asset presentation)

- Financial instrument classification and measurement

Obligations for Foreign Company Branches

Under Section 575 of the Companies Act 2016, a registered foreign company (branch) must lodge:

- Home-jurisdiction financial statements and auditor's report (generally within two months after its AGM)

- A duly audited statement of assets, liabilities, and profit/loss from Malaysian operations

Accounting records must be retained for seven years under Section 245(3).

Penalties for Non-Compliance

Non-compliance carries real consequences under the Companies Act 2016:

- Section 245(8): Directors responsible for failure to maintain adequate accounting records face fines up to RM500,000, imprisonment up to three years, or both

- Sections 258 and 259: Failure to circulate or lodge financial statements exposes responsible officers to fines up to RM50,000 per offence, plus continuing fines

SSM actively enforces these provisions — its 2022 enforcement report documents compounds and prosecutions for accounting record and lodgement failures.

Reconciling group IFRS or US GAAP accounts with Malaysian MFRS requirements across multiple jurisdictions is a genuine compliance risk. Working with experienced international accounting advisors reduces exposure to filing errors, missed deadlines, and audit risk. VJM Global supports multinationals navigating these multi-framework obligations through cross-border accounting and international tax advisory services.

Frequently Asked Questions

What are the financial reporting standards in Malaysia?

Malaysia operates under two MASB-issued frameworks: MFRS (full IFRS-equivalent, mandatory for non-private entities) and MPERS (IFRS for SMEs-based, for qualifying private companies). MPSAS governs public-sector reporting under the Accountant General's Department. Islamic banking institutions follow MFRS, supplemented by BNM Shariah requirements.

Are IFRS and MFRS the same?

Substantively yes. MFRS is word-for-word equivalent to IFRS Standards, preserving all accounting policy options and using IASB-aligned effective dates. MFRS 101 paragraph 16AA requires compliant statements to also assert IFRS compliance, making dual reporting valid when all requirements are met.

Is IFRS S1 and S2 mandatory in Malaysia?

Malaysia is adopting IFRS S1 and S2 through the NSRF using a phased, climate-first approach. Main Market issuers with market cap above RM2B began mandatory reporting in 2025, with other entity groups following in 2026 and 2027. Timelines vary by entity type, so confirm the requirements that apply to your organization.

What is the difference between MFRS and MPERS in Malaysia?

MFRS applies to listed companies, financial institutions, and regulated entities — it requires comprehensive disclosures and fair-value measurements. MPERS is a simplified alternative for qualifying private companies, offering cost-model options and reduced disclosure requirements at significantly lower compliance cost.

Who is required to use MFRS in Malaysia?

MFRS is mandatory for all non-private entities — Bursa Malaysia-listed companies, BNM-regulated financial institutions, SC-licensed entities, and their subsidiaries preparing consolidated financial statements. Private companies (Sdn Bhd) not meeting these criteria may use MPERS.

What are the consequences of non-compliance with MFRS in Malaysia?

Directors risk fines up to RM500,000 and up to three years' imprisonment under Section 245(8) for accounting record failures, while failure to lodge financial statements carries fines up to RM50,000 under Sections 258–259. SSM can also invoke strike-off powers under Section 549, and a poor enforcement record damages investor confidence.