Introduction

UK businesses managing intercompany transactions with Singapore entities face a dual compliance challenge that many finance teams underestimate. When a UK parent charges management fees, interest, or royalties to its Singapore subsidiary, that pricing must simultaneously satisfy both HMRC and IRAS — each with distinct thresholds, documentation formats, and enforcement mechanisms.

The stakes are high. Singapore's 17% corporate tax rate versus the UK's 25% makes transfer pricing scrutiny inevitable from both authorities.

This guide covers what UK businesses need to know across six areas:

- Singapore's transfer pricing legal framework

- Mandatory documentation requirements and thresholds

- Accepted pricing methods

- Penalties and surcharges

- Updates from the 8th Edition of the IRAS Transfer Pricing Guidelines (November 2025)

- How to keep your positions defensible under HMRC's parallel requirements

UK businesses face stricter intragroup financing rules, tightened documentation standards, and new simplified approaches. Navigating both regimes together requires a coordinated group TP policy.

TLDR:

- Singapore enforces arm's length pricing under Section 34D of the Income Tax Act, updated in the 8th Edition Guidelines (November 2025)

- Transfer Pricing Documentation is mandatory for businesses with gross revenue above S$10 million where related-party thresholds are breached

- IRAS imposes a 5% surcharge on TP adjustment values, plus fines up to S$10,000 for non-compliance

- The 8th Edition tightened intragroup loan rules, simplified TPD conditions, and piloted a new Simplified & Streamlined Approach (SSA) for routine distributors

- UK businesses must calibrate their group TP policy to satisfy both HMRC and IRAS expectations simultaneously

Understanding Transfer Pricing in Singapore: The Core Framework

What Transfer Pricing Means for UK-Singapore Transactions

Transfer pricing governs the pricing of goods, services, loans, royalties, and intellectual property between related entities in different jurisdictions. For UK businesses, Singapore is strategically important: its 17% corporate tax rate (compared to the UK's 25% main rate) creates an 8-percentage-point differential that makes pricing scrutiny a priority for both IRAS and HMRC.

Singapore's Legal Basis

The arm's length principle is codified in Section 34D of the Singapore Income Tax Act (ITA). The IRAS Transfer Pricing Guidelines — currently in their 8th Edition — provide the practical framework for applying it. Singapore follows OECD TP Guidelines and shares the UK's foundational approach, but its local documentation thresholds, safe harbour rules, and penalty regime differ in important ways.

Who Qualifies as Related Parties

That framework applies wherever a related-party relationship exists. Under Singapore law, two entities are related parties if one directly or indirectly controls the other, or both are under common control. In practice, this captures:

- A UK parent company and its Singapore subsidiary

- Singapore sister companies sharing a common UK holding entity

- Any arrangement where one party can influence the other's commercial decisions

Singapore's TP rules cover both cross-border and domestic related-party transactions. One notable exception: IRAS has confirmed that no adjustment will be imposed under Section 34D for domestic loans entered on or after 1 January 2025.

Advance Pricing Agreements (APAs)

Singapore offers three types of APAs as a proactive option for UK businesses wanting pricing certainty before IRAS raises a query:

- Unilateral APA — agreed with IRAS alone; faster but no protection against HMRC challenge

- Bilateral APA — agreed jointly between IRAS and HMRC; eliminates double taxation risk and locks in methodology upfront

- Multilateral APA — spans three or more tax authorities; relevant where a UK group has additional related parties in other jurisdictions

For most UK-Singapore structures, a bilateral APA offers the most complete protection.

Singapore Transfer Pricing Documentation: Who Must Comply and Key Thresholds

Primary Trigger: S$10 Million Gross Revenue

Businesses with gross revenue exceeding S$10 million in a basis period must prepare contemporaneous TP documentation. "Contemporaneous" means completed by the income tax return due date for that year, and documentation must be dated to prove this — a rule tightened in recent editions.

Transaction-Level Exemption Thresholds

From Year of Assessment (YA) 2026, the exemption threshold for non-goods transactions increased from S$1 million to S$2 million. Key thresholds:

- Purchase/sale of goods: S$15 million

- Related-party loans: S$15 million

- Services, royalties, rental, guarantees: S$2 million (up from S$1 million)

Exemption from documentation does not exempt a transaction from the arm's length requirement. UK businesses must still be able to justify their pricing if IRAS enquires.

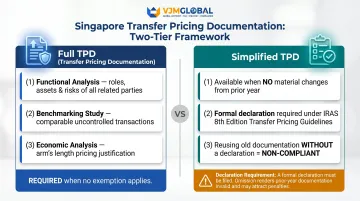

Two Tiers of Singapore TPD

- Full TPD (local file equivalent) covers functional analysis, benchmarking, and economic analysis — required when no exemption applies.

- Simplified TPD is available where there are no material changes from the prior year, but the 8th Edition rules now require a formal declaration to accompany it — reusing old documentation without this declaration is non-compliant.

Country-by-Country Reporting (CbCR)

UK parent companies heading groups with consolidated revenue above the OECD threshold (S$1,125 million) must submit CbC reports. Singapore does not require a separate Master File, but some information expected in a Master File overlaps with local TPD requirements.

Record Retention: Five Years

TP documentation and supporting records must be kept for at least five years. UK businesses must maintain accessible records for their Singapore entities, particularly when documentation is prepared centrally in the UK.

Accepted Transfer Pricing Methods Under Singapore's Guidelines

Five OECD-Aligned Methods

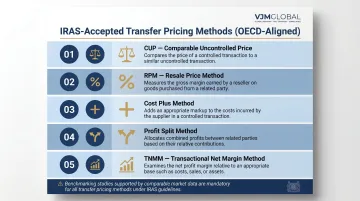

IRAS accepts the five OECD methods:

- Comparable Uncontrolled Price (CUP) — Compares pricing to similar uncontrolled transactions

- Resale Price Method (RPM) — Measures gross margin on resale activities

- Cost Plus Method (CPM) — Adds appropriate markup to costs incurred

- Profit Split Method — Allocates combined profits based on relative contributions

- Transactional Net Margin Method (TNMM) — Examines net profit margin relative to an appropriate base

Benchmarking studies are mandatory to support whichever method is selected, and taxpayers must justify the selected method based on the Singapore entity's functional profile. The choice of method also determines how working capital adjustments and comparability refinements apply in practice.

Working Capital Adjustments

The 8th Edition TPG confirmed that taxpayers can make working capital adjustments to comparables to improve reliability. Accepted interest rates include the actual cost of funding or commercial lending rates, consistent with OECD guidance.

Beyond these technical refinements, the 8th Edition also introduced a new compliance pathway for qualifying entities.

Simplified & Streamlined Approach (SSA) Pilot

The 8th Edition introduced a new SSA pilot for the period 1 January 2026 to 31 December 2028. Qualifying taxpayers with routine distribution and marketing support functions can apply a prescribed margin and be deemed to meet the arm's length standard.

Eligibility criteria:

- Operating expenses between 3% to 30% of annual net revenues

- Transaction reliably priced using a one-sided TP method

- Prescribed Return on Sales (ROS) of 1.50% to 5.50%, determined by industry grouping and asset/expense intensity

UK businesses with Singapore distribution entities that meet these thresholds can bypass full benchmarking studies — reducing both compliance costs and audit risk during the pilot period.

Penalties, Surcharges, and IRAS Audit Enforcement

5% TP Surcharge

Under Section 34E of the ITA, if IRAS determines that related-party transactions are not at arm's length and makes an adjustment, a 5% surcharge is applied to the value of that adjustment. The surcharge is separate from the additional tax arising from the adjustment itself and applies once a Notice of Assessment is issued. Objections must follow IRAS's formal Objection and Appeal Process.

Conditions for Surcharge Remission

IRAS may fully or partially reduce the surcharge if the taxpayer has good compliance records in the current and two immediately preceding years of assessment. The 8th Edition tightened this condition to exclude any taxpayer with a prior history of surcharges or penalties: a single compliance lapse can disqualify a business from remission entirely.

General Non-Compliance Fine

Separately from the surcharge, failure to prepare TPD can result in fines of up to S$10,000. This applies to:

- Not preparing TP documentation

- Not preparing documentation with prescribed details

- Not retaining documentation for five years

- Not submitting documentation within 30 days of IRAS request

- Providing false or misleading documentation

IRAS Audit Practices

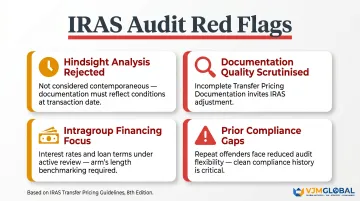

IRAS reviews TPD to assess arm's length compliance through a fact-finding and discussion process. Key enforcement signals from the 8th Edition include:

- Analysis conducted with hindsight is not considered contemporaneous and will not satisfy audit requirements

- Documentation quality is under heightened scrutiny — poorly prepared or incomplete TPD invites adjustment

- Intragroup financing arrangements are a specific focus area, with IRAS applying closer review to interest rates and loan terms

- Stricter enforcement applies to businesses with prior compliance gaps, who face less flexibility during audit

UK businesses should treat contemporaneous documentation as non-negotiable, not a formality prepared after the fact.

Key Updates from the 8th Edition of Singapore's Transfer Pricing Guidelines (2025)

Strengthened Guidance on Intragroup Financial Transactions

The most significant change for UK businesses: related-party loans must be reviewed periodically to ensure pricing remains arm's length as economic conditions shift. IRAS has clarified that tax deduction will not be allowed on interest expense exceeding the arm's length amount, even where withholding tax was paid on the full interest to the foreign related party.

UK parent companies lending to Singapore subsidiaries should reassess their loan pricing against these updated expectations.

Tightened Simplified TPD Rules

Two key changes affect UK businesses using group cost recharges into Singapore:

- Prior-year TPD reliance now requires a formal declaration confirming the documentation remains valid

- Pass-through cost arrangements must be supported by written agreements (including email correspondence) — invoices alone are no longer sufficient

Domestic Loan Exemption

For domestic related-party loans entered on or after 1 January 2025 (where neither party is in the lending business), IRAS will not make Section 34D TP adjustments. This is a clear departure from the 7th Edition's approach and reduces compliance burden for Singapore-to-Singapore related-party lending.

MAP (Mutual Agreement Procedure) Updates

The 8th Edition introduced guidance on when to file a protective MAP when domestic objections are running concurrently, and clarified how protective filings interact with ongoing domestic appeals. UK businesses facing a TP dispute involving both HMRC and IRAS should review their MAP filing timelines carefully — these updates directly affect how treaty rights under the UK-Singapore double tax agreement are preserved during concurrent proceedings.

How UK Businesses Should Structure Their Singapore TP Compliance Approach

Practical Compliance Sequence

UK businesses should follow this structured approach:

- Map all intercompany transactions with Singapore entities and assess whether they cross documentation thresholds

- Determine the most appropriate TP method for each transaction type and prepare or update benchmarking studies

- Ensure TPD is completed and dated by the Singapore tax filing deadline

- Review intragroup loan arrangements against the 8th Edition financing guidance

- Assess SSA pilot eligibility for any routine distribution entities

Aligning UK and Singapore TP Positions

UK businesses must ensure their Singapore TP positions are also defensible under HMRC's rules. Since both jurisdictions follow OECD guidelines, positions should be consistent — but thresholds, documentation formats, and surcharge mechanisms differ.

Under the UK Transfer Pricing Records Regulations 2023, UK entities in MNE groups meeting the CbCR threshold must maintain Master File and Local File documentation. SME exemptions under Section 166 TIOPA 2010 may apply to smaller UK businesses.

Group TP policy should be calibrated for both HMRC and IRAS expectations, not just one jurisdiction. Businesses managing obligations across both regimes — such as the 250+ UK clients VJM Global has supported with international tax compliance — often benefit from advisors who understand both UK and Asia-Pacific requirements to avoid misalignments between group policy and local filings.

Proactive Use of APAs

For material, recurring intercompany transactions — particularly intragroup services, IP licensing, and financing — UK businesses should consider applying for a bilateral APA between IRAS and HMRC. This removes uncertainty and protects against double taxation by locking in agreed pricing methodology upfront. The UK-Singapore Double Taxation Agreement includes MAP provisions (Article 26) and associated enterprises provisions (Article 9) enabling correlative adjustment relief.

Frequently Asked Questions

What is transfer pricing in Singapore?

Transfer pricing refers to the pricing of transactions between related entities, such as a UK parent and its Singapore subsidiary. Singapore requires such transactions to comply with the arm's length principle under Section 34D of the Income Tax Act, enforced through the IRAS Transfer Pricing Guidelines.

What transfer pricing documentation is required in Singapore and who must prepare it?

Singapore requires local Transfer Pricing Documentation (TPD) and Country-by-Country Reporting (CbCR). Businesses with gross revenue exceeding S$10 million must prepare TPD. Parent entities must submit CbC reports if the group meets the OECD revenue threshold of S$1,125 million.

What is the threshold for transfer pricing documentation in Singapore?

From YA 2026, the transaction-level exemption threshold for non-goods transactions is S$2 million (increased from S$1 million), but the gross revenue trigger for mandatory TPD preparation remains at S$10 million. Falling below the threshold does not exempt a transaction from the arm's length requirement.

How do you prepare transfer pricing documentation in Singapore?

TPD must be completed by the income tax return due date and include a functional analysis, TP method selection and justification, and a benchmarking study. Businesses with no material changes from the prior year may use Simplified TPD, provided they include a formal declaration under the 8th Edition rules.

What is the penalty for non-compliance with transfer pricing rules in Singapore?

IRAS imposes two key penalties: a 5% surcharge on the value of any TP adjustment made under Section 34E, plus a fine of up to S$10,000 for failure to prepare documentation. The surcharge applies regardless of whether additional tax is payable.

What is the Singapore Master Transfer Pricing Guide?

This refers to the IRAS e-Tax Guide: Transfer Pricing Guidelines, currently in its 8th Edition (released November 2025). It covers how IRAS applies the arm's length principle, documentation requirements, accepted TP methods, and dispute resolution procedures.