Introduction

India pulled in $81.04 billion in FDI in 2024 — the highest in three years — and Singapore entrepreneurs are driving a significant share of that flow. The economy grew 6.5% that year, and Singapore alone contributed $17.6 billion (37% of total inflows) in the first nine months of FY2025-26, cementing its position as India's largest FDI source for seven consecutive years.

Yet a fundamental confusion stalls many entry plans: "LLC" does not exist as a legal structure in India. Singapore founders search for "LLC registration in India" assuming a direct equivalent to their Pte Ltd, only to encounter a legal vacuum. The term has no standing under the Companies Act, 2013. This gap leads to registration errors, wrong structure choices, and compliance delays that can cost months of rework before operations even begin.

This guide clarifies what "LLC registration in India" actually means and maps you to the correct legal structures: Private Limited Company or Limited Liability Partnership. It covers exact registration steps, costs, required documents, and tax implications — including how the India-Singapore Double Taxation Avoidance Agreement can reduce your tax burden immediately upon registration.

Key Takeaways

- India has no "LLC" — the closest equivalents are Private Limited Company (Pvt Ltd) and Limited Liability Partnership (LLP) under the Companies Act, 2013

- Singapore entrepreneurs can own 100% of an Indian Pvt Ltd under the automatic FDI route in most sectors

- At least one director must reside in India for 182+ days in the prior year — appointing a resident nominee director resolves this requirement

- The SPICe+ portal handles name reservation, DIN, PAN, TAN, and incorporation in one integrated filing — typically 7–15 working days

- The India-Singapore DTAA limits withholding tax to 10–15% on interest, royalties, and fees for technical services

What Is an LLC in India?

"LLC" is not a legal term under Indian corporate law. The Companies Act, 2013 does not define or recognize "Limited Liability Company." Unlike the U.S., UK, or Singapore, India's legislation uses different nomenclature. When foreign founders search for "LLC in India," they're broadly referring to any structure offering limited liability protection.

Two primary equivalents exist:

| Structure | Governance | Limited Liability | FDI Allowed | Best For |

|---|---|---|---|---|

| Private Limited Company (Pvt Ltd) | Companies Act, 2013 | Yes — shareholder liability limited to share value | 100% under automatic route (most sectors) | Scalable businesses, investor-ready ventures, multi-sector operations |

| Limited Liability Partnership (LLP) | LLP Act, 2008 | Yes — partner liability limited to contribution | Restricted (government approval only, sector limits apply) | Professional services, consulting, smaller ventures without foreign investment |

For most Singapore entrepreneurs, the table above makes the choice straightforward. A Pvt Ltd allows full foreign ownership, supports up to 200 shareholders, and creates a credible corporate entity suitable for customer contracts, institutional relationships, and future fundraising.

An LLP carries fewer compliance obligations, but it does not permit 100% FDI, a critical disqualifier for most foreign investors.

Why Singapore Entrepreneurs Are Choosing India

India's GDP hit $3.91 trillion in 2024, growing at 6.5% — making it one of the fastest-expanding major economies in the world. For Singapore entrepreneurs, the timing matters: sectors like manufacturing, fintech, and consumer goods still have room for early entrants to establish durable positions.

Singapore's capital flows into India reflect this opportunity. Singapore contributed $14.94 billion in FY2024-25 (19% of total inflows) and $17.6 billion in just April–December of FY2025-26 (a 37% share), making it India's top FDI source for seven consecutive years. That volume isn't coincidental — it's backed by a formal bilateral framework that reduces friction and cost for Singapore investors specifically.

That framework rests on three pillars:

- CECA (Comprehensive Economic Cooperation Agreement): In force since August 2005, CECA bundles a free trade agreement, bilateral investment treaty, improved DTAA, and broad economic cooperation. Total India-Singapore bilateral trade reached $34.26 billion in FY2024-25.

- India-Singapore DTAA: Cuts withholding tax to 10–15% on dividends, 10% on interest (banks and financial institutions), 10% on royalties, and 10% on technical service fees — rates unavailable to investors from countries without an equivalent treaty.

- Tax-efficient holding structures: Singapore entities are commonly used as intermediate holding companies for India-bound investment, combining Singapore's low corporate tax rates with DTAA treaty benefits to reduce the overall tax burden on repatriated profits.

In practice, this means Singapore founders enter India with established legal pathways, treaty-backed protections, and a large peer group who have already worked through the regulatory process — a meaningful head start compared to investors from most other jurisdictions.

Choosing the Right Business Structure: Pvt Ltd vs. LLP for Singapore Entrepreneurs

Private Limited Company (Pvt Ltd) — Recommended for Most

Core advantages:

- 100% FDI under automatic route in most sectors (no prior government approval required)

- Supports up to 200 shareholders (individuals or corporate entities)

- Creates a separate legal entity suitable for customer contracts, institutional relationships, and investor readiness

- Preferred by VCs and institutional investors for future funding rounds

- Clear governance framework under Companies Act, 2013

Requirements:

- Minimum 2 directors (at least 1 must be an India resident)

- Minimum 2 shareholders (can be the same as directors; can be Singapore individuals or corporate entities)

- Registered office address in India (leased space acceptable)

- No minimum paid-up capital mandated by law (₹1 lakh is standard practice)

Who should choose Pvt Ltd: Singapore entrepreneurs planning to scale, seek investment, operate across multiple sectors, or build a long-term India presence.

Limited Liability Partnership (LLP) — Restricted for Foreign Investors

Advantages:

- Fewer mandatory compliances than Pvt Ltd

- No minimum capital requirement

- Simpler governance structure

Critical limitation for Singapore investors:

100% foreign ownership is NOT permitted in an LLP under India's FDI policy. FDI in LLPs requires government approval (not automatic route) and is restricted to sectors where 100% FDI is allowed in companies with no performance conditions.

Additional restrictions for foreign-owned LLPs:

- No FII/FVCI investment allowed

- Cannot access External Commercial Borrowings (ECBs)

- Cannot make downstream investments (investing in other entities)

- Prohibited from agricultural/plantation activity, print media, and real estate business

Bottom line: LLPs suit Indian residents or joint ventures where the foreign partner holds a minority stake. For Singapore entrepreneurs seeking full ownership, Pvt Ltd is the clear path.

One Person Company (OPC) — Generally Inapplicable

OPC is designed for Indian residents only. It is not available to Singapore entrepreneurs unless they hold OCI (Overseas Citizen of India) status and qualify as Indian residents. Confirm eligibility with a legal advisor before considering this route.

FDI Sector Restrictions: Where Government Approval Is Required

While most sectors allow 100% automatic FDI into a Pvt Ltd, certain sectors require prior government approval beyond specified thresholds:

| Sector | FDI Cap | Govt Approval Threshold |

|---|---|---|

| Defence | 100% | Beyond 74% |

| Broadcasting (News TV, FM Radio) | 49% | Up to 49% |

| Digital Media (News & Current Affairs) | 26% | Up to 26% |

| Print Media (newspapers/periodicals) | 26% | Up to 26% |

| Multi-Brand Retail Trading | 51% | Up to 51% |

| Banking - Private Sector | 74% | Beyond 49% |

| Pharmaceuticals - Brownfield | 100% | Beyond 74% |

Note: Press Note 3 (2020) requires government approval for any FDI from entities in countries sharing a land border with India (China, Pakistan, Bangladesh, Myanmar, Nepal, Bhutan, Afghanistan). This does not apply to Singapore investors directly.

Prohibited sectors (no FDI allowed): Lottery, gambling, chit funds, tobacco manufacturing, atomic energy, and railway operations (except permitted activities).

Refer to DPIIT's Consolidated FDI Policy for current sector classifications.

Eligibility Requirements for Singapore Entrepreneurs

Resident Director Requirement (Non-Negotiable)

Under Section 149(3) of the Companies Act, 2013, at least one director must have resided in India for 182+ days during the preceding financial year.

Singapore entrepreneurs who don't live in India typically appoint a professional nominee director through a business setup firm — such as VJM Global — to meet this requirement legally.

Other Requirements

- Requires at least 2 shareholders — Singapore individuals or corporate entities qualify, and they can also serve as directors

- Registered office must be a physical Indian address; leased space works with a rental agreement and landlord's No Objection Certificate

- No statutory minimum paid-up capital, though ₹1 lakh is standard practice and builds credibility with banks and partners

Step-by-Step: How to Register an LLC in India

All company registrations in India are processed through the Ministry of Corporate Affairs (MCA) portal. Typical timeline: 7-15 working days when documents are correctly prepared. Delays typically stem from name objections or incomplete documentation.

Step 1: Obtain a Digital Signature Certificate (DSC)

All proposed directors must obtain a Class 3 DSC from a government-authorized certifying authority. This is required to digitally sign and file documents on the MCA portal.

Costs (from VSign):

- Indian nationals: ₹750-₹1,200 (1-3 years)

- Foreign nationals: ₹3,220-₹5,720 (1-3 years)

- USB token: ~₹500 additional

Singapore-based directors can apply online using a valid passport and address proof.

Step 2: Apply for Director Identification Number (DIN)

Every director must have a DIN — a unique identifier issued by the MCA. DIN applications are now integrated into the SPICe+ form at incorporation, so no separate advance application is needed.

Step 3: Reserve a Company Name via RUN Service

Use the MCA's RUN (Reserve Unique Name) service to check availability and reserve your company name.

Naming rules:

- Name must end with "Private Limited"

- Must not be identical or deceptively similar to existing registered entities

- Must comply with MCA naming guidelines

Procedural details:

- Fee: ₹1,000 per application

- Submit up to 2 proposed names as backups

- Approved name is reserved for 20 days

Step 4: Prepare Incorporation Documents

Required documents:

- Memorandum of Association (MoA) — outlines business objectives and authorized capital

- Articles of Association (AoA) — governs internal operations and director authority

- Passport (mandatory identity proof for foreign nationals)

- Bank statement or utility bill as address proof (not older than 2 months)

- Recent passport-sized photographs of all directors and shareholders

- Registered office proof: rental agreement or sale deed, utility bill, and landlord's NOC if leased

Step 5: File SPICe+ Incorporation Application on MCA Portal

With documents in order, submit Form SPICe+ (INC-32) along with MoA, AoA, DSC, director declarations, and registered office proof. The Registrar of Companies (RoC) reviews the application and issues a Certificate of Incorporation upon approval.

SPICe+ integrates 10 services into one filing:

- Name reservation (Part A)

- Company incorporation (Part B)

- DIN allotment (up to 3 directors)

- PAN (Permanent Account Number)

- TAN (Tax Deduction Account Number)

- EPFO registration

- ESIC registration

- Professional Tax registration (state-specific)

- Bank account opening request

- GSTIN (optional GST registration)

Timeline: 3-5 working days for SPICe+ verification; 2-3 working days for Certificate of Incorporation issuance.

VJM Global's role: The business setup team can manage the entire SPICe+ filing process on behalf of Singapore entrepreneurs, covering DSC coordination, MoA/AoA drafting, and RoC liaison to cut processing time and avoid common rejection errors.

Step 6: Obtain PAN, TAN, and Open a Business Bank Account

Once the Certificate of Incorporation is issued, PAN and TAN are automatically generated through the SPICe+ process. The company must then open a business bank account in India to receive and transact funds.

FEMA compliance: Foreign currency remittances from Singapore follow FEMA (Foreign Exchange Management Act) guidelines. Post-facto reporting to the RBI is required for FDI inflows.

Step 7: Register for GST (If Applicable)

GST registration is mandatory if annual turnover exceeds:

- ₹40 lakh for suppliers of goods (normal category states)

- ₹20 lakh for suppliers of services or goods in special category states

Even below-threshold businesses may voluntarily register to claim input tax credits and appear credible to B2B clients. Verify current thresholds at the CBIC GST Portal.

Documents Required, Costs, and Key Tax Obligations

Documents Required

For directors and shareholders:

- Passport (mandatory for foreign nationals)

- Digital Signature Certificate (DSC)

- Director Identification Number (DIN)

- Address proof (bank statement or utility bill, not older than 2 months)

- Recent passport-sized photograph

For the company:

- Memorandum of Association (MoA)

- Articles of Association (AoA)

- Proof of registered office address (rental agreement or sale deed + utility bill)

- No Objection Certificate (NOC) from landlord (if operating from leased premises)

Registration Costs

Government filing fees (SPICe+ INC-32):

| Authorized Share Capital | Government Fee |

|---|---|

| Up to ₹15,00,000 | NIL |

| ₹15,00,001 to ₹50,00,000 | ₹2,000 |

| ₹50,00,001 to ₹1,00,00,000 | ₹2,000 + ₹200 per ₹10,000 above ₹50 lakh |

| Above ₹1,00,00,000 | ₹1,02,000 + ₹100 per ₹10,000 above ₹1 crore |

Additional costs:

- RUN name reservation: ₹1,000

- DIN application: ₹500 per director

- PAN + TAN: ₹143 (auto-generated via SPICe+)

- DSC (foreign national): ₹3,220–₹5,720 (1–3 years)

- USB token: ~₹500

Stamp duty (varies by state):

Stamp duty on MoA and AoA varies by state of registered office — the table below illustrates the range for ₹1 lakh authorized capital:

| State | MoA + AoA Total Stamp Duty |

|---|---|

| Ladakh, Sikkim | ₹0 |

| Dadra & Nagar Haveli | ₹40 |

| Karnataka, Punjab | ₹10,000 |

Professional advisory fees: Costs vary by service provider. VJM Global offers end-to-end incorporation support including advisory, document preparation, and filing services. Contact VJM Global directly for specific pricing.

Total cost range: For a basic Pvt Ltd incorporation with ₹1 lakh authorized capital, expect total costs (government fees + DSC + stamp duty + advisory) to range from approximately ₹15,000 to ₹30,000, depending on state and service provider.

Key Tax Obligations

Once incorporated, your Indian entity faces three main compliance areas: corporate income tax, transfer pricing on related-party transactions, and treaty-based withholding on payments back to Singapore.

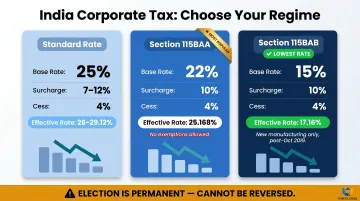

Corporate Income Tax — three regimes to choose from:

| Tax Regime | Base Rate | Surcharge | Cess | Effective Rate |

|---|---|---|---|---|

| Standard (turnover up to ₹400 Cr) | 25% | 7–12% | 4% | 26.00%–29.12% |

| Section 115BAA (concessional, no exemptions) | 22% | 10% | 4% | 25.168% |

| Section 115BAB (new manufacturing, post-Oct 1, 2019) | 15% | 10% | 4% | 17.16% |

Key considerations:

- Section 115BAA requires permanently forgoing specified exemptions (additional depreciation, SEZ benefits, etc.)

- Section 115BAB applies only to new manufacturing companies incorporated after October 1, 2019

- MAT (Minimum Alternate Tax) does not apply to companies opting for 115BAA or 115BAB

- Once elected, this choice cannot be reversed

India-Singapore DTAA Benefits:

The DTAA reduces withholding tax on key cross-border payments:

| Income Type | DTAA Rate | Domestic Rate (Without Treaty) |

|---|---|---|

| Dividends | 10% (25%+ shareholding) / 15% (other) | Up to 20% |

| Interest | 10% (banks/financial institutions) / 15% (other) | Up to 40% |

| Royalties | 10% | Up to 10% |

| Fees for Technical Services | 10% | Up to 10% |

DTAA capital gains amendment (2016): Shares acquired after April 1, 2017 are subject to source-based taxation (India has the right to tax). Shares acquired before April 1, 2017 remain governed by prior residence-based rules.

Limitation of Benefits (LOB) clause: To claim treaty benefits for capital gains, the Singapore entity must incur at least S$200,000 (in Singapore) or INR 25,00,000 (in India) in annual operational expenditure. This prevents shell company treaty shopping.

Structure cross-border payments — dividends, royalties, and service fees — with DTAA rates in mind before your first transaction. Obtain a Tax Residency Certificate (TRC) from Singapore's IRAS to claim treaty benefits; without it, Indian counterparties will apply domestic withholding rates by default.

Common Mistakes Singapore Entrepreneurs Make When Registering an LLC in India

Choosing LLP Thinking It Allows Full Foreign Ownership

This is the most frequent error. Singapore entrepreneurs familiar with their Pte Ltd structure assume India's LLP is a direct equivalent. In reality, 100% FDI into an LLP is not permitted under India's current FDI policy. Foreign investment in LLPs requires government approval, is restricted to specific sectors, and carries severe operational limitations (no ECBs — external commercial borrowings — no downstream investment, no FII/foreign institutional investor participation).

Result: The entrepreneur may be forced to restructure or take on an Indian partner. Converting from an LLP to a Pvt Ltd with existing FDI requires prior government approval, creating delays and costs.

Solution: Always verify the FDI route before selecting the entity type. For full foreign ownership, choose Pvt Ltd.

Underestimating the Indian Resident Director Requirement

Many Singapore founders assume they can register and manage the company entirely remotely without any India presence. Section 149(3) of the Companies Act, 2013 mandates at least one director who has resided in India for 182+ days in the preceding financial year.

Result: Application rejection at the RoC level.

Solution: Appoint a qualifying resident director before incorporation. Professional resident director services are a standard offering from India-based advisory firms like VJM Global, handling the appointment process and ongoing compliance obligations.

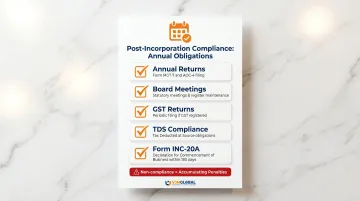

Neglecting Post-Incorporation Compliance

Registration is only the beginning. Indian companies must:

- File annual returns (Form MGT-7 and AOC-4)

- Hold board meetings and maintain statutory registers

- File GST returns (if registered)

- Comply with TDS (Tax Deducted at Source) obligations

- Submit Form INC-20A (Declaration for Commencement of Business) within 180 days of incorporation

Singapore entrepreneurs who treat India incorporation as a one-time task often accumulate penalties for non-compliance.

Engage an India-based compliance partner early. VJM Global's team handles annual return filing, GST compliance, TDS management, and board meeting documentation — drawing on 30+ years of experience with foreign companies entering India.

Additional Risks

- Skipping DPIIT sector verification before assuming 100% automatic FDI eligibility

- Failing to report foreign currency remittances or downstream investments to the RBI under FEMA

- Assuming CECA grants automatic regulatory benefits without confirming its specific coverage (trade, investment framework, DTAA)

Frequently Asked Questions

What is an LLC company in India?

"LLC" is not a legally defined term in India. The closest equivalents are Private Limited Company (Pvt Ltd) and Limited Liability Partnership (LLP) under the Companies Act, 2013, both offering limited liability protection and separate legal entity status.

Can I register an LLC in India?

Yes — Singapore entrepreneurs can register an equivalent entity in India, specifically a Pvt Ltd company allowing 100% FDI under the automatic route in most sectors, provided they meet the resident director and documentation requirements.

How much does it cost to open an LLC in India?

For a basic Pvt Ltd with ₹1 lakh authorized capital, total costs typically fall between ₹15,000 and ₹30,000. This covers:

- Government fees: ₹0–₹2,000 (varies by capital)

- DSC charges: ₹3,220–₹5,720 for foreign nationals

- Stamp duty: ₹0–₹10,000 depending on state

- Professional advisory fees (variable)

Which is better, LLC or LLP in India?

For Singapore entrepreneurs seeking full foreign ownership and scalability, Pvt Ltd is better since 100% FDI is allowed under the automatic route. An LLP does not permit full foreign ownership under FDI rules and is suitable only for professional service ventures with Indian partners.

Which is better, LLP or OPC?

OPC (One Person Company) is restricted to Indian residents — Singapore entrepreneurs qualify only if they hold OCI status. For most Singapore entrepreneurs, LLP is also limited due to FDI restrictions, making it viable only in specific professional service contexts with Indian partners.

Ready to register your Indian Pvt Ltd company? VJM Global manages the full process — resident director appointment, SPICe+ filing, post-incorporation compliance, and DTAA advisory — so you can focus on your business, not the paperwork.

Contact VJM Global: info@vjmglobal.com | +91 98915 76441