Introduction

The US market generates over $27 trillion in GDP annually — and for UK companies ready to move beyond exporting, a branch office is the fastest way to establish a direct commercial footprint there. Unlike forming a US subsidiary, a branch operates under your existing UK legal identity, with no separate US incorporation required.

That said, many UK business owners and directors underestimate the legal, tax, and operational complexity involved. Choosing the wrong structure or skipping critical compliance steps can expose your UK parent company to unlimited US liability and trigger unexpected tax burdens like the branch profits tax.

Missing state-level registration requirements alone can result in IRS penalties and back taxes that stall operations from the start.

This guide covers:

- What a US branch office is and how it compares to a subsidiary

- The step-by-step registration process across US states

- Federal and state tax obligations, including UK-US treaty implications

- Visa requirements for transferring UK staff

- Common pitfalls that cost UK companies time and money

Key Takeaways

- A US branch is an extension of your UK company, not a separate entity: faster to set up, but your UK company carries full liability for US operations

- Register in a US state, appoint a registered agent, obtain an IRS EIN, and comply with federal/state taxes

- The UK-US tax treaty can reduce branch profits tax from 30% to as low as 5% (or 0%), depending on your structure and planning

- UK employees working in the US need an L-1 visa (not just visitor status)

- Most UK businesses underestimate state selection, US employment law obligations, and ongoing HMRC reporting requirements

What Is a US Branch Office and Is It Right for Your UK Business?

A US branch office is a direct extension of your UK parent company that conducts business in America under the parent's legal name. Profits and liabilities flow directly back to the UK entity. This contrasts sharply with a US subsidiary (typically a C-Corporation or LLC), which is a separate legal entity incorporated under US law.

The core structural distinction:

| Attribute | Branch Office | US Subsidiary |

|---|---|---|

| Legal identity | Extension of UK parent | Separate US legal entity |

| Liability exposure | UK parent bears full liability | Limited liability protects parent |

| Tax treatment | Income taxed at parent level in UK and US | Separate US tax filings; treaty benefits |

| Setup complexity | Lower initial cost and faster | Higher setup cost; ongoing governance |

| Best for | Early-stage market testing, low litigation risk | Long-term commitment, liability protection |

That structural difference has direct legal consequences. Under US law, a branch is classified as a foreign corporation registering to do business in a state. According to Cornell Law School's Legal Information Institute, a foreign corporation must file notice of doing business, meet qualification standards, and pay applicable state taxes — or risk fines and injunctions.

Tax exposure is the other critical factor. Branch income is taxable in both the UK and the US. The US imposes a branch profits tax under IRC Section 884 — a 30% federal levy on profits earned in the US.

The 2001 UK-US Double Taxation Convention reduces that rate to 5% for qualifying UK companies, and potentially 0% where Limitation on Benefits tests are satisfied.

Who Should Consider a Branch Office?

A branch structure typically makes sense for UK companies that are:

- Testing the US market before committing to a full subsidiary setup

- Running sales, consulting, or client servicing with a small US headcount

- Operating in low-litigation sectors such as professional services or representative activities

- Planning a 1–2 year US presence before converting to a full subsidiary structure

- Expecting early operating losses that can offset UK parent profits

What often goes wrong: UK companies either over-invest in a full subsidiary when a branch would suffice, or they expose the UK parent to US legal claims by underestimating their litigation risk. If your US activities involve physical products, contractual disputes, or regulated industries, a subsidiary's liability shield is worth the additional setup cost.

How to Open a Branch Office in the USA: Step-by-Step Process

Most UK companies complete this process within 4–8 weeks, depending on state choice and complexity. The steps cover branch registration, tax identification, US banking, and ongoing compliance obligations.

Step 1: Choose Your US State of Registration

UK companies must register their branch in a specific US state. Your choice affects tax rates, regulatory burden, and business law framework.

Common state choices:

| State | Filing Fee (USD) | Key Advantages | Considerations |

|---|---|---|---|

| Delaware | $245 | Business-friendly courts, strong corporate law precedent | Must also register where you physically operate |

| Florida | $70 | Lowest filing fee, no state income tax | Sales tax compliance required |

| California | $100 | Access to major market | High ongoing franchise tax (minimum $800 annually) |

| New York | $225 | Financial services hub | Complex tax and employment regulations |

| Wyoming | $150 | Low fees, business-friendly | Limited local market access |

Note: All fees are payable in USD. GBP equivalents vary with exchange rates.

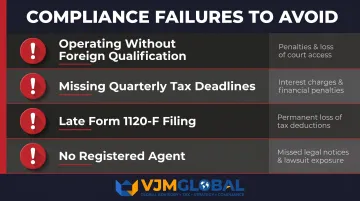

Critical rule: If you physically operate in a state (office space, employees, inventory), you must register there as a "foreign" (out-of-state) entity—even if you initially registered in Delaware. Operating without registration can result in fines, loss of court access, and back-tax assessments.

Step 2: Appoint a Registered Agent

Every US state requires a registered agent: a person or service with a physical address in the state who receives legal notices and official correspondence on your behalf.

UK-based directors cannot serve as their own registered agent. You'll need a commercial service, with annual costs ranging from around $100 (budget providers) to $250–$436 for mid-tier and premium options like CT Corporation. Premium services typically include compliance calendars, document management, and faster notice forwarding — worth considering if your US operations involve litigation risk.

Step 3: File Registration Documents with the State

To register, file an Application for Authority (or equivalent) with your chosen state's Secretary of State office.

Required documents typically include:

- Certified copy of your UK certificate of incorporation

- Statement of company details (name, registered address, directors)

- Certificate of Good Standing from Companies House (issued within 60 days)

- Registered agent appointment form

- State filing fee payment

Processing times range from 1–4 weeks for standard filing. Most states offer expedited processing (24–48 hours) for additional fees of $50–$150.

Step 4: Obtain a US Employer Identification Number (EIN)

An EIN from the Internal Revenue Service functions as your US tax identification number. You need it to open a bank account, hire employees, and file federal taxes.

Application methods for foreign entities:

| Method | Timeline | Contact |

|---|---|---|

| Telephone | Immediate (assigned during call) | +1-267-941-1099 (Mon–Fri, 6am–11pm ET) |

| Fax | 4 business days | +1-304-707-9471 |

| 4 weeks | IRS, Cincinnati, OH 45999 |

The online application is not available to companies whose principal place of business is outside the US. Use Form SS-4, and on Line 7b, enter "foreign" or "N/A" if your responsible party lacks a US Social Security Number.

Step 5: Open a US Business Bank Account

Opening a US bank account is often the most time-consuming step for UK companies. Most major banks (Bank of America, Chase, Citibank) require in-person documentation for foreign entities, including:

- Branch registration certificate (Certificate of Authority)

- EIN confirmation letter

- UK parent company incorporation documents

- Passport copies of authorised signatories

- Board resolution authorising the account

- Proof of US business address

Timeline: Expect 2–6 weeks for document review and compliance checks. International banks with US presence (HSBC, Barclays US) may offer faster routes for existing UK clients.

Step 6: Register for State and Federal Tax Obligations

Your branch must register with:

- Federal: File Form 1120-F (U.S. Income Tax Return of a Foreign Corporation) annually

- State income tax: Register in each state where you operate

- State sales tax: If selling products, register for sales and use tax permits

- Payroll taxes: If employing US staff, register for federal and state employment taxes

Quarterly estimated tax payments begin from your first year of operation.

⚠️ Critical deadline: Missing the 18-month filing deadline for Form 1120-F can result in permanent loss of deductions — meaning you're taxed on gross rather than net income. Set this as a hard calendar date from day one of US operations.

Legal, Tax, and Compliance Considerations for UK Companies

UK-US Tax Treaty Implications

The 2001 UK-US Double Taxation Convention provides significant relief, but only if structured properly.

Branch Profits Tax: Under IRC Section 884, the standard rate is 30% on effectively connected earnings. The treaty reduces this to 5% for qualifying UK corporations owning at least 10% voting power, and potentially 0% for companies meeting Limitation on Benefits tests.

Critical: You must file proper treaty claims to access these rates—default treatment is the statutory 30%.

HMRC Obligations for UK Parent Companies

Your UK company must continue filing UK corporation tax returns reporting US-sourced profits. HMRC's Double Taxation Relief Manual (DT19851) confirms that:

- Admissible for UK tax credit: US Federal income tax, Federal excise taxes, Net Investment Income Tax

- Not admissible: FICA (Social Security/Medicare), self-employment contributions

Transfer pricing rules apply to transactions between your UK parent and US branch. Proper documentation is essential to claim foreign tax credits and avoid double taxation.

Beneficial Ownership Information (BOI) Reporting

As of March 21, 2025, FinCEN issued an interim final rule that removed BOI reporting for US companies but retained it exclusively for foreign companies registered in any US state.

Requirements for UK branch offices:

- File beneficial ownership information within 30 days of state registration

- Report UK beneficial owners (not required to report US persons)

- Civil penalties of up to $500 per day for non-compliance

In practice, this means UK branches carry a reporting burden that newly formed US domestic companies do not.

State-Level Compliance Obligations

Forty-four states impose corporate income tax, with rates ranging from 2.25% (North Carolina) to 11.5% (New Jersey). Each state where your branch operates may require:

- Annual report filings ($50–$300 per state)

- State income tax registration and quarterly estimated payments

- Sales tax permits and monthly/quarterly filings (if selling products)

- Business licences and professional permits

Multi-state operations can trigger dozens of filing obligations. A single employee working remotely from another state can create tax nexus requiring separate registration.

Intellectual Property Protection

UK or EU trademark registrations provide no protection in the USA. Before or immediately upon US market entry:

- Register trademarks with the USPTO ($250–$350 per class)

- File patent applications separately with the USPTO

- Engage a US-licensed attorney (required for foreign trademark applicants since 2019)

Typical trademark timeline: 8–12 months for initial examination; 12–18 months total if no oppositions arise.

The Value of Dual-Jurisdiction Expertise

Navigating UK-US compliance requires advisors who understand both systems simultaneously — not just one side of the equation. At a minimum, your advisory team should cover:

- US federal filings: Form 1120-F preparation, treaty elections, and BOI compliance

- State-level obligations: Nexus analysis, multi-state registration, and sales tax

- HMRC coordination: Foreign tax credit claims, transfer pricing documentation, and UK return adjustments

- IP protection: USPTO filings coordinated with your existing UK registrations

VJM Global has served 250+ UK businesses on cross-border compliance and works with specialist US-side partners to ensure both the HMRC and IRS obligations are handled in tandem — so nothing falls through the gap between jurisdictions.

Staffing, Visas, and Employment Law Considerations

Visa Requirements for UK Employees

UK nationals cannot simply relocate to work in the US—even for your own branch office. The L-1 Intracompany Transferee visa is the most common route:

| Visa Type | Eligible Roles | Maximum Stay | Requirements |

|---|---|---|---|

| L-1A | Executives and managers | 7 years | 1 continuous year employment with UK parent in preceding 3 years |

| L-1B | Specialised knowledge workers | 5 years | Same employment requirement |

New office provision: Initial L-1 admission for a new US branch is limited to 1 year. You must demonstrate secured premises and financial ability to support operations.

Critical mistake: Using an ESTA or B-1 visitor visa for work activities beyond attending meetings. Working in the US without proper authorisation — even briefly — carries serious legal consequences including visa bans.

Employment Law for US-Based Hires

US employment law differs fundamentally from UK law. Key distinctions:

At-will employment: No requirement to show cause for dismissal (except in Montana). UK-style notice periods and disciplinary procedures don't apply unless contractually specified.

Benefits costs: BLS data (December 2025) shows private-sector benefits average 29.9% of total compensation — roughly $13.79 per hour on top of $32.36 in wages. Budget at least 30% above base salary for:

- Health insurance (no NHS equivalent — competitive necessity)

- Paid leave (no statutory minimum at federal level)

- Retirement contributions (401(k) matching)

- Social Security and Medicare (7.65% employer portion)

- Unemployment insurance and workers' compensation

State-specific requirements: Minimum wage, overtime rules, paid sick leave, and family leave vary significantly. California requires meal breaks; New York mandates wage theft notices; Massachusetts requires paid family leave contributions.

Employee vs. Independent Contractor Classification

The IRS applies a common law test examining three factors:

- Behavioural control: Do you control what work is done and how?

- Financial control: Does the worker have significant investment, unreimbursed expenses, opportunity for profit/loss?

- Type of relationship: Written contracts, benefits, permanency, whether services are key to your business

Getting this wrong is costly. Penalties for misclassification include:

- Employer's share of FICA and FUTA (7.65% + 0.6%)

- Percentage of federal income tax that should have been withheld

- Interest and penalties for failure to pay

- Criminal penalties in cases of wilful misclassification

A March 2024 Department of Labor rule restored a multi-factor "economic reality" test, tightening the classification standard. UK companies hiring US-based workers should review contractor arrangements carefully before operations begin.

Common Mistakes UK Companies Make When Opening a US Branch Office

Choosing a Branch for the Wrong Reasons

Many UK companies default to a branch structure because it appears simpler and cheaper—without analysing:

- Branch profits tax exposure: Even with treaty relief, the 5% rate can make total US tax burden higher than a subsidiary structure

- Liability risk: US litigation exposure is significantly higher than the UK; one lawsuit against your branch exposes your entire UK parent company

- Long-term tax efficiency: What saves £2,000 at setup can cost £20,000+ annually in additional taxes

Conduct proper tax modelling comparing branch vs. subsidiary before committing. The right structure depends on your specific revenue projections, profit margins, and risk profile.

Treating US Compliance as an Afterthought

UK companies often focus on commercial readiness—hiring sales teams, leasing office space, building marketing campaigns—before establishing proper legal infrastructure.

Common failures:

- Operating in multiple states without foreign qualification (triggering penalties and loss of court access)

- Missing quarterly estimated tax deadlines (incurring interest and penalties)

- Failing to file Form 1120-F within 18 months (permanently losing deductions)

- Not appointing a registered agent (missing legal notices and lawsuit service)

New York law (BCL Section 1312) explicitly bars unregistered foreign corporations from maintaining court actions. California imposes penalties of up to $25,000 per year for failure to file required information.

Applying UK Employment Practices to US Workers

UK-based HR teams managing small US workforces often apply UK policies directly:

- 3-month probation periods with progressive discipline procedures

- 4-week notice periods

- Statutory sick pay and parental leave standards

- TUPE-style protections

US employment is fundamentally at-will. Importing these UK practices creates unintended contractual obligations, wrongful termination exposure, and employee relations problems that can be costly to unwind.

The solution is US-specific employment documentation — offer letters, employee handbooks, confidentiality agreements — tailored to each state where you employ workers. Engage a US employment lawyer rather than relying on UK HR policies.

Frequently Asked Questions

How much does it cost to open a branch office in the USA?

One-time setup costs typically include state filing fees ($70–$245), a registered agent fee ($100–$300/year), and a free EIN application. Professional legal and accounting fees generally run $2,500–$6,500. Expect ongoing annual compliance costs of $2,000–$4,000 covering tax filings, state reports, and agent renewal.

How to open a branch office in the USA?

Choose a US state, appoint a registered agent with a physical address in that state, file an Application for Authority with the Secretary of State, obtain an EIN from the IRS by phone or Form SS-4, open a US business bank account, and register for federal and state tax obligations. The process typically takes 4–8 weeks from start to fully operational.

Who manages a branch office in the USA?

A branch is managed by whoever the UK parent company appoints—typically a US-based director, country manager, or transferred executive. No requirement exists to appoint a US citizen, but any UK national physically working in the US must hold an appropriate visa such as the L-1 intracompany transferee visa.

Can a UK company open a US branch office without a visa?

The branch itself can be registered without anyone physically present in the US, but any UK national who travels to the US to work (not just attend meetings) requires an appropriate work visa. The L-1 is most common for intracompany transfers; ESTA or B-1 visitor visas only permit limited business activities, not ongoing work.

What is the difference between a branch office and a subsidiary in the USA?

A branch has no separate legal identity — the UK parent bears full liability for all US obligations. A subsidiary is a separately incorporated US entity (typically a C-Corporation) that limits the parent's liability to its investment and generally offers better tax treaty access and protection from US litigation.

Do UK companies pay tax in both the UK and the USA on US branch income?

Yes — US-sourced branch income is taxable in both countries. The UK-US Double Taxation Treaty provides relief through exemption or a credit for US taxes paid, but the branch profits tax (up to 30%, or as low as 0% under treaty) may still apply. Professional tax advice before setup is essential.

Opening a US branch office offers UK companies a fast route to American market presence—but only when structured correctly. Get state selection, tax planning, and compliance infrastructure right from day one, and your branch becomes a valuable market-testing platform. Get it wrong, and you risk unlimited liability exposure, punitive tax treatment, and regulatory penalties that derail your expansion before it begins.