Introduction

A UK company receiving dividends from a US subsidiary, licensing IP to American clients, or employing staff on US soil can find itself taxed on the same income by both HMRC and the IRS. Without the right structure in place, that double exposure isn't a remote risk — it's a predictable outcome.

The US-UK Double Taxation Convention (DTC) exists precisely to prevent this. Yet most guidance focuses on US expatriates living in the UK, leaving UK businesses without clear answers about permanent establishment risks, withholding tax obligations, or how to formally claim treaty relief.

This guide is written from the UK business perspective: what the DTC actually protects you from, which triggers create unexpected US filing obligations, and the specific forms required to access reduced withholding rates.

Key Takeaways

- The treaty prevents double taxation by splitting taxing rights between the US and UK and enabling foreign tax credits — not by exempting income entirely

- Permanent establishment (PE) rules are critical: triggering a PE creates significant US corporate tax and filing obligations

- Reduced withholding rates (0% on interest/royalties, 0–15% on dividends) must be actively claimed via Form W-8BEN-E — they are never applied automatically

- The Limitation on Benefits (LOB) clause prevents treaty shopping; UK holding structures must meet substance requirements to qualify

- Filing obligations remain even when the treaty reduces tax to zero; Form 1120-F and Form 8833 are typically still required

What Is the US-UK Double Taxation Convention?

The US-UK Double Taxation Convention is a bilateral treaty that eliminates double taxation and prevents fiscal evasion on income and capital gains between the two countries. Formally titled the Convention Between the Government of the United States of America and the Government of the United Kingdom, it was signed on 24 July 2001 (amended by Protocol on 19 July 2002) and entered into force on 31 March 2003.

Taxes Covered

UK side:

- Income Tax

- Corporation Tax

- Capital Gains Tax

- Petroleum Revenue Tax

US side:

- Federal income taxes under the Internal Revenue Code

- Federal excise taxes on foreign insurer policies and private foundations

- Not covered: Social Security taxes (governed by separate Totalization Agreement signed in 1984)

How the Convention Works

The treaty doesn't create double exemption—it allocates "first taxing rights" to one jurisdiction while requiring the other to provide relief through a foreign tax credit. Both countries may tax the same income, but the combined tax burden won't exceed the higher of the two countries' rates.

Article 24 of the treaty establishes the credit mechanism:

- UK residents can credit US tax paid against UK Corporation Tax on the same profits

- Companies holding 10%+ voting power in a US subsidiary can claim underlying tax credits on dividends received

Key Treaty Provisions Every UK Business Must Know

The Saving Clause (Article 1(4))

The US retains the right to tax its own citizens and green card holders as if the treaty didn't exist. This creates complications when UK businesses employ US nationals in management roles: the US can tax those individuals on worldwide income regardless of treaty provisions.

The Saving Clause doesn't affect the UK company's own treaty claims, but it impacts how benefits apply to US persons on your payroll. Article 1(6) extends this rule to former citizens for ten years following loss of status where tax avoidance was a principal purpose.

Article 7: Business Profits

Business profits of a UK company are taxable only in the UK unless the company carries on business in the US through a permanent establishment. PE is the most critical concept in the entire treaty. Crossing that threshold triggers:

- US federal corporate tax obligations

- Form 1120-F filing requirements

- Potential state-level tax exposure

- Transfer pricing documentation

Article 13: Capital Gains and FIRPTA

Gains are generally taxable in the seller's country of residence. However, the treaty explicitly preserves the US right to tax gains from disposing of US real property interests under IRC section 897 (FIRPTA). This includes:

- Direct US real estate holdings

- Shares in US real-property-holding companies meeting the asset-ratio test

- REIT distributions attributable to gains from real property sales

UK businesses selling US real estate face US tax regardless of treaty protection. The treatment of income flows — such as interest and royalties — follows a different and more favourable logic.

Articles 11 and 12: Interest and Royalties

For qualifying UK business recipients, the treaty reduces withholding on interest and royalties to 0% — compared to the 30% default US rate. In practice, this means those payments are taxable only in the UK.

Critical exceptions where 0% doesn't apply:

- Income effectively connected with a US permanent establishment

- Excess payments under "special relationships" (transfer pricing concerns)

- Contingent interest as defined under US domestic law

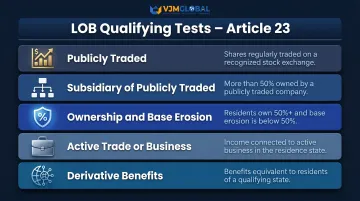

Limitation on Benefits (LOB) – Article 23

The LOB clause is the treaty's anti-abuse gatekeeper. Only genuine UK residents — not entities created purely to exploit treaty benefits — can access reduced rates. UK holding companies or conduit structures face heightened scrutiny.

Five qualifying tests:

| Test | Key Requirement |

|---|---|

| Publicly Traded | Principal share class listed on recognized UK/US exchange |

| Subsidiary of Publicly Traded | 50%+ owned by five or fewer publicly traded qualifying companies |

| Ownership & Base Erosion | 50%+ owned by qualified persons AND <50% of gross income paid to non-residents as deductible payments |

| Active Trade or Business | Engaged in substantial active business in UK relative to US activity |

| Derivative Benefits | 95%+ owned by seven or fewer EU/EEA/NAFTA residents entitled to equivalent treaty rates |

Approximately 1,100 treaties worldwide now comply with OECD BEPS Action 6 minimum standards, which the US-UK LOB predates but aligns with. Where objective tests fail, Article 23(6) gives competent authorities discretion to grant benefits — provided treaty shopping wasn't a principal purpose of the arrangement.

Permanent Establishment: The Biggest Risk for UK Companies in the US

A PE is a fixed place of business through which a UK business wholly or partly carries on US trade. Once triggered, profits attributable to that PE become taxable under US federal (and potentially state) corporate tax rules, which brings both administrative complexity and direct tax costs.

What Triggers a US Permanent Establishment

Fixed place PE:

- US office, branch, factory, or workshop

- Warehouse (unless used solely for storage/delivery)

- Construction or installation project exceeding 12 months

Dependent agent PE:

- A person (other than independent agent) habitually exercising authority to conclude contracts binding on the UK company

- US-based sales staff concluding deals on your behalf typically triggers this

Safe Harbour Activities (What Does NOT Create a PE)

Article 5(4) protects activities of a preparatory or auxiliary nature:

- Storage, display, or delivery facilities

- Maintaining stock for processing by another enterprise

- Purchasing goods or collecting information

- Conducting market research or feasibility studies

Independent agents acting in the ordinary course of business (brokers, commission agents) generally don't create PE exposure.

Where employees are concerned, the treaty provides its own protection through the 183-day rule.

The 183-Day Rule for Employees

UK-resident employees working temporarily in the US may avoid US taxation if all three conditions are met:

- Employee present in US fewer than 183 days in any twelve-month period

- Remuneration paid by employer not resident in the US

- Remuneration not borne by a US permanent establishment

UK companies regularly rely on this provision to structure short-term US assignments and project-based secondments without triggering a US tax liability.

Compliance Consequence of Triggering a PE

A UK business with a US permanent establishment must:

- Register for US federal tax purposes

- File Form 1120-F (U.S. Income Tax Return of a Foreign Corporation)

- File Form 8833 disclosing treaty position

- Manage potential state-level tax registrations and returns

- Maintain transfer pricing documentation

IRS Instructions for Form 1120-F recommend protective returns even where treaty provisions reduce tax to zero. Given that PE determinations are highly fact-specific, filing a protective return is a prudent step even when you believe no liability exists.

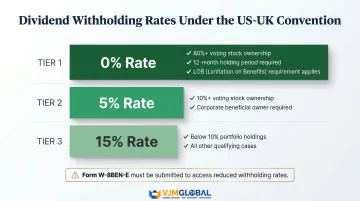

Withholding Tax Rates on US-Source Income Under the Convention

When a UK business receives US-source income, the US typically withholds tax at source. The treaty reduces these default 30% rates—but only if the UK business formally establishes eligibility by submitting Form W-8BEN-E to the US payer.

Dividend Withholding Rates – Three-Tier Structure

| Rate | Ownership Threshold | Additional Conditions |

|---|---|---|

| 0% | 80%+ voting stock | 12-month holding period ending on dividend date; must satisfy LOB requirements |

| 5% | 10%+ voting stock | Beneficial owner must be a company (not individual) |

| 15% | Below 10% (portfolio) | All other cases |

The 0% rate was introduced by the 2002 Protocol. Qualifying UK parent companies can eliminate dividend withholding entirely, provided they meet all treaty conditions — including the 12-month holding period and applicable Limitation on Benefits (LOB) tests.

Interest and Royalties: Zero-Rate Treatment

Both interest and royalties qualify for 0% withholding at source under Articles 11 and 12 for qualifying UK business recipients. This means income is taxable only in the UK.

Exceptions where full withholding may apply:

- Income connected to a US permanent establishment (PE-connected income reverts to business profits rules under Article 7)

- Contingent interest arrangements

- Excess payments under transfer pricing scrutiny ("special relationships")

Form W-8BEN-E: The Entity Certificate

Form W-8BEN-E is the IRS certificate — formally titled "Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities)" — that a UK company submits to US payers to certify its foreign status and claim a reduced treaty rate.

Key distinctions: W-8BEN applies to foreign individuals; W-8BEN-E applies to foreign entities — companies, partnerships, and trusts.

Validity: Three years from signing date, or until circumstances change. Change in circumstances requires notification within 30 days and submission of a new form.

Submitting W-8BEN instead of W-8BEN-E is one of the most common compliance errors UK businesses make — and it can result in the US payer withholding the full 30% default rate rather than the treaty rate.

How UK Businesses Can Claim Treaty Benefits

Step 1: Establish UK Tax Residency

Treaty benefits are available only to UK tax residents. For companies, this means:

- Incorporation in the UK (statutory test under Section 14, Corporation Tax Act 2009), or

- Central management and control in the UK (common law test from De Beers Consolidated Mines Ltd v Howe)

HMRC guidance confirms: "A company resides where its real business is carried on and the real business is carried on where the central management and control actually abides."

Documentary evidence to maintain:

- Board meeting minutes showing UK location of strategic decisions

- Director residency documentation

- HMRC correspondence confirming UK tax residence status

- Certificate of incorporation (if UK-incorporated)

Step 2: Submit Form W-8BEN-E to US Payers

UK businesses receiving US-source income should provide a completed W-8BEN-E to each US payer. This form certifies:

- Foreign entity status

- UK tax residency

- Treaty eligibility and claimed reduced rate

- LOB category qualification

The form must be renewed every three years or when circumstances change (ownership structure, residence status, LOB eligibility).

Step 3: File Form 8833 for Treaty-Based Return Positions

If a UK business has a US filing obligation and takes a treaty position overriding US domestic law (e.g., claiming income is not attributable to a US PE), you must attach Form 8833 to the US return to disclose the treaty position.

Penalty for non-disclosure: $1,000 per failure; $10,000 for C corporations under IRC section 6712.

Seek Professional Guidance

Each of the steps above is manageable in isolation, but they interact in ways that can create compliance gaps. Getting PE classification wrong, for instance, can trigger W-8BEN-E errors and Form 8833 obligations simultaneously.

Professional guidance is particularly valuable when:

- Your UK entity has personnel or contracts creating potential US PE exposure

- Ownership changes affect your LOB qualification

- You're restructuring operations across the US and UK

- Transfer pricing documentation needs to align with treaty positions

VJM Global has supported over 250 UK businesses with international tax compliance, helping them structure cross-border operations and avoid unexpected US tax obligations. Engaging specialist advice before making structuring decisions is significantly cheaper than correcting compliance failures after the fact.

Common Misconceptions UK Businesses Have About the Convention

Misconception 1: "The Treaty Means We Can't Be Taxed in Both Countries"

The treaty allocates "first taxing rights" rather than "sole taxing rights" in most cases. It doesn't guarantee that only one country taxes the income. Instead, it ensures the other country provides relief, typically through a foreign tax credit.

That said, timing differences can still create temporary double taxation. The US may withhold tax when a dividend is paid, while UK credit relief isn't available until the company files its Corporation Tax return months later.

Misconception 2: "Treaty Benefits Apply Automatically"

Treaty benefits are never automatic. UK businesses must actively claim them through:

- Correct forms (W-8BEN-E, not W-8BEN)

- Meeting Limitation on Benefits requirements

- Disclosing treaty positions on Form 8833 where required

Failure to submit proper documentation means the default 30% US withholding rates apply—even when the treaty would have reduced the rate to 0%.

Misconception 3: "Using a UK Holding Company Always Provides Full Treaty Protection"

The LOB clause (Article 23) is specifically designed to prevent treaty shopping. A UK holding company that exists primarily to channel income to a non-UK parent may be denied treaty benefits. OECD BEPS Action 6 frameworks have strengthened this scrutiny — approximately 1,100 treaties now comply with minimum standards that require substance tests, not just legal form. UK holding structures must demonstrate:

- Real business operations in the UK

- Economic substance beyond nominee directors and mailbox addresses

- Active decision-making and management in the UK

- Business purpose beyond obtaining treaty benefits

Frequently Asked Questions

Does the UK have a double taxation agreement with the USA?

Yes. The US-UK Double Taxation Convention was signed in 2001 (amended by Protocol in 2002) and is a bilateral income tax treaty covering individuals and businesses in both countries. It addresses income taxes, capital gains, and provides mechanisms to eliminate double taxation through foreign tax credits and reduced withholding rates.

Do I have to pay taxes in both the US and the UK?

Both countries may tax the same income under domestic law, but the Convention allocates "first taxing rights" and requires the other country to provide a foreign tax credit. Both obligations must be actively managed through proper filing and credit claims — the combined burden rarely exceeds the higher of the two rates, but relief isn't automatic.

How can I avoid double taxation between the UK and the US?

The main mechanisms are claiming foreign tax credits (offsetting UK tax paid against US liability or vice versa), submitting Form W-8BEN-E to claim reduced withholding rates on US-source income, and using treaty provisions to limit where income is taxable. Treaty benefits require active claims and correct documentation, so proactive planning is essential.

What is the tie-breaker for the US and UK double tax treaty?

For individuals, the treaty applies sequential criteria — permanent home, centre of vital interests, habitual abode, nationality — then competent authority agreement if unresolved. For companies, Article 4(5) provides no objective criteria; dual residence is settled by competent authority determination only. Where authorities cannot agree, the entity loses most treaty benefits, retaining only foreign tax credit relief, non-discrimination protection, and mutual agreement procedure access.

Are you taxed on foreign income in the UK?

UK tax-resident companies are taxable on worldwide income — including US-sourced income — under the Corporation Tax Act 2009. TIOPA 2010 provides foreign tax credit relief for US taxes already paid, and the treaty ensures the credit applies so income isn't taxed above the UK Corporation Tax rate.

What is the double taxation convention in the UK?

A double taxation convention (DTC) is a bilateral tax treaty the UK has signed with another country (including the US) that determines which country has taxing rights over specific income and provides relief mechanisms so the same income is not taxed twice in full by both jurisdictions. The UK has DTCs with over 130 countries, using foreign tax credits, exemptions, or reduced withholding rates to eliminate double taxation.