Introduction

Singapore employers answer to three statutory agencies at once — each running its own enforcement regime:

- CPF Board: mandates accurate contribution calculations and timely monthly payments

- Ministry of Manpower (MOM): prosecutes Employment Act violations including incorrect wage computation

- IRAS: imposes tax undercharging penalties that can reach 200% of the amount at issue

A single payroll miscalculation can trigger all three simultaneously — backdated CPF demands, MOM prosecution, and IRAS penalties in one compliance event.

The risk is especially acute for foreign and multinational companies unfamiliar with Singapore's evolving regulatory requirements. Since September 2023, the CPF Ordinary Wage ceiling has risen in phases — $6,800 (2024), $7,400 (2025), and $8,000 (2026) — requiring annual payroll system recalibrations.

On top of that, the 1 March AIS submission deadline is non-negotiable. IRAS actively cross-matches CPF contribution data against reported employment income, so discrepancies get flagged quickly.

With that compliance picture in mind, this checklist walks through each audit area in sequence — CPF contribution verification, statutory levy compliance (SDL/FWL), and IRAS annual reporting requirements including IR8A, AIS, and IR21 tax clearance obligations.

Key Takeaways

- A Singapore payroll audit covers five areas: employee classification, salary timing, CPF contributions, statutory levies (SDL/FWL/SHG), and IRAS income reporting

- Employers must retain payroll records for five years under the Income Tax Act and submit employment income data electronically by 1 March via AIS

- Common failures: wrong CPF rates at age thresholds (55, 60, 65, 70), under-reported benefits-in-kind, and missed IR21 filings for departing foreign employees

- Running quarterly internal reconciliations cuts penalty exposure across CPF Board, MOM, and IRAS before they compound

What You Need Before Starting a Singapore Payroll Audit

Effective auditing begins with document consolidation. Gather the following core records before commencing review:

Essential Documentation:

- Employment contracts and offer letters showing approved pay rates

- Payroll registers for the review period

- Itemised payslip records for all payment cycles

- CPF submission acknowledgements from the CPF Board

- SDL, FWL, and SHG payment receipts

- IRAS forms: IR8A, Appendix 8A (benefits-in-kind), Appendix 8B (ESOP/ESOW gains), IR21 (tax clearance for departing foreigners)

- Work pass records for all foreign employees (EP, S Pass, Work Permit)

Audit Role Separation:

While not statutorily mandated, the maker-checker principle—assigning the audit to someone independent of payroll processing—creates essential distance for detecting internal discrepancies. Given that CPF late payment triggers automatic 1.5% monthly interest and IRAS penalties can reach 200% of tax undercharged, this control significantly reduces exposure to both errors and penalties.

Foreign companies unfamiliar with Singapore's compliance calendar often benefit from engaging a specialist advisor to lead or support the review. VJM Global works with multinational companies on cross-border payroll compliance, including audit preparation for Singapore operations.

System Readiness Pre-Audit:

Verify that payroll software reflects current statutory parameters. The CPF Ordinary Wage ceiling increased to S$7,400 in 2025 and will rise to S$8,000 from 1 January 2026, while the Annual Salary Ceiling remains at S$102,000. All variable pay data—overtime, bonuses, allowances—for the audit period must be finalised and approved before review begins.

Singapore Payroll Audit Checklist: Five Key Areas to Review

Singapore payroll compliance spans five distinct areas: worker classification, salary and payslip obligations, CPF contributions, statutory levies, and IRAS income reporting. Each carries its own deadlines, thresholds, and penalties. Work through them in sequence to avoid gaps.

Employee Data and Worker Classification

Verify employment classification accuracy:

- Confirm each worker is correctly designated: full-time, part-time, temporary, contractor, or director

- Check that CPF obligations, leave entitlements, and tax treatment align with classification

- Flag individuals potentially misclassified as contractors to avoid CPF underpayment and Employment Act violations

Contractor vs. Employee Distinction:

CPF contributions are mandatory for employees engaged under a contract of service. Independent contractors (contract for service) are exempt. The distinction hinges on control over how work is performed, a principle applied by both MOM and the CPF Board.

Director CPF Obligations:

Directors' fees voted at General Meetings carry no CPF obligation. However, executive directors engaged under a contract of service receive wages subject to CPF. This dual status creates audit risk when payroll records fail to separate directors' fees from employment wages.

Personal Particulars Verification:

- NRIC/FIN accuracy

- Nationality and work pass type (EP/SP/WP)

- Employment start and end dates

- PR status and year of membership (affects graduated CPF rates)

Errors in these core identifiers cascade into CPF calculation errors, incorrect AIS submissions, and tax clearance failures for departing foreign employees.

Salary Payments, Payslips, and Overtime

With classification confirmed, the next audit area is payment timing and documentation — both governed by the Employment Act with criminal penalties for non-compliance.

Payment Timing Compliance (Employment Act):

- Basic salary: paid within 7 days after the end of the salary period

- Overtime pay: paid within 14 days after the salary period

- Termination by employer: salary due on the last day of work or within 3 working days

- Resignation with notice: salary due on the last day of work

Violations carry criminal penalties. First-time offenders face fines of $3,000 to $15,000 and/or up to 6 months' imprisonment.

Itemised Payslip Requirements:

Since 1 April 2016, all employers must issue itemised payslips containing 13 mandatory elements:

- Full name of employer and employee

- Date of payment

- Basic salary (with rate and hours/days/pieces for non-monthly workers)

- Salary period start and end dates

- Allowances paid (fixed and ad-hoc)

- Additional payments (bonuses, rest day/public holiday pay)

- Total salary earned

- Overtime hours worked

- Overtime payment period

- Overtime pay

- Itemised deductions (including employee CPF contribution)

- Net salary paid

Payslips must be issued with payment or within 3 working days.

Pay Rate Reconciliation:

Cross-reference approved rates in offer letters and increment letters against actual payroll outputs. Verify that every salary payment, bonus, commission, and shift differential was disbursed at the correct rate with no unauthorised variances.

CPF Contributions

Accurate salary records feed directly into CPF — where age-band thresholds and annual ceiling updates create the most frequent systematic errors.

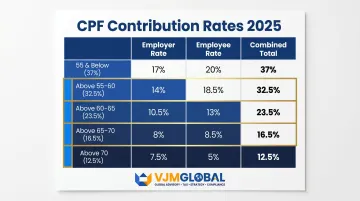

Age-Band Rate Verification:

CPF contribution rates change at four critical age thresholds: 55, 60, 65, and 70. For 2025, rates for Singapore Citizens and SPRs (3rd year onwards) earning $750+ per month are:

| Age Group | Employer Rate | Employee Rate | Total |

|---|---|---|---|

| 55 and below | 17% | 20% | 37% |

| Above 55 to 60 | 15.5% | 17% | 32.5% |

| Above 60 to 65 | 12% | 11.5% | 23.5% |

| Above 65 to 70 | 9% | 7.5% | 16.5% |

| Above 70 | 7.5% | 5% | 12.5% |

From 1 January 2026, rates for the 55–60 and 60–65 brackets increase by 1.5 percentage points to 34% and 25% respectively. New rates apply from the first day of the month after the employee reaches the age threshold.

Ordinary Wage Ceiling Updates:

The CPF Ordinary Wage ceiling rose from $6,000 (pre-September 2023) to:

- $6,800 (2024)

- $7,400 (2025)

- $8,000 (2026)

Failure to update this parameter creates systematic under-contribution for all employees earning above the old ceiling. It is one of the most common findings in Singapore payroll audits.

Additional Wage (AW) Ceiling Calculation:

The AW ceiling formula is: $102,000 minus Total Ordinary Wages subject to CPF for the calendar year. This calculation is applied per employer, per year. As the OW ceiling increases, the "headroom" for bonuses subject to CPF decreases, though the $102,000 annual cap remains unchanged.

Foreign Employee Exemption:

Foreigners holding EP, S Pass, or Work Permit — non-Citizens and non-PRs — are exempt from CPF contributions. Confirm that the payroll system excludes these employees from CPF calculation entirely.

Statutory Levies: SDL, FWL, and SHG Contributions

Beyond CPF, three separate levy obligations apply depending on workforce composition. Each has its own rate structure, remittance deadline, and common oversight risk.

Skills Development Levy (SDL):

- Rate: 0.25% of total monthly wages

- Minimum: $2 per employee (wages $800 or less)

- Maximum: $11.25 per employee (wages $4,500 or more)

- Applies to: All local and foreign employees rendering services in Singapore

- Remittance: Via CPF EZPay or directly to SkillsFuture Singapore (SSG) for all-foreign workforces

Unlike CPF, SDL applies to foreign workers. Multinational employers managing EP/SP/WP holders frequently miss this obligation.

Foreign Worker Levy (FWL):

Since 1 September 2025, the S Pass levy rate harmonised to $650 across all sectors and tiers. Work Permit levies remain tiered by sector, skill level, and Dependency Ratio Ceiling (DRC):

| Sector | DRC | Tier Structure |

|---|---|---|

| Services | 35% | 3 tiers (up to 10%, 10–25%, 25–35%) |

| Manufacturing | 60% | 3 tiers (up to 25%, 25–50%, 50–60%) |

| Construction | 83.3% | No tiers; rates by skill/source |

FWL payment deadline: by the 17th of the following month (or next working day if the 17th falls on a weekend/public holiday).

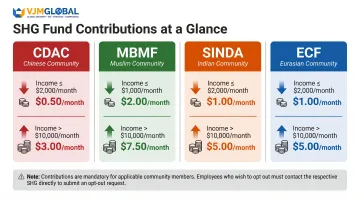

Self-Help Group (SHG) Contributions:

Four funds (CDAC, MBMF, SINDA, ECF) require employer deductions based on employee ethnicity indicated on NRIC:

| Fund | Community | Lowest Band | Highest Band |

|---|---|---|---|

| CDAC | Chinese | $0.50 ($2,000 or less) | $3.00 (above $7,500) |

| MBMF | Muslim | $3.00 ($1,000 or less) | $26.00 (above $10,000) |

| SINDA | Indian | $1.00 ($1,000 or less) | $30.00 (above $15,000) |

| ECF | Eurasian | $2.00 ($1,000 or less) | $20.00 (above $10,000) |

Incorrect ethnic classification leads to systematic deduction errors across the workforce. Employees who opt out must contact the respective SHG directly.

IRAS Annual Income Reporting: IR8A, AIS, and IR21

The final audit area covers annual income reporting to IRAS — where missed deadlines and incomplete forms trigger assessments and penalties that are difficult to reverse after the fact.

Auto-Inclusion Scheme (AIS) Requirements:

Employers with 5 or more employees must register for AIS and submit employment income electronically to IRAS. Deadline: 1 March of the year following the income year. For Year of Assessment 2026, employers must submit 2025 employment income data by 1 March 2026.

Form IR8A Coverage:

Required under Section 68(2) of the Income Tax Act for:

- Full-time and part-time resident employees

- Non-resident employees who rendered service in Singapore

- Company directors (including non-resident directors)

- Board members receiving fees

- Pensioners

- Employees who left but received income in the reporting year

Appendix 8A (Benefits-in-Kind):

Must be completed for employees provided with:

- Accommodation/housing (taxable at Annual Value less rent paid by employee)

- Car and car-related benefits (taxable based on private usage value)

- Utilities and household expenses

- Club memberships

- Holiday passages

- Gifts and awards exceeding $200 in value

Housing allowances paid in cash carry the same tax treatment as employer-provided accommodation: both are fully taxable. This distinction is a frequent misclassification in IRAS audits.

Appendix 8B (ESOP/ESOW):

Required for employees deriving gains from stock option plans or share ownership schemes. Must include number of shares, exercise price, open market value at exercise/vesting, and calculated taxable gain.

IR21 Tax Clearance:

Employers must file Form IR21 at least one month before a non-Singapore Citizen employee (including PRs leaving permanently) ceases employment or leaves Singapore for more than 3 months. From the date the employer becomes aware of the departure, all monies due to the employee must be withheld until a Clearance Directive is received from IRAS.

Failure to file or withhold carries a fine of up to $1,000. Beyond the fine, the employer may be held liable for the employee's outstanding tax directly.

Deemed Exercise Rule for ESOP/ESOW:

Foreign employees leaving Singapore with unexercised stock options or unvested share awards are deemed to have exercised them at the point of tax clearance, triggering immediate tax liability. This must be reported on IR21 and Appendix 8B, with sufficient funds withheld to cover the resulting tax.

How to Interpret Payroll Audit Findings

Clean Audit Results

A compliant payroll presents:

- Payroll outputs matching employment contracts and approved variance reports

- CPF submissions reconciling with payroll registers

- All statutory forms filed on time

- No unexplained pay adjustments or rate discrepancies

This baseline confirms audit readiness for MOM, CPF Board, or IRAS review.

Minor Issues

Examples include a payslip issued a few days late for a single month, or a minor OW/AW classification discrepancy with no material underpayment. These can typically be corrected internally. Document the correction, update payroll system parameters, and retain evidence of remediation.

Significant Findings Requiring Escalation

More serious findings require escalation beyond internal correction. These include:

- Systemic CPF underpayments across multiple employees

- Unreported taxable benefits-in-kind (housing allowances, car benefits)

- Missing IR21 filings for departed foreign employees

- CPF age-band rate failures affecting multiple pay cycles

IRAS and the CPF Board actively cross-reference data. The AIS system enables IRAS to pre-fill over 2 million individual tax returns using employer-submitted data. This creates inherent cross-checks between AIS submissions, CPF contributions, and individual filings — mismatches surface as anomalies in automated profiling.

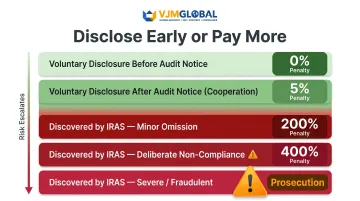

Voluntary Disclosure Programme (VDP) Benefits

IRAS offers meaningful penalty relief for proactive error correction:

| Disclosure Timing | Penalty Rate |

|---|---|

| Within 1-year grace period | 0% |

| After grace period (voluntary) | 5% per year of tax undercharged |

| IRAS discovers via audit | Up to 200% of tax undercharged |

| Wilful evasion (voluntary) | 200% (compounded in lieu of prosecution) |

| Wilful evasion (IRAS discovers) | Up to 400% + prosecution (7 years jail, $50,000 fine) |

Voluntary disclosure before an external audit substantially reduces financial exposure.

Government Audit Consequences

Once IRAS or another agency initiates a review, the penalty options narrow considerably. If issues surface during a government-initiated audit:

- CPF Board: Backdated contribution demands plus 1.5% monthly interest (minimum $5), potential court fines of $1,000–$5,000 (first conviction) and up to 6 months' imprisonment

- MOM: Salary payment violations carry fines of $3,000–$15,000 (first offence) and up to 6 months' jail

- IRAS: Inaccurate income reporting attracts penalties up to 200% of tax undercharged

A complete evidence pack — CPF acknowledgements, levy payment receipts, AIS submission confirmations — gives your team the documentation needed to respond quickly, challenge inaccuracies, and demonstrate good-faith compliance from the outset.

Common Payroll Errors Found in Singapore Audits

Benefits-in-Kind Misclassification

The most frequent IRAS finding involves benefits-in-kind that employers fail to value or report correctly. Three categories account for most violations:

- Housing: Both cash housing allowances and employer-provided accommodation are fully taxable at the Annual Value of the property, less any rent paid by the employee

- Car benefits: Taxable based on private usage value, with detailed valuation formulas published by IRAS

- Gifts and awards: Any amount exceeding S$200 per occasion must be reported in Appendix 8A

CPF Age-Band and Wage-Ceiling Errors

Failing to update contribution rates when employees cross age thresholds (55, 60, 65, 70) creates systematic over- or under-contribution requiring retrospective adjustment. Not applying the updated Ordinary Wage (OW) ceiling after government-announced changes compounds the error across multiple pay cycles before anyone catches it.

Worker Misclassification

Treating employees as independent contractors to avoid CPF contributions is a recognised compliance failure with serious consequences. The CPF Board can retrospectively assess contributions for misclassified workers, plus 1.5% monthly interest — and in serious cases, prosecution.

Deemed Exercise Rule Oversight

Companies administering share plans from overseas parent entities commonly overlook the deemed exercise rule for foreign employees. Any ESOP or ESOW plan granted on or after 1 January 2003 triggers a deemed gain calculation at tax clearance.

The gain — calculated as open market value minus exercise price — must be reported on IR21 and Appendix 8B, with sufficient funds withheld. This becomes a particularly sharp compliance trap when the employment relationship is ending and timelines are tight.

Best Practices for Ongoing Payroll Compliance

Establish Formal Audit Frequency

At minimum, conduct an annual comprehensive review. Ideally, implement:

- Monthly reconciliation of CPF submissions against payroll registers

- Mid-year compliance check when statutory rate changes take effect

- Full annual audit before the 1 March IRAS reporting deadline

Companies with cross-border workforces — mixing locals, PRs, and EP/S Pass holders — face layered compliance exposure across CPF, FWL, and IR21 obligations. Engaging a specialist payroll advisory firm helps ensure each employee category is handled correctly. VJM Global works with foreign and multinational companies operating across Singapore, India, and other jurisdictions to align payroll processes with local statutory requirements.

Maintain a Clean Evidence Pack

At the end of each payroll cycle, consolidate:

- Payroll register summaries

- CPF submission receipts

- SDL records

- FWL payment confirmations

- Bank disbursement files

The Income Tax Act requires businesses to retain records for five years from the relevant Year of Assessment. Organising these by cycle significantly reduces audit response time.

Create a Year-End Compliance Calendar

Key milestone dates:

- January 1: New CPF rates and OW ceiling take effect (if changed)

- January–February: Reconcile payroll registers, draft IR8A, value benefits-in-kind, conduct AIS pre-submission review

- 1 March: AIS submission deadline

- Monthly by 14th: CPF contributions due (grace period)

- Monthly by 17th: FWL payment due

- Within 7 days of salary period end: Salary disbursement

- At least 1 month before departure: File IR21 for foreign employees

Monitor Regulatory Updates

The CPF Board publishes rate changes on its Infohub news page under "CPF-related announcements." The 2026 rate increases were announced on 7 April 2025, providing approximately 9 months' lead time. Subscribe to CPF Board updates and monitor MOM's website for Employment Act amendments.

Frequently Asked Questions

Frequently Asked Questions

What should be included in a payroll audit?

A Singapore payroll audit covers five key areas:

- Employee data verification and classification accuracy

- Salary payment timing and payslip compliance

- CPF contribution correctness across age bands and wage ceilings

- Statutory levy compliance (SDL, FWL, SHG)

- IRAS annual reporting accuracy (IR8A, AIS, IR21)

What is the payroll legislation in Singapore?

Three primary laws govern Singapore payroll:

- Employment Act — salary disbursement timing, payslip requirements, and overtime rules

- CPF Act — contribution rates and employer obligations

- Income Tax Act — employer reporting to IRAS, covering IR8A, AIS submissions, and IR21 tax clearance

How far back does a payroll audit go?

Singapore law requires employers to retain payroll records for at least five years from the relevant Year of Assessment under the Income Tax Act. IRAS and the CPF Board can investigate payroll compliance within this five-year window.

What triggers a payroll audit in Singapore?

IRAS profiles employers for targeted intervention through automated data matching and cross-agency data sharing. Common triggers include:

- Mismatches between AIS-reported employment income and CPF contribution records

- Late or non-filing of IR8A

- Unusually high expense claims

- Income-versus-contribution inconsistencies flagged across government agencies

What are common payroll mistakes found in Singapore audits?

The most frequent errors include incorrect CPF age-band rate application at thresholds (55, 60, 65, 70), under-reported taxable benefits-in-kind (especially housing allowances and car benefits), missed IR21 filings for departing foreign employees, and failure to update the CPF Ordinary Wage ceiling in payroll systems after government-announced increases.

How often should Singapore employers conduct internal payroll audits?

A three-tier audit cadence works best for most employers:

- Monthly — reconcile payroll registers against CPF submissions

- Mid-year — compliance check when statutory rate changes take effect (typically 1 January)

- Annual — full audit before the 1 March IRAS AIS submission deadline

Companies with multi-jurisdiction workforces should add quarterly reviews.