Introduction

Under Singapore's Companies Act 1967, all private limited companies incorporated in Singapore must appoint an ACRA-registered auditor within three months of incorporation and undergo an annual statutory audit — unless they qualify for specific exemptions. Yet many foreign companies establishing operations here overlook the exemption criteria or assume that qualifying for an exemption eliminates all financial compliance obligations.

While small company, small group, and dormant company exemptions provide relief from statutory audit requirements, exempt companies still must prepare unaudited financial statements, maintain accurate accounting records for five years, and file annual returns with ACRA within strict timelines.

Misunderstanding these requirements can result in penalties up to S$5,000, ACRA enforcement action, and reputational damage.

This guide covers who must comply with Singapore's audit requirements, how exemptions work, what obligations remain for exempt companies, annual filing deadlines, and the consequences of non-compliance.

TLDR: Key Takeaways

- Private limited companies must appoint an ACRA-registered auditor within 3 months of incorporation unless exempt

- Exemptions require meeting 2 of 3 thresholds — revenue ≤S$10M, assets ≤S$10M, employees ≤50 — for two consecutive years

- Exempt companies still prepare unaudited financial statements, maintain 5-year accounting records, and file annual returns

- Audit fees are negotiated directly with auditors — no statutory minimum or maximum applies

- Late filings incur penalties up to S$600; serious Companies Act breaches carry fines up to S$5,000 plus potential court action

What Is a Statutory Audit in Singapore and Why Is It Required?

A statutory audit is an annual, legally mandated examination of a company's financial statements by an independent, ACRA-registered public accountant. Required under Part 6 of the Companies Act 1967, the audit ensures financial statements give a true and fair view of the company's financial position and comply with Singapore Financial Reporting Standards (SFRS).

Why it matters beyond legal compliance:

- Protects shareholder interests through independent verification of financial accuracy

- Increases stakeholder confidence among investors, lenders, and business partners

- Supports sound investment decisions with reliable financial data

- Upholds Singapore's business reputation as a transparent, well-regulated corporate hub

For foreign companies, this regulatory structure signals predictability — audited financials carry credibility with banks, partners, and regulators across borders. Audit quality itself is governed by the Public Accountants Oversight Committee (PAOC), established under the Accountants Act 2004. Notably, most PAOC members are not practicing public accountants, a deliberate design choice that reinforces independent oversight.

Singapore Audit Requirements: Who Must Comply?

Core rule: All private limited companies in Singapore must conduct a statutory audit annually unless they qualify for one of three exemptions: small company, small group, or dormant company.

Auditor Appointment Requirements

Under Section 205 of the Companies Act:

- Directors must appoint at least one auditor within 3 months of incorporation

- The auditor must be an ACRA-registered public accountant, accounting firm, accounting corporation, or accounting LLP

- If directors fail to appoint an auditor, ACRA may appoint one on their behalf upon written application from any member

Auditors must be registered under the Accountants Act 2004. A person is disqualified from serving if they:

- Are an officer or employee of the company

- Are a partner, employer, or employee of an officer of the company

- Are indebted to the company for more than S$2,500

Auditor Role in the Audit Process

Auditors express an independent opinion on whether financial statements comply with SFRS and present a true and fair view. They must have full access to company records, including:

- Accounting books and ledgers

- Supporting documentation for transactions

- Bank statements and reconciliations

- Contractual agreements affecting financial position

Audit work follows Singapore Standards on Auditing (SSAs), which govern risk assessment, audit planning, evidence gathering, materiality determinations, and reporting.

Auditor Remuneration

There is no statutory minimum or maximum audit fee. Fees are negotiated between the company and the auditor, varying by size, complexity, and industry. Key rules under Section 205(16) and Section 206 include:

- Fees are fixed by the company at a general meeting, or by directors if authorised

- Companies must disclose auditor remuneration at a general meeting if shareholders request it

Auditor Resignation or Removal

Removal (Sections 205(4)-(6)):

- Requires ordinary resolution at a general meeting with "special notice" (at least 28 days)

- Company must immediately send a copy to the auditor and the Registrar

- Auditor may make written representations within 7 days and has the right to be heard orally at the meeting

Resignation:

- Non-public interest companies: Auditor may resign by giving written notice, effective on the date specified

- Public interest companies: Auditor cannot resign without the Registrar's written consent and must state reasons

Any change in auditors must be lodged with ACRA within 14 days. Non-compliance carries a fine not exceeding S$5,000.

Audit Exemptions in Singapore: Small Company, Small Group, and Dormant Companies

Small Company Exemption

A private company qualifies for audit exemption if it meets at least 2 of 3 criteria for the immediate past two consecutive financial years:

- Total annual revenue ≤ S$10 million

- Total assets ≤ S$10 million (at end of financial year)

- Number of employees ≤ 50 (at end of financial year)

For newly incorporated companies (less than 2 years old), the criteria apply to the current financial year only.

The company must be a private company throughout the financial year to qualify.

Small Group Rule for Subsidiaries

Small company status alone is not enough if the business is part of a larger group. When a company has a parent or acts as one, both conditions must be satisfied:

- The individual company qualifies as a "small company"; AND

- The entire group meets the same 2-of-3 quantitative thresholds on a consolidated basis for the immediate past two consecutive financial years

Two points catch many companies off guard when applying the group test:

- All entities in the group — including foreign subsidiaries — count toward consolidated revenue, assets, and headcount

- Group membership is determined by Accounting Standards, not by whether consolidated financial statements are actually filed

Dormant Company Exemption

A dormant company with no accounting transactions and total assets not exceeding S$500,000 is exempt from audit requirements.

Under Singapore law, a company is dormant during any period in which no accounting transaction occurs. The following actions do not break dormancy:

- Appointment of a company secretary or auditor

- Maintenance of a registered office

- Keeping of statutory registers

- Payment of fees to ACRA

- Taking of shares by a subscriber to the constitution

Unlike the small company exemption, the dormant company exemption is not limited to private companies.

Maintaining and Losing Exempt Status

A small company remains exempt until it is disqualified. Disqualification triggers:

- The company ceases to be a private company at any time during the financial year

- The company fails the 2-of-3 quantitative test for two consecutive financial years

- For group companies: the group fails the consolidated test for two consecutive years

Shareholder override: Shareholders holding at least 5% of total issued shares (excluding treasury shares) can require the company to have its accounts audited, even if it otherwise qualifies for exemption. Notice must be given at least one month before the end of the financial year.

Common Misconception: Exemption ≠ Zero Compliance

Audit exemption does not mean full compliance exemption. Exempt companies still carry ongoing obligations — financial record-keeping, annual filings, and director responsibilities remain in full effect. These are covered in the next section.

What Exempt Companies Still Need to Do

Prepare Unaudited Financial Statements (UFS)

All Singapore-incorporated companies must prepare financial statements in accordance with Accounting Standards (SFRS or SFRS for Small Entities), even if exempt from audit. Audit exemption only means the statements won't be independently audited. Preparation remains mandatory.

UFS components typically include:

- Statement of comprehensive income

- Director's statement

- Balance sheet

- Statement of changes in equity

- Cash flow statement

- Notes to the financial statements

These components support tax submissions, AGM obligations, and shareholder accountability — each covered below.

Maintain Proper Accounting Records

Under Section 199(2) of the Companies Act, companies must retain accounting records for at least 5 years from the end of the financial year in which those transactions occurred.

ACRA regularly conducts compliance checks, and external auditors may still be appointed if a company faces legal issues or shareholder disputes. Good record-keeping means companies can prove compliance during checks or disputes.

These record-keeping obligations connect directly to annual reporting requirements — including AGMs and statutory filings.

AGM and Annual Return Obligations

AGM Requirements for Private Companies:

| Requirement | Details |

|---|---|

| AGM deadline | Non-listed companies: within 6 months after FYE |

| Exemption from AGM | Private companies are exempt if they send financial statements to all entitled persons within 5 months after FYE |

| Dispensation | Private companies can dispense with AGMs entirely if all members with voting rights pass a resolution to that effect |

Even with dispensation, companies must still file annual returns and provide financial statements to members. Members can request an AGM by notifying the company no later than 14 days before the end of the 6th month after FYE.

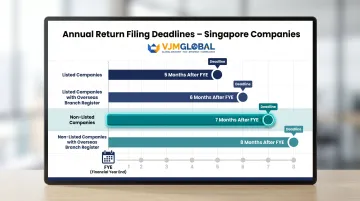

Annual Return Filing Timelines:

| Company Type | Filing Deadline |

|---|---|

| Listed companies | Within 5 months after FYE |

| Listed companies with overseas branch register | Within 6 months after FYE |

| Non-listed companies | Within 7 months after FYE |

| Non-listed companies with overseas branch register | Within 8 months after FYE |

These filing deadlines apply regardless of audit status.

Annual Filing Requirements and Reporting Obligations

XBRL Filing Requirements for Financial Statements

Most Singapore-incorporated companies must file financial statements in XBRL format with ACRA:

Filing categories:

- Full XBRL: Required for most Singapore-incorporated companies limited by shares, including public companies and insolvent private companies (filed with PDF copy of directors-authorised financial statements)

- Simplified XBRL: Smaller private companies may file a reduced set of approximately 120 data elements instead of the full taxonomy

- Solvent Exempt Private Companies (EPCs): Exempt from filing financial statements; file Annual Return with a Declaration of Solvency only

- Dormant Relevant Companies: Exempt from filing financial statements if dormant since incorporation or end of previous FY and total assets do not exceed S$500,000

Estimated Chargeable Income (ECI) Filing

Beyond XBRL, companies must also submit Estimated Chargeable Income (ECI) to IRAS within 3 months of their financial year end. ECI captures estimated taxable income for the Year of Assessment, allowing IRAS to assess tax liability ahead of the final return.

ECI Filing Waiver:

A company is not required to file ECI if both conditions are met:

- Annual revenue is S$5 million or below for the financial year; AND

- ECI is nil for the Year of Assessment (before deducting exempt amounts under partial tax exemption or startup tax exemption)

If ECI is nil but revenue exceeds S$5 million, the company must still file. Companies that qualify for the waiver do not need to seek confirmation from or inform IRAS.

Consequences of late filing: IRAS may issue a Notice of Assessment based on an estimation of income; the company loses eligibility for interest-free instalment payments.

Financial Year End (FYE) Choice and Tax Planning

FYE selection isn't just an administrative choice — it directly shapes your compliance calendar and tax position. Companies can select any FYE upon incorporation, with December 31 or calendar quarter-ends being common choices for reporting alignment.

FYE choice affects:

- Compliance timelines: Annual return filing deadlines count from FYE

- Tax planning windows: A longer first basis period — for example, an FYE that runs up to 18 months — maximises income covered by the Startup Tax Exemption Scheme (SUTE)

- Eligibility for incentive schemes: SUTE and other schemes apply to the first 3 consecutive Years of Assessment; strategic FYE selection optimises benefit periods

Singapore's Audit Standards, Regulatory Framework, and Non-Compliance Penalties

Singapore Standards on Auditing (SSAs)

Audits in Singapore must be conducted in accordance with the Singapore Standards on Auditing (SSAs), issued by the Institute of Singapore Chartered Accountants (ISCA) and prescribed by the Accounting Standards Council (ASC).

Key characteristics:

- Currently 37 SSAs in force, organised in numbered groups mirroring the ISA numbering system

- The SSAs are aligned with and substantially converge to the International Standards on Auditing (ISAs) issued by the International Auditing and Assurance Standards Board (IAASB)

- Cover risk assessment, audit planning, evidence gathering, materiality, and reporting requirements

Accounting Standards and Regulatory Bodies

Two-tier SFRS framework:

- Full SFRS (International): Based on IFRS Standards, applicable to larger entities and entities with public accountability

- SFRS for Small Entities: Based on the IFRS for SMEs Standard, available for qualifying smaller private companies (revenue ≤S$10 million, assets ≤S$10 million, employees ≤50)

Regulatory bodies:

- ACRA (Accounting and Corporate Regulatory Authority): Registers public accountants, monitors audit quality through the Practice Monitoring Programme (PMP), and publishes audit quality findings

- PAOC (Public Accountants Oversight Committee): Oversees audit regulation under the Accountants Act; most members are not public accountants, ensuring independence

- ISCA (Institute of Singapore Chartered Accountants): Issues and maintains SSAs and related guidance; provides continuing professional education

- ASC (Accounting Standards Council): Sets accounting standards for Singapore

Companies with operations in both Singapore and India face compliance obligations across two distinct regulatory frameworks. VJM Global, a member of EAI International, works with Singapore-incorporated companies that have Indian parent entities or subsidiaries to manage these overlapping requirements.

Penalties for Non-Compliance

Late annual return filings:

- Within 3 months of due date: S$300 late lodgement penalty

- More than 3 months after due date: S$600 late lodgement penalty

Companies Act breaches:

- Breach of Section 205 (e.g., failure to appoint auditor, non-compliance with removal procedures): Fine up to S$5,000

- Persistent breaches (3+ offences in 5 years): Director disqualification for 5 years; potential striking off of company

Tax filing non-compliance:

- Failure to file income tax return (Income Tax Act Section 94A): Fine up to S$5,000 + penalty equal to double (2x) the tax owed for the relevant Year of Assessment; continuing offence: S$100/day after conviction

- Errors in tax returns (Section 95): Penalty up to double the tax undercharged; fine up to S$5,000

ACRA's enforcement powers extend to striking off companies and disqualifying directors — penalties that can permanently affect a business's ability to operate in Singapore.

Frequently Asked Questions

What is the audit requirement in Singapore?

All private limited companies must conduct an annual statutory audit under the Companies Act and appoint an ACRA-registered auditor within 3 months of incorporation. Exemptions apply for companies that qualify as a small company, small group, or dormant company based on specific financial thresholds.

How much is the audit fee in Singapore?

There is no statutory minimum or maximum audit fee in Singapore. Fees are negotiated between the company and the auditor and typically vary based on company size, complexity, and industry. Companies must disclose auditor remuneration at a general meeting if shareholders request it.

How many Singapore Standards on Auditing are there currently?

37 SSAs are currently in force, issued by ISCA and prescribed by the Accounting Standards Council. They align with International Standards on Auditing (ISA), covering audit planning, risk assessment, evidence gathering, and reporting.

What are the 7 principles of auditing?

The seven generally recognised principles of auditing (established in ISO 19011:2018) are: integrity, fair presentation, due professional care, confidentiality, independence, evidence-based approach, and risk-based approach. Singapore's SSAs are built on these same principles.

What are the penalties for not complying with audit requirements in Singapore?

Penalties vary by violation type:

- Late annual returns: fines up to S$600

- Companies Act breaches: fines up to S$5,000 plus potential court summons

- Failure to file IRAS tax returns: fines up to S$5,000 plus twice the tax owed

Do dormant companies in Singapore need to be audited?

Dormant companies are generally exempt from statutory audit if they have had no accounting transactions and total assets do not exceed S$500,000. They must still maintain accounting records for 5 years and file simplified returns or declarations with ACRA.