Introduction

If your company operates in Singapore, you have a legally binding obligation to retain accounting records for a minimum period—yet many businesses dispose of documents too early or don't realize when longer retention is required.

Non-compliance carries serious consequences under both the Companies Act and Income Tax Act, with penalties recently escalating to S$10,000 for Companies Act violations alone.

The rules vary depending on GST registration status, whether a tax dispute is active, and your company's dissolution status. This guide covers:

- The minimum retention periods mandated by IRAS and ACRA

- Which records and documents are covered

- What triggers extended retention obligations

- How to manage compliance practically

Key Takeaways

- Singapore law requires companies to retain accounting records for 5 years from the relevant Year of Assessment (YA)

- Both IRAS (Income Tax Act) and ACRA (Companies Act) enforce this — non-compliance puts you at risk with two regulators simultaneously

- Retention periods extend beyond 5 years during tax disputes, IRAS audits, or litigation

- Penalties for non-compliance reach S$10,000 under the Companies Act or S$5,000 under the Income Tax Act — plus IRAS can disallow your expense claims entirely

- Enterprise Innovation Scheme records require 7-year retention

The Legal Basis: Singapore's Mandatory Accounting Record Retention Rules

Singapore enforces record retention through two parallel legal frameworks: ACRA requires companies to maintain proper accounting records under the Companies Act 1967, while IRAS mandates retention for at least 5 years from the relevant Year of Assessment under the Income Tax Act 1947 and GST Act 1993.

The Historical 7-Year Rule

Before January 1, 2007, Singapore required a 7-year minimum retention period. The Companies (Act 2 of 2007) reduced this to 5 years. Despite this legislative change, many companies voluntarily maintain 7-10 year retention policies as protection against late audits or to satisfy investor requirements.

How the 5-Year Period Is Calculated

Critical distinction: The Income Tax Act counts 5 years from the Year of Assessment (YA), while the Companies Act counts from the end of the financial year. Getting the starting point right matters — miscalculating it can leave records disposed of too early.

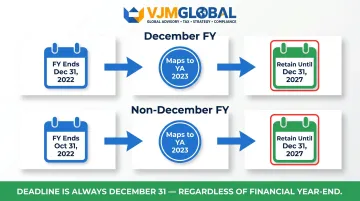

December financial year example:

- Financial year ending December 31, 2022 maps to YA 2023

- Records must be kept until December 31, 2027

- Formula: Retain until December 31 of (YA year + 4)

Non-December financial year example:

- Financial year ending October 31, 2022 maps to YA 2023

- Records must be kept until December 31, 2027

- The retention deadline is always December 31 regardless of your financial year-end date

Once you've established your retention window, the next question is where those records must physically — or digitally — reside.

Where Records Must Be Kept

Records must be stored at the company's registered office address or another location approved by directors. Cloud and electronic storage is fully acceptable—no prior IRAS approval is needed, provided records are:

- Accurate and complete

- Legible and accessible for inspection

- Protected against unauthorized modification

- Retrievable in human-readable format (Excel, CSV, PDF, or Word)

Dissolved or Struck-Off Companies

The 5-year obligation does not end with dissolution. A former officer of a dissolved company must ensure all records are retained for at least 5 years from the date of dissolution. For wound-up companies, the liquidator bears this responsibility.

How Long to Keep Different Types of Accounting Records

The 5-year rule applies broadly, but the specific documents required differ significantly between GST-registered and non-GST-registered companies. This distinction affects both what must be kept and the evidentiary standard IRAS expects during audits.

For GST-Registered Companies

GST-registered businesses face stricter documentation requirements because every input tax claim must be supported by documentation. Missing invoices or payment evidence can lead to IRAS disallowing GST claims during audits.

Required record categories:

Income records:

- Tax invoices and simplified tax invoices issued

- Serially numbered receipts and cash register tapes

- Export documents (bills of lading, air waybills, export permits)

- Credit notes for returns

- Evidence of payment received (bank statements are mandatory)

Purchase and expense records:

- Invoices and receipts for all purchases

- Import documents (bills of lading, import permits, subsidiary import certificates)

- Payment vouchers for services

- Staff remuneration vouchers and CPF contribution evidence

- Rental agreements

Accounting and supporting records:

- General ledgers, journals, sales and purchase listings

- Stock and inventory lists

- Profit & Loss Statements and Balance Sheets

- Fixed asset schedules

- Detailed schedules for public transport, overseas travel, and entertainment expenses

- Records of business goods used for non-business purposes

- Records of disposal of business assets, free gifts, or samples

- Stock removal records from licensed warehouses

- Missing Trader Fraud due diligence documentation

For the comprehensive categorized requirements, reference IRAS's official Record Keeping Guide for GST-Registered Businesses.

For Non-GST-Registered Companies

Non-GST companies have fewer prescribed categories, but IRAS still expects records that can substantiate every income and expense line during a review.

Core records required:

- Invoices received, receipts, vouchers, contracts, and credit/debit notes

- General ledgers and journals covering income, expenses, assets, liabilities, and profits

- CPF contribution records and staff remuneration vouchers (including employee details)

- Expense schedules for public transport, overseas travel, and entertainment — note date, place, amount, persons involved, and business purpose

- Fixed asset schedules recording purchase date, cost, sale date, and sale price, plus any capital allowances claimed

- Bank statements — not legally mandatory for non-GST companies, but critical if IRAS questions cash flow or expense claims

Weak fixed asset records directly affect capital allowance claims. If incorrect allowances are filed without supporting documentation, IRAS treats this as an income tax offense — maintain a fixed asset register with purchase receipts as a minimum baseline.

When the 5-Year Rule Gets Extended

The 5-year minimum is a floor, not a ceiling. Certain legal and practical circumstances require longer retention, and most businesses don't account for them until it's too late.

Active Tax Disputes or IRAS Objections

If your company files an objection to an IRAS assessment or becomes involved in a tax dispute, records must be retained until the dispute is fully resolved—regardless of how many years have elapsed. This can push the effective retention period to 7+ years in complex cases.

During an IRAS or ACRA Audit

If IRAS initiates a compliance review or audit, all records relevant to the period under review must be maintained throughout the process. Companies that disposed of records before an audit commenced may face penalties even if the statutory retention period had already lapsed, as disposal will be treated as non-cooperation.

Enterprise Innovation Scheme - 7-Year Requirement

Under Income Tax Act Sections 37R(24) and 37R(26), records supporting Enterprise Innovation Scheme cash payout claims must be retained for 7 years, not the standard 5. This is the most clearly documented statutory extension.

Internal Policy and Industry-Specific Norms

Companies in regulated industries, those with investors or external auditors, or those with cross-border transactions often adopt internal policies retaining records for 7 or 10 years. For companies with multi-jurisdictional exposure, the statutory minimum rarely reflects actual risk—your retention policy should account for where your obligations extend, not just where your entity is registered.

Risk factors warranting extended retention:

- Multi-jurisdictional tax obligations (particularly USA, UK, or Australian parent companies)

- Ongoing transfer pricing arrangements requiring documentation

- Complex corporate structures with intercompany transactions

- Industries subject to sector-specific audits or regulatory scrutiny

What Happens If You Don't Keep Records for the Required Period

Financial Penalties - Recently Increased

Singapore operates a two-tier penalty framework:

| Statute | First Offense Fine | Imprisonment | Subsequent Offense | Enforced By |

|---|---|---|---|---|

| Companies Act S199(6) | Up to S$10,000 | Up to 12 months | Default penalty | ACRA |

| Income Tax Act S94(2) | Up to S$5,000 | Up to 6 months (in default of payment) | N/A specified | IRAS |

| GST Act S46(6) | Up to S$5,000 | Up to 6 months | S$10,000 and/or up to 3 years | IRAS |

Note that these figures reflect recent legislative changes: the Companies Act penalty rose from S$5,000 to S$10,000 (Act 24 of 2025, effective May 6, 2026), and the Income Tax Act fine increased from S$1,000 to S$5,000 (Act 27 of 2021).

Operational Consequences - Usually More Damaging Than the Fines

When records are absent or insufficient, IRAS can exercise "best judgement" to estimate your company's revenue, which typically results in:

- Disallowed expense claims and capital allowance deductions

- Rejected GST input tax claims

- Export sales reclassified as local supplies subject to 9% GST

- Significantly higher tax bills than actual liability

Definition of Improperly Kept Records

IRAS considers records "improperly kept" in three situations:

- No source documents or accounting ledgers were ever created

- Records existed but were disposed of before the minimum retention period ended

- Records exist but are disorganized or inaccessible, preventing IRAS from verifying transactions

Records that exist but cannot be produced in a legible, organized format during an audit carry the same penalties as records that were never kept.

Best Practices for Managing Record Retention in Singapore

Establish a Clear Retention Schedule

Map your financial year end to the YA calendar and set firm internal review dates. For example:

- Schedule an annual records audit each January

- Confirm which YA records have passed the 5-year mark

- Verify no active disputes or audits prevent disposal

- Document disposal decisions for audit trail purposes

Sample retention schedule (December financial year end):

| Financial Year End | Maps to YA | Safe Disposal Date | Check Before Disposal |

|---|---|---|---|

| Dec 31, 2022 | YA 2023 | Dec 31, 2027 | No active audits/disputes? |

| Dec 31, 2023 | YA 2024 | Dec 31, 2028 | No active audits/disputes? |

Adopt a Digital-First Record-Keeping System

Cloud-based accounting software enables automated transaction tracking, document storage, and audit-trail preservation. IRAS maintains an Accounting Software Register Plus (ASR+) listing software that fulfills compliance requirements.

Benefits of electronic record-keeping:

- Eliminates need to retain physical copies of most source documents

- Automatic date/time stamps create tamper-proof audit trails

- Searchable records reduce retrieval time during audits

- Remote access enables compliance verification from any location

- Integration with e-commerce platforms (Amazon, Shopify, Etsy) ensures automatic transaction recording

VJM Global uses cloud-based systems, automation tools, and AI-assisted workflows when supporting foreign clients with Singapore accounting compliance — ensuring records meet IRAS's integrity, completeness, accuracy, availability, and reliability standards.

Storing records well is only half the equation. Once records pass their retention date, disposing of them correctly is equally important.

Establish Secure Disposal Procedures

Once records pass their retention date and no active disputes or audits exist, Singapore's Personal Data Protection Act (PDPA) requires proper disposal.

Disposal procedures:

- Physical documents: Professional shredding services with certificate of destruction

- Digital records: Permanent deletion or certified data destruction methods (not just moving to trash/recycle bin)

- PDPA compliance: Section 25 requires disposal of personal data once retention purpose expires

Key compliance conflict: Tax law requires retention for 5 years, but PDPA requires disposal once that obligation lapses. Holding onto personal data indefinitely — without legal justification — violates privacy law.

Frequently Asked Questions

How long do you need to keep accounting documents in Singapore?

The minimum retention period is 5 years from the relevant Year of Assessment (YA), as required by both IRAS and ACRA. This period extends if your company is involved in a tax dispute, IRAS audit, or litigation. Enterprise Innovation Scheme records require 7-year retention.

What is the record retention law in Singapore?

Two statutes govern record retention in Singapore: the Companies Act 1967 (enforced by ACRA) and the Income Tax Act 1947 / GST Act 1993 (enforced by IRAS). Both independently require a minimum 5-year retention period, with penalties up to S$10,000 for non-compliance.

What is the 7-year retention policy?

Singapore reduced its statutory minimum from 7 years to 5 years on January 1, 2007. Some companies still voluntarily maintain a 7-year policy for protection against late audits, investor requirements, or to align with parent company standards in jurisdictions like the United States.

Does the 5-year rule still apply if a company is dissolved or struck off in Singapore?

The obligation survives dissolution. A former officer must keep all records for at least 5 years from the date of dissolution; for wound-up companies, the liquidator holds this responsibility. Ceasing operations does not end the retention requirement.

Can accounting records be kept in digital or electronic format in Singapore?

Yes — IRAS accepts electronic records without prior approval, provided they are accurate, legible, and protected against unauthorized modification. Physical copies are not required if digital equivalents meet these standards and can be retrieved in Excel, CSV, PDF, or Word format upon request.